BB Healthcare Trust has a slightly different approach to healthcare investment, focusing on companies that are looking to improve the underlying process of keeping us all fit and well.

[Note — as of 2 March 2022, this trust has been renamed Bellevue Healthcare Trust]

It’s a theme that will strike a chord will many of us. Healthcare professionals are undoubtedly heroes but the clunkiness and unconnected nature of healthcare systems worldwide is a constant source of misery and frustration, for both practitioners and patients.

As with many things, technology might be the solution.

Whether it’s a Zoom call with your GP, better monitoring of those most at risk, or simply working out what’s actually happening by joining the dots from the data of millions of patients, there’s a lot that can be improved. Not only can costs be cut, but we can tackle health problems in their early stages rather just dealing with their eventual consequences.

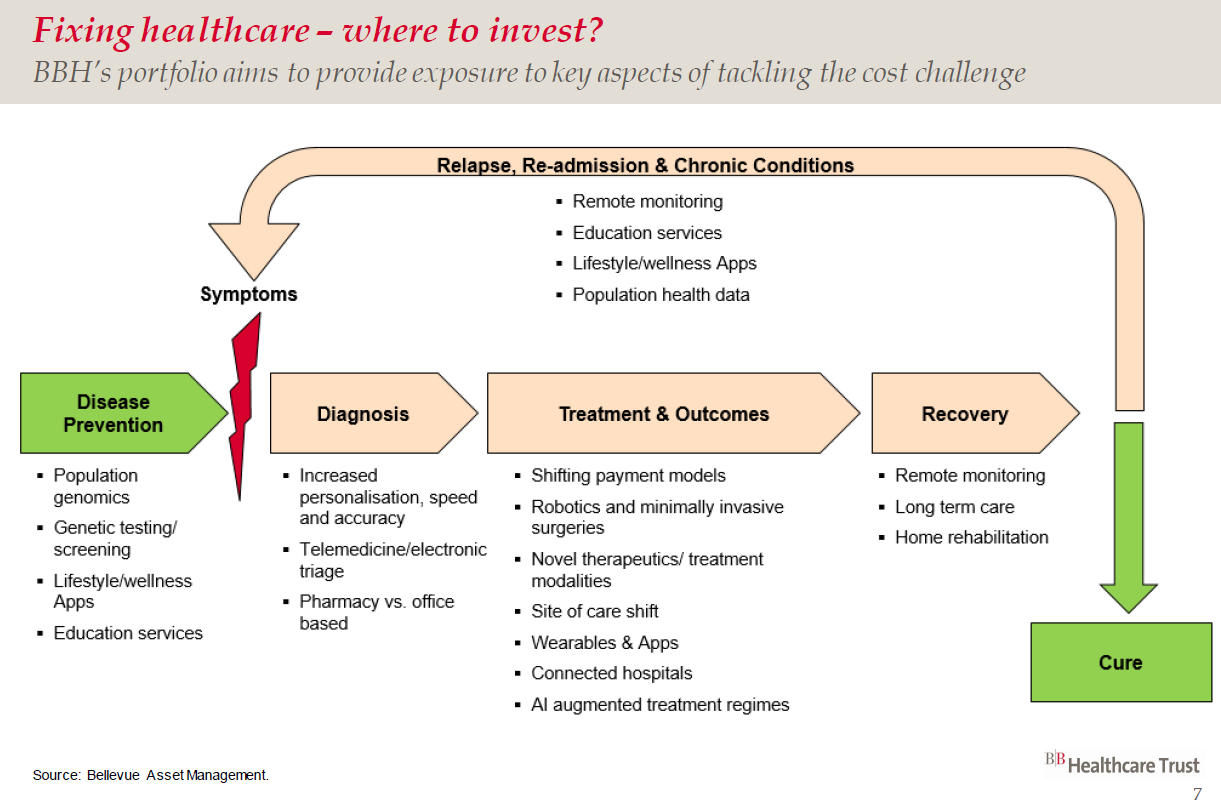

Here’s a slide from a recent BB Healthcare presentation that fleshes this out a bit more:

I first bought shares in BB Healthcare last summer, alongside two others in the same sector, and have topped up a couple of times since. Here’s the usual summary info:

Key stats for BB Healthcare Trust

- Listed: December 2016

- Managers: Paul Major (late 40s) and Brett Darke (early 40s?)

