Hello again. Here’s my latest quarterly portfolio review.

After lagging behind global markets in the first quarter, I was a little ahead in both the second and the third. Year-to-date, both my portfolio and the global market tracker I benchmark against are up around 12.5%.

| Portfolio / Benchmark | Q3 2021 | Q2 2021 | Q1 2021 | Annualised since Jan 2018 |

|---|---|---|---|---|

| My portfolio | +2.4% | +7.9% | +1.8% | +11.5% |

| Vanguard FTSE Global All Cap (fund) | +1.2% | +6.9% | +4.0% | +10.8% |

| Vanguard LifeStrategy 60 (fund) | +0.8% | +4.5% | +0.9% | +6.8% |

| Vanguard UK All-Share Index (fund) | +2.2% | +5.6% | +5.7% | +2.7% |

The usual explanatory note: I use the Vanguard global tracker fund as my main benchmark. The more conservative LifeStrategy 60 fund (essentially a global 60% equity/40% bond portfolio) and UK index tracking fund provide additional reference points.

Annualised since January 2018, I’m up 11.5% compared to 10.8% for global markets. That means I’m a little shy of my +2-3% a year stretch target, but I’m still pretty happy with my overall progress.

Bond yields have started to rise again in the last few weeks. While they were falling, roughly from mid-May to early August, my quality-type investments (the likes of Fundsmith, Lindsell Train etc) put in a decent showing again. At the risk of over-analysing, that’s probably why I outperformed a little in the second and third quarters.

Markets have been pretty skittish for the last couple of weeks, even though the rise in bond yields has been both smaller and more gentle than we saw earlier this year.

That said, 2021 has certainly been unusual in that we’ve seen no major market decline of 10% or more. In fact, I’m not even sure we’ve had a 5% drop. On average, as stock market historians often tell us, we should probably expect to see a 10% fall around once a year.

After its late spurt at the end of 2020, the UK market was only marginally ahead of global markets this year at 14%. Scooting around some other major markets, the US was up 15%, Europe 12%, Japan 6%, and China was down 16%. Among the smaller markets, both India and Russia posted returns in excess of 30%.

Not so great expectations

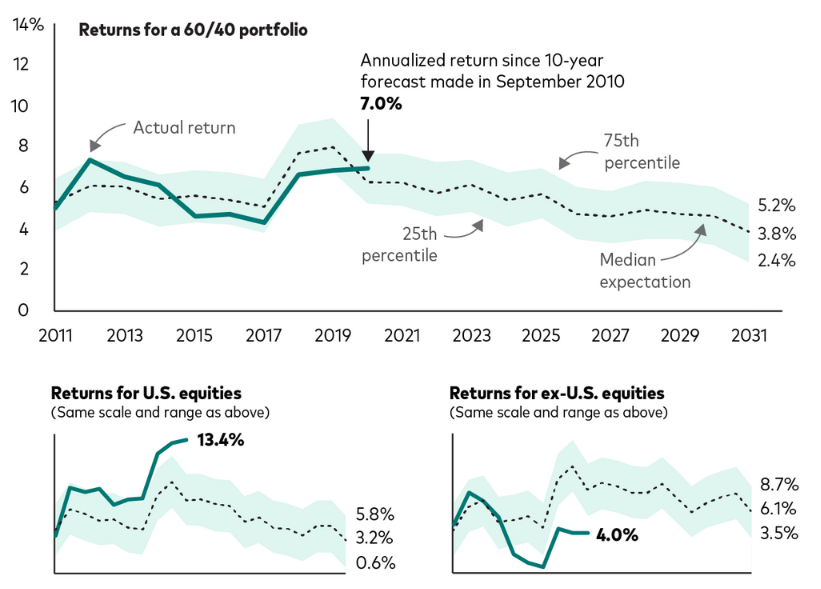

Trusts4U tweeted an interesting piece from Vanguard recently where the fund giant looked at how its market forecast model had performed over the last ten years and what it is suggesting about future potential returns:

It’s no surprise to see that US equities did a lot better than Vanguard expected over the last 10 years and that non-US equities did much worse. When it comes to the 60/40 portfolio, these two effects net off, however.

From its lower base, Vanguard expects non-US equities to perform better over the next ten years but its mid-point prediction is an anaemic-looking 6% a year. Its mid-point prediction for the 60/40 is just 3.8%, well below the 7.0% enjoyed over the last decade.

