Baillie Gifford’s newest investment trust, Keystone Positive Change, got off to a volatile start earlier this year but its managers have their eyes fixed firmly on the long term.

Perhaps somewhat hastily, I took an initial stake in Keystone when it proposed the manager change in late 2020.

I added a little more before the decision was ratified by shareholders in mid-February. Then I topped up again when the share price sank in March when tech/growth seemingly fell from favour.

My position size is about where I’d like to be now, so I’m not planning on buying any more shares for the time being. The ups and downs of the share price over the last few months have left me a few per cent below water though.

Now Keystone has published its first results under Baillie Gifford’s management, let’s see how things are shaping up.

Key stats for Keystone Positive Change

Note that the recent manager change makes the 10-year NAV return pretty meaningless, but I have included it for completeness.

- Founded: 1954

- Ticker: KPC (was KIT prior to 11 Feb 2021)

- Managers: Kate Fox and Lee Qian from 11 Feb 2021

- Management firm: Baillie Gifford (was Invesco up 10 Feb 2021)

- Share price: 310p

- Indicated spread: 308p-312p (1.3%)

- Market cap: £192m

- Net asset value (NAV): 314.2p

- Discount to NAV: 1.3%

- Costs: 0.55% OCF and 1.1% KID

- 10-year NAV total return: +101%

- Benchmark: MSCI All Countries World Index

- AIC sector: Global

- Year-end: 30 Sep

- Results released: Apr/May (interims) and Dec (finals)

- Current dividend and yield: 11.2p and 3.6%, but will be significantly lower and possibly zero from 2022 onwards

- Dividends paid: Mar, Jun, Sep (interims) and Dec (final), no interims from 2022 onwards

- Links: Website – AIC page – Kepler Feb-21 review – Retail webinar

Price data as of 30 Apr 2021

What is Positive Change?

Baillie Gifford’s Positive Change team is led by partner Kate Fox and investment manager Lee Qian and consists of seven full-time professionals.

They look for high-quality growth companies, similar to Baillie Gifford’s other trusts and funds. However, in addition, the companies owned by the trust should also make a positive impact on society and/or the environment.

The net is cast pretty wide when it comes to what is classed as a positive impact and Fox says the less obvious ideas are often among her personal favourites.

When it comes to public-facing funds, the team runs the £2.4bn Baillie Gifford Positive Change open-ended fund, which launched in January 2017, in addition to the £190m Keystone Positive Change.

Investing style

It’s a concentrated low-turnover investing approach.

The open-ended fund aims to own 25-50 companies and had 33 as of December 2020. Portfolio turnover is expected to around 20% a year, on average, and the March 2021 factsheet notes it as 19%.

Keystone Positive Change is aiming for 30-60 companies and had 33 as of March 2021. Its portfolio turnover should be similar at 20% a year.

Both the fund and the trust are looking to beat the MSCI All Countries World Index by 2% per annum over rolling five-year periods.

The three key differences between the trust and fund will be:

- Keystone can employ gearing — Baillie Gifford trusts that use gearing typically have a high single-digit percentage;

- Keystone can buy slightly smaller companies — down to $500m rather than $1bn for the fund; and

- Keystone can buy private companies — 5-10% in unquoted firms within 3 years is the expectation, gradually increasing thereafter with authority to go up to 30%.

Right now, the fund and the trust look very similar indeed. The top 10 positions are the same in both, with 51.8% in these holdings for the trust compared to 49.9% for the fund.

No significant gearing has been employed yet and no sub-$1bn or private companies been purchased. However, no doubt this will all change over time.

It’s fair to say that the open-ended fund has done spectacularly well since launching, sucking in an extraordinary amount of new money, as this table shows:

| Year/period to | Assets | Return |

|---|---|---|

| Dec 2017 | £15m | +43% |

| Dec 2018 | £63m | +5% |

| Dec 2019 | £192m | +26% |

| Dec 2020 | £2.0bn | +80% |

| Apr 2021 | £2.4bn | +6% |

Since inception in January 2017 through to March 2021, the open-ended fund was up 33% a year, relative to 11.1% from MSCI All Countries World Index.