- Management firm: Bellevue Asset Management

- Ticker: BBH

- Return since IPO: +103% (18.2% pa)

- Current price: 184.25p

- Indicated spread: 184.0p-184.5p (0.3%)

- Results released: Feb/Mar (finals) & Jul (interims)

- Market cap: £945m

- Net asset value (NAV): 182.4p at 8 Mar 2021

- Premium to net assets: 1.0%

- NAV updated: daily

- Costs: 1.1% OCF and 1.3% KID

- Net cash: 6.6%

- Current dividend and yield: 6.03p and 3.3%

- Dividend policy: 3.5 % of NAV as of 30 Nov each year

- Dividends paid: Apr and Aug

- Sector: Biotechnology & Healthcare (2nd out of 6 over 3 years)

- Links: Website – AIC page – Kepler report

Price and return data as of 8 Mar 2021.

Introducing Bellevue

BB Healthcare is run by Bellevue, a Swiss-based asset manager that specialises in healthcare investments.

Bellevue looks after about £9bn of assets in total and runs six funds, the largest of which is the £3.6bn BB Biotech (see these recent paid-for research notes from Edison and Quoted Data).

BB Biotech doesn’t have a London listing but is quoted in Switzerland, Germany, and Italy. It has returned nearly 14% a year since it was launched in November 1993.

By way of comparison, that’s a little behind the 16% annual return Worldwide Healthcare is reckoned to have generated since it launched in April 1995.

Nevertheless, both BB Biotech and Bellevue are held in high regard and this meant the launch of BB Healthcare in the UK at the tail end of 2016 generated a decent amount of interest. It raised £150m although it had been looking to raise £200m.

BB Healthcare’s managers

For the first couple of years, Dr Daniel Koller, who has run BB Biotech since 2010, was one of the managers of BB Healthcare. However, he stepped back in March 2019, leaving Paul Major and Brett Darke to run the show.

This was an expected move according to Bellevue and doesn’t seem to have radically altered the way the trust is run as far as I can tell.

Major joined Bellevue about six months before BB Healthcare was launched. He spent 18 years as a healthcare analyst prior to joining Bellevue and has a biochemistry degree.

He seems to do most of the trust’s presentations, including this one for the Kepler Spring Conference just last week, where he confessed to being in his late 40s (when everything starts aching and breaking as he put it).

Darke came on board in September 2017. He’s probably a few years younger than Major but has a similar background in healthcare-related finance. He studied Medicines and Management at Cambridge.

Major and Darke are based in London but seem to be able to tap into the wider expertise that Bellevue offers. And the board of BB Healthcare provides a wealth of sector experience.

Chairman Randeep Grewal trained as a Vascular and General Surgeon, Justin Stebbing is “a clinical oncologist and has published over 500 peer-reviewed papers on cancer”, and Professor Tony Young is “a practicing frontline NHS Consultant Urological Surgeon, Director of Medical Innovation at Anglia Ruskin University, President of the Institute of Decontamination Sciences, and National Clinical Director for Innovation for the NHS”.

Major, Stebbing, and Young discussed COVID and its implications in this Citywire podcast a few months ago. It was implied this would be the first in a series although there’s been no follow-up episode to date.

Investment style

BB Healthcare says it invests in the “global healthcare industry including companies within industries such as pharmaceuticals, biotechnology, medical devices and equipment, healthcare insurers and facility operators, information technology (where the product or service supports, supplies or services the delivery of healthcare), drug retail, consumer healthcare and distribution”.

I won’t revisit the detailed case for healthcare investment but, in short, it’s the twin effects of the global population getting older and wealthier, both of which tend to increase the proportion of income spent on treating our ever-growing ailments.

The MSCI World Healthcare index has returned some 11.3% a year in dollar terms since January 1995, which is some 3 percentage points greater than the main MSCI World index, so this trend has been in evidence for a long time already.

BB Healthcare is not constrained by any index, geography, or company size although liquidity is a key focus so it has no unquoted holdings.

It seeks to ensure 90% of its portfolio can “be liquidated in a reasonable number of trading days” and won’t start a new position unless it can invest 1% of its portfolio “within an acceptable level of liquidity”.

The trust’s portfolio is pretty concentrated with an upper limit of 35 holdings. There are currently 30 positions with about half the portfolio in the top 10.

There’s a policy that no single investment will exceed 10% of net assets at the time of acquisition although a few holdings have crept above this level at times, due to good share price performance.

Portfolio turnover is relatively high, in common with many funds in this sector. In BB Healthcare’s case, there is a strong focus on company valuations rather than holding through all the ups and downs.

