BlackRock Smaller Companies seems to have come off the boil a little since long-time manager Mike Prentis retired about eighteen months ago. But is this a blip or something more permanent?

Snapping up small caps

This trust has been part of my portfolio for just over three years now. I bought a small amount to start with and then have topped up a number of times in order to build up a more meaningful position size.

I’ve done much the same thing with Henderson Smaller Companies and Acorn Income.

The theory was that I could take advantage of the fact small-cap shares tend to quite volatile but have a great long-term track record. So I could buy a little bit more when the sector fell out of favour and discounts got a bit wider.

So what happened? Well, it kind of worked…

The sector has been more volatile than I expected but it’s hardly alone in that.

And although I’ve bought at lower prices than the trust trades at today, my overall return to date is probably only a few percentage points above the total return over the last three years.

In other words, the volatility did work in my favour a little but you could argue whether it was worth the effort.

Key stats for BlackRock Smaller Companies

- Founded: 1906

- Ticker: BRSC

- Fund management firm: BlackRock

- Manager: Roland Arnold (since Jun 2019, early 40s)

- 10-year net asset return: +227%

- Share price: 1,464p

- Indicated spread: 1,458p-1,470p (0.1%)

- Results released: May (finals) and Nov (interims)

- Market cap: £715m

- Net asset value (NAV): 1,496p

- Discount: 2%

- Costs: 0.7% OCF and 1.2% KID

- Management fee: 0.6% on first £750m and 0.5% above this, no performance element

- Number of holdings: 110

- Gearing: 5%

- Current dividend and yield: 32.5p and 2.2%

- Dividends paid: Jun and Dec

- Sector: UK Smaller Companies (5th out of 19 over the last 10 years)

- Links: Website – AIC page – Kepler report – Citywire webinar

Price details as of 10 November 2020

A little history

BlackRock Smaller Companies has been around since the early 1900s and was previously known as The North British Canadian Investment Company, NB Smaller Companies Trust, 3i Smaller Quoted Companies, and Merrill Lynch British Smaller Companies.

It became BlackRock Smaller Companies fairly recently in 2008.

BlackRock was set up in 1988 but is now reckoned to be the world’s largest fund manager. It had over $7 trillion of assets under management at the end of 2019, making it slightly bigger than Vanguard and well ahead of State Street and Fidelity.

While BlackRock runs nine UK investment trusts, none of them is particularly large. The biggest is BlackRock World Mining, closely followed by BlackRock Smaller Companies and BlackRock Throgmorton. The nine trusts only have a collective market cap of £3bn.

Mike Prentis ran BlackRock Smaller Companies from September 2002 to May 2019. Ronald Arnold worked with Prentis since 2005 and was co-manager of the trust for just over a year before taking over as lead manager in June 2019.

Arnold also manages two open-ended funds for BlackRock. Both have around £500m in assets — one is run along similar lines to BlackRock Smaller Companies while the other is focused on UK blue chips.

A terrific long-term performer

The track record under Prentis was superb. In the sixteen full years that he was in charge, the trust returned 1,190% on a net asset basis and 1,543% in share price terms (equivalent to 19.1% a year compounded).

The trust’s benchmark returned 337% over the same period. And Prentis beat this benchmark in every one of those sixteen years, which is truly remarkable.

Here’s the breakdown by year:

Arnold’s first year to February 2020 made it seventeen benchmark beats in a row. The trust’s share price and net asset value increased by 14% while the benchmark rose just 1.4%.

Year #18 could well see an end to this run, although there are a few months left so things could still change.

At the half-year stage, the share price was down 16% and the NAV by 7%. The trust’s benchmark had fallen just 1%.

A month and a half later, thanks to the vaccine news, the share price is now up 1% since the end of February with the NAV down 1%.

The trust’s benchmark will have recovered as well but I suspect the gap is a lot narrower than it was at the half-year stage.

