On 1 November 2020, the UK’s largest fund, Fundsmith Equity, will celebrate its tenth birthday. A fair amount about this fund has changed over the past decade but a lot more has stayed the same.

I’ve long been a fan of Terry Smith and Fundsmith’s no-nonsense approach to investing.

Indeed, a copy of Smith’s 1992 book, Accounting For Growth, is sitting on the shelf above me, admittedly alongside plenty of less serious titles.

How Fundsmith Equity invests

As its factsheet states, Fundsmith Equity is, “just a small number of high quality, resilient, global growth companies that are good value and which we intend to hold for a long time, and in which we invest our own money“.

Smith has also described its investment process as “not seeking tomorrow’s winners, but looking for companies that have already won”.

There’s an even shorter version that goes:

- Buy good companies

- Don’t overpay

- Do nothing

Despite liking this approach to investing, I didn’t buy into Fundsmith Equity until the start of 2018.

Those who took the plunge earlier will have done substantially better, potentially even quintupling their money.

How Fundsmith started

Smith, then 57, set up Fundsmith with several colleagues in 2010 after a successful and often controversial City career.

Fundsmith Equity was the first fund the company launched and Smith reportedly put in £25m of his then £60m fortune.

Last year’s Sunday Times Rich List reckoned Smith was worth £300m and I suspect that number is now significantly higher.

Fundsmith’s approach was influenced by the style and success of the pension scheme of Tullett Prebon, the inter-dealer firm where Smith was CEO. This held around 20 companies for several years, rarely buying or selling, and generated an average annual return of about 14%.

Since 2010, a Luxembourg-based and a sustainable version of Fundsmith Equity have both been launched, as have two investment trusts that focus on emerging markets and global smaller companies.

But Fundsmith Equity remains Fundsmith’s main fund by some distance.

Let’s look at how it has evolved over the last decade…

First, what hasn’t changed

The fund’s management fees have stayed at the same percentage of net assets throughout, despite its enormous growth in size.

According to the first factsheet in November 2010, the fund’s assets were £39m.

As of 30 September 2020, they were £21.6bn, over 500 times greater.

The annual management charge for the I class has remained at 0.9%, the T class 1.0%, and the R class 1.5%.

About 80% of investors’money resides in the cheapest I class with just 2% in the most expensive R class.

When Fundsmith launched, a couple of years before the Retail Distribution Review shook up fund charges, 0.9% a year looked pretty reasonable. But that’s not the case today.

Fortunately, the fund’s other operating expenses have benefited from economies of scale over the past decade. The ongoing cost figure for the I class has come down from 1.15% to 0.95%.

As Smith often points out, the low level of buying and selling within Fundsmith Equity means its total costs including transaction charges compare very favourably with most other popular open-ended funds.

While that’s true, other successful firms, notably Lindsell Train and Baillie Gifford, have repeatedly lowered their management fees as their funds have grown in size.

Lindsell Train Global, with £8bn of assets, has ongoing charges of 0.5% for its cheapest units. The £15bn Scottish Mortgage comes in at 0.35%.

Having got my main grouch out of the way, let’s look at how the fund’s top ten holdings have changed:

Fundsmith Equity’s top holdings

| Position | Mar 2011 | Dec 2011 | Dec 2012 | Dec 2013 | Dec 2014 |

|---|---|---|---|---|---|

| 1 | InterContinental Hotels | Becton Dickinson | Reckitt Benckiser | Stryker | Microsoft |

| 2 | Domino’s Pizza | L’Oreal | Dr Pepper Snapple | Microsoft | Dr Pepper Snapple |

| 3 | Microsoft | Nestle | Stryker | Domino’s Pizza | Stryker |

| 4 | Reckitt Benckiser | InterContinental Hotels | Imperial Tobacco | Dr Pepper Snapple | Becton Dickinson |

| 5 | Nestle | Microsoft | Domino’s Pizza | Reckitt Benckiser | Imperial Tobacco |

| 6 | Imperial Tobacco | Unilever | ADP | Becton Dickinson | Unilever |

| 7 | Schindler | Stryker | InterContinental Hotels | InterContinental Hotels | Kone |

| 8 | Becton Dickinson | Imperial Tobacco | Becton Dickinson | Unilever | Reckitt Benckiser |