A large chunk of that lead over its benchmark was generated in 2020, with the fund very roughly 10% ahead in 2017 and 2018 and level in 2019.

Four types of company

The portfolio is split into these four categories:

Simple enough.

The idea generation process is organic in nature, with no sector restraints envisaged.

Here’s a screengrab from Keystone’s recent webinar that outlines the investment process. Unfortunately, the video was a little blurry.

To summarise, Fox says companies need to meet both aims of high-quality growth and positive impact to be considered.

Ideas are reviewed first from a financial point of view and then an impact analysis is carried out to assess what positive impact the company might have.

Once in the portfolio, stocks are discussed weekly with fuller portfolio reviews every 6 weeks. There’s also ongoing monitoring and engagement with each company.

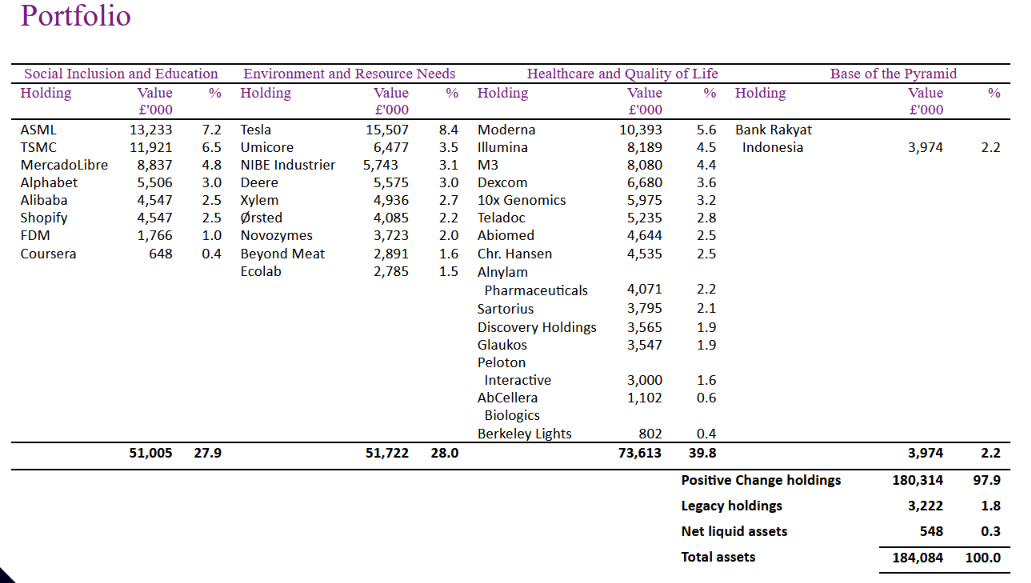

The current portfolio

Here’s how Keystone’s portfolio looked as of March 2021:

There are some very well-known companies here, particularly among the largest positions. Tesla is Keystone’s largest holding although quite a few other Baillie Gifford trusts reduced their position size in it earlier this year.

Fox says the largest overlap with other Baillie Gifford trusts is about 20% with Scottish Mortgage.

I believe that Tesla, ASML, Alibaba, Alphabet, MercadoLibre, Shopify, Moderna, Alnylam, and Illumina are held by both Keystone and Scottish Mortage.

However, Keystone’s more concentrated approach means it has larger stakes in most of these companies. Indeed, it looks to have around 40% in these nine positions (presumably the 20% figure is what Scottish Mortgage has in these companies).

Baillie Gifford seems to own the same type of companies across many of its trusts. So, although the names of the individual holdings may differ, the share price of the trusts themselves often move in tandem. Those with a narrower focus tend to be volatile, though.

Social rather than environmental?

It’s tempting to make a remark about the base of the pyramid looking rather small, but I was a little surprised to see just one company under that heading. Had I read the open-ended fund’s 2019 Impact Report more closely, I would have realised that was likely to be the case as the open-ended fund has a similar set-up.

Healthcare/quality of life is the biggest of the four categories right now, both in overall weighting and the number of companies held.

