Putting some money into HgCapital Trust back in 2010 was one of my better investment decisions of recent years. It’s consistently been one of the top-performing private equity trusts since it launched.

I bought this trust several times between 2010 and 2016, which was a rare period when its share price performance was pretty flat.

As it subsequently became a very large position size for me, I trimmed by holding by about a third in 2018.

Its shares are up around 50% since then, so my position size is more or less back to where it was a couple of years ago.

I last covered HgCapital Trust in March 2019 so its interim results earlier this week provided a good opportunity to update my thoughts.

Key Stats for HgCapital Trust

- Listed: 1989

- Managers: Hg Pooled Management Ltd — AIC website lists: Nic Humphries (since 2001), Matthew Brockman (2010), Justin Von Simson (2003)

- Ticker: HGT

- 10-year net asset return: +301%

- Benchmark: FTSE All-Share

- Current price: 285p

- Indicated spread: 284p-286p (0.7%)

- Market cap: £1.2bn

- Net asset value: 282p as of 31 Aug 2020

- Premium to net assets: 1%

- Costs: 1.8% OCF and 3.9% KID

- Net cash: 3% as of 31 Aug 2020

- Number of holdings: 37

- Current dividend and yield: 5p and 1.8%

- Results released: Mar (finals) and Sep (interims)

- Dividends paid: May and Oct

- Continuation vote: every 5 years, next one in 2025

- Sector: Private Equity (3rd out of 15 over 10 years)

- Links: Website — AIC page — Edison reports

History

HgCapital Trust’s focus has narrowed over the years.

While I think it has always been concentrated on the UK and Northern Europe, when I first invested in it back in 2010, it covered healthcare, industrials, services, and technology.

Over the last decade, the technology sector has increasingly dominated the trust’s portfolio, and in particular business-related software and services such as payroll, tax, enterprise resource planning, legal & regulatory compliance.

It’s not the glamourous, consumer-facing end of the tech sector, but it seems to be working out pretty well.

The trust was originally set up as an unlisted investment company in 1982 and was called Grosvenor Development Capital. It joined the stock market in December 1989 when it had net assets of around £10m.

The trust’s original manager, Grosvenor Venture Managers, was bought by Mercury Asset Management in 1994 and the trust was renamed Mercury Grosvenor in 1995.

Early investments included a number of technology and biotech names you might recognise if you’ve been hanging around the markets for a few decades.

Sage, BTG, Celsis, Biocompatibles, Shield Diagnostics, Chiroscience, and Shire were all part of the trust’s portfolio.

Mercury Asset Management was bought by Merrill Lynch in 1997. Then Mercury’s private equity operations were the subject of a management buy-out in 2000 and HgCapital was born.

HgCapital is an independent partnership and today manages some $30bn with 150 professionals based in London, New York, and Munich.

The trust changed its name to HgCapital Trust in 2003 and eventually grew large enough to join the FTSE 250 in 2018.

In 2019, net assets passed the £1bn mark for the first time, marking a 100-fold increase since the trust floated thirty years earlier.

