Our house is being battered by a thunderstorm as I write this. Owning a UK smaller company investment trust in 2020 has felt very similar. But storms pass.

Henderson Smaller Companies, one of my holdings in this sector, reported its annual results recently, so I’ve been checking on its progress.

Before diving into that, some thoughts on the wider sector…

A savage 2020

Across the 24 investment trusts in the UK Smaller Companies sector, the average loss year to date is 22.6%.

Only two trusts are in positive territory — Oryx International Growth (+8.7%) and Miton UK MicroCap (+2.7%) — and twenty have recorded a loss of 15% or more.

There are plenty of reasons why.

The UK market as a whole has struggled and this often has a knock-on effect for smaller companies.

The FTSE 250 and SmallCap indices are down around 20% this year, when you strip out the performance of the investment companies they contain. That’s a couple of percentage points worse than the FTSE 100.

Somewhat surprisingly, the AIM market, often derided for the quality of the businesses it contains, is down just 7%.

Small caps often seem to outperform in good times but lose ground in bad ones. They tend to be less well-financed than larger companies and have more of a domestic focus.

I’m not sure if they are less ‘digital’ than larger companies, for want of a better word, but that may be a factor this year, too.

Less than 3% of the FTSE 250 and FTSE Smallcap indices are classed as technology businesses (although it’s a fairly narrow definition). The AIM market fares better at 13% and has a similar percentage classed as healthcare, both of which are likely to have helped in 2020.

And at the trust level, discounts have widened significantly, from 2.7% at the end of 2019 to 11.4% at the end of July 2020.

In truth, that narrow discount at the end of 2019 did look a little racy. I normally think of a 10% discount for this sector as being typical.

Lastly, 2019 was a great year for the sector with the average share price up 42% and net asset value up 30%, so the pullback should be seen in that context.

Smaller companies are often feast or famine and the last 18 months provides an excellent illustration of that.

Consolidation on the way?

We’ve started to see some merger and takeover activity in the investment sector in recent weeks and that may spread to UK Smaller Companies as well.

Of the 24 trusts, 5 have market caps of roughly £500m+ but the remainder are all below £200m and 12 are worth less than £100m.

You could make the argument that a smaller company trust should be on the smaller side itself, to give it more room for manoeuvre, but charges often start to get excessive under the £100m mark.

A lot of the trusts in this sector have been around a while. Two-thirds have been listed for 15 years or more. A little clearout may be overdue.

How I’m playing this sector

My strategy is based on the fact that smaller companies have tended to outperform larger ones over the long term.

And smaller company trusts have, as a group, seemingly done better than their benchmarks. The active approach does seem to add value.

Small-cap trusts have a relatively big pond to fish in. There are around 800 companies on the main market and AIM valued at between £20m and £4bn, collectively worth around £400bn.

The UK small-cap trust sector has just over £5bn in assets under management, so it accounts for just over 1% of that total.

The choice for UK trusts specialising in larger companies is a bit more limited, as there are only around 250 companies valued at over £1bn, with many of those in low-growth sectors.

In the AIC’s table of the top 20 performing trusts of the last 20 years (based on annual ISA contributions rather than total performance), UK smaller company trusts occupy seven slots. Other smaller company trusts account for another four.

What has worked in the past is not guaranteed to work in the future of course. But I think it’s a good place to start and makes small-caps a sensible side bet alongside my core of global trusts.

In common with my other thematic choices, I’ve gone for a small basket of trusts rather than pick a single favourite.

I went for two of the larger, more established names, BlackRock Smaller Companies and Henderson Smaller Companies, plus a wildcard called Acorn Income that’s suffering from a little over gearing right now.

I’ve been building up these positions for a few years, on the basis that the volatile nature of the sector could provide some decent buying opportunities.

It certainly hasn’t disappointed on that front, although I’m pretty much flat with Henderson Smaller Companies having bought both a little higher and lower than the current price.

Key Stats For Henderson Smaller Companies

- Founded: 1887

- Manager: Neil Hermon (since November 2002)

- Ticker: HSL

- 10-year net asset return: +270%

- Benchmark: Numis Smaller Companies index

- Current price: 776.5p

- Indicated spread: 776p-777p (0.1%)

- Market cap: £595m

- Discount to net assets: 13.0%

- Costs: 0.42% OCF and 1.12% KID

- Gearing: 11%

- Number of holdings: 104

- Current dividend and yield: 23.5p and 3.0%

- Results released: Jan (interims) and Aug (finals)

- Dividends paid: Mar, Oct

- Sector: UK Smaller Companies (5th out of 19 over 10 years)

- Links: Website and AIC page

Not a lot has actually changed with these numbers since I last looked at this trust in detail this time last year.