Overall, I’d say the portfolio leans heavily towards positive social change rather than positive environmental change.

A full portfolio as of February 2021 was also published so we can see that Coursera, Peloton, AbCellera, and Bank Rakyat were bought in March.

The trust’s interim results, published last week, added a little detail on two of these recent additions:

Firstly, Peloton, which is a pioneer of connected fitness equipment for use at home and has an ambitious goal of achieving 100 million subscribers over the coming decades. The beneficial effects of fitness are well known and include lower risk of heart disease, stroke, diabetes, depression, dementia, and certain types of cancer. By lowering friction and, over the medium term, cost, we believe Peloton will help drive better health outcomes alongside being a profitable and growing business.

Secondly, AbCellera, which performs antibody discovery services for pharmaceutical and biotech partners. The company increases the speed of antibody discovery and potentially discovers better quality antibodies by leveraging on its in-house technology. By achieving this, we expect AbCellera to help improve and expand antibody treatments for large patient populations suffering from some of the world’s most common diseases, including cancer. A meaningful share of the antibodies therapeutic market could lead to a very attractive investment outcome.

These two investments were funded by reductions to Alphabet and Japanese medical platform, M3.

Three fund holdings not in Keystone

There are three holdings that were in the open-ended fund at the end of 2020 that are yet to appear in Keystone:

- HDFC — 3.0%

- Kingspan — 3.0%

- Safaricom — 0.6%

HDFC is an Indian bank and classed under ‘Social Inclusion and Education’ (it’s also held by Monks) while Kenyan mobile firm Safaricom sits in ‘Base of the Pyramid’. Both of these will probably be added to Keystone’s portfolio soon, I suspect.

Kingspan has been embroiled in the Grenfell scandal and after waiting to see how that situation developed, Baillie Gifford now seems to be selling down its position so it seems unlikely it will appear in Keystone’s portfolio anytime soon.

Reviewing the first few months

We all like our investments to get off to flying starts, so they can begin life with a little green in our portfolio.

Sadly, as often happens, that wasn’t the case here although I suspect it’s something that will be largely forgotten a few years down the line.

The Keystone of old was a UK trust with a big value slant. It also had quite a high percentage of less liquid holdings, so 40% of the old portfolio was sold down prior to the vote on the manager change on 10 February.

Only half of Keystone’s shareholders voted, but nearly 96% of them were in favour.

It looks the new portfolio only took a week or two to compile as the end of February valuation showed just 6% in legacy assets and cash.

However, that early sell-down of the less-liquid 40% meant Keystone missed some of the early stages of the value rally in January and February and then switched into growth stocks pretty much when the NASDAQ market peaked in mid-February.

Had the vote on the manager change been at the end of March, it would have been a completely different story. But it’s impossible to predict such things so I’m pretty relaxed about it. It’s pleasing to see Fox and Qian haven’t overreacted to the recent volatility either.

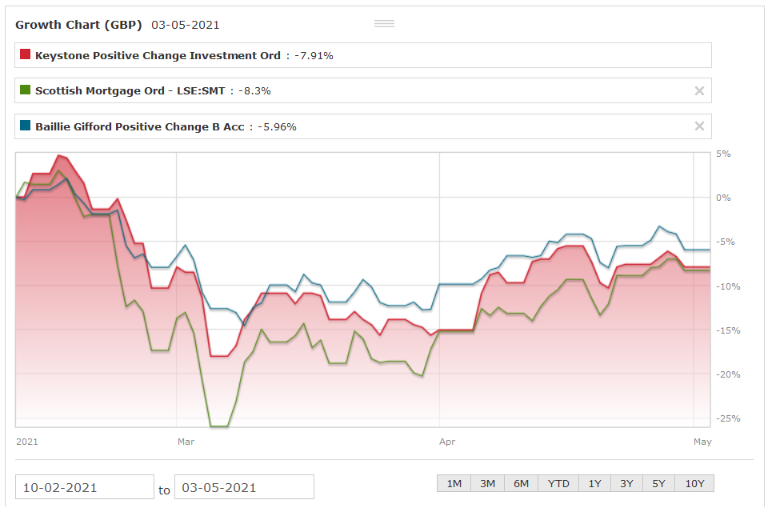

Of course, this wasn’t just a Keystone thing as it also affected many other Baillie Gifford trusts and funds. Here is Keystone, the open-ended fund, and Scottish Mortgage for comparative purposes.