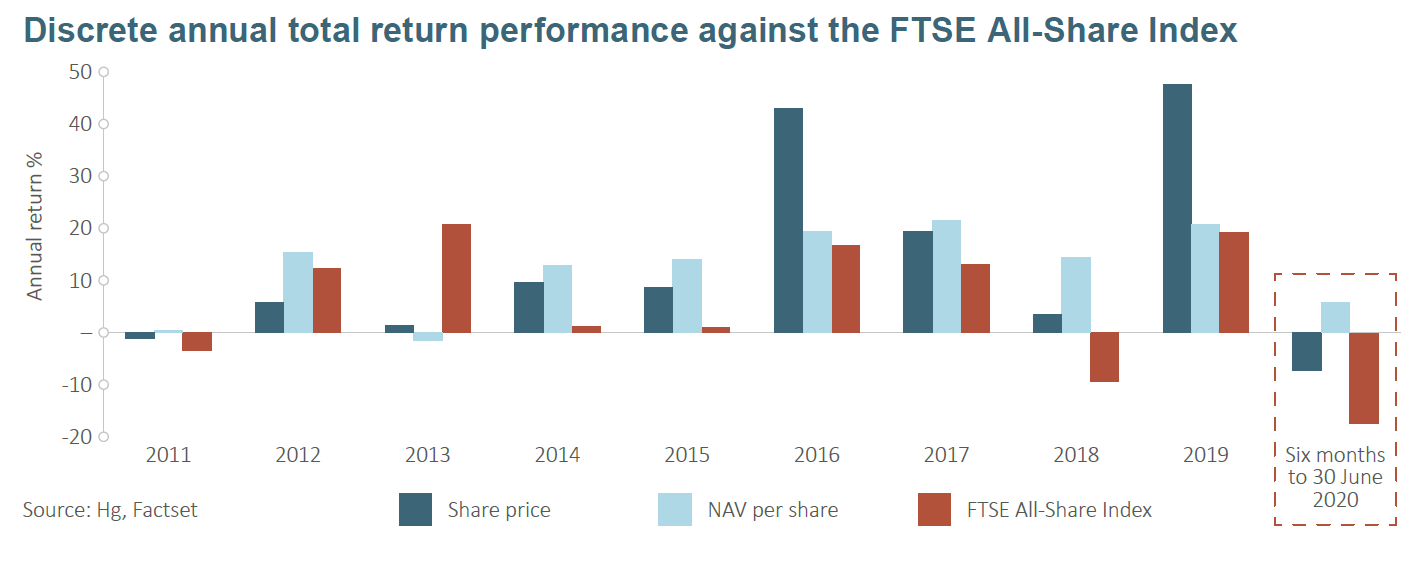

Long-term performance

HgCapital Trust has been one of the best-performing investment trusts of the last 20 years. And the last five years have been particularly strong:

{kind=link}

Within the private equity sub-sector, 3i and Harbourvest have done a little better over the last 10 years, but HgCapital Trust is ahead over 1, 3, and 5 years.

In 2020, it’s up 9%, making it the best performer out of the 16 in the sector.

Two other private equity trusts are flat (Princess and Apax Global Alpha) while most of the rest have lost more than 10%, partly thanks to widening discounts.

Since the start of 1992, the annualised return for HGT’s share price is 15.3%, even better than the 13.4% average for the last 20 years.

Of course, the 1990s were a great time for stock markets, so that provided an extra tailwind.

However, I think that puts HgCapital Trust a smidgen ahead of Scottish Mortgage over that timeframe, the latter returning 14.8% a year.

It’s also ahead of Allianz Technology and Polar Capital Technology since they launched in 1995 and 1996.

Of course, there have been periods when HgCapital Trust’s share price returns have been less impressive.

It did very well in 2000, but then lost about a third of its value as the bear market deepened from 2001 to early 2003.

It held up pretty well during the global financial crisis, losing maybe a quarter of its value.

The early 2010s were another lacklustre period, with the share price hovering around £1 for a few years. While the net asset value continued to increase, the discount widened to well over 20% at times.

I think I got pretty lucky here, as that was when I built up my initial position. The share price has shot ahead since then, particularly in 2016 and 2019.

The discount has also narrowed and HgCapital Trust is one of a few private equity trusts that now seems to trade at around its net asset value.

Most of the rest of the sector trades on a discount of 15-30%, although the infrequent nature of their net asset value updates can make direct comparisons tricky.

Investing structure

This gets a little gnarly but bear with me…

HgCapital Trust invests alongside other, unlisted HgCapital funds.

While HgCapital’s total stake in most of its investments is often between 60% and 90%, HgCapital Trust will only hold a fraction of that.

Most of Hg’s funds are split into Mercury, Genesis, and Saturn.

Mercury invests in deals from £75m to £450m while Saturn is for £1.3bn plus. Genesis sits in the middle.

There have been various iterations of these funds over the years. We’re now up to 9 for Genesis, 3 for Mercury and 2 for Saturn.

There is also another fund called Transition Capital which “offers privately-owned businesses an attractive alternative to a minority equity sale… giving entrepreneurs access to the support of Hg and its network, whilst retaining control of their business.”

As each of these Hg funds is launched, HGCapital Trust is “committed” to invest a certain amount.

