Worldwide Healthcare Trust reckons it is the best-performing investment trust since it launched in April 1995. It’s returned 4,082% which works out at 15.8% annualised.

What’s more, it’s beaten its benchmark, the MSCI World Health Care index, by over four percentage points a year.

Incredible stuff although it’s worth adding a little context.

The AIC lists 393 investment companies and VCTs in its stats at the moment.

Less than a quarter of them, 88 in total, are older than Worldwide Healthcare. So while it’s top, it’s top of a smaller pile than you might have imagined.

And being extra picky, since Worldwide Healthcare made this claim a few months ago, I think HgCapital Trust has crept ahead of it.

Still, such a high return and, more importantly, over such a long period can only be applauded.

Key Stats for Worldwide Healthcare Trust

- Founded: 1995

- Managers: OrbiMed: Sven Borho (aged 53) and Trevor Polischuk (50-ish?)

- Ticker: WWH

- 10-year net asset return: +440%

- Benchmark: MSCI World Health Care

- Current price: 3,547.5p

- Indicated spread: 3,545p-3,550p (0.1%)

- Market cap: £2.1bn

- Net asset value: 3,532p as of 16 Sep 2020

- Premium to net assets: 1%

- Costs: 0.9% OCF and 2.0% KID

- Net cash: 3% as of 31 Aug 2020

- Number of holdings: 78

- Current dividend and yield: 25p and 0.7%

- Results released: Jun (finals) and Nov (interims)

- Dividends paid: Jan and Jul

- Continuation vote: every 5 years, next one in 2024

- Sector: Biotechnology & healthcare (3rd out of 4 over 10 years)

- Links: Website — AIC page — Edison reports

History

Worldwide Healthcare was originally called Finsbury Worldwide Pharmaceutical when it was launched back in 1995.

Its original management company, M&I Investors, was founded by Viren Mehta and Sam Isaly in 1989.

Metha and Isaly went their separate ways in 1998 with Metha founding Metha Partners and Isaly setting up OrbiMed with Sven Borho and Carl Gordon.

The initial brief was to just invest in drug companies. 60-80% was put into 10-15 major pharmaceutical companies with the balance in speciality pharmaceutical and smaller biotech firms.

In 2010, its remit was expanded to include healthcare equipment & technology, and service providers. The benchmark was switched from the Datastream Worldwide Pharmaceutical And Biotechnology Index to the MSCI World Health Care Index to reflect this change.

And the trust altered its name to Worldwide Healthcare.

As an aside, it’s interesting to note how well many of the old Finsbury investment trusts have done over the years.

Finsbury Growth & Income, managed by Nick Train, is the only trust to still use the Finsbury name I think. Its ten-year return is nearly double that of its 24 sector rivals in the UK Equity Income sector.

Finsbury Technology eventually became the top-performing Allianz Technology Trust while Finsbury Life Sciences ended up as Biotech Growth (which is also run by OrbiMed).

I believe there were a couple of other Finsbury trusts but my Googling skills weren’t up to the job of tracking them down.

Finsbury Asset Management, who originally performed all the trust’s admin functions, has gone through multiple changes as well over the years. It was bought by Rea Brothers not long after the trust launched. Rea Brothers was then bought by Close Brothers in 1999.

After a reorganisation at Close Brothers in 2007, the trust admin team set up a new firm called Frostrow Capital. Frostrow now runs the admin side of Finsbury Growth & Income, Worldwide Healthcare, Witan, Fundsmith Emerging Equities, and several other trusts.

Scandal and a change of manager

Sam Isaly was the lead manager for the trust from inception to late 2017.

In December 2017, he was accused of harassment and a few days later he was removed as portfolio manager and as a director of Worldwide Healthcare.

Sven Borho and Trevor Polischuk took over the reins. They had been listed in the trust’s accounts since 2015, alongside Isaly as a three-person management team, but I’m not sure how deep their involvement was before that.

However, Borho helped set up OrbiMed and has been a portfolio manager for M&I then OrbiMed since 1993. Polischuk joined OrbiMed in 2003. They certainly don’t lack experience!