The share price, discount, gearing level, and the number of companies in the portfolio are all pretty much identical.

However, we’ve swung from a gain of nearly 40% to a loss of nearly 40% in just a few weeks, with a small premium turning into a discount just shy of 20% at one point.

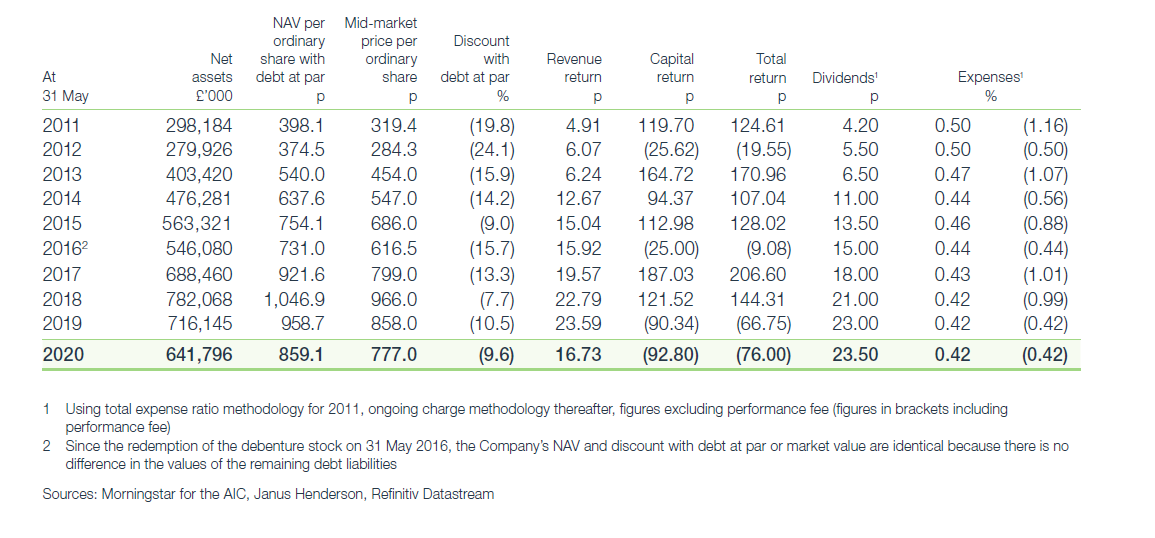

Ten-year record

Here’s the summary table from the latest set of accounts:

Perhaps the most eye-catching thing here is the dividend growth, from 4.2p in 2011 to 23.5p in 2010. The yield has risen from 1.3% to a respectable 3.0% as a result.

In fact, since Hermon was appointed to run the trust in 2004, dividends have grown from 1.0p per share.

You need to go back a little further to establish that the trust slashed its dividend from 3.95p in 1999 to 0.5p in 2000.

It had been paying out of its revenue reserves for a few years and decided to reset things by emphasising total return rather than income growth.

So while the dividend growth has still been very impressive since the turn of the century it’s been from an artificially low base.

Dividends in 2021 and beyond

Having notched up 17 years of increasing dividends, and therefore closing in on AIC Dividend Hero status (which is 20 years), it will be interesting to see what happens next.

There was a small increase for the year to May 2020 of 0.5p per share to 23.5p, but that was entirely from the interim payout. The final dividend was held at 16.5p.

As the coronavirus outbreak coincided with many companies’ final payouts for 2019, Henderson’s investment income fell from £19.4m to £14.2m for the year to May 2020 and it will probably be lower still next year.

There was a £5m fall in its revenue reserve to £19.4m as a result.

The revenue reserve represents just over a year’s dividends, so there’s a bit more left in the tank. But I would be very surprised if there was an increase in the next interim dividend.

This time next year, when things are hopefully a little clearer, we might see a token increase in the final dividend. However, I’m not expecting much in the way of income growth here for a few years.