| 9 | Dr Pepper Snapple | Procter & Gamble | Microsoft | 3M | Philip Morris |

| 10 | 3M | PepsiCo | Unilever | Imperial Tobacco | Domino’s Pizza |

| Position | Dec 2015 | Dec 2016 | Dec 2017 | Dec 2018 | Dec 2019 | Sep 2020 |

|---|---|---|---|---|---|---|

| 1 | Microsoft | Microsoft | PayPal | PayPal | Microsoft | Microsoft |

| 2 | Sage | Amadeus | Amadeus | Microsoft | PayPal | PayPal |

| 3 | Imperial Tobacco | Stryker | Microsoft | Amadeus | Philip Morris | |

| 4 | Dr Pepper Snapple | CR Bard | Novo Nordisk | Novo Nordisk | Estee Lauder | Idexx |

| 5 | Philip Morris | IDEXX | Dr Pepper Snapple | Waters | Novo Nordisk | |

| 6 | PepsiCo | PepsiCo | Waters | Reckitt Benckiser | Amadeus | Philip Morris |

| 7 | Amadeus | PayPal | CR Bard | PepsiCo | Novo Nordisk | Intuit |

| 8 | Stryker | InterContinental Hotels | InterContinental Hotels | Intuit | Stryker | Estee Lauder |

| 9 | CR Bard | Dr Pepper Snapple | Stryker | Stryker | McCormick | McCormick |

| 10 | Johnson & Johnson | Philip Morris | Philip Morris | Philip Morris | Intuit | L’Oreal |

The initial list of top ten holdings was published in the factsheet for March 2011, which is why the first column isn’t headed December 2010.

Microsoft seems to be the only company that’s been ever-present in Fundsmith Equity’s top ten, although I guess it may have dropped out for a short time mid-year during 2012 or 2013.

It may seem like an obvious choice now, but Microsoft’s share price barely moved from 2001 to 2013 and it was only when Satya Nadella took over the role of CEO in 2014 that investors seemed to regard it as a growth story once more.

Fundsmith was early to the Office party. Microsoft’s share price was around $26 when the fund launched. It’s now over $200 and I suspect it’s made more money for Fundsmith Equity holders than any other company.

Although Fundsmith also has a large stake in Facebook, the other big tech stocks — Apple, Amazon, and Alphabet — are notable by their absence as are Chinese stocks like Tencent and Alibaba.

Low return on capital employed, a key yardstick used by Fundsmith, is often cited as the main reason for their exclusion and there are other rationales given near at the end of this article on Seeking Alpha.

However, Microsoft and Facebook don’t seem to have a significantly higher return on capital employed and I would have thought Apple, Amazon, and Alphabet are classic examples of “companies that have already won”.

Many firms appear multiple times in Fundsmith Equity’s top ten over the years, most notably Stryker, Amadeus, Becton Dickinson, InterContinental Hotels, PayPal, PepsiCo, Reckitt Benckiser, and Philip Morris.

And a number of former top ten positions are still held in the portfolio. At the end of 2019, the following still represented position sizes of around 3-4%:

- InterContinental Hotels

- Reckitt Benckiser

- Becton Dickinson

- PepsiCo

- ADP

- Kone

- Unilever

- Sage

- Amadeus

- Stryker

- Waters

Fundsmith Equity’s sells

The vast majority of Fundsmith Equity’s monthly portfolio commentaries begin with, “there were no outright sales or purchases of holdings made in the month”.

But a couple of companies a year, on average, have been sold over the last decade.

For the first year or so, the identities of companies sold weren’t disclosed but Fundsmith now tells us when it sells out completely of a position and why it has done so.

Here are the sales I found from scouring the factsheets:

- SGS (Aug 2012)

- Serco (Feb 2013)

- Sigma-Aldrich (Jun 2013)

- Schindler (Jun 2013)

- McDonald’s (Jul 2013)

- Waters (Oct 2013)

- Swedish Match (May 2014)

- CDK Global (Nov 2014)

- Invidior (Dec 2014)

- Choice Hotels (Jun 2015)

- Domino’s Pizza, Inc (Nov 2011 and Oct 2015)

- Ebay (Oct 2015)

- Procter & Gamble (Jan 2016)

- JM Smucker (Jul 2017)

- Imperial Tobacco (Nov 2017)

- CR Bard (Dec 2017)

- Dr Pepper Snapple (Feb 2018)

- Nestle (Jun 2018)

- Colgate-Palmolive (Jan 2019)

- 3M (Sep 2019)

- Clorox (Apr 2020)

Some of these sales were unwanted stakes demerged from larger holdings, such as CDK Global and Invidior. The former subsequently found its way into Smithson’s portfolio only to be sold from that within a year.