Investment style

Since Arnold worked with Prentis for so long, the switch in lead manager was probably as seamless as you could ever hope to see.

“High quality, dynamic, growth companies” are preferred. The most recent Kepler report highlights five key criteria that Arnold looks for:

- proven, trustworthy management;

- strong market positions;

- clear record of earnings growth;

- good conversion of earnings into cash; and

- sound balance sheet.

Stock selection is the primary focus but consideration is also given to sector weightings and underlying themes. There aren’t set limits for sector weightings but the trust’s overall sector position is one of the things reviewed at each board meeting.

Up to 50% of net assets can be held in AIM companies although the exact split doesn’t seem to be disclosed.

The trust can’t hold more than 6% of any listed company’s share capital. The last annual report listed 28 positions (just over a quarter of the total) where BlackRock Smaller Companies held in excess of 3% of a company’s shares. The largest stake was just under 5%.

This something I plan to keep an eye on as one concern I have is that the trust could grow too large to carry on investing in the same size companies it has in the past.

The rate of portfolio turnover is middling I’d say. It was around 40% in the year to February 2020 but is likely to be significantly higher in the current financial year. For the first six months, portfolio turnover was 35%.

Given the extreme swings in valuations we’ve seen, that doesn’t seem unreasonable and many other trusts were similarly active on the trading front.

Size matters

The latest portfolio breakdown by size showed 30% consisted of companies valued between £200m and £600m and 40% between £600m and £1.5bn, with a roughly equal split above and below the two extremes.

The top ten holdings in September 2020 accounted for around 20% of net assets, ranging from YouGov at 2.5% down to Treatt at 1.7%. There are currently 110 positions in total, which is much higher than most small-cap trusts.

New additions to the portfolio tend to be between 0.25% and 0.5% in size initially and then built up over time. However, it’s unusual for any position to account for more than 3% of the trust’s NAV.

Only companies valued at less than £2bn are considered as new investments but existing holdings are kept if they go above this value “providing the investment adheres to the original thesis and it remains the most attractive opportunity that can be found amongst a comparable peer group.”

Shares are generally sold within 30 days of being promoted to the FTSE 100, however, which currently has a minimum market cap of around £4bn.