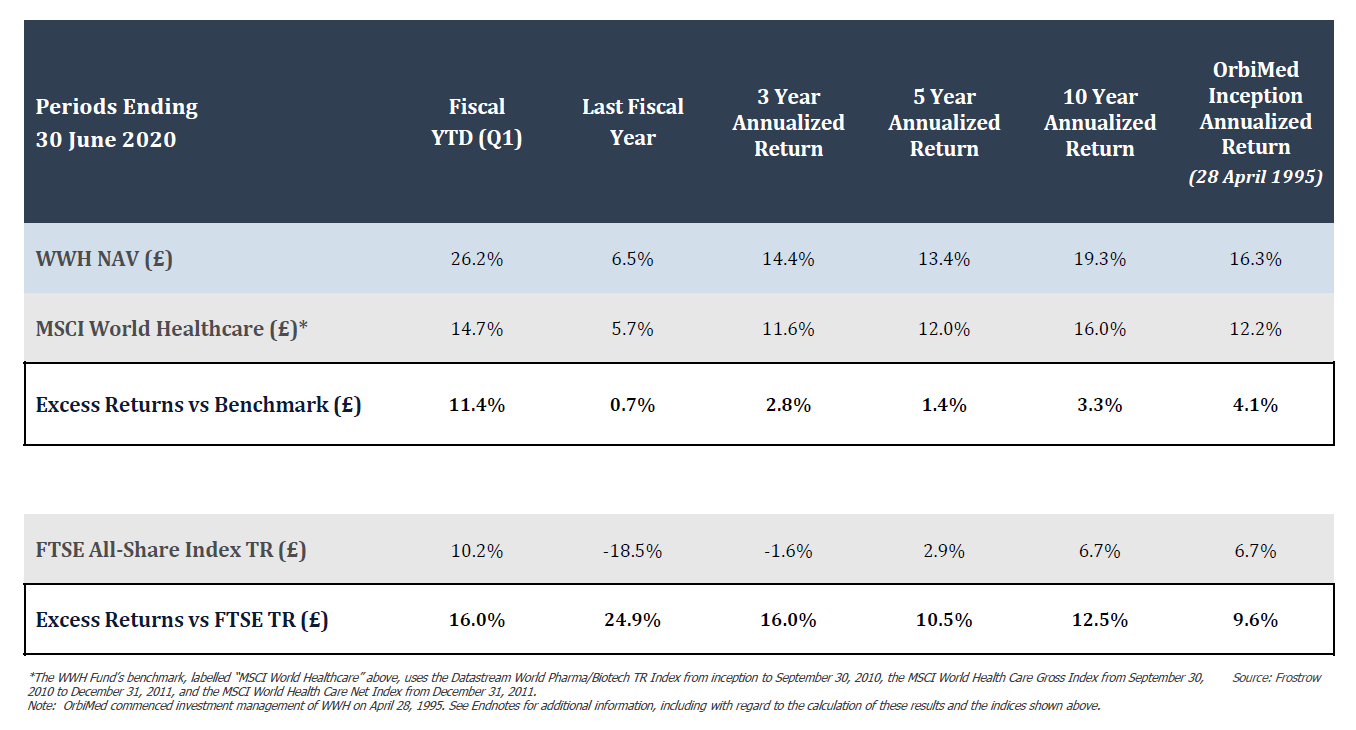

Performance

Here’s a little more detail on Worldwide Healthcare’s performance over time:

Healthcare spending as a proportion of GDP has doubled for most major economies to 10-12% over the last few decades but it’s more than tripled for the US.

{kind=link}

That trend is expected to continue and be reinforced by demand from the likes of China, India, and other emerging markets over the next few decades.

Put simply, there are more patients every year and they are getting both richer and older.

That means healthcare has been a great place to be invested over the last 25 years, crushing the returns available from the UK stock market.

On a global basis and in US dollar terms, the sector is up 11.2% a year since the start of 1995, comfortably ahead of the 7.9% a year the MSCI World Index has returned.

One thing that does stand out to me is how Worldwide Healthcare’s lead over the sector has generally narrowed over time. Although the outperformance in the second quarter of 2020 was startlingly good, it is only three months.

As the trust has grown, I suspect it has become a little less nimble. Back in 1997, its portfolio was less than £70m whereas it is now over £2bn.

But the departure of Isaly doesn’t seem to have had that much of an effect. The excess returns over three years are greater than those over five, for example.

Although the last five years have been pretty strong, the first half of the 2010s was even more impressive, with the very strong performance of the biotech sub-sector providing rocket fuel for the trust’s returns.