And while Ebay was sold in 2015, the demerged stake in PayPal was retained and has since become one of the portfolio’s largest positions.

CR Bard was bought by Becton Dickonson, another Fundsmith holding.

But the majority of sales over the last decade were put down to a perceived deterioration in quality, due to factors like a questionable acquisition or a major strategy change.

Waters was sold in 2013 due to concerns about its low growth. But it made its way back into the portfolio later on and even became a top-ten position again.

Some of these sales look very good with hindsight, notably Serco and Imperial Tobacco (now Imperial Brands) which are both trading at a much lower price. Quite a few others have just trodden water since Fundsmith sold out.

However, a few like McDonald’s, Nestle, and Procter & Gamble have made decent progress since they left the portfolio.

The Sigma-Aldrich sale was unfortunately timed as it was bought out by Merck at a 75% higher price just over a year later.

The US-listed version of Domino’s Pizza is notable for having been sold twice. As Andrew at Fund Hunter pointed out to me recently, it’s probably the worst sell decision Fundsmith has made.

The first time Domino’s was sold was after a 100% gain in the first year of the fund’s life. It was repurchased when the valuation looked more reasonable but then cut loose once more in 2015, again on valuation concerns.

The original/repurchased Domino’s stake probably rose several times in value but its shares have quadrupled since the fund last sold out.

Commenting in Fundsmith’s 2015 report, Smith said:

We sold our holding in Domino’s Pizza during the year since it had reached a valuation which we felt was only justifiable if the current rapid rate of growth is sustainable, which we would doubt. However, we sold it with some regret and trepidation. Regret since it is undoubtedly a fine business and had been our best performing share since the inception of our Fund. Trepidation since selling shares in good companies is something we are justifiably reluctant to do. Still, we believe that you ‘make money with old friends’ which is to say that we would be keen to own Domino’s again if the opportunity arises at a valuation which we regard as at least reasonable.

Since Domino’s was sold, valuation rarely seems to have been cited as a reason for a sale so perhaps there was a lesson learned here?

How Fundsmith Equity has grown

| Metric | Dec 2010 | Dec 2011 | Dec 2012 | Dec 2013 | Dec 2014 | Dec 2015 |

|---|---|---|---|---|---|---|

| Size (£bn) | 0.06 | 0.2 | 0.8 | 1.6 | 3.0 | 4.6 |

| New money (£bn) | n/a | 0.1 | 0.5 | 0.5 | 0.9 | 1.0 |

| 1-year return | # 6.1% | 8.4% | 12.5% | 25.3% | 23.3% | 15.7% |

| 1-year MSCI World | # 7.3% | -4.8% | 10.7% | 24.3% | 11.5% | 4.9% |

| Since inception | 6.1% | 15.0% | 29.4% | 62.2% | 100.0% | 131.4% |

| Portfolio turnover | 5.0% | 12.9% | -0.2% | 0.2% | Negative | Negative |

| 7-day liquidity | n/a | n/a | 70% (2-day) | 74% (4-day) | 85% | 84% |

| Metric | Dec 2016 | Dec 2017 | Dec 2018 | Dec 2019 | Sep 2020 |

|---|---|---|---|---|---|

| Size (£bn) | 9.1 | 13.4 | 15.8 | 18.8 | 21.6 |

| New money (£bn) | 2.6 | 1.8 | 2.1 | -1.4 | -0.5 |

| 1-year return | 28.2% | 22.0% | 2.2% | 25.6% | * 13.5% |

| 1-year MSCI World | 28.2% | 11.8% | -3.0% | 22.7% | * 4.2% |

| Since inception | 196.6% | 261.7% | 269.6% | 364.4% | 427.0% |

| Portfolio turnover | Negative | Negative | 5.4% | 13.4% | -4.1% |

| 7-day liquidity | 72% | 68% | 69% | 57% | 64% |

# = 2-month return, * = 9-month return

New money is a figure that I have calculated as a rough estimate of the cash that flowed into the fund that year. It’s the net increase in fund size less the gain for that year (based on the average of the starting and closing fund size).