I say “committed” as HgCapital Trust does have the option not to invest under certain circumstances, which I believe is fairly unusual when it comes to private equity investment trusts. That said, as far as I know, this option has never been used.

As of 30 June 2020, the trust’s outstanding commitments were £935m, which was split £455m Genesis, £300m Saturn, £130m Mercury, and £50m Transition Capital.

Churn, churn, churn…

Quite often it seems, an underlying investment will be sold by one Hg fund and bought by another as part of a larger transaction.

In August, Visma, HGCapital Trust’s largest investment was sold by Genesis 7 and rebought by Saturn 2. Other outside investors were involved in this $12.2bn deal and Hg as a whole saw its stake in Visma drop from 63% to 54%.

It can be confusing when you look at the individual investments in the portfolio. Before this deal, the first investment for Visma was listed as 2014, but Hg’s original involvement in the business dates back to 2006.

By the end of August, this latest Visma deal (and a few others) saw HgCapital Trust’s outstanding commitments drop to £814m, just over 70% of its net asset value.

70% is a little higher than the long-term average for outstanding commitments, which has been around 60% since 2008. But it’s shifted about a lot over the years, ranging anywhere from 20% to 120%.

HgCapital Trust expects to fulfil these commitments over the next 4-5 years. Similar refinancing deals are likely to be done, so it’s likely to be partly funded from sales made by old Hg funds.

These sort of transactions can seem a little sordid. They no doubt trigger payments for the management company and they are often used by companies to justify higher and higher valuations when very little new money is invested in a business.

It was a particular criticism, one of many admittedly, levelled at the ill-fated Woodford Investment Management.

It pays to keep an eye on any full disposals made, to see how the proceeds compare to the latest carrying value in the portfolio.

Out of 9 full disposals since the start of 2018, proceeds exceeded the latest carrying value on 8 occasions, with a write-down of less than £1m on the ninth (although it was written down by a lot more the year before).

That provides some comfort. Most of HgCapital Trust’s investment seemed to get revalued upwards on a fairly regular basis. In the first half of 2020, 15 rose and 2 fell. In 2019, 19 rose and just 1 fell.