Impressive consistency… but with a caveat

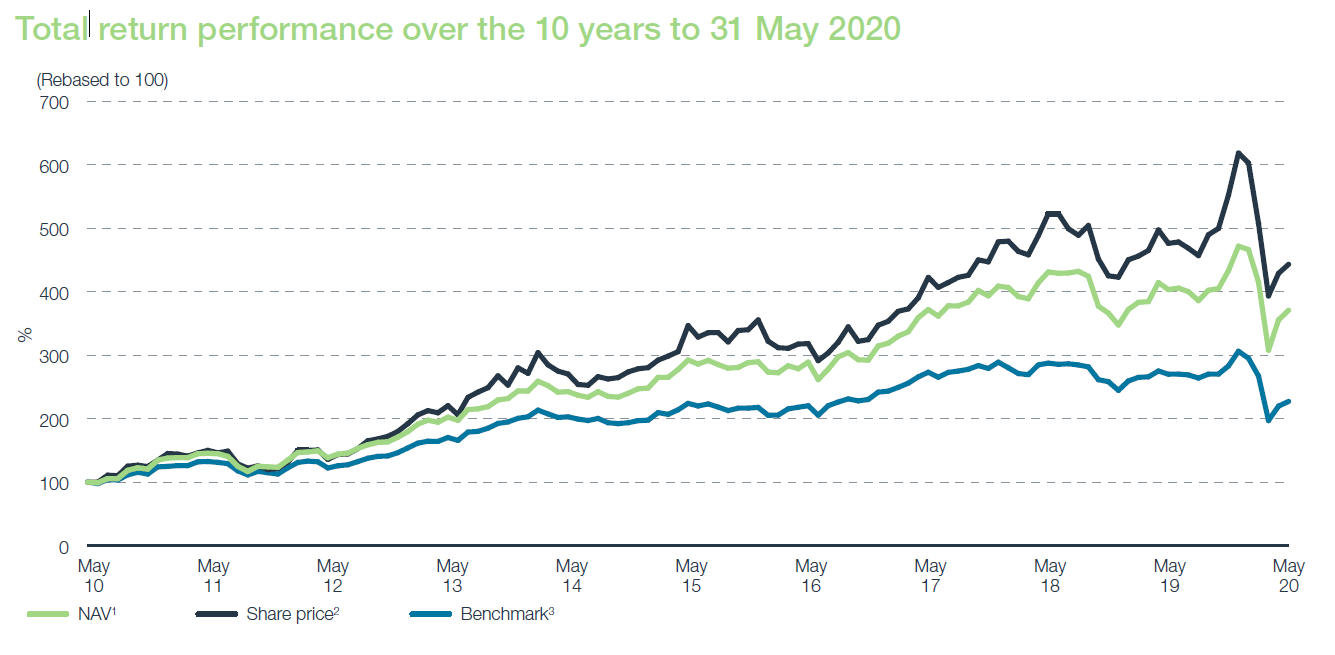

Neil Hermon has now outperformed his benchmark in 15 of the 17 full years in which he has managed the trust.

Over the last decade, his annualised net asset value total return has been 14.3%, outperforming the benchmark by 5.8 percentage points per annum.

You can see that consistency in this chart of Henderson Smaller Companies’ performance over the last 10 years. It also highlights just how exceptional the ramp-up of share prices in the second half of 2019 was:

Henderson Smaller Companies’ benchmark is the Numis Smaller Companies index excluding investment companies, which measures the bottom 10% by market cap on the main London market.

This index has reputedly beaten the FTSE All-Share by 3.3 percentage points a year from 1955 to 2019, although roughly half of that period was calculated by back-testing so is arguably less reliable.

The outperformance over the last decade has been 2.4 percentage points. Narrower, therefore, but still meaningful.

In practice, though, this benchmark misses quite a lot of what Henderson Smaller Companies invests in, seeing that only three of the trust’s top 10 are included in it.

The Numis index only includes about half of the FTSE 250, in which Henderson has 55% of its net assets invested.

It excludes everything on AIM, which accounts for just under 30% of Henderson’s net assets (the balance is mostly in the FTSE SmallCap).

There are several other versions of the Numis index, some of which include AIM or the bottom 20% of the main market but ignore the bottom 5%. These might make better comparators, but I don’t have the data to tell if their performance has been materially different.

For the year ended May 2020, the choice of benchmark did flatter Henderson somewhat.

Its NAV fell 8.2% which was much better than the benchmark’s -15.9%.