The apparent outflow in 2019 is somewhat misleading, though. I believe about £2bn was taken out the fund’s numbers in April of that year due to a reorganisation that saw the Luxembourg version of the fund (SICAV) being reported separately.

The SICAV version of Fundsmith now has over €5bn in assets. Add in Smithson, Fundsmith Emerging Equities, and Fundsmith Sustainable Equity, and Fundsmith’s total retail assets under management are nearly £30bn and therefore generate nearly £300m in annual management fees!

Defining turnover and liquidity

A couple of definitions may help with the final two rows of this table.

Portfolio turnover “has been calculated in accordance with the methodology laid down by the FCA. This compares the total share purchases and sales less total creations and liquidations with the average net asset value of the fund”.

Somewhat confusingly, this definition can create a negative figure. Indeed, it often has in the case of Fundsmith due to the heavy fund inflows it tends to have.

7-day liquidity “is calculated based upon 30% of trailing 20-day average volume”.

So, this measures the ‘Woodford’ factor. If the fund had to redeem a lot of money to investors, this gives you an indication of how quickly it could that.

That’s the theory anyway. In practice, mass redemptions are more likely to occur when everyone is panicking and it will be more difficult to sell.

As often with these things, it’s the trend in the numbers that is probably more useful, rather than the number itself.

Fundsmith Equity’s returns

Fundsmith marginally trailed the market in the two months to December 2010 but it’s beaten it in every calendar year since.

Barring a major reversal, 2020 should be another year of decent outperformance.

I’d say that it’s the fund’s consistency that is more impressive than its outperformance.

In five calendar years, Fundsmith outperformed by a few percentage points or less. But in the four others (2011, 2014, 2015, and 2017), it’s notched up a win of over 10 percentage points.

2020 could become the fifth 10-pointer, although it’s a little below that level at the moment.

This consistency adds up. As of September 2020, Fundsmith Equity was up 427% since it launched while the MSCI World Index rose 192%.

Portfolio turnover has remained low

Although I’ve included portfolio turnover from Fundsmith’s factsheet, the odd way which the FCA calculates it doesn’t seem to be particularly helpful here.

As we’ve seen, Fundsmith seems to buy and sell around two holdings a year, probably representing 5-8% of its portfolio by value, so its turnover is much lower than most funds.

In terms of transaction charges, Fundsmith paid around £2.5m in 2019 and £6.5m in 2018, which is tiny compared to the £15bn average fund size over those two years.

Dealing spreads for most of Fundsmith’s investments are also very tight and stated to be just 0.05% of asset value.

But liquidity has decreased over time

Plenty of pundits have suggested the sheer size of Fundsmith could be limiting its investment options.

Terry Smith has been fairly dismissive of such concerns, pointing out that many US funds that invest in similar companies to Fundsmith are significantly larger.

A 5% position size in the Fundsmith portfolio, normally enough to secure a top ten holding, now represents an investment of more than £1bn.

Looking across all of Fundsmith’s 29 current holdings, I reckon the average stake they own is just over 2%. Their holdings in Microsoft, PayPal, and Visa, for instance, are all well under 1% of those companies’ total share capital.

The average company size of Fundsmith investments has risen from £41bn in 2012 to £142bn in 2020. Microsoft probably accounts for a lot of that increase, though. At £1.2 trillion, the average would likely fall to £100bn if it was excluded.

There are several companies where I believe Fundsmith owns more than 3%:

| Company | % of shares held by Fundsmith |

|---|---|

| InterContinental Hotels | 9.0% |

| Sage | 7.8% |

| Intertek | 7.2% |

| Waters | 6.3% |

| McCormick | 6.1% |

| IDEXX | 5.0% |

| Brown-Forman | 3.2% |

The top three are all UK-listed. Sage and InterContinental are valued at around £8bn while Intertek is £10bn.

Fundsmith’s list of investing opportunities is definitely shrinking. Whether it is shrinking enough to have a discernible impact on performance is hard to tell.

The US-listed Domino’s Pizza, for example, was worth around £5bn when Fundsmith sold out, so its relatively small size may have also been part of the reason it was cut loose.

It’s around £13bn today, so if it found its way back into the portfolio for a third time, it would certainly be one of the smallest companies Fundsmith held.

I think there about 1,000 listed companies larger than Domino’s and probably around 500 valued at £25bn or more. In theory, this should be a deep enough pond to fish in, even for someone as picky as Fundsmith.