Lower forward expectations are something I have mentioned occasionally so none of this is new information but I thought it was a useful way to present such data. And the folks at Vanguard deserve credit for highlighting the accuracy or otherwise of their old forecasts.

My trading

It was another quiet quarter for me on the trading front.

I took part in an open offer for Bluefield Solar Income a few months ago, topped up International Biotechnology Trust after its discount widened out, and added some non-ISA dividends to my Vanguard All-World ETF.

I’ve still got a few non-ISA positions that I’d like to tidy up a bit over the next few years and the introduction of the extra 1.25% dividend tax last month serves as another good reason for doing so.

Acorn Income, one of my UK small-cap holdings, has decided to fall on its sword after initially proposing a complete mandate change to a global sustainable equity income strategy. I think it’s a sensible decision, given the trust’s size and its overly complicated structure.

I have two options with this shareholding. I can either roll my holding over into Unicorn UK Income, an open-ended fund run by the same managers, or cash out close to net asset value. I will probably choose the latter and when the distribution is made in mid-November I will need to decide where to put it. Currently, I’m thinking of topping up several holdings, most likely my three biotech/healthcare trusts, Gresham House Energy Storage, and Keystone Positive Change.

Crypt-oh!

I’ve been a casual observer of cryptocurrencies for a few years, alternatively shaking and scratching my head. But in common with a number of other financial bloggers, this has been the year when I finally decided to take the plunge, albeit in a very limited way.

I now have a small position in a crypto company called KR1. It’s been around since 2016 and is invested in several dozen crypto assets, often getting into some very early-stage projects thanks to the connections it has built up. Its management team own a significant number of its shares and they have just signed a long-term incentive deal that could see their stake go much higher. This blog post by Wexboy from November 2020 covers the company in some detail, although many of the figures are obviously quite dated.

KR1 trades on the Aquis Stock Exchange, which means that although you can put it into an ISA, the level of regulation and disclosure is a lot lower than the main London market. What’s more, there’s no up-to-date portfolio listing meaning you have to piece together what it owns from its individual announcements. It also has an annoying habit of not publishing its December year-end results until 30 June and June half-year results until 30 September. In other words, it’s very much buyer beware.

As of last night, its portfolio of crypto assets was worth in the region of £275m and its market cap was £223m however there are a significant number of shares yet to be issued (just over 30% of the current share count if my back of the envelope maths is correct) in respect of the performance fees for 2020 and 2021 and for options yet to be exercised.

That means it is probably trading at a premium of around 10% to its net asset value but this figure shifts around quite a lot, as you might imagine. When I looked again this morning, the portfolio value had dropped to £260m and it’s been as high as £320m and as low as £100m even in the short time that I have owned it.

Under its new management arrangements, fees of 1.9% are payable up to £250m of net assets and 1.7% above that level with 20% of any gains paid out as a performance fee entirely in new shares. That’s very expensive compared to most funds, being more in line with fee structures for private equity or hedge funds.

I’ve only been invested in it for a few months and I very much see this as a learning position (I’m working my way through The Basics Of Bitcoins and Blockchains for example) combined with an experiment as to how much volatility I can live with. Crypto price falls can be savage, with 25% daily or overnight drops a regular occurrence and numerous 80-90% drawdowns over the last decade. While the KR1 share price has been less volatile than crypto prices and the value of its own portfolio in recent months, it’s the most speculative position I hold right now.

It’s included in my overall portfolio returns, hence the reason I’ve mentioned it here, although it’s my smallest position by some distance.

Performance by holding

Here’s how my individual holdings have performed so far this year and in 2020. The names link to my most recent review of each holding.

| Holding | End of Q3 2021 | 2020 |

|---|---|---|

| Acorn Income | +35.7% | -14.1% |

| HgCapital | +30.0% | +21.6% |

| RIT Capital Partners | +25.5% | -0.4% |

| Baronsmead Venture Trust | +22.0% | +6.2% |

| BlackRock Smaller Companies | +19.7% | +4.1% |

| JPMorgan Global Growth & Income | +18.4% | +15.9% |

| Henderson Smaller Companies | +18.3% | -0.6% |

| Gresham House Energy Storage | +15.9% | +10.8% |

| Fundsmith Equity | +13.3% | +18.4% |

| Vanguard All-World ETF | +12.6% | +12.2% |

| BB Healthcare | +12.5% | +29.1% |

| Smithson | +9.2% | +31.7% |

| Keystone Positive Change | +4.4% | -0.8% |

| Lindsell Train Global | +2.9% | +11.9% |

| Bluefield Solar Income | -0.5% | -2.5% |

| HICL Infrastructure | -0.7% | +7.0% |

| Worldwide Healthcare | -2.3% | +19.9% |

| International Biotechnology | -8.3% | +35.6% |

It’s been a good year for UK smaller companies with Acorn, Baronsmead, BlackRock, and Henderson all in the upper echelons of my chart. The discount on Acorn Income has narrowed because a cash exit is in sight, which is why it’s at the very top of the pile.

