RIT Capital Partners is one of a number of conservatively managed global investment trusts that I hold in an attempt to give my portfolio a little ballast. It seems like a good time to see how that’s working out!

23 years and counting

RIT Capital Partners has the dubious honour of being my longest-held position, stretching all the way back to late 1996 when I began with a monthly savings scheme.

I topped up with lump sums in 2001, 2003, 2011, and 2015.

I’ve yet to sell any and for quite a while it’s been one of my largest positions. However, having built up a capital gain (albeit a smaller one than I had at the start of this year!), it’s possible I might sell some in the next few years to use up some capital gains allowance and top-up some of my smaller positions.

For some time, though, I think was somewhat guilty of being asleep at the wheel with this holding, with its past performance lulling me into complacency.

I took a proper look at RIT’s holdings for one of the first articles on this blog, having just skimmed its accounts for a few years, and was surprised by the extent to which it had shifted from owning shares directly to owning them through funds. Its underlying charges have risen substantially as a result of this move.

Revisiting its progress this time last year, I concluded that despite trading at a premium of around 10% and those high underlying charges, its defensive qualities remained attractive enough.

Change at the top

Long-serving chairman Lord Rothschild stepped down last year, in what appeared to be an orderly succession plan. He’s been intimately involved with RIT from the start as its history page describes:

Jacob Rothschild joined the bank in 1959 and played a significant role in developing its business. In 1971 he was appointed Chairman of Rothschild Investment Trust which had a value of £5 million. In 1980 he left the bank to concentrate on developing the business of Rothschild Investment Trust, which was subsequently renamed RIT. At that time RIT was a listed investment trust with net assets of some £80 million.

RIT was subsequently built up through a combination of internal growth and acquisitions so that by the 1980’s it had become an investment holding company, J Rothschild Holdings plc with assets of about £650 million. As a result of its acquisition of a number of financial services businesses during this period, the company no longer qualified as an investment trust and in 1988, J Rothschild Holdings plc demerged into two entities – J Rothschild Assurance which was subsequently renamed St. James’s Place Capital plc and RIT Capital Partners plc.

RIT Capital Partners plc was listed on the London Stock Exchange with net assets of £281m on 1 August 1988. It is now one of the UK’s largest investment trusts, with a market capitalisation of around £3 billion.

It’s too early to tell if much has changed behind the scenes but, for me at least, there was nothing in its recent results that indicated a significant shift in thinking.

I speculated at the time that Lord Rothschild stepping down might result in the premium to net assets declining. That happened to some extent, even before the recent market carnage, although whether his departure was the key driver of this is impossible to know.

Key stats for RIT Capital Partners

- Listed: 1988 (around 100p)

- Manager: Ron Tabbouche (since 2012, now 46 years old)

- Ticker: RCP

- Benchmark: MSCI All Country World (50% in £, 50% local currency)

- 10-year net asset value return: 90% as of 6 April 2020

- Recent price: 1,724p

- Indicated spread: 1,720p-1,728p (0.5%)

- Exchange market size: 1,000

- Market cap: £2.7bn

- Discount to net assets: 2.3% as of 29 February 2020 (could be very different as of 31 March)

- Costs: 0.7% OCF, 3.9% KID

- Gearing: 6.5% as of 31 January 2020

- Current dividend and yield: target of 35p in 2020 (2.0%)

- Results released: March (finals) and August (interims)

- Sector: Flexible (3rd out of 17 over 10 years)

- Major holders: Rothschild family own 21%

- Links: Website and AIC page

RIT sits in the Flexible sector, having relocated from Global a couple of years ago.

While it’s mostly an equity investor, it largely uses equity funds, hedge funds, private equity funds, and direct private investments. About a quarter of its assets are in absolute return and credit funds.

Its structure is very similar to Caledonia, but it’s nowhere near as conservative as the likes Personal Assets or Capital Gearing which both hold a large proportion of fixed income.

Technically, RIT is trading at a discount to its net asset value at the end of February but a lot has happened since then.

The shares held up pretty well until 5 March and were just over £20 at that time having started the year at £21. But they collapsed to as low as 1,252p over the next two weeks before bouncing back to nearly £18 in just one week!

RIT has said its March net asset value should be released in mid-April so we’re a little in the dark on how its investments have held up in recent weeks. I’m hoping it releases a detailed update, much as Caledonia has just done.

But it’s good to see that the bid/offer spread on the shares has remained relatively narrow. A lot of trusts have seen their spreads widen dramatically in recent weeks and it’s put me off considering them as potential top-up candidates.

The upside/declines debate

RIT says it look to capture most of the update from bull markets while limiting the damage caused by those pesky bears:

Since your Company’s listing in 1988, we have participated in 73% of the market upside but only 38% of the market declines. This has resulted in our NAV per share total return compounding at 11.0% per annum, a meaningful outperformance of global equity markets. Over the same period the total return to shareholders was 12.2% per annum.

As far as I can tell, this statistic was first mentioned in March 2014, when the figures where 70% of upsides and 38% of declines respectively, so the numbers haven’t shifted too much in recent years.