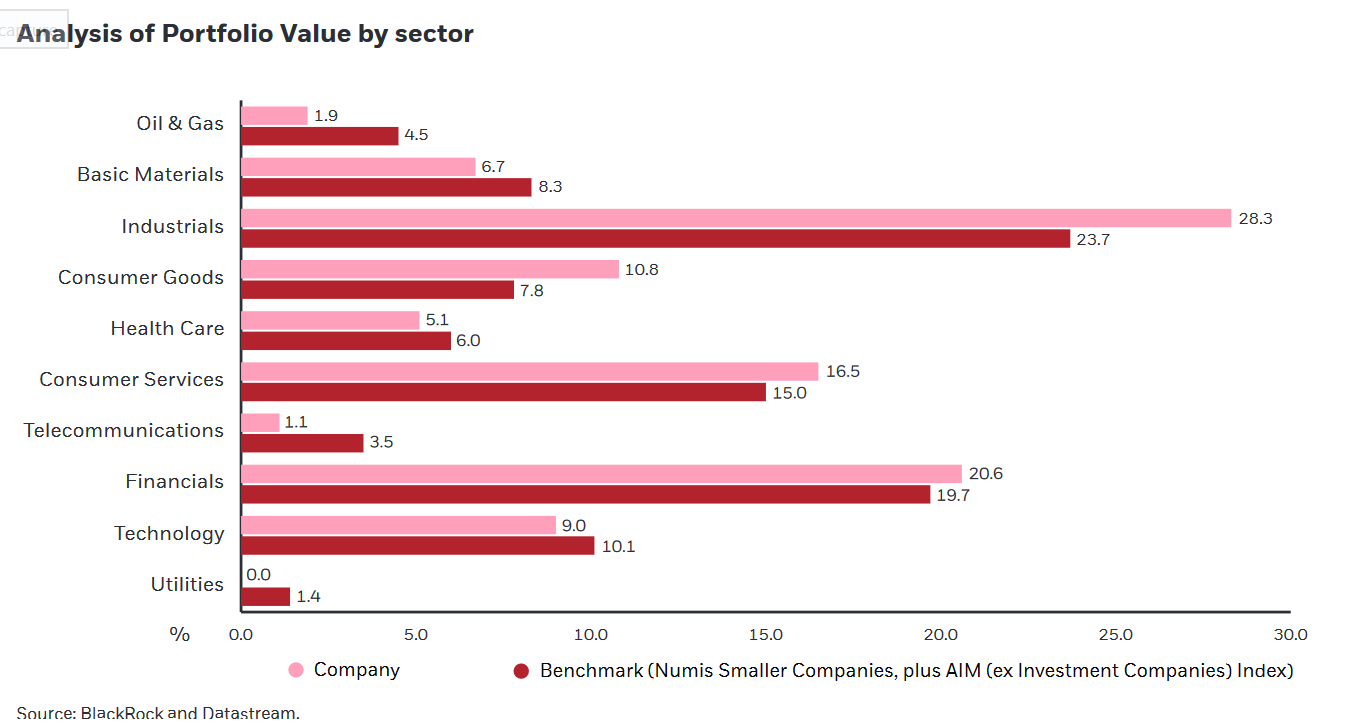

Portfolio analysis by sector

The latest full list of portfolio holdings, as of September 2020, can be downloaded here.

Here’s the sector analysis versus the trust’s benchmark:

More specifically, Arnold says he is overweight media companies, financial companies, aerospace & defence companies, and leisure goods companies.

He’s underweight mining, oil & gas, and food producers, plus travel & leisure. The latter has decreased recently through some purchases of pub companies and a cinema group.

Being slightly underweight in both healthcare and technology in 2020 has also been a handicap you would have thought.

The portfolio review for the half-year to August 2020 was pleasingly humble:

To hold ourselves to account; with hindsight we came into the year with too much exposure to the UK domestic economy, through both consumer and travel & leisure companies.

We felt that the significant Conservative majority in parliament would finally lift the cloud that had been hanging over the UK by increasing the likelihood of progress with Brexit negotiations. With the perceived anti-business policies of the Labour Party no longer a risk, we finally had the catalyst for investors to reappraise the compelling investment case and value proposition offered by UK plc.

However, as the COVID-19 virus began to spread across the world, these sectors were amongst the worst impacted by lockdown restrictions given their exposure to discretionary spending. The issue has been compounded by the re-emergence of Brexit concerns, with investors once again shying away from the UK domestic economy.

Arnold thinks many of these companies “have dealt with the challenges of the pandemic well, having raised money, strengthened balance sheets, and cut costs”. He believes many such shares are “overplaying the downside risks”.

The strong performance of such shares and the trust itself, in the aftermath of last week’s vaccine news, lends support to this point of view.

It’s certainly true that small-cap shares can bounce back quickly when the mood becomes more positive. BlackRock Smaller Companies’ share price went from £1.50 in late 2008 to over £5 in early 2011, for example.

Left in the shade by Throgmorton

It’s interesting to compare the portfolio of BlackRock Smaller Companies with its stablemate, BlackRock Throgmorton.

Throgmorton was also managed by Prentis but Dan Whitestone took over in 2018 after being co-manager for a few years prior to that.

The two trusts are of a similar size, have a similar number of positions, and own many of the same companies.

However, Throgmorton has the ability to short shares, which is pretty unusual for an equity investment trust. It also tends to invest a little bit more in shares listed outside of the UK.

This may be why it has done rather better than BlackRock Smaller Companies recently. From November 2010 to June 2019, the returns of the two trusts were almost identical but since then Throgmorton is up 23% versus 6% for BlackRock Smaller.