Over the year to November 2020, 8 new positions were started and 8 were sold, although the pandemic meant valuations were more volatile than normal. 2 of the new positions were previous holdings and 3 of the exits were due to takeovers.

As a percentage of average net assets, 62% of portfolio value was sold during 2019 and 83% in 2020.

The typical holding period is said to be 3-5 years and BB Healthcare reckons around 40% of its current portfolio was held when the trust was launched.

Investment targets

BB Healthcare looks for both capital growth and income, aiming both to beat the MSCI World Healthcare index and generate double-digit annual returns over rolling three-year periods.

In its first four years, shareholder returns were 18.1% a year versus 12.6% for the healthcare index suggesting we can tick both boxes.

The first two years saw excess returns of five percentage points each and the third a deficit of two. The year to November 2020 was BB Healthcare’s best yet, with excess returns of fourteen percentage points.

Since its launch, BB Healthcare has managed to outperform the rest of its sector, with a lower level of volatility. Biotech Growth did have a healthy lead over it up until a few weeks ago, but the tech/biotech rout since then has changed the picture dramatically.

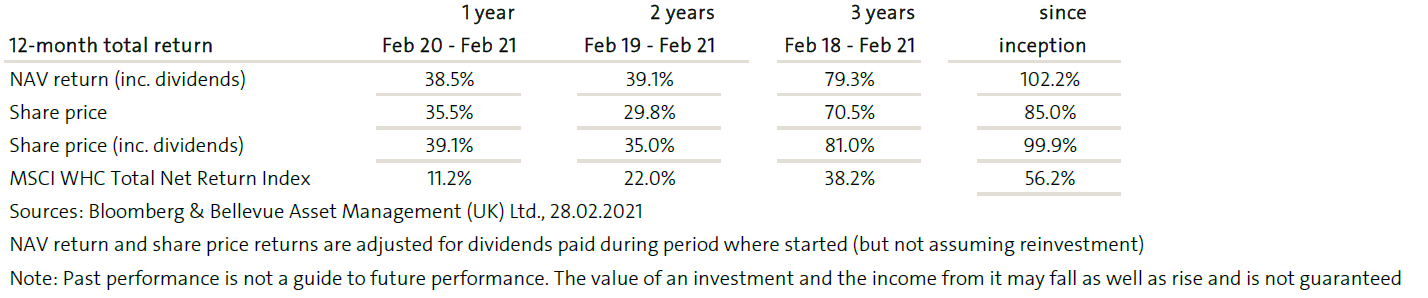

Here’s the latest performance data from BB Healthcare’s February 2021 factsheet:

Share issuance and discount/premium control

BB Healthcare looks to limit any discount or premium that its shares trade at but it doesn’t set any fixed percentage at which it will intervene.

As it has turned out, it’s traded at a small premium pretty much the whole time it’s been listed.

When it floated it had 150m shares but it issued 57m more in September 2017 and another 34m in November 2018. It’s regularly issued smaller parcels of shares, 284 times in total, to keep its premium down.

The share count has more than trebled to 512m since December 2016 and its market capitalisation has risen from an initial £150m to nearly £1bn.

I don’t think any share buybacks have taken place but the Board did discuss them when the pandemic first struck last year. However, it was decided that “higher returns would be made from investing more capital into the portfolio companies than buying back shares.”

That proved to be correct.

There is also an annual redemption facility but a total of just 1.3m shares have been redeemed this way the four times this has been offered to date.

Large share issuance like this can be a concern as it can reduce the pool of potential investments.

BB Healthcare’s Chairman admits he is often asked about it but reckons the trust’s strategy still has room to grow without affecting returns or liquidity. He also says the Board will only sanction further issuance as long as they feel it won’t impact returns.

Portfolio

BB Healthcare seems to play its cards very close to its chest when it comes to its full portfolio. Its top 10 holdings are published monthly but I couldn’t find a complete list anywhere, not even in its full report and accounts.

That’s highly unusual and a little off-putting. I prefer to see all the gory detail to better gauge the types of companies being held.

Here are the latest top 10 holidings:

There’s a couple of well-known players in there and BB Healthcare has also invested in the likes of Teladoc, Intuitive Surgical, Illumina, and Fitbit. For the most part, though, I wouldn’t say I’m that familiar with many of its holdings.

Its twenty other holdings have a median position size of 2.4% but we don’t know too much more about them. A few are mentioned in passing in the annual report, most notably a disastrous foray into NMC Health which resulted in a 100% write-down.