The measure provided by Fundsmith, 7-day liquidity, has declined from 85% in 2014 to 64% today. While that still seems pretty decent, I don’t have much to compare it to and the direction of travel is pretty clear.

So, liquidity is one area that I will be watching over the next few years.

One thing that could happen to stop the fund getting too big is that it could be closed to new investors or even new money entirely. I think we’re a few years away from that being considered but we have to see how things play out.

It’s certainly a topic that’s not going to go away and we’ll have to see how Fundsmith’s commentary on this evolves.

Portfolio breakdown

Here are some further stats on the portfolio and the mix of sectors Fundsmith is invested in:

| Metric | Dec 2010 | Dec 2011 | Dec 2012 | Dec 2013 | Dec 2014 | Dec 2015 |

|---|---|---|---|---|---|---|

| Average company founded | n/a | n/a | 1902 | 1901 | 1907 | 1908 |

| Number of holdings | 22 | 24 | 28 | 25 | 27 | 28 |

| Average company size (£bn) | n/a | n/a | 41 | 52 | 58 | 60 |

| US % | n/a | 55% | 60% | 61% | 60% | 58% |

| Technology % | n/a | 9% | 11% | 15% | 23% | 24% |

| Healthcare % | 15% | 17% | 17% | 17% | 18% | 22% |

| Consumer staples % | 62% | 49% | 44% | 45% | 39% | 38% |

| Consumer discretionary % | 5% | 5% | 13% | 13% | 9% | 3% |

| Metric | Dec 2016 | Dec 2017 | Dec 2018 | Dec 2019 | Sep 2020 |

|---|---|---|---|---|---|

| Average company founded | 1912 | 1916 | 1922 | 1925 | 1928 |

| Number of holdings | 29 | 28 | 28 | 28 | 29 |

| Average company size (£bn) | 69 | 84 | 92 | 114 | 142 |

| US % | 64% | 62% | 64% | 66% | 68% |

| Technology % | 25% | 28% | 31% | 30% | 29% |

| Healthcare % | 26% | 28% | 25% | 24% | 23% |

| Consumer staples % | 35% | 28% | 27% | 32% | 30% |

| Consumer discretionary % | 4% | 4% | 3% | 3% | 7% |

The median age of the companies Fundsmith invests in has got noticeably younger. The addition of young upstarts like Facebook and PayPal to the portfolio in recent years will have played a part here. I’d expect to see this number continue to rise.

The number of holdings has been in the high 20s for several years now. Fundsmith says it will generally own 20-30 stocks but if the fund continues to grow in size, I wouldn’t be surprised to see the upper limit rise to, say, 35.

The US holdings have become more significant over time, as has the weighting toward technology and healthcare, although the latter has fallen off a little in the last few years. The consumer staples sector has seen the largest decline.

We’ve seen that sector shift already in the way the top ten holdings have evolved, with consumer goods firms sliding down the list and the latest top three consisting of Microsoft, PayPal, and Facebook.

While a lot of this change has come from Fundsmith Equity’s buy and sell decisions, I suspect a fair amount has also been due to just letting its existing positions ride.