Indeed, Throgmorton has traded at a premium for most of this year and is now considering a placing on top of regularly issuing new shares to soak up the high demand for its shares.

It will be interesting to see if the relative performance of these two trusts continues to differ or if this was a one-off.

Dividend growth on hold

BlackRock Smaller Companies has increased its dividend each year since 2004.

Growth was pretty sedate from 2004 to 2010 but over the last ten years, the payout has increased by an impressive 19% a year on average.

The current financial year is likely to change all that of course.

The interim dividend was held at 12.8 pence but the earnings supporting this fell from 22.2p last year to just 4.6p. Even adjusting for special dividends received last year, the fall in income from the portfolio was 68%.

There are still revenue reserves of £17m, greater than the full-year payout of £15m, and the capital reserves are distributable as well.

However, the final dividend may still be “re-assessed” depending on how payouts recover over the next several months. It won’t be formally declared until May 2021.

Gearing used sparingly

BlackRock Smaller Companies is usually fully invested with a little borrowing on top to juice returns.

Gearing can go up to 15% but between 5% and 10% seems most typical.

There are three long-term borrowing facilities in place that total £60m.

One of these, for £15m, expires in 2022. This has a coupon of 7.75% which will be nice to see the back of.

The other two long-term loans were secured more recently and charge a more palatable 2.74% and 2.41%. These are due to be repaid in 2037 and 2044 respectively. The latter of these was taken out as a replacement for the £15m loan due to mature in 2022.

There are also two short-term debt facilities that can provide an additional £45m of borrowing when required.

At the end of August 2020, £10m of the short-term facilities were drawn down, giving a total debt figure of £70m. There was £44m of cash of the balance sheet offsetting this.

Discount control

There doesn’t seem to be any formal discount control policy in place.

The trust has the authority to issue up to 10% of new share capital or buy back up to 15%, should the directors think it will benefit shareholders. That’s fairly standard.

The discount to net assets has fluctuated quite a lot over the past decade, from a discount of up to 20% to a small premium at the end of 2019.

However, although a handful of shares were issued in late 2019 and early 2020, I don’t think there have been any buybacks since 2003.

In other words, the directors seem to have been happy to let the discount just do its thing.

Low charges

The charges seem pretty reasonable here. As one of the largest trusts in the sector, it’s also one of the cheapest.

A 10% performance fee was in place but it was removed in March 2018. It had a fairly low cap of 0.25% of net assets a year, which was often hit.

In return for the performance fee being dropped, a slightly higher basic management fee was introduced of 0.6% up to £750m of net assets and 0.5% above that level.

Overall, as a result of the fee reshuffle in 2018, total costs were reckoned to come down from 0.9% a year to 0.7%, assuming a full performance element was due. So, it was a meaningful reduction.

The Key Information Document figure of 1.25% breaks down into 0.33% for transaction fees and 0.92% of ongoing costs. I assume the latter includes a little for interest costs, which aren’t included in the standard ongoing charge.

Skin in the game

As of February 2020, the five directors held around 100,000 shares between them, worth a total of around £1.5m.

However, 91,000 of these were held by one director, Robert Robertson, who has been on the board since 2008.

The chairman, Ronald Gould, who joined the board in April 2019, bought his first 1,000 shares earlier this month. That turned out to be nicely timed as it was just before the rally prompted by the vaccine news.

The trust is about to introduce a rule that will limit the service of directors to nine years or twelve in the case of the chairman. This will probably see three directors, including Robertson, leave in the next year or so.

A new director, Mark Little, was appointed in October 2020 as the first of three likely replacements.

There’s no information on the number of shares held by Arnold or by other BlackRock employees.

In summary

After a brief honeymoon period for Arnold in 2019, this year has proved a lot tougher.

I liked the mea culpa in the latest results, though, and it’s hard to say what Mike Prentis would have done differently in the circumstances.

BlackRock Smaller Companies certainly hasn’t been alone in its struggles. Indeed, it is still ahead of the sector average return over the last year.