As many readers will be aware, NMC Health was subject to fraud and embezzlement on a grand scale (the group’s indebtedness was grossly understated to the tune of $4.5 billion). Multiple criminal and civil probes are ongoing. We are obviously frustrated to have suffered losses, but the central tenet of any due diligence process begins with a company’s audited regulatory filings, which contain a statement from the auditor attesting that they reflect a “true and fair view” of the entity. Unfortunately, this turned out not to be the case here.

We have recommended to the Board a total write down of the value of the investment in the portfolio due to the uncertainty of ever receiving any value from the resolution of the sorry tale; a recommendation we would never have expected and one we hope we never have to make again.

The Company held a position in NMC since May 2019. We were aware of questions about governance and accounting then, and subsequently, but we felt these concerns were reflected in NMC’s share price, making it a well-positioned play on expansion of developing market healthcare provision. We spent significant time on due diligence and with management, including its board members. The pertinent questions were asked but, alas, the information we received turned out to be very wrong. The extent to which any of the individuals concerned were complicit in this remains to be seen.

As far as I can tell, NMC wasn’t mentioned by the managers in any previous report or update although I haven’t searched every monthly factsheet.

It does raise a few concerns and reminds me of the Wirecard fiasco that beset European Opportunities. It’s not clear how much was lost although it’s worth highlighting that, even after this write-down, 2020 was BB Healthcare’s best year so far relative to its benchmark index.

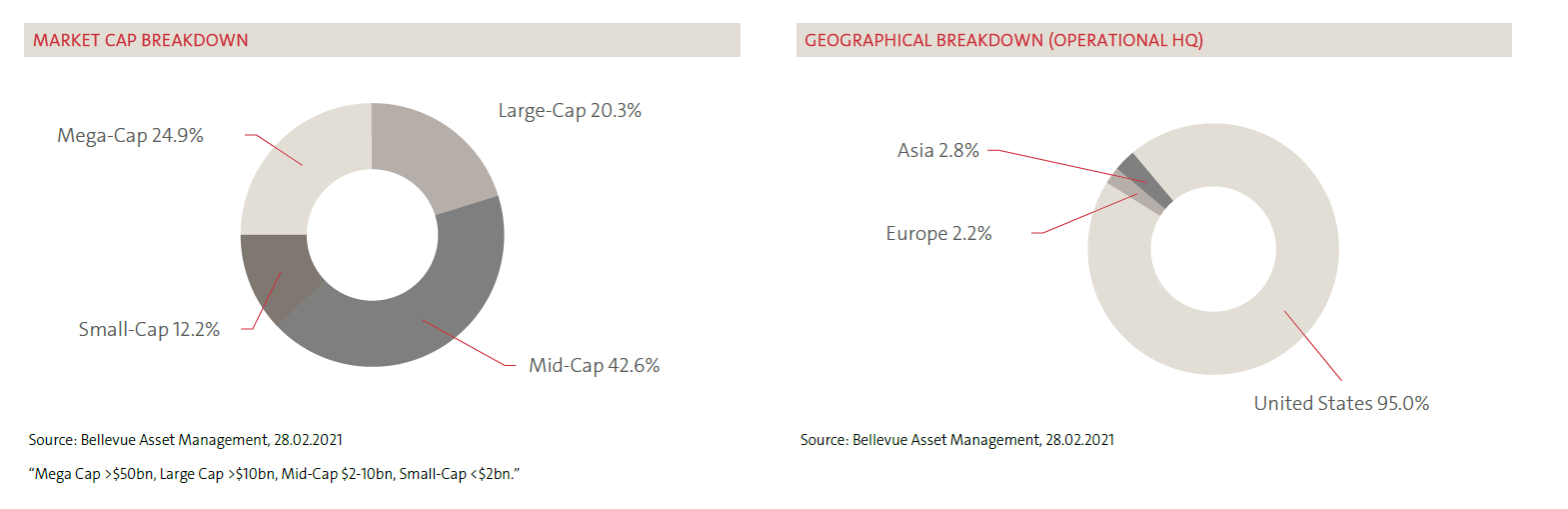

The trust provides some additional categorisation of its portfolio into size and base of operations:

It’s notable that more is invested in both small-caps (12% vs 9%) and mid-caps (43% vs 34%) than it was a few months after BB Healthcare launched.

So, that does support the Board’s argument that the liquidity of underlying investments has not been a major problem to date.

The heavy US focus is typical of many healthcare funds and mainly a factor of following the money. Simply put, healthcare is a long-term game and US investors are the ones who seem happiest to fund it on this basis.