In just a few weeks, Keystone fell nearly 20% and Scottish Mortgage over 25%. They’ve both since recovered to just 8% down. The Positive Change fund fared slightly better, losing 6%.

However, it’s a good illustration of just how volatile this trust might be, given its focus on growth companies. Although these type of stocks have been on a seemingly relentless rise for a decade, when they do fall, they seem to fall a lot faster and harder than the overall market.

Discounts and premiums

The Keystone of old was a regular buyer of its own shares last year because its discount to NAV widened to 20%.

The news of the manager change narrowed the discount to around 5% and since the vote was passed, it’s traded anywhere from a premium of a few per cent to a discount of a few per cent.

No share repurchases or new share issues have been made since September and the trust has the usual standard authority to issue up to 10% of its shares or buy back 15% without seeking permission from its shareholders.

A couple of large holders from the Invesco days — Wells Fargo and 1607 Capital Partners — seem to be gradually selling down their positions.

Wells Fargo dipped below 11% at the end of April and 1607 dropped to 9.5% in mid-February.

Both these companies are labelled as value investors, so it seems more likely than not that they will continue selling although they don’t seem to be in any particular hurry.

But it’s worth noting that continued selling pressure from these two could cause the discount to widen a little from its current level.

Skin in the game

The five directors increased their combined holding in Keystone shares from 48,100 to 74,300 (an increase of about £100,000) in early December when the manager change was first proposed.

Apart from dividend reinvestments, one director added another 3,500 shares (£10,000) in late March in what looks now to be a pretty well-timed purchase.

Baillie Gifford doesn’t seem to publish the number of shares owned by its employees as far as I can tell. But this information usually only appears in the full annual report, which won’t be available until December anyway.

Charges

As with all of Baillie Gifford’s trusts, the charges are on the low side.

Its management charge is waived for the first six months and then will be:

- 0.70% of the first £100m of market cap;

- 0.65% between £100m and £250m; and

- 0.55% in excess of £250m.

There is no performance fee.

The base management charge is actually a little higher than it was under Invesco so the trust’s next published cost figure may nudge up close to 1% once admin costs are added to the mix.

That will make the trust quite a bit more expensive than the 0.53% total charges levied on the open-ended version, but then the latter is twelve times the size.

Dividends

Finally, just a quick note on the dividend.

Keystone is keeping its 2021 dividend flat compared to the previous year so that means there will be three interims of 2.4p per share in March, June, and September followed by a 4.0p final in December for a total of 11.2p.

From 2022 onwards, the dividend will just be the minimum required to retain investment trust status, i.e. 85% of income less expenses.

As the open-ended version only has a trailing yield of 0.3%, the trust’s higher expenses may mean it pays no dividend at all.

In summary

In a recent interview with the soon-to-be-retired Charles Plowden, senior partner of Baillie Gifford, he said he regarded the firm’s investment trusts almost as a shop window for the larger wall of institutional money the firm manages elsewhere.

Indeed, its trusts, with £32bn of assets in total, account for just under a tenth of the £340bn Baillie Gifford looked after at the end of April.

I’m not sure I’m that keen to be thought of in that way, but I am happy to take a long-term view on this position. I’m expecting to see a lot more volatility along the way but also to be compensated for that by higher returns.

The more I hear Baillie Gifford’s various managers speak, the more I like their way of thinking, such as not worrying about short-term news, focusing on how the company is performing, thinking in decades, and not getting carried away by the bumper year they had in 2020.

I may well add more of the firm’s trusts to my portfolio over the next few years but I’m still mulling over exactly which ones.

Scottish Mortgage feels like a one-stop-shop for the best that Baillie Gifford, or perhaps Monks if I want to dial down the volatility a bit.