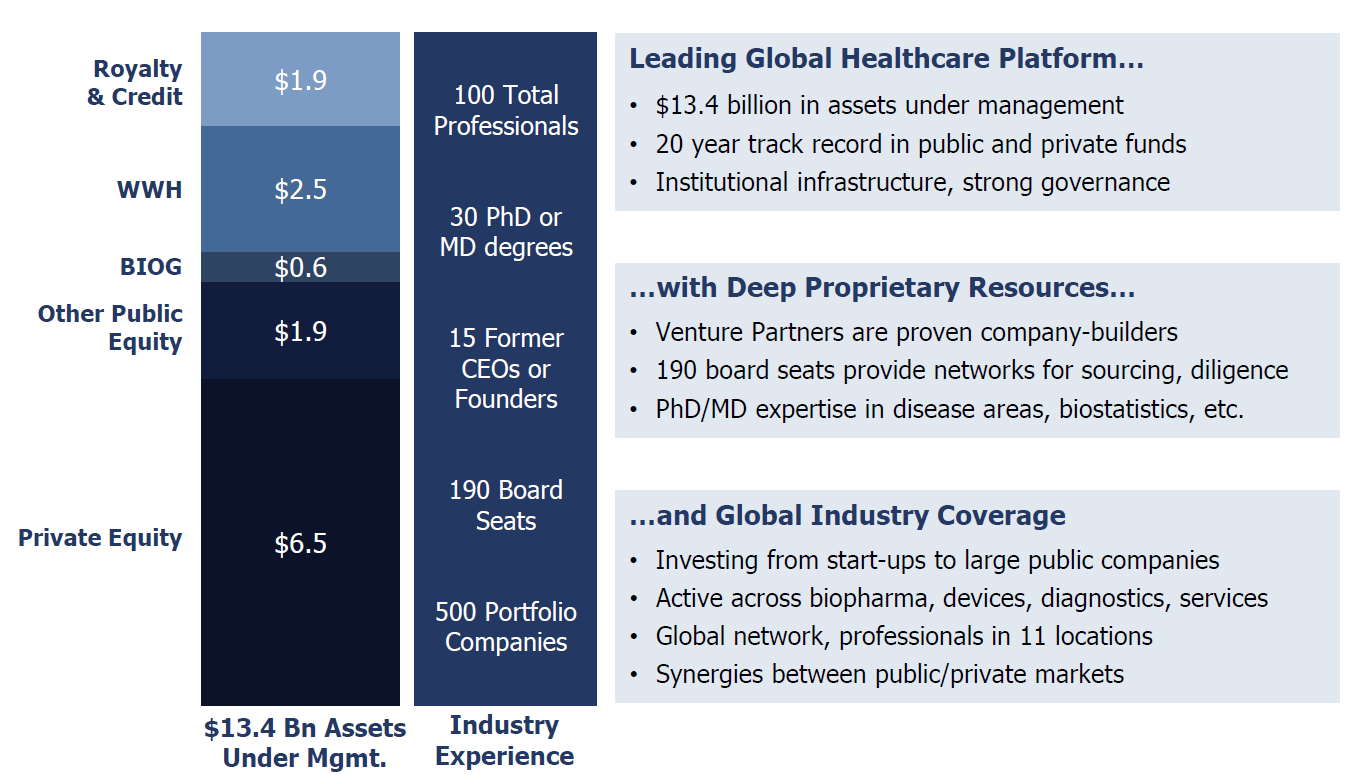

OrbiMed’s range of funds

OrbiMed had $13bn of assets under management as of March 2020, making it one of the largest healthcare investment specialists in the world.

If Worldwide Healthcare’s performance since then is any guide, that assets figure is probably around $17bn now.

Here’s a breakdown:

Worldwide Healthcare is described as the flagship and ‘best ideas’ fund in presentations made by Borho, which is a nice thing to hear.

The two UK investment trusts it looks after account for a quarter of its assets, which is also reassuring.

Nearly half of its assets are in private equity, which should give it good insight into the young upstarts and the latest trends in this sector.

Investment policy & process

According to a recent Edison report, “stocks are selected from an investible universe of around 1,000 companies, from early-stage preclinical businesses through to multinational biopharmaceutical firms. The managers seek companies with underappreciated product pipelines, robust balance sheets, strong management teams, and which are trading on reasonable valuations”.