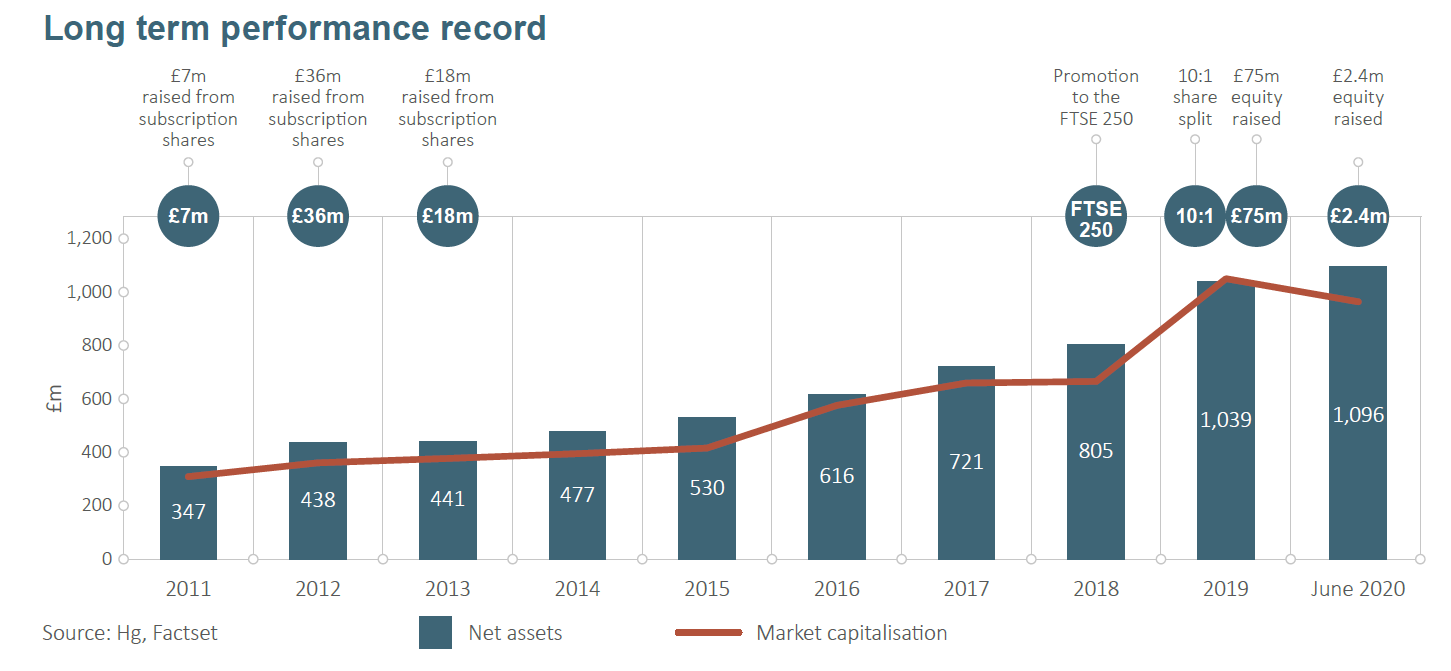

Capital raising

The June 2020 accounts contain a useful chart showing how HgCapital Trust has grown in size in recent years:

A placing in 2010 raised £50m and the new share issued came with subscription shares attached, allowing investors to buy more shares over the next few years. This raised about £60m from 2011 to 2013.

Another placing for £64m took place last year. And as HgCapital Trust has sometimes traded at a premium, it has been able to issue small amounts of new shares. It raised £11m this way in 2019 and a further £3m so far in 2020.

