One of the questions that often gets asked about Smithson, Fundsmith’s global smaller company investment trust, is whether it is in danger of growing too large.

Or maybe it’s just me?

It’s a question that’s been bugging me for a while but after digging into its latest annual results, I’m now a lot more comfortable on this front.

I bought some Smithson shares at its IPO in 2018 and I’ve made several top-ups since then. I stopped buying in April 2020 when I got to my desired position size.

Key stats for Smithson Investment Trust

- Listed: 19 October 2018 at 1,000p

- Managers: Simon Barnard and Will Morgan with oversight from Terry Smith

- Ticker: SSON

- Benchmark: MSCI World SMID Index (SMID = Small and Mid-Cap)

- Recent price: 1,634p

- Indicated spread: 1,633p-1,635p (0.1%)

- Market cap: £2.5bn

- Premium to net assets: 2.0% as of 22 Mar 2021

- Costs: 1.0% OCF, 1.04% KID

- Cash/debt: 0.8% net cash as of 28 Feb 2021

- Dividend: Nope

- Results released: Mar (finals) and Aug (interims)

- Style: Quality-focused concentrated portfolio with low turnover

- Sector: Global smaller companies (3rd out of 5 since Oct 2018)

- Links: Website and AIC page

Price data as of 22 Mar 2021.

How Smithson has grown in size

Smithson was initially looking to raise £250m when it floated in October 2018.

However, its IPO was wildly popular and it ended up raising £823m, making it the largest investment trust flotation of all time.

Smithson has consistently traded at a small premium to its net asset value, apart from a few days this time last year. The trust regularly issues small parcels of new shares to soak up investor demand and ensure its premium doesn’t become too large.

In less than two and a half years, Smithson’s share count has increased by 85% and its share price has risen by more than 60%.

Its current market cap is £2.5bn, which is ten times the initial planned size for its flotation.

Is that a big number?

As a loyal listener of More Or Less, I know that it’s important to put numbers like this into context.

£2.5bn makes Smithson the largest of the five trusts specialising in global smaller companies. Herald and Edinburgh Worldwide are the next biggest, both valued at £1.4bn.

Smithson is already the 14th largest investment trust out of the 400 or so covered by the AIC’s statistics service. They are a bunch of trusts of a similar size to Smithson and the fifth-largest trust (RIT Capital Partners) isn’t that much larger at £3.7bn.

But it is still small compared to the £28bn of assets managed by the Fundsmith Equity fund and its European sidekick Fundsmith Equity SICAV.

And while lots of trusts issue new shares on a regular basis, few do so to the extent that Smithson does. As its 2020 annual report states:

Since [the IPO] the Company has raised a further £925 million net of costs in the secondary market, making the Company the most successful investment trust in terms of secondary share issuance in each of 2019 and 2020.

What’s more, Smithson’s stated brief is to look for investments ranging in size from £500m to £15bn. As it has a concentrated portfolio of around 30 companies, you can see it’s already become quite difficult for the trust to invest in companies at the lower end of that range.

For example, if Smithson wants to put 3% of its portfolio into a £1.5bn company, it needs to buy £75m. That’s equivalent to 5% of that company’s entire share capital.

It becomes harder to buy and sell when your stake is that large, as you could shift the company’s share price due to the volume of your trades.

What’s the current situation?

Smithson had an investable universe of 83 companies when it floated in 2018 and said it planned to have a portfolio of between 25 and 40 companies.

It started with 29 holdings and has bought 5 more and sold 3, making the current portfolio 31 positions.