OrbiMed is increasingly looking towards Asia but the US still dominates its portfolio with a 70% weighting.

Here are a few of Worldwide Healthcare’s self-imposed restrictions:

- at least 50% of the portfolio will normally be invested in larger companies (i.e. with a market capitalisation of at least U.S.$10bn);

- at least 20% of the portfolio will normally be invested in smaller companies (i.e. with a market capitalisation of less than U.S.$10bn);

- investment in unquoted securities will not exceed 10% of the portfolio at the time of acquisition;

- a maximum of 5% of the portfolio, at the time of acquisition, may be invested in each of debt instruments, convertibles and royalty bonds issued by pharmaceutical and biotechnology companies; and

- a maximum of 30% of the portfolio, at the time of acquisition, may be invested in companies in each of healthcare equipment and supplies & healthcare providers and services.

Right now, unquoteds (1.0%) and debt instruments (0.7%) are a bit of a sideshow but the two healthcare sectors are a major feature at around 25% of the portfolio, although their weighting in the trust’s benchmark is much higher.

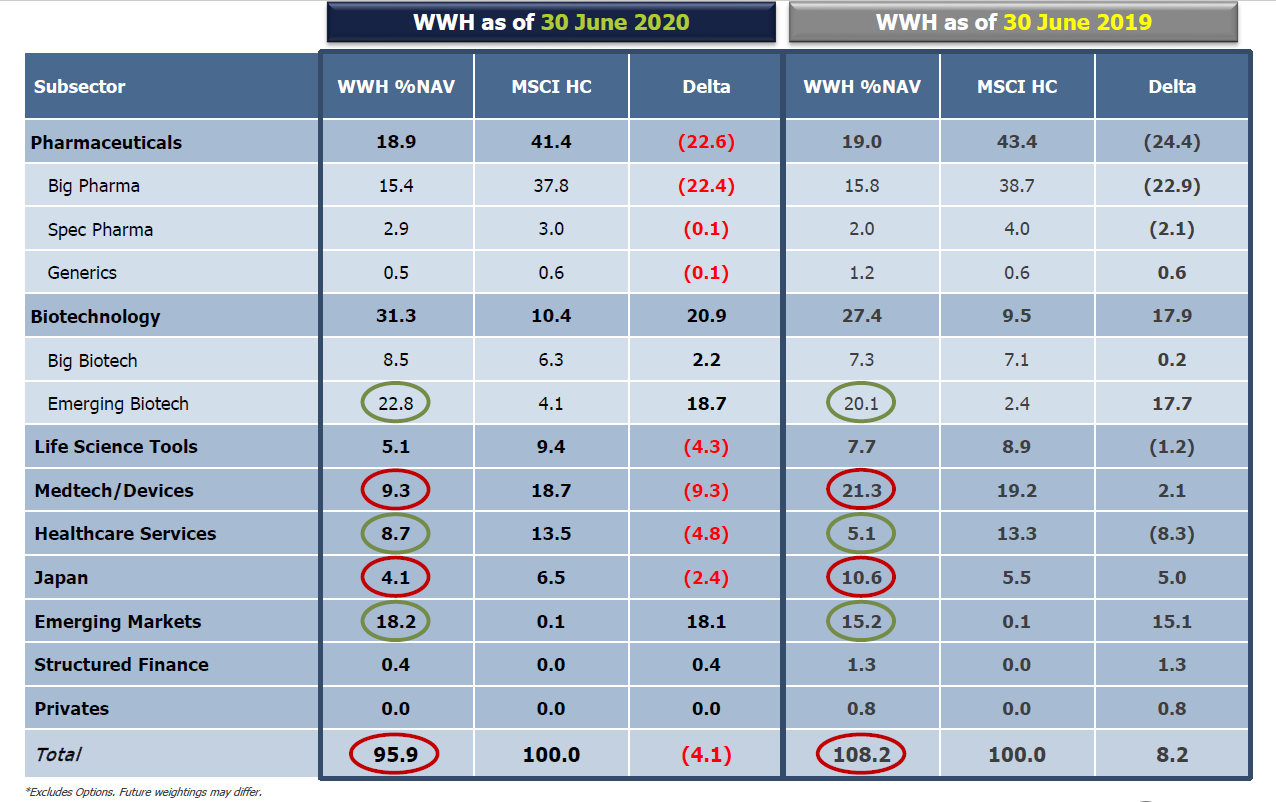

Portfolio

Here’s a useful slide from one of the Worldwide Healthcare’s recent presentations, showing how its portfolio differs from the broader healthcare sector:

Although the trust’s weighting towards drug firms is similar to the index, it’s highly skewed towards smaller biotech firms at the expense of lumbering pharmaceutical giants.