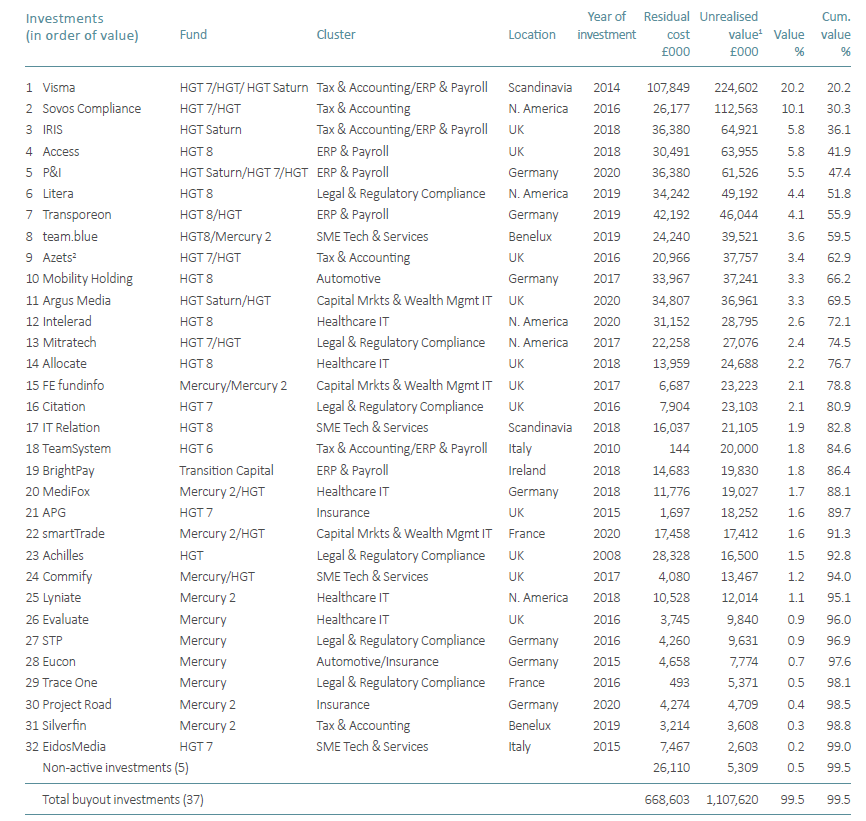

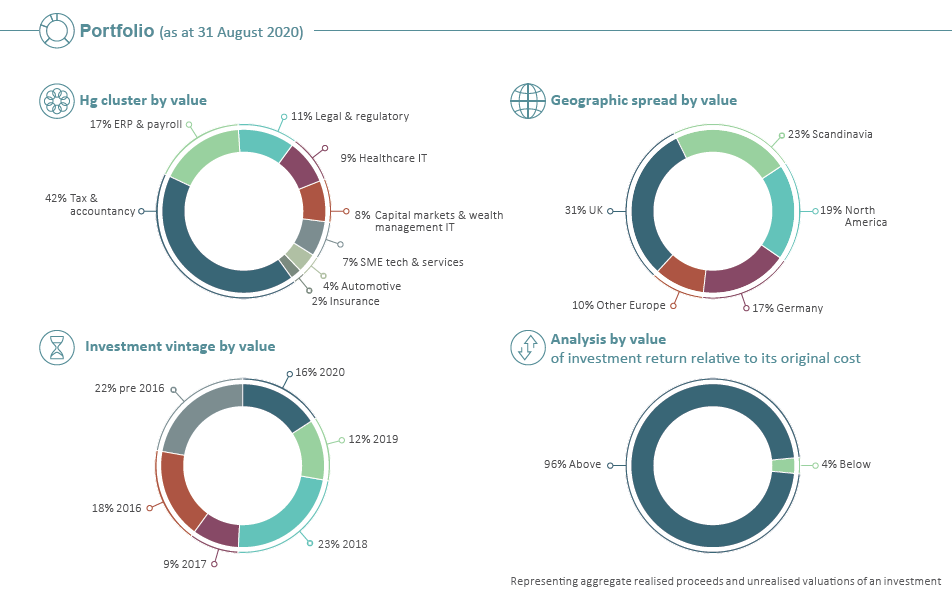

The portfolio

This is a detailed breakdown from the 2020 half-year results:

There’s probably not too much for me to add here on the individual holdings. The accounts and trust website have plenty of supporting information on these companies if you like to delve deeply into this sort of thing.

It is a concentrated portfolio, though, with the top 2 accounting for 30% and the top 15 around 80%.

Here’s a further analysis by sector and location, this time from the August 2020 factsheet:

The trust’s accounts provide a little detail on the underlying financials and valuation of the portfolio as well.

For the top 20 holdings, average sales growth was 23% over the last 12 months, whereas profits have grown by 27%.

On a valuation basis, the average multiple is 20.6 times profits before depreciation and amortisation.

That’s up from 19.8 at end of 2019, 16.4 at the end of 2017, and 14.5 at the end of 2015.

In other words, there’s been a fair amount of profit multiple expansion in recent years.

On the flip side, at the end of 2015, the equivalent figures for sales and profit growth were 10% and 12%. Both sales and profit growth have therefore more than doubled over the past five years.

Gearing

HgCapital Trust has an £80m borrowing facility on which it pays interest of LIBOR plus a margin of 2.25% to 2.50%.

This facility is fully drawn down right now but was more than offset by cash in the bank as of both June and August 2020.

The trust is in negotiations to expand this to £200m to help fund its investment commitments over the next few years, so I would expect it to move to a net borrowing position sometime soon.

It has said that “the reaction of the banking markets to HGT has been very encouraging”, but we will have to see if translates into a reduction in interest costs!

A fully drawn £200m facility (and zero cash) would represent 18% gearing based on the current net asset value, so that doesn’t seem too unreasonable.

Charges

Private equity is not cheap.

Many would say it’s outrageously expensive.

For the first half of 2020, HgCapital Trust’s basic ongoing charges came out at 1.8% of net assets. That probably puts it in the middle of the pack as far as private equity trusts are concerned.

But it’s important to understand that the basic ongoing charge is only part of the picture.

In 2019, HgCapital Trust incurred some £3.3m in administrative expenses but £15.5m for ‘priority profit share’. This is an amount paid to Hg for participation in its various funds. The percentage charged varies from 0.5% to 1.75%.

On top of that, there is carried interest, essentially a performance fee payable based on the returns per individual investment. However, this isn’t included in the basic ongoing charge.

Carried interest works out as 20% of any gains over 8% a year on an investment, although it doesn’t apply to all the Hg funds that the trust participates in for some reason.

As of 31 August 2020, £71m of carried interest had been deducted from the net asset value figure, reflecting gains already recognised on the existing portfolio value of £1,119m.