Here’s the market cap of each company in the portfolio and my crude estimate of how much of each company Smithson holds.

| Company | Mkt cap £bn | % owned by Smithson |

|---|---|---|

| Fevertree | 2.9 | 4.4% |

| Sabre | 3.7 | 3.2% |

| Rightmove | 4.9 | 2.2% |

| IPG Photonics | 8.3 | 1.2% |

| Domino’s Pizza Enterprises (Aus) | 4.5 | 2.0% |

| ANSYS | 20.1 | 0.5% |

| Equifax | 14.8 | 0.6% |

| Cognex | 10.3 | 0.9% |

| Verisk Analytics | 20.1 | 0.4% |

| Domino’s Pizza Group (UK) | 1.7 | 4.8% |

| Recordati | 8.0 | 1.0% |

| Temenos | 7.5 | 1.1% |

| Masimo | 9.1 | 0.9% |

| Rational | 6.5 | 1.2% |

| Qualys | 2.9 | 2.8% |

| Fortinet | 21.8 | 0.4% |

| Verisign | 15.2 | 0.5% |

| Simcorp | 3.7 | 2.0% |

| Halma | 8.8 | 0.8% |

| Paycom | 16.3 | 0.4% |

| MSCI | 24.1 | 0.3% |

| Technology One | 1.7 | 3.8% |

| Geberit | 16.5 | 0.4% |

| AO Smith | 6.4 | 0.9% |

| Nemetschek | 5.1 | 1.0% |

| Diploma | 3.0 | 1.5% |

| Spirax-Sarco | 8.5 | 0.5% |

| Fisher & Paykel | 9.3 | 0.5% |

| Ambu | 7.2 | 0.6% |

| Abcam | 3.5 | 0.7% |

| Chr. Hansen | 8.5 | 0.3% |

I’ve calculated the percentage Smithson owns by using the value held at December 2020 divided by the current market cap of each company.

That means any share price movements in 2021 and any subsequent sales or purchases by Smithson are not included. But I think the figures produced should be close enough for the purposes of this exercise.

There are two companies in the portfolio worth just £1.7bn but the next smallest is £2.9bn. My example above about a £1.5bn company looks much less of an issue in this light.

There are only 6 positions where Smithson owns more than 2% of that company’s shares, which surprised me a little. Fevertree and Domino’s Pizza Group are the two largest but they are still less than 5%.

The average market cap is £9.5bn, which is again quite a bit higher than I would have guessed. Smithson’s Owner’s Manual, which I don’t think has been updated since the IPO, suggested the average would be £7bn.

In fact, there are now 7 market caps that have risen above the £15bn upper limit suggested for new investments.

Smithson’s benchmark, the MSCI World SMID index, contains over 5,000 companies. The largest of these is £35bn but the mean average is only £2.3bn. So while Smithson is hunting in the same pool, it’s very much concentrating on the bigger fish.

There’s still room to grow

Although I’m a lot more comfortable having looked at these numbers, it’s still hard to get a feel for how big Smithson could get before its size starts to materially narrow its investment options.

Its portfolio turnover is very low, probably just one or two new purchases in a typical year, so you could argue that new investment ideas don’t need to be that plentiful.

If we start to see a number of company stakes exceed the 5% mark, particularly in the top 10 holdings, then I think that would give me pause.

A significant increase in the number of companies in the portfolio might be another indicator. Of course, we’re still some way below the upper limit of 40 set out in the Owner’s Manual.

Smithson’s directors have been pretty upfront about issuing new shares. As is often the case, they highlight the marginal benefits to shareholders and skip over the much higher management fee that it generates.

There are also the usual assurances that they will take their foot off the pedal if they think the trust is getting too big to deliver on its mandate.

I would assume that, at some point, investor demand might ease and proportionally fewer new shares will need to be issued.

For example, despite the recent success of Scottish Mortgage, its share count of 1.4bn is much the same as it was three years ago. At £16.5bn, it’s much larger of course, but it suggests this could be a problem that fixes itself in due course.

Smithson’s portfolio weightings

Like all Fundsmith funds, Smithson’s strategy is centred on buy and hold. This table shows just how little its portfolio has changed since its IPO:

| Company | 2020 | 2019 | 2018 |

|---|---|---|---|

| Fevertree | 5.7 | 3.9 | – |

| Sabre | 5.1 | 4.9 | 5.0 |

| Rightmove | 4.8 | 5.5 | 5.1 |

| IPG Photonics | 4.3 | 3.6 | 2.0 |

| Domino’s Pizza Enterprises (AU) | 4.0 | 3.3 | 2.9 |

| ANSYS | 4.0 | 4.8 | 4.0 |

| Equifax | 4.0 | 4.9 | 5.1 |

| Cognex | 4.0 | 3.5 | 4.1 |

| Verisk Analytics | 3.9 | 5.0 | 5.1 |

| Domino’s Pizza Group (UK) | 3.6 | 4.2 | 3.0 |

| Recordati | 3.6 | 3.9 | 4.5 |

| Temenos | 3.6 | 2.5 | 1.9 |

| Masimo | 3.6 | 4.9 | 5.3 |

| Rational | 3.5 | – | – |

| Qualys | 3.5 | – | – |

| Fortinet | 3.4 | – | – |

| Verisign | 3.3 | 2.8 | 4.2 |

| Simcorp | 3.2 | 3.5 | 3.2 |

| Halma | 3.1 | 3.9 | 4.3 |

| Paycom | 3.0 | 2.4 | 2.1 |

| MSCI | 2.9 | 2.8 | 2.2 |

| Technology One | 2.8 | 2.8 | 3.4 |

| Geberit | 2.7 | 3.1 | 3.3 |

| AO Smith | 2.5 | 3.0 | 3.0 |

| Nemetschek | 2.2 | 1.8 | 1.8 |

| Diploma | 2.0 | 2.5 | 1.9 |

| Spirax-Sarco | 1.9 | 2.4 | 3.1 |

| Fisher & Paykel | 1.8 | 3.4 | 3.1 |

| Ambu | 1.8 | 2.9 | 2.8 |

| Abcam | 1.1 | 1.6 | 2.0 |

| Chr. Hansen | 1.0 | 1.4 | 2.0 |

| Check Point Software | – | 4.8 | 5.1 |

| CDK | – | – | 4.5 |

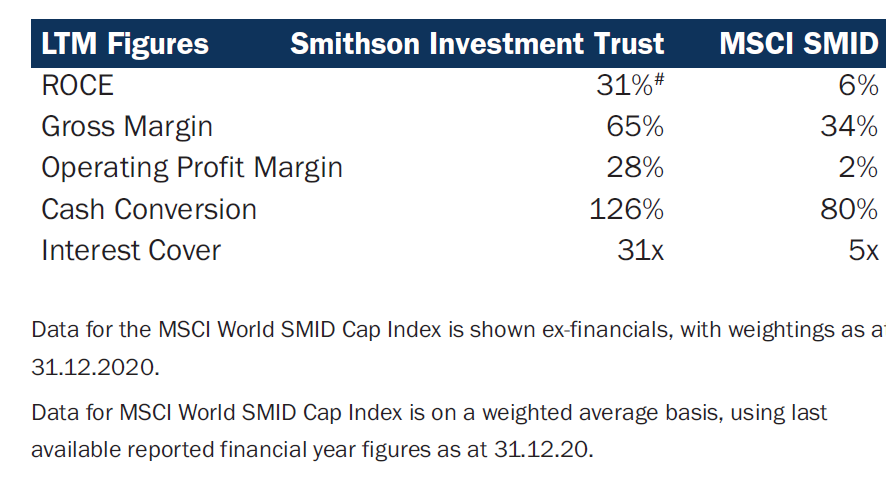

And here’s the standard look-through Fundsmith likes to provide for the financial metrics of its portfolio companies:

Return on capital employed (ROCE) increased from 28% last year to 31% while the average ROCE for the benchmark went the other way, slumping from 11% to 6%.

Likewise, Smithson’s cash conversion metric rose from 104% to 126% while its benchmark fell from 84% to 80%.

Both of these increases are pretty impressive considering the effects of the pandemic on company finances and demonstrate the underlying strength of the businesses that Smithson owns.

Portfolio changes

2019 saw the first portfolio changes with the purchase of Fevertree and the sale of CDK.

Fevertree is well-known to most UK investors and Smithson materially increased its position in March 2020 at the height of the stock market panic, hence its very large position as at December 2020.

However, Fevertree results last week were poorly received and its shares are down 15% so far in 2021. At 10 times sales, I’d say it still looks quite expensive.

The sale of CDK was prompted by a change of company strategy that Smithson wasn’t keen on.