Europe and the UK may be home to a lot of medical know-how and Asia will become increasingly important, but the US is likely to rule the roost for the foreseeable future.

Major reckons the trust’s US weighting is likely to be high 80s or low 90s for some time.

Sector rotation

A lot of manager commentary centres on the relative merits of the various sub-sectors of the healthcare industry.

BB Healthcare uses slightly different categories than the standard industry classifications. Here’s how it currently compares to the MSCI World Healthcare index:

| Sub-sector | MSCI H/C index | BB Healthcare |

|---|---|---|

| Conglomerates | 11.8 | – |

| Diversified Therapeutics | 34.2 | 16.7 |

| Dental | 0.7 | – |

| Diagnostics | 2.2 | 7.7 |

| Distributors | 1.2 | – |

| Facilities | 1.1 | – |

| Focused Therapeutics | 9.0 | 32.5 |

| Generics | 0.6 | – |

| Healthcare IT | 1.9 | 5.2 |

| Healthcare Technology | 0.7 | – |

| Managed Care | 9.0 | 11.3 |

| Medical Technology | 15.7 | 15.9 |

| Services | 2.5 | 6.9 |

| Tools | 8.0 | 3.8 |

| Animal Health | 1.4 | – |

| Total | 100.0 | 100.0 |

There are a number of smaller sub-sectors that BB Healthcare tends to avoid entirely and Major is very disparaging of low-growth / high-yielding drug giants, describing Glaxo-bashing as one of his favourite pastimes.

Over the course of the last year, a lot of the changes related to pandemic beneficiaries, where valuations got too frothy for the team’s liking, and companies more attuned to elective surgery, which they felt would take longer to recover than the market seemed to be pricing in.

In a few cases, it turned out that BB Healthcare sold too early. A 7% position in Dental last year, largely Align Technology, was seen as too risky and sold, before racking up significant further gains. It was a similar story at Teladoc. That’s always a danger when you focus on valuations.

It’s well worth reading the trust’s monthly factsheets to get a feel for where the team feels the healthcare winds are blowing and for their thoughts on the wider economy and how it might recover from the pandemic.

It’s fair to say that Major is cautious on how long we will be dealing with the effects of COVID and also on how effective vaccines might be in stopping the spread of the disease.

Paying dividends from capital

The trust is “yield agnostic” when looking for individual investments but pays out a fixed 3.5% of its net asset value each year in two equal instalments.

The dividend is based on the asset value at the trust’s year-end of 30 November but the payment is delayed somewhat. The current dividend of 6.03p based on the NAV as of 30 November 2020 won’t be paid out until August 2021 and April 2022.

These types of dividend policies are often a marmite issue, with some investors preferring to generate yield from share sales and warning that the level of dividends are inherently more volatile.

I’m more relaxed and it does seem that these policies attract a wider range of investors, helping to keep any discount to NAV to a minimum.

That said, the shareholder register is notably free of Hargreaves Lansdown and interactive investor, the presence of which normally indicates plenty of interest from private investors.

Brewin Dolphin Wealth Management is the largest holder at 5.9%, followed by Quilter (another wealth manager) at 4.2%, and Schroders at 3.2%.

Gearing

BB Healthcare can gear up 20% to enhance its returns but says somewhere between 5% and 10% would be typical in normal market conditions.

However, the mangers’ cautious approach to current valuations has meant the trust has been running a small cash balance for about a year now. I think net cash peaked at 10% at the end of November and it’s since reduced to just under 7%.

When borrowing is required, a multi-currency revolving credit facility can be used. The current one is limited to $150m and is with The Bank Of Nova Scotia. It was renewed in January 2021 and expires in January 2022.

Charges

There is no performance fee charged, unlike most of the other trusts in this sector.

The management charge is 0.95% and based on market capitalisation each month rather than net assets. The fee structure hasn’t changed since the trust launched despite the market cap going up more than sixfold.

While most of the sector is bunched around the 1% mark for overall costs, it would be good to see a tiered fee structure put in place here, especially given the large share issuance that has taken place.

However, BB Biotech, despite being much larger, charges a flat 1.1% of net asset value so we could be waiting a while on this front.

By and large, the trusts in this sector have managed to beat their benchmarks over the long term, so that does make the higher charges easier to stomach.

Your bog-standard MSCI World Healthcare ETF will set you back 0.25% a year, should you prefer the passive route.

Skin in the game

There’s no information on the holdings of Major and Darke but there was a comment that they were “heavily invested” in last week’s presentation.

The directors seem to take their fees in shares each quarter.