When I wrote about this trust last summer, I highlighted the fact it was unrealistic to expect its benchmark-beating form to continue indefinitely, obviously jinxing it in the process!

But, as we saw last week, when this sector moves, it doesn’t muck about. It doesn’t take much of a mood change to alter the picture.

With themed investments like this, you have to be prepared to take the rough with the smooth. Of course, writing that is easier than doing it. My UK small-cap holdings have certainly weighed down my overall performance this year and they are still underwater, despite the recent rally.

Yet I still think the case is strong for small-cap trusts to perform well over the long term (five years and beyond) and BlackRock Smaller Companies’ focus on growth should keep near the top of the pile.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Hey IT, great article as usual. Been meaning to buy some of BRSC, might do it when it pulls back to 1400 as I missed the big vaccine bump.

By the way, what are your thoughts about Asia-focused ITs? I had my eyes on Asia Dragon Trust and Schroder Asian Total Return. Any ones in particular you like? I realize I am slightly late to the party here but better late then never…

Thanks M. I haven’t looked at Asia trusts for a while now, except for a piece I did on the 3 China specialists a few months ago: https://www.itinvestor.co.uk/2020/09/china-investment-trusts-come-of-age/

The Baillie Gifford and JPMorgan Asian and Japanese trusts all seem to have done very well recently but I have no idea whether they will continue to do so.

Thanks ITInvestor, will read it now.

P.S. Totally agree with you that nobody knows if these funds will continue to do well, in fact I think they are overvalued and I hate buying at the historical top, but with Biden’s election “win” I see China profiting massively in the next few years\decades and feel like I need to have a position there to protect against US imminent decline.

BGCG has now (well, 26 Nov) managed to get shareholder approval to issue more shares so I’m hoping this will bring its premium down to a more palatable level!

Seems like a risky portfolio, 12.28% in BABA and 10.41% in Tencent. Probably can just buy these 2 and do better without paying their fees. Would be much more impressive if they would have achieved this performance with smaller positions (4-5% of entire portfolio) over multiple stocks.

That’s actually less their weighting in the main China index. In MSCI China, Alibaba is 20% and Tencent is 16%. I think all three China trusts have what looks like high weightings to these two companies but I think they are all actually underweight.

Just to round this one off with the end result for year #18 to 28 Feb 2021:

https://investegate.co.uk/blackrock-smaller-companies-tr/prn/final-results/20210507161532P3375/

NAV return: +16.1%

Share price: +17.2%

Benchmark: +24.9%

All with income reinvested. So the record run has indeed come to an end although BRSC is still ahead over 3, 5, 10, and 15 years (which isn’t that surprising given the 17 annual beats on the trot!)

The annual dividend was raised by 2.5% to 33.3p despite revenue per share falling 64% to 13.6p. Revenue reserves remaining are about 1 years of dividends.

Great post. Thanks.

What’s your current thinking on BRSC, three years later?

I still hold and have topped up my initial holding quite a few times although it is still one of my smaller positions overall and I have roughly the same amount in Henderson Smaller Companies (HSL). Not a lot seems to have changed about the way either trust is run as far as I can tell over the last few years but I’m happy with that as I don’t want to see frequent strategy shifts.

I would have preferred to see a bit more in the way of buybacks at both BRSC and HSL, especially when the discount reached the 15% level. A lot of trusts in the sector seem reluctant to do much unless their discounts are noticeably wider than others in the sector. BRSC has done a little in the way of repurchases but not much. T

If I was choosing some small-cap trusts today, I would probably mix them up a bit more as quite a few like HSL, BRSC, AUSC, MTU and so on have a fairly similar growth style and are more correlated than I initially appreciated. For example, I might have added a third trust from one of the concentrated/private equity style trio of Odyssean, Rockwood, and Strategic Equity Capital or perhaps one of the European small-cap trusts.

Hope that’s useful.