Three new companies were introduced to the portfolio in 2020: Rational, Qualys, and Fortinet. Rational is a commercial oven maker while Qualys and Fortinet are cybersecurity businesses.

Check Point, 2020’s sole outright disposal, is also involved in cybersecurity but has seen its sales growth slow markedly despite increasing its marketing spend.

It’s notable that both CDK and Check Point were in Smithson’s top 10 holdings in the trust’s early days, indicating that Barnard is happy to sell when the facts seem to change.

In February 2021, Smithson bought into the US-based pest-control business Rollins after its share price fell following its latest results. In the same month, Abcam, which makes and distributes antibodies and related research tools, was sold due to concerns about its capital allocation.

Like Fevertree, Rollins doesn’t look overly cheap at 8 times sales and its share price was substantially lower all the way from the trust’s IPO to July 2020.

Perhaps that’s an indication that new investment opportunities are quite thin on the ground?

Among the businesses that have been held throughout, there haven’t been many major position size changes.

IPG and Temenos have been the largest upwards movers. The latter’s share price hasn’t moved much, so I suspect increasing its position size has been a conscious decision.

A few companies have seen their weightings fall significantly but only Chr Hansen now has a weighting materially less than the 2% minimum position size we saw in Smithson’s first set of accounts.

Barnard says “discretionary portfolio turnover, excluding the investment of proceeds from new shares issued, was 21.6% for the year … [with a] concentration of trading activity that occurred during the market lows of March and April, with very little occurring subsequently.”

By way of comparison, discretionary portfolio turnover was 6.1% in 2019.

Performance to date

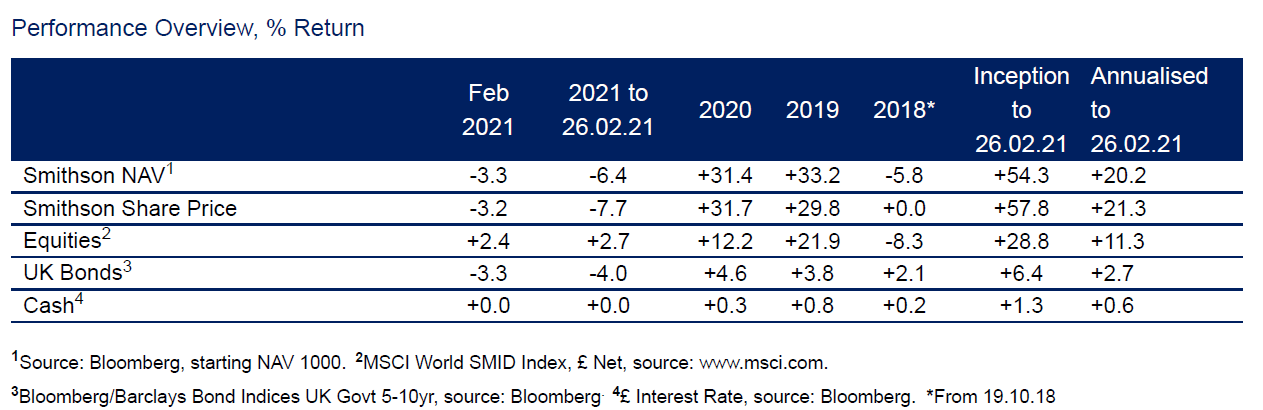

Like other funds that play the quality game, Smithson’s performance has levelled off somewhat over the past several months.

However, to beat your benchmark by ten percentage points, albeit for just under two and a half years, is pretty impressive.

I’d expect this gap to narrow over time as 2020 was an exceptional year for Smithson in terms of outperformance. Only three of its holdings were negative contributors to its overall return.

Barnard was upfront about this being an exceptional year at the start of his manager’s report. That’s something I like to see.

The MSCI World SMID index that Smithson uses as its benchmark has performed very similarly to the main MSCI World index over the past ten years, with the latter just 0.1 percentage point a year ahead.

If we go back a bit further, small and mid-caps have done slightly better, though. Since its inception in 1994, the SMID is ahead at 8.7% annualised in US dollar terms versus 8.1% for MSCI World.