It’s often reeled out by trust commentators, including myself to be fair, but I’m still not sure exactly how it’s calculated. Is it done on an annual or quarterly basis, or is a subjective call made as to when an upside/decline begins and ends?

And while 73% and 38% sounds impressive — i.e. most of bull markets but not of bears — as no other fund produces a similar statistic it’s hard to know whether to applaud it or shrug your shoulders.

Markets tend to rise a lot more than they fall, although falls tend to be a lot steeper.

Certainly, during the market fall of late 2018, RIT seemed to prove its worth although I’d say it fell about half as much as global markets did.

It’s too early to say how the current bear market will work out for RIT. It fell over 35% at one point but at the time of writing it’s down about 18%, roughly the same as a global tracker.

A benchmark quibble

Back in 2014, RIT tweaked the benchmark it uses to measure its performance.

Previously it used the MSCI World Index but it changed to the MSCI All Companies measured 50% in sterling and 50% in local currencies.

This introduced an increased weighting for emerging markets, compared to developed markets like the US and Europe. That seemed fair enough to me considering the way it invests.

Its current quoted-equity portfolio only has about half its assets in the US and Europe and some 40% in Asia/Japan. The low US weighting is undoubtedly a key reason its performance has trailed your common garden global tracker over the past decade.

But the currency split made the revised benchmark an easier comparator because sterling has steadily weakened over the last decade.

If we use a sterling version of the MSCI ACWI then bottom row becomes 35%, 81%, and 199%.

So, there’s little change over 3 years but the relative performance over 5 and 10 become far less flattering, especially when you look at net asset value returns.

Of course, this situation could flip if sterling had a prolonged period of strength.

As a UK-based investor, I tend to use sterling-based world indices. As far as I am aware, every other global fund or trust I own does the same. I’m certainly no currency expert, though, so there could be a fine point of detail here regarding RIT’s choice that I am not aware of.

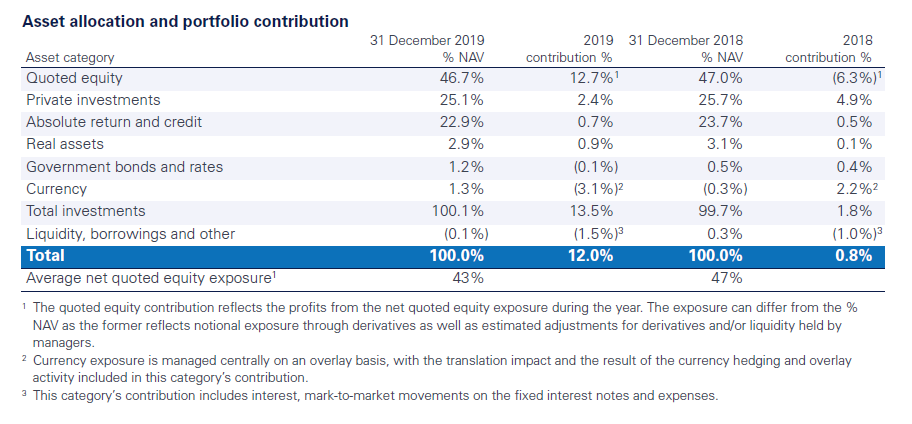

The portfolio

Here’s the high-level breakdown of RIT’s portfolio.

The quoted equity part of the portfolio can be split into individuals stocks (6%), long-only equity funds (30%), and hedge funds (11%).

Likewise, RIT’s private company investments are either directly held (10%) or via funds (15%).

The fund positions typically vary between 1% and 5% of net assets. Most of the quoted equity funds seem to target specific regions while nearly all the private equity funds are US-based. The absolute return and credit funds are nearly all global.

There seems to be a fair amount of churn within the individual stock positions. Impressively, they contributed 5% to net asset value in 2019, despite being only a small part of the overall portfolio.

Perhaps it’s time RIT reversed the recent trend and backed its own judgment a little more rather than relying on fund managers?

The return on real assets last year was also very good, with the gold price doing the heavy lifting here. The year-end weighting of 3% was lower than the average of 6% throughout 2019.

I’m certainly looking for the absolute return and credit part of the portfolio to have a better 2020, relative to the other parts of the RIT’s portfolio.

Having contributed 2.4% to NAV in 2016, it’s returned around a quarter of that the past two years, despite having roughly the same portfolio weighting throughout.

Those charges

Although RIT’s ongoing charge looks reasonable, it’s a different story when you look at the Key Information Document where the figure jumps to nearly 4%.

Interest costs add 0.5% and the underlying costs of funds used another 1.0%. Performance fees and the carried interest within the private equity funds account for 1.6%.

RIT has produced a document giving a bit more background and the way these calculations are being made is still evolving, making it harder to draw definitive conclusions here.

But the shift away from mostly direct investments to more of a fund-based approach seemed to take place about a decade ago. And it has also been RIT’s worst period of relative performance against the wider market.

Summing up

The early signs are that RIT is planning to continue much the way it did under Lord Rothschild. With his family owning over a fifth of the shares and his daughter, Hannah Rothschild, on the Board that’s probably not a great surprise.