The likes of Baillie Gifford US Growth and Baillie Gifford China Growth could be interesting as well, although I would expect them to be more volatile than Keystone.

Schiehallion is another interesting trust, as it focuses purely on BG’s unquoted expertise, although I think it’s more difficult to buy in decent size.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

As usual a very useful review.

The pace of change following the move to BG is remarkable – the costs of trading alone will have had a measurable effect on performance in that first month. Shame about Pelton today.

You comment on the overlap between the various BG fund holdings. When the much larger aggregate institutional mandates are taken into consideration there perhaps starts to be a potential issue of liquidity……

On Schiehallion, I bought some earlier this year and found no problem dealing in a reasonable size – to my pleasant surprise dealt well inside the quote. I suppose it depends on your definition of “reasonable size”. It is, though, in the “specialist” sector and so not available (or indeed appropriate) for all.

Thanks Phil. Interesting to hear that about Schiehallion although I have found some trusts can be easy to buy but a lot harder to sell in an equivalent volume. Of course, ideally, you don’t want to sell but it’s useful to have an exit plan in case things don’t pan out the way you expect.

You can look at BG’s 13-F disclosures in the US to get a feel for their largest holdings. This one allows you to sort by % held and you can see there are quite a few over 10%. Among KPC’s big holdings, BG is in quite deep with Moderna and Illumina.

https://whalewisdom.com/filer/baillie-gifford-co#tabholdings_tab_link

Yes indeed, liquidity can become a real problem in falling markets, and not just for trusts, of course. I have my eyes wide open on this – 30 years as a private-client stockbroker was a good teacher!

Hi, what platform do you use to invest? I’m currently using Vanguard’s platform, but I’m unsatisfied with the lack of choice. Looking forward to hearing from you.

Hi Faris, our family holdings are spread over a number of the major platforms but I’d rather not list them out here. I think Vanguard is fine if you want a relatively low-cost way of just holding their funds and ETFs but you’ll need another broker if you want to buy investment trusts and so on.

Monevator’s broker comparison table is the place I normally check to see how all the platforms compare on costs and main features: https://monevator.com/compare-uk-cheapest-online-brokers/

However, it’s worth noting that we are still seeing a fair amount of consolidation, such as ii’s purchase of EQi which is expected to take place this summer. So you could choose one broker only to see your account moved to another platform a short time later.

All the Baillie Gifford investment trusts are trading at premiums (apart from Keystone, on a small 2% discount) and have higher charges than their open-ended siblings. So although I’m a fan of closed-ended funds, for the BG range of ITs I struggle to see the investment case.

Schiehallion is a fascinating one (sorry to be slightly off-topic). There’s a) the Premium, b) the C-share that’s trading now, and finally c) the quoted part of the portfolio.

Affirm was one of the first to list, and it popped on IPO day – the timing was right. It’s now down by… 50% and below the listing price.

Hopefully it’s still worth more than they paid, but given the volatility of these Unicorn companies on listing, the more that list, the more volatile the NAV may be.

The problem is that their ‘USP’ is that they don’t sell on IPO, unlike other VCs. But in the current market with such frothy valuations, selling on IPO does make sense in certain stocks (personally, I was always sceptical about Affirm – BNPL with an overreliance on Peloton as a client is not my bag), though I see the appeal of holding e.g. AirBnB and Stripe for the long-term.

Keystone… I’ll be honest, I don’t really get the ‘green’ angle here, but I suppose it’s good that it’s becoming more popular. It just so often feels box-ticking-y. I think the Stewart Sustainable team do the best job at this sort of thing.

Yes, I’ll probably do a follow-up piece on Schiehallion at some point – I did a pre-IPO piece in March 2019 then a very brief follow-up after six months so I could do with a refresher!

With Keystone and its bigger open-ended cousin, it’s definitely a very broad definition and less environmentally focused than the like of Impax and other sustainable funds from what I can tell.

There’s an interesting Liontrust launch coming up in this area soon: https://investegate.co.uk/liontrust-esg-trust/rns/intention-to-float/202105070700038486X/