Smithson’s strong performance in 2020 has opened up a bit of a lead over Fundmsith Equity. At the end of last week, it was up 60% since launch whereas Fundsmith Equity had returned 43% over the same period.

However, as you would probably expect, Smithson’s share price was noticeably more volatile than Fundsmith Equity when markets crashed this time last year.

Compared to the other trusts in the global smaller companies sector, Smithson trails Edinburgh Worldwide (106%) and Herald (79%). Both of these have a strong tech-focus. It’s well ahead of North Atlantic Smaller Companies (34%) and BMO Global Smaller Companies (15%).

Again, we should caveat this by stressing this is a very short time period. But it’s all we have to go on right now.

Skin in the game

Terry Smith, other founder partners of Fundsmith, and key employees owned 3.06m shares of Smithson as of December 2020, up from 2.99m last year. But the increased number of shares in issue meant their stake dropped from 2.6% to 2.2%.

However, it’s good to see the number of shares held increase. The IPO prospectus said Fundsmith folks subscribed for 3.15m shares back in 2018, indicating some were sold during 2019 although I guess staff changes could have been a factor, too.

Terry Smith himself still owns 2.5m shares, as far as I know, through a company modestly called Eighth Wonder Limited.

Andrew McHattie’s new book, Investment Trusts: A Complete Guide, includes a comment from Investec that Barnard has 90% of his investable wealth in Smithson with the balance in Fundsmith Equity. I think I mentioned in a previous post that this would personally give me severe diversification concerns!

The three directors (the smallest trust board I’ve come across) took home just £84,000 in salaries last year but own nearly £0.6m in Smithson shares.

Less encouraging is the fact that they haven’t bought any additional shares since the IPO.

However, I think it’s fair to say that there are few concerns that the trust’s managers aren’t aligned with our interests due to a lack of shares held.

Charges

As with all things Fundsmith, the basic management charge of 0.9% of the market cap is very much on the high side but when you look at total costs it’s a more reasonable proposition.

There’s no performance fee to worry about.

The annual management charge is also 0.9% for the main Fundsmith Equity fund with Fundsmith Emerging Equities (a £350m investment trust) coming in at 1.0%.

Fundsmith earned £16.1m in management fees from Smithson in 2020 but the annual run rate based on the current market cap would be £22.5m.

Dividends

Smithson’s investments don’t tend to pay much in the way of dividends. The current portfolio yield is 0.7% and so is exceeded by the trust’s total running costs of just over 1.0%.

Smithson hasn’t paid a dividend so far and seems unlikely to do so in the near future.

Should its portfolio income exceed its costs at some point in the future then it might be required to pay something out as the laws that govern investment trusts specify that they have to pay out at least 85% of their net income.

Gearing

Smithson has the ability to take on borrowings up to 15% of its net asset value but only on a short-term basis for “liquidity purposes or for discount management purposes including the purchase of its own shares”.

Typically, it runs with a small cash position of a few per cent or less.

In summary

Smithson continues to impress me, despite the fact that its method of investing has underperformed in recent months. That happens sometimes. I’m in the camp that prefers to ride the ups and downs rather than changing strategies on a regular basis.

There were some interesting comments made by Terry Smith in Fundsmith’s recent annual meeting, seemingly praising the next generation of talent coming through as he starts to think more about succession plans.

I inferred Barnard was in that group as there aren’t too many people he could have been talking about!

It’s worth remembering that Barnard is still relatively untested as a manager, as far as public records go. He’s in his late 30s and ran two funds for Goldman Sachs before joining Fundsmith in September 2017.

One was a multi-asset fund called GS Global Income Builder Fund so doesn’t give much of a read-across. The other, the GS Global Millennials Fund, is a concentrated global equity growth fund. It seems to have returned around 60% in the eighteen months Barnard was running it.

Clearly, Smith has a lot of faith in Barnard and I believe he and co-manager Will Morgan joined Fundsmith specifically so that they could launch Smithson.