They bought 140,000 shares at the IPO – the standard equivalent of one year in fees – although one of them has since left the Board due to other commitments.

The remainder, plus Young who joined in September 2020, have since built up a holding of nearly 300,000 shares between them, worth just over £0.5m.

It’s not a massive combined investment, but for a trust that’s not yet five years old, it seems reasonable. What’s more, it’s nice to see their ongoing commitment to add to their positions.

Summing up

As this is one of three trusts I own in the biotech and healthcare sector, my stake here is one of my smaller positions and likely to stay that way.

But I’m been pretty impressed by what I’ve seen so far. The lack of a full portfolio listing, the flat fee structure, and the NMC episode are all things I could do without, but I can live with them in a smaller-sized holding.

The trust takes a more active approach than I usually go for, which is something that needs watching. So far, it has paid dividends (pun intended) and the one year of underperformance to date was pretty minor.

The fact that the departure of Koller, seen as a potential red flag at the time if I recall, was followed by the trust’s best-ever year also provides some confidence that there could be strength in depth at Bellevue.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Mmmm.. Not sure at all why the phrases “I would run” and “a mile” plus “thanks but no thanks” immediately spring to mind.

Could you elaborate, Graham? Curious to know what aspects you found offputting as nothing raised any significant red flags for me.

It is of course a matter of judgement (that’s what makes it interesting), but my answers having read the piece would be: Apparent lack of transparency of holdings and some lack of clarity in other areas (“disastrous foray into NMC”); high U.S. weighting; stated disdain for more conservative potential investments; dividend policy; charges policy; arguably modest holdings by at least some of the insiders.

I’m sure it’s a question of “feel”, but happy to leave you to it… (But many thanks and good wishes to you anyway).

Thanks, Graham – all fair concerns I think although I suppose you could say similar things about many other trusts as well. The lack of a full portfolio listing is the only thing that appears to be unique to BBH, as far as I am aware anyway. Best wishes to you as well.

Very interesting review as I had not reviewed the Trust previously. I would have no issues with it except the lack of transparency on their list of holdings but can live with that as the sector breakdowns are given. Would certainly look at it as I think Genetics is going to be big in medicine going forward. I personally own one Genetic company – Fulgent Genetics (FGLT) and is powering ahead despite being very young with a bit of a wobble with the recent downturn in Tech stocks. The Europeans are the leaders in Healthcare/Pharma and new products processes so it is difficult to know which one to go for. The CEOs of the vaccine companies involved in Covid-19 are nearly all French/German. This comes from the embracing of STEM by European countries including Ireland since the 1960s. The UK unfortunately whilst they have great Universities they are not linked to the practical business world. Even the Oxford/AstraZenica vaccine involves EU/Irish lead scientists – Professors Hill and Lambe. So for me using a Trust makes sense as I am not a medical/healthcare specialist. Will consider shortly an investment in this one. Thanks

Hi; good analysis here again. I’ve never owned BBH but I have owned Biotech Growth (BIOG) for many years and every £1 I invested is now worth £5, so obviously I’m very happy and have no plans to jump ship. But I thought I’d make some comments regarding BB anyway.

The dividend yield of 3.5% is a distinguishing feature and may appeal to those seeking extra income. It probably adds some downside protection as we can see from the relative outperformance during the downturn. Personally I consider the biotech sector is one better suited for capital growth.

I don’t like trusts which don’t publish full portfolio listings because I can’t really see a reason not to. This has certainly put me off investing in other trusts before.

At the moment BBH is on a 3% premium and BIOG a 2% discount (Sharescope). So perhaps BIOG looks better value, but a year ago BBH was on 1% discount and BIOG a 5% discount, so relatively BIOG has moved further.

I’d certainly consider BBH if I was a new investor to the sector but I wouldn’t consider it a “slam-dunk” compared to others; so smaller holdings in 2/3 trusts (like yourself) could be the way to go.

Interesting analysis; thanks.

Addendum: I meant to say BIOG was on a 9% discount a year ago! Sorry.

Many thanks Stuart for taking the time to write this article. I hold International Biotechnology (IBT) and Worldwide Healthcare (WWH) and although it’s early days since I’ve invested, I’m pleased so far with their performance. There is a little bit of overlap with their holdings but not much. I guess it’s a bit like holding a Global IT, so many of them have either Microsoft or Tencent or both!

On first glance I don’t think there’s much of an overlap of BBH with either IBT or WWH.

I will take a more detailed look at BB Healthcare, interesting article.

Thank you.