Emerging markets, which don’t feature at all in the MSCI World Health Care index, are the other key differentiator. Worldwide Healthcare particularly likes the prospects for Chinese companies, especially now non-profitable biotech firms are eligible to join the market.

On a monthly and quarterly basis, therefore, we should expect to see quite a wide variation between the performance of Worldwide Healthcare and its benchmark. Measured over a few years, it should even out a little, with the trust hopefully adding to its long-term outperformance.

Overall, Worldwide Healthcare’s portfolio looks reasonably concentrated for a trust of this size. The largest position is 5%, the top 10 some 40%, and the top 40 around 87%. There is a fairly long tail of small positions, typically taking the number of holdings to between 70-80 companies.

Portfolio turnover seems pretty high at around 100% for both the last two years.

In the year to March 2019, the portfolio started the period at a value of £1.3bn and £1.4bn of investments were bought and £1.5bn were sold.

In the year to March 2020, the start value was £1.4bn with another £1.4bn bought and £1.2bn sold.

Transaction costs came out at £3m in 2020 and £2.5m in 2019 (about 0.2% of net assets each year).

Most of the biotech/healthcare trusts I have looked at so far, at least those invested mostly in publicly quoted companies, seem to have similarly high portfolio turnover rates. But most seem to outperform the sector, too.

Sector prospects

Concerning the key US healthcare market, Borho and Polischuk seem fairly sanguine about the upcoming presidential election. They see universal healthcare coverage as a very low probability, regardless of who wins, and believe the winner would be reluctant to “bash the healthcare industry” in the wake of the pandemic.

The annual total of new drug approvals in the US has risen from around 20 in the early 2000s to 50-60 over the last couple of years and 40 up to early September in 2020. This should help drive revenues higher over the next few years.

Borho seems very bullish on the sector’s long-term prospects, pointing to high levels of innovation taking place right across the industry.

Fancy graphic time…

The COVID-19 pandemic may be dominating the news headlines but I don’t think it’s a significant part of the story here.

Worldwide Healthcare reckons a lot of smaller companies involved in producing tests and vaccines look rather pricey and may not make that much money from the crisis due to political and social pressure. Over the long term, though, it could result in increased spending in areas like diagnostics.

M&A activity has been a big feature of the sector in recent years. And it might be about to return after Gilead Sciences last week agreed to buy Immunomedics for $21bn. The deal was for $88 per share, more than double the $42 share price just before the announcement.

I don’t think Immunomedics was in Worldwide Healthcare’s portfolio but this news seemed to boost the whole sector a touch. Immunomedics was a big holding for both International Biotechnology Trust and Biotech Growth, whose shares both jumped in response to the news.

Skin in the game

The directors own just over 50,000 shares in Worldwide Healthcare worth nearly £2m.

Borho replaced Isaly on the board in 2018 and he owns 10,000 shares (£0.35m).

Polischuk’s stake isn’t disclosed and there is no information on the total stake held by OrbiMed staff in total.

Discount control

A discount control mechanism has been in place since 2004, with aim of limiting Worldwide Healthcare’s discount to net assets to a maximum of 6%.

Also in 2004, a share placing raised £67m and had warrants attached to sweeten the deal. About the same amount was raised over the next few years as these warrants were exercised.

After the warrants expired in 2009, a bonus of issue of subscription shares was made. This brought in a further £65m of funds between 2009 and 2014.

Much of the cash raised was effectively spent on buybacks. £170m was spent in total, predominantly from 2007 to 2013.

Since 2013, the discount has shrunk beneath the 6% level and buybacks have become relatively rare.

Indeed, since 2017, Worldwide Healthcare has usually traded around its net asset value or at a premium of 1-2%.

It has issued new shares on a fairly regular basis to keep the premium at a low level, with the number of shares rising from 45m in 2013 to 59m today.