For now, my position size in Smithson is a lot smaller than my holding in Fundsmith Equity although I may look to narrow that gap at some stage if it continues to tick my boxes.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Thanks as always. I’ve been taking an interest in this lately. I can’t find a portfolio of Global mid-cap quality like it. They are companies that I think have strong management, and long-term sustainable growth opportunities (in contrast to Baillie Gifford, which feels more Private Equity-ish i.e. they will have a) lumpy returns and b) a higher miss rate, but the ‘hits’ grow so much they should compensate.

I didn’t know the detail about Barnard being so invested in it – really useful to know. It does help.

It is very early days as you say, given Barnard’s relative unknown qualities, but I am comforted that Barnard seems to be comfortable with the fairly defined Fundsmith playbook.

What I found interesting was how he handled the pandemic. It looked like he managed to do a good job of rebalancing i.e. selling the healthcare when it was consensus, and recycling it into the more beaten-up sectors. While I think this is possibly against the ‘Do Nothing’ mantra, it seems like a pretty positive thing to be doing.

On the other hand, I don’t have a sense of his skill at buying things at a good price – as you say it doesn’t seem an especially obvious time to be buying Rollins. Similarly with Fevertree, it went down a fair bit after they started buying – in contrast Lindsell Train went into Fevertree pretty much right at the bottom – I think their buying discipline is underrated. Hopefully if the companies compound it won’t matter so much in the long-run, but I hope he can do this better going forward. Terry Smith/Julian Robins also seem quite adept at this – they did well buying Facebook when it was out of fashion, and in particular did a great job buying Novo Nordisk when it dived.

I also think that it can be seen as a ‘stealth’ ESG fund – a lot of the holdings pop up in ‘ethical’ funds I look at. Perhaps this is more likely with a younger manager, but I think it’s good – not just for ‘doing the right thing’ but because I think good companies should do better over the long term.

Going back to your original point about the AUM – I tend to go by the rule of thumb that a fund shouldn’t invest in any company that has a smaller market cap than the fund. On that basis I think Smithson is fine. In addition, I think that as these quality mid-caps grow, it will be reasonable for them to invest in bigger firms. Maybe one day they’ll need a new fund for smaller firms again!

(To try and contextualise this, look at the size of some of the classic investment trusts in the 90s!).

I’m at my desired weighting now I think, so hope it recovers from its wobbly start to the year. Their style has possibly been affected by the recent US yield rises.

(sorry, this ended up longer than I intended it to…).

Thanks, Tom. I think I’m the last person who can criticise overly long comments 🙂

That market cap / fund size rule seems like a good one – certainly a lot simpler than my example.

Interesting point about the rejuggling Barnard did. Smithson seemed to recover from the March 2020 lows much more strongly than Fundsmith Equity did and that could be the reason why.

Yep, one day we might even see a Smithgrandson!

Excellent, thanks very much. As a long time supporter of small caps what is your view of the this area of the market and which fund do you think has the best prospect.

@nigel — I’m still a fan of small-cap trusts, largely because many of the top-performing ITs and UTs of the last 20 years or so have had a small-cap focus. I wouldn’t claim any special insight into whether they look particularly good value or not right now though.

As for the global small-cap trust sector, it’s a bit of mixed bag to be honest.

Both Edinburgh and Herald have that strong tech focus and I would tend to think of them as tech trusts first and small-cap trusts second. I think they’re likely to be most volatile of the bunch, as I believe they have been in the past.

Herald is 50% UK, which is pretty unusual for a trust classified as global and there is that question mark over how long Katie Potts will continue as the lead manager.

Succession is probably even more of an issue for North Atlantic Smaller Companies with Chris Mills now being 68 (I think) and fairly scant details as to what the succession plan is (as far as I know anyway). And I think it has even more in the UK, 70%, than Herald does.

And the BMO trust has struggled for a long time now. It seems to lack a clear identity to me, although I haven’t looked at it closely.

Smithson also has issues you could say, with its lack of a track record. I like the Fundsmith style, though, so I’m happy to keep holding it alongside my stake in Fundsmith Equity.

Of course, there are plenty more small-cap trusts that specialise on a regional basis, with the UK sector particularly well represented but plenty of choice in Asia, Japan, Europe, and North America. So, if you had strong views on any particular region, picking 2 or 3 trusts across these sectors could be an alternative way to go.