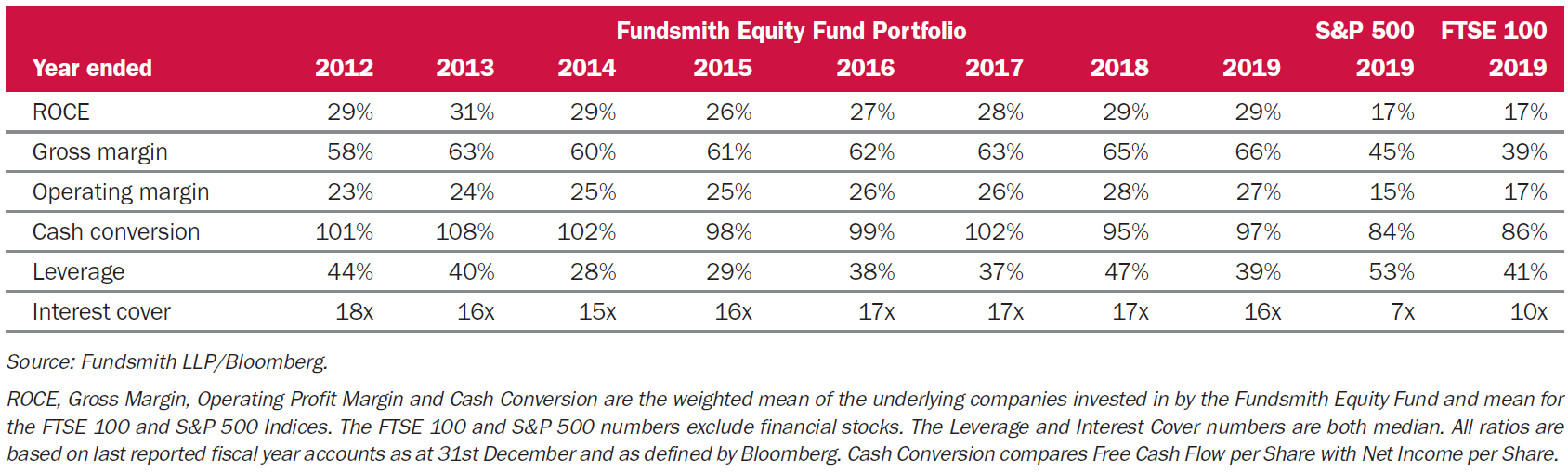

Feel the quality

Here’s the table Fundsmith produces that shows the underlying characteristics of its holdings relative to the US and UK market:

In short, Fundsmith companies have better profit margins, better cash flow, and lower debts. This all helps them produce a much higher return on capital employed.

Margins have crept higher over the past decade while cash conversion has got a little worse, but not much else has changed.

I think Fundsmith started producing this table in 2014 and the figures for both the S&P and FTSE 100 haven’t changed much either. However, cash conversion seems to have improved a little in both the US and the UK, while US companies have become a bit more indebted.

What’s in store for decade #2?

Even the most ardent Terry Smith fan probably wouldn’t have predicted it would end its first decade up more than five times and with well over £20bn in assets.

As of 30 September 2020, Fundsmith has produced an annualised return of 18.2%, far greater than the 11.4% a year from the MSCI World Index.

Fundsmith Equity has also beaten the 15.3% per year return in sterling that a US index tracker would have given you over the last decade.

It does, however, trail the Nasdaq 100, which has returned around 22% a year over the last decade. But then so does pretty much every other fund you can think of!

It’s pretty hard to imagine any of these annual return figures being as good in Fundsmith’s second decade.

I still reckon Fundsmith Equity will beat global market indices but I suspect the difference will be narrower.

As mentioned earlier, fund size/liquidity does look it is becoming more of an issue although there are steps Fundsmith can take to address this. I’d trust Fundsmith to act in good time but I’ll still be watching what they say about this in future reports and shareholder meetings.

Come 2030 and Smith will be 77. Julian Robins, who seems to be his second-in-command when it comes to investment decisions, will probably be in his late 60s given that he attended Oxford University from 1981-84.

We may see some younger names come to the fore, perhaps like Simon Barnard and Will Morgan, the team that runs Smithson.

But perhaps the safest prediction of all is that the annual management charge will still be 0.9%!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Great write up. Somehow I stumbled across Fundsmith fairly early on and then added. With that I considered them a member of my Oeic gang of 4 with Lindell Train, Marlborough Special Sits and sadly Woodford. Luckily the 3 have saved my blushes. I avoid tinkering now and happy to sit back with the Woodford liquidations going into ITs like Smithson and a punt on Temple Bar.

I used to diversify but now my portfolio consists of one fund only. I know this approach wouldn’t suit many investors but I’m confident that Fundsmith is my route to steady and sustained profit. So I reckon I’m very happy to rely on Terry Smith for a good while yet.

Why diversify, Fundsmith is gold plated!

I have only recently discovered IT investor. Really enjoy the interesting articles. I have been invested in fundsmith for about 4 years to my personal profit. Also been in Lindsell train global for the same time but found that rather lacklustre over last year so moving out.

Keep up the good work IT investor.

Michael Davison… Snap, I was purely in Fundsmith for 5 years… I have diversified now, 10% Fundsmith 90% Smithson!

If Fundsmith do not buy and sell many companies within their portfolio. Is it necessary to charge approx 0.95% in fees?

I think Fundsmith would say the work needed to research existing and potential positions is much the same, regardless of how frequently they buy and sell. But it is a high charge relative to other funds that have several billion pounds of assets like Lindsell Train Global and Scottish Mortgage.