The much-maligned Key Information Document estimates what carried interest adds to a trust’s annual cost. In HgCapital Trust’s case, it’s 1.9%.

Added to transaction costs of 0.2% and 1.8% of basic ongoing charges that comes to a stomach-churning 3.9% a year in total charges.

But it does mean that to achieve ongoing share-price returns of 14% per annum, the underlying investments need to return around 18%a year. That’s a huge ask.

When a trust has performed as well as HgCapital Trust, I can live with these charges. Should returns drift back nearer the 8% level then the amount of carried interest should get reduced accordingly.

However, for me, a private equity trust really needs to be able to consistently beat an appropriate benchmark like a global tracker to justify its place in my portfolio.

Skin in the game

As at the end of 2019, partners and staff of Hg owned 13.1m shares (3.2% of the total, now worth some £37m). That was a significant increase on the 7.4m shares held at the end of 2018, which seems encouraging.

No figures were provided in the 2020 interim accounts for this, so we’ll need to wait until next March for the next update.

I suspect Hg partners and senior staff make a lot more from priority profit share and carried interest than they do from their HgCapital Trust shares, but there’s some alignment of interests with mere mortal shareholders here.

Directors of the trust, including the recently retired Chairman of 16 years Roger Mountford, own around £1.5m.

Dividend

HgCapital Trust’s dividend has generally risen over time but it has dropped a few times (most recently in 2005 and 2012), depending on what has been happening with its underlying cash flows.

0.09p per share was paid out for the 1990 financial year — the trust’s first full year as a listed company.

This had increased to 4.8p for 2019, after three years of paying out 4.6p per share.

5.0p per share should be paid in respect of 2020, with an interim of 2.0p due in October 2020 and a final payment of 3.0p likely to follow in May 2021. Obviously, the final payment may change depending on the situation with COVID-19.

HgCapital says it’s looking for modest dividend progression over time, so I’d expect the dividend yield to hover around the 2% mark in future, as it seems to have done for most of the time I have owned this company.

Summing up

I can’t see too many negatives here, which of course could be a warning sign in itself.

The underlying costs are high but worth paying, I think, given the long-term performance record.

The portfolio is very concentrated, but it’s been that way for most of the time I’ve been holding it.

Hg seems to select far more winners than losers. The fact that just 4% of the trust’s portfolio is valued at less than its original cost is a testament to this.

Should tech stocks fall out of favour, this could clearly dent the valuation. But that’s true for most high-flying trusts.

Likewise, a dip in returns could see the discount widen nearer the level suffered by most other private equity trusts.

When I looked at this trust last year, the fact that it said “future commitments may represent a further step up in size” did alarm me a little. But now they’ve happened, they don’t look too scary.

Although my position size is at much the same level as it was before I cut it back a couple of years ago, I’m feeling a little more relaxed about letting this holding ride this time around.

That’s no doubt influenced by the fact that the private equity trust I bought with my HgCapital part disposal back in 2018, Princess Private Equity, didn’t do nearly as well. I recently ditched it and recycled the proceeds into three biotech and healthcare trusts.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

I invested some money in it as well because of your recommendation … thanks a bunch 🙂

Glad you made some money M. But I would stress that nothing I write about here should be considerd a recommendation for someone else to buy!

Correct, “recommendation” is the wrong word- I just went over all the ITs in your portfolio and picked the ones I liked, this was one of them. Anyway, keep up the great work.

I have some shares in HG, and also in Harbourvest. HG has definitely been the better investment, and was up 10% in a day a few weeks ago following a transaction, although Harbourvest has done okay, without shooting the lights out. In general I am very positive on private equity although, as you say, the costs are not cheap. I also have some additional PE exposure through SMT’s investments in unlisted securities.

Harbourvest seems a lot more diversified than HGT so I think you’d expect it to be steadier and less spectacular. Not a bad combination to have. And SMT has obviously knocked it out of the park, especially over the last year.

HG has launched a podcast series where its managers talk to some of the people running the trust’s major investments. Only five 20-minute episodes published so far but something else to add to my listening list!

https://hgcapital.com/insight/orbit-an-hg-podcast/