Gearing

Worldwide Healthcare can gear itself up 20% via direct borrowing and Borho recently remarked he was pretty comfortable running at 10-20% for most of the time.

However, he’s taken a more conservative stance in recent months, even adopting a 5% cash position after the strong run the sector had in the second quarter of this year.

Gearing is provided through a US dollar overdraft with JPMorgan Securities (overnight US rate plus 45 basis points).

On top of that, Worldwide Healthcare can also use derivatives (up to 5% net) and equity swaps (up to 12% gross). The latter is used to “gain access to the Indian and Chinese markets either because the Company is not locally registered to trade or to gain exposure to thematic baskets of stocks”.

The combined leverage from all these methods is limited to 140%.

I get a little twitchy when I see mention of gross and net gearing commitments on factsheets as I don’t find it easy to understand the full extent of the risk being taken. So I’ll probably keep an eye on this going forward for any notable changes.

Charges

This isn’t a cheap trust given it has £2bn of assets.

OrbiMed receives 0.65% plus a 15% performance fee.

Frostrow Capital, which provides all the admin services, gets a tiered fee that works out at 0.15% on the current market cap of £2bn.

The Key Information Document’s 2.0% charge breaks down into 0.3% transaction costs (a little higher than noted earlier), 1.2% ongoing charges and a 0.5% performance fee.

I would assume the higher ongoing element, as opposed to the 0.9% OCF mentioned in most documentation, represents the costs of the trust’s debt.

Dividends

Many of Worldwide Healthcare’s holdings don’t pay dividends so the income here is pretty low as a result.

Currency fluctuations can also see the amount paid out vary from year to year.

Worldwide Healthcare generally seems to pay out what it receives but has built a revenue reserve of about one and a quarter years (£18m).

A shift away from higher-yielding stocks in the year ended March 2020 saw the payout drop from 26.5p to 25.0p representing a current yield of 0.7%.

In summary

I recently bought back into Worldwide Healthcare, having owned it for a brief time in its early days in the late 1990s.

While I’m kicking myself for being so short-sighted in the past, I’m pleased I wasn’t too stubborn to buy back into it at a (much, much) higher price.

It’s one of three biotech/healthcare trusts I hold, so it’s a fairly small position size for me right now although I expect I’ll add to it over the next few years.

Other healthcare trusts that specialise in the narrower niche of biotech, such as Biotech Growth and the Swiss-listed BB Biotech and HBM Healthcare, boast a better performance over the last 10 years.

But I like Worldwide’s all-rounder approach as that should mean a little less volatility.

It still owns a decent slug of biotech and I’m getting additional biotech exposure via another holding in International Biotechnology Trust which I hope to cover in a blog post before this year is out.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

I believe Hansa Trust used to be Finsbury Trust

Many thanks for that info John. It looks like Hansa was called Finsbury Trust from 1992 to 2001 and prior to that, it was known as Scottish & Mercantile.

I’ve since come across another one called Close Finsbury Eurotech Trust which was launched in August 2000 (not great timing for a technology trust) and that only raised some £30m when it first listed.

It ended up being liquidated after its shareholders decided to wind it up at the end of 2006. From what I can tell, it launched at £1 but hit 25p within its first year and a low of 12p a year after that. It did recover to around 40p but shareholders seemed to have had enough at that point.

So not all the Finsbury trusts have done as well as WWH, BIOG, ATT, and FGT!

Thanks for a comprehensive write up. Do we know if the 15% performance fee is on any gain or kicks in above a certain level?

Regard

Pete

Found now on trustnet. Details had to be opened out.

Frostrow Capital LLP receives a periodic fee equal to 0.30% p.a. of the Company’s market capitalisation up to GBP 150 million of such market capitalisation and 0.20% per annum on market capitalisation in excess of GBP 150 million plus a fixed amount equal to GBP 50,000 p.a. Investment Manager is also entitled to the payment of a performance fee. The performance fee amounts to 16.5% of any out-performance of the NAV over the benchmark index. At each quarterly calculation date any performance fee payable is based on the lower of: (i) the cumulative out-performance of the investment portfolio over the benchmark index as at the quarter end date; and (ii) the cumulative out-performance of the investment portfolio over the benchmark as at the corresponding quarter end date in the previous year.