But he ran the roost at RIT for nearly 50 years, including nearly all the 30+ years it’s been a listed company.

Having lagged world markets for an extended period now, I’m certainly looking for RIT’s much-touted defensive qualities to prove their worth in 2020.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

And the shares rise 10% on the date I publish this, zapping my argument somewhat!

I know this is the wrong post, but I wondered if you’d heard more about MNL from MS. I find the portfolio fascinating, but the Annual Report is far too brief (especially from the Chairman!) and I have no sense of how the deal with the Subscription for shares works, followed by the Manager selling a load of shares. Creating liquidity was mentioned, but I haven’t seen any explanation of it. So basically I have major governance concerns, which is a shame.

RIT – I suspect performance will gently decline now that Jacob R is off the board – I think he’s hard to replace, both for his mind and his contacts.

I don’t have a problem with the external funds generally, as they tend to be the sort that ‘normal’ investors can’t access, ditto the private equity deals – I think you have to think of it as a way of accessing the parts other funds can’t reach…

However I still don’t have a sense of how to evaluate Ron Tabbouche, whereas Mickey Breuer-Weil always had a good reputation.

Your article on RIT Capital Partners was for me timely. I used to subscribe to ‘Money Week’ and following Merryn Somerset Webb’s IT recommendations I invested in – SMT, RCP,and CLDN. The latter two hardly justify their defensive qualities although they have recovered somewhat recently, whereas SMT never claiming to be defensive has out shined both of them. My concern with all three is how they establish their NAV. All three invest in unquoted stocks, private investments, private equity and the like and it is the NAV which is supporting the stock price.

@tom_grlla

Nothing from MS since my initial contact but I suspect he’s pretty busy so I wasn’t too fussed about chasing it up! The buying and selling confused me a little as well, at it’s pretty unusual for the manager to run his own discount control policy rather than the trust itself! It looks like Kepler are planning a research note on MNL fairly soon, so that may shed some light on the workings behind the scenes.

Difficult to know how the trust will fare without his founder. They were obviously working on the succession for a long time so you would think they looked at aspects like maintaining contacts. And the family continue to be big holders. For me, the funds and the lack of visibility into what they actually hold make it difficult to gauge what’s really going on. So it requires more trust (sic) than usual to keep holding.

@Nigel

Glad you found the article useful. To be fair to both Caledonia and RIT, the share price reaction is somewhat out of their control and we’ll need to see how the NAVs fare over the next few months to see how defensive they have been in this particular instance. SMT’s focus on big tech, which has held up better than most this year, has no doubt been a help.

But you’re right to highlight the uncertainty over part of their NAV. Caledonia has written down its leisure holdings, which have been most affected by the shutdown, but seem to be holding back on writing down everything else on valuation grounds. Given they would typically hold these private investments for several years, and many of them are fairly recent purchases, I’m prepared to cut them a little slack for a while. Their final results in May should add some more colour.

Interesting times … unfortunately!

I went through RCPs chaiman’s statements and what stuck out was how they were prepared to make macro calls about market levels, regions, currencies etc. and stick to them for a number of years. For example they’ve been defensively positioned for some time now because of overvalued equity markets. I have no problem with skilful underperformance like this (same applies to Berkshire Hathaway) so I topped up my holding when HL was showing them at a 20% discount to NAV. Whilst I share your concerns about management changes I bear in mind that the Rothschilds have 250 years of experience in their blood rather than the couple of decades of most top fund managers.

Keep up the good work.

Thanks Tom. Flip-flopping on major calls would be a concern but I haven’t seen any particular signs of that either. Perhaps it isn’t that surprising that the approach has become more conservative in recent years, with the change at the top utmost in their minds.

Just to update this with the March 2020 NAV that was published this morning. It was 1,798p before the deduction of an interim dividend of 17.5p due to be paid on 30 April.

The share price on 31 March was 1,806p so the effective premium then was 0.5%.

Global markets have rebounded 5% in April so far, so if we assume RIT has increased by 4%, its NAV now would be 1,870p versus 1,841.5p for the share price last night plus the dividend due at the end of the month. A discount of 1.5% therefore, but that’s a rough guess at best.

I make RIT’s NAV decline in Q1 2020 as 10.3%. The MSCI World GBP was down 15.5%, so RIT avoided a third of the downward move in markets.

So some downside protection but not as much as claimed in the recent annual reports.

For the sake of completeness, here is how 2020 turned out for RCP.

“The preliminary, unaudited, diluted net asset value of RIT Capital Partners plc (the Company) as at 31 December 2020 (with debt at fair value) was 2,292p per £1 ordinary share (30 November 2020: 2,159p).

This represents an unaudited NAV per share total return (including dividends) of 16.4% for the year. The 2020 NAV performance exceeded both of the Company’s investment KPIs: RPI+3.0% of 4.2% and the MSCI All Countries World Index (50% Sterling) of 12.7%.”

Very decent in the circumstances and now at a 7% discount to its December 2020 NAV. Doubt it will regain its premium rating anytime soon but am happy to continue holding. Might trim my position a little bit for CGT purposes as part of a wider tidying-up exercise.