The AIM market held up pretty well over the same period to May 2020 (down around 5%). Including this in the benchmark would have definitely narrowed the outperformance gap.

Fees and charges

I’m being a little niggly here but it’s relevant because Henderson does have a 15% performance fee based upon its benchmark.

No performance fee was payable in 2019 or 2020, as it’s rolled over to future periods when the share price falls over the course of the year.

But there was a performance fee paid in both 2017 and 2018, which bumped up the very reasonable basic ongoing charge of 0.4% to a less impressive 1.0%.

Performance fees have been payable about half the time over the last decade, so the actual ongoing charge has probably been around 0.7%.

By way of comparison, the ongoing charge for CUKS, the iShares MSCI UK Small Cap ETF, is only a little lower at 0.58%. It was listed in 2009, covers 245 companies, and has £190m in assets but it hasn’t performed nearly as well as Henderson Smaller Companies.

Mid-cap trackers that cover the FTSE 250 do tend to be a lot cheaper, though, varying from 0.1% to 0.15%.

Investing style

A recent interactive investor podcast provided a useful summary of Hermon’s investing approach. He describes it as growth-orientated but with an eye on valuations. Growth at a reasonable price, or GARP as it’s usually referred to, was mentioned numerous times.

Hermon takes a stock-specific approach when picking companies rather than one based on macro-economic calls.

He seeks quality companies that can be held for the long-term, saying the trust’s average holding period is around 5 years.

Sector focus is not a priority but the preference for growth leads him to industries like electronics, software, media, and pharmaceuticals and away from the likes of food producers, retail, and mining.

At just over 100 companies, it’s a pretty well-diversified portfolio. The largest positions tend to be about 3% with 25% in the top 10 and 40% in the top 20. Just over half of the portfolio has a weighting of less than 1%.

Scouring the full portfolio list didn’t ring any particular alarm bells for me in terms of anything overly speculative. There’s around 3% in oil, gas, and related services that I’d happily do without, but that was pretty much it.

While the portfolio is growth-orientated, I’d still say it was relatively conservative.

It sounds like there was more portfolio activity than usual earlier this year, which seems to be a common theme among many trusts reporting recently.

For example, Hermon cites Gym Group and Mitchells & Butlers as two companies he’s keen on and that might look cheap when they begin to get to more normal levels of operation again.

He’s warier of companies supplying big-ticket items, believing these could take much longer to recover.

Skin in the game

There’s a fairly limited shareholding across the board of directors, worth just £150,000 in total.

Penny Freer and Alexandra Mackesy, both appointed in September 2018, bought shares for the first time in the last few months.

Both Neil Hermon and Indriatti van Hien (who was appointed Deputy Fund Manager in June 2016) are said to have shareholdings in the trust but of an undisclosed amount. They also receive a proportion of any performance fee paid.

Hermon is in his early 50s I reckon, so should be in charge for a few more years. But the appointment of deputies often signals a departure is at least being prepared for.

In summary

Henderson Smaller Companies had a decent year in the circumstances although quite a few other trusts (most notably Oryx, JPMorgan, Standard Life, BlackRock Throgmorton, and Montanaro) have fared better recently.

It’s noticeable that after a swift bounceback in late March and early April, the share price hasn’t done much since. The net asset value has continued to creep up, though, causing the discount to get wider and wider.

Over the long term, I’m still expecting Henderson (and BlackRock Smaller) to be near the top of the UK small-cap pile, assuming they continue their run of consistency.

It’s unlikely they’ll be the very best performers over 5 or 10 years, given they don’t have very concentrated portfolios. The likes of Rights & Issues, Oryx, and newcomer Odyssean, all of which are much more focused, seem more likely to take turns occupying the top slot.

I’d be surprised if the UK smaller companies sector matched its performance in the 2010s over the next decade. Although it is pretty much at the level it was three and a bit years ago, it trebled in the five years before that.

Nevertheless, it still seems like a good place to fish to me, assuming you’re happy to ride out the inevitable ups and downs.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Fair to say that we’ve seen a decent bounceback since August 2020 with the share price up nearly 60% since then.

Neil Hermon was interviewed by James Carthew of QuotedData last week. Runs for about 30 minutes but gives a good overview of the trust’s development under his management, the investing style, and thoughts about the sector going forward from here.

https://quoteddata.com/weekly-show-090421-neil-hermon-11/