My long-term holdings in HgCapital and RIT have both done very well this year. For Hg, it’s merely a continuation of the last few years while RIT has spent some time in the doldrums so it’s good to see it bounce back, especially considering Lord Rothschild has officially retired as Chairman after running the trust for such a long time.

In the battle of the quality managers, it’s another year where Terry Smith has outboxed Nick Train and Michael Lindsell. Fundsmith has done better than Smithson, too. This looks like being the third year on the trot that Lindsell Train Global Equity has lagged its benchmark, although it wasn’t that far behind in both 2019 or 2020, and it’s level with world markets over the past five years. I don’t expect Lindsell Train to make any major changes to its strategy and I’m happy to sit tight for now.

Keystone has bounced back a little after Baillie Gifford took over at probably the worst possible time for its style of investing in February of this year. At the end of August, it had nearly 13% of its assets in Moderna so that’s something to keep an eye on. Moderna has more than trebled this year, making it by far the best performing stock in the S&P 500, but it fell heavily on 1st October after Merck announced positive results for its COVID pill. Keystone has lagged Scottish Mortgage over the last six months but is well ahead of Baillie Gifford US Growth, Monks, and Edinburgh Worldwide.

It continues to be a difficult year for healthcare stocks and for biotech in particular. BB Healthcare has done alright but both Worldwide Healthcare and International Biotechnology are in negative territory although they have done a lot better than sector rivals Syncona and Biotech Growth.

It’s a similar mixed story for my renewables and infrastructure holdings with Gresham House Energy Storage striding ahead but HICL and Bluefield largely flat. Bluefield’s interims this week will make very interesting reading given what is going on with energy prices as it sells the power it produces on fixed-price contracts for the 12 to 24 months. HICL is probably the position I have the least conviction in here but I’m in no rush to make any rash decisions.

Caledonia, which I sold out of in March/April, is up just under 20% year to date but I’ve taken it out of the performance table. KR1, being a tiddler of a position, is also left out for the time being but it’s up a few hundred per cent this year, all before I bought it naturally!

You can read my fund profiles at Money Makers

I’ve been busy writing fund profiles over at Money Makers these past few months with recent pieces on the likes of Baillie Gifford US Growth, Supermarket Income REIT, Montanaro European Smaller, and Law Debenture to mention just a few. I’ve also published updated pieces on Fundsmith Equity, HgCapital, and Lindsell Train Investment Trust.

Here is the sign-up page that provides full details of what you get as a paying member of Money Makers.

Until next time…

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Excellent article as ever.

Do you rebalance your portfolio or let your winners run?

Hi there,

I stumbled across your work tonight after reading Personal Asset Trusts quarterly report and wondering what happened to Robin Angus then finding your article on PAT.

I wanted to say what I’ve read I’ve thoroughly enjoyed and feel like we have a rather similar outlook on investing although I’ve largely watched from the sidelines until now.

I’m now looking to make some investments shortly so will be subscribing to ensure I’m viewing all your posts!

Thanks, Liam. That’s very nice to hear 🙂 Best of luck with your investing exploits.

Hi Peter, I rarely sell things to rebalance but I might do when position sizes for a trust or a theme feel like they are getting a little too large. I did that with HGT a few years ago, and it turns out I would have better staying put, so far anyway. I tend to rebalance, in a fashion, when reinvesting dividends or adding new money.

Do you know the returns of the S&P 500 and Nasdaq 100 over the same periods?

Thanks

Using the UK-based ETFs (CNX1 for Nasdaq and IUSA for the S&P) I’m seeing 15.8% as of 30 Sep 2021 for the Nasdaq and 17.3% for the S&P. So that includes any currency effects and the underlying ETF costs for UK-based investors.

The dollar-based index returns were a percentage point or so lower it would seem:

https://www.nasdaq.com/articles/september-third-quarter-2021-review-and-outlook-2021-10-01