It was only a few weeks ago that I reviewed Acorn Income Fund after it announced a strategic review ahead of a continuation vote due later this year.

There was a further update this week and I thought I’d do another article to help collect my thoughts.

The plan is to replace the current managers — Unicorn and Premier — and appoint BMO. The fund will shift from UK smaller companies to a global sustainable equity income mandate.

[At least that was the plan up until further announcements were made on 12 August and 1 September. The BMO appointment has been shelved and shareholders now get to choose between cash close to NAV or a roll-over into Unicorn UK Income — more details here.]

While there will still be an income focus, the dividend payout could roughly halve although there would also have been a significant cut if the existing strategy was maintained.

Acorn is a very heavily geared fund, using a big chunk of zero dividend preference shares (ZDPs) as its method of borrowing, and this has the effect of significantly boosting the yield from its underlying portfolio.

While the future level of gearing hasn’t been disclosed yet, I suspect the ZDP structure will disappear and a lower borrowing level put in place. The ZDPs are due to be redeemed on 28 February 2022 as things stand.

The reaction so far

Scouring the message boards, a number of Acorn Income shareholders are distinctly unhappy with the magnitude of the change having bought into the fund as a geared play on UK smaller companies.

I can understand that and everyone has to decide whether the revamped mandate fits into what they want to achieve with their portfolio.

We’re not exactly short of UK small-cap trusts, though, and the ability of investment trusts to reinvent themselves plays an important role in improving the calibre of those on offer.

The share price reaction has pretty muted so far with no real change on the day the news was released, followed by a 2% jump the day after.

Acorn Income currently sits on a 14% discount to net assets so there’s ample scope for this to narrow if investors do warm to the policy change over time. The discount on UK small-cap trusts averages around 6% right now but there’s quite a wide variation with a number of the tiniest vehicles on discounts of 20%+.

The need for change

According to the fund’s board “maintaining the status quo will not remove the historical challenges of scale and liquidity it is facing”. It’s not a decision the Board would have made lightly so I suspect they had already gotten a decent amount of feedback that the fund’s upcoming continuation vote would be it’s last.

From what I can tell, the gearing didn’t seem to be making much, if any, impact on long-term returns. The bid/offer spread has narrowed but is still wider than I’d like and the small size of the fund makes it relatively expensive to run.

What’s more, most of my other UK small-cap holdings have done a lot better than Acorn in the last few years. As a result, I now have a little more in this investment style than I’d like.

Given my doubts, Acorn was looking like the obvious candidate for a trim and perhaps even a complete chop. However, I was happy to wait and see what changes were being proposed.

As it happens, switching to both a global and a sustainable mandate could fit in fairly well with my overall strategy. I’ve got around two-thirds of my portfolio in global funds/trusts and recently bought into Keystone Positive Change.

Ethical investing is one of the most marmite topics in investing right now and I don’t intend to delve into all the various arguments here.

For me, it’s clearly the direction of travel and, given the choice, I prefer my money to be invested in non-evil things. Sure, there’s fad risk with this style and there has definitely been some overheating in certain areas.

But I’m willing to take the long-term view while keeping an eye on performance and the tone of what the managers are saying.

Trusts in the green space

There are a few ethical investment trusts but it’s still a relatively niche part of the overall sector.

For example, there are just three trusts in the AIC Environmental sector.

Impax was launched in 2002, Jupiter Green in 2005, and Menhaden in 2015. Collectively, they have assets of less than £1.5bn with Impax accounting for the vast majority of that figure.

More recently, we have seen a few property trusts dedicated to social housing, such as Civitas and Home REIT, but I regard that as a slightly different specialist area.

Keystone Positive Change, with its broader remit, was only created in February of this year and Liontrust ESG Trust is looking to raise £150m when it floats in June/July.

A revamped Acorn Income, should be changeover be approved, would take the number of equity ethical trusts to six although they could be spread over a few different AIC sectors (Keystone sits in Global rather than Environmental).

What happens next?

It will be a few months before all the boxes can be ticked and the changeover can officially take place.

A circular outlining the proposed changes in more detail is due in July. This will be followed by an EGM in early August where shareholders will vote on whether to approve the new-look structure.

After that, on 10 August, Acorn Income’s AGM takes place where shareholders will decide whether the trust will continue for a further five years. I guess the two meetings could be held back-to-back on the same day but the precise timing will be revealed in due course.

I believe 75% of shareholders have to vote that the company shouldn’t continue for a wind-up to take place and I presume the hurdle is similar for such a significant change in investment policy.

Assuming shareholders do approve the policy/manager change and then vote for a continuation, there will be a name change to the rather long-winded “BMO Global Sustainable Equity Income Fund Limited”.

The new strategy

From the recent announcement (my bold):

The Company’s investment objective be changed to achieve long-term capital growth and an attractive and growing dividend yield by investing principally in a portfolio of publicly listed global companies that make a positive impact on society and the environment. The detailed investment policy will be set out in the circular.

The strategy will invest in a diversified global portfolio of 30 to 50 high quality, cash-generative companies that are in complete alignment with the positive sustainability themes identified within the UN Sustainable Development Goals. The strategy will also aim to deliver an attractive level of income to shareholders.

The initial portfolio yield is expected to be circa 3.5%.

So it will be a fairly concentrated portfolio, which is fine with me given that I am pretty well-diversified across nearly 20 trusts, funds, and ETFs.

I’m a little less sure about the relatively high yield and what restrictions this might place on the type of companies considered for the portfolio. I’m guessing it will mean the focus is on larger and more mature companies.

How the portfolio yield translates into the dividend payout is yet to be determined as we still don’t know the level of gearing or if there’s going to be a change to how the management fee is split between the fund’s capital and revenue accounts. But Acorn’s directors clearly think the new approach will provide a more consistent if somewhat lower payout.

The new management firm

BMO Asset Management, owned by Bank Of Montreal, runs a number of UK-listed investment trusts following its takeover of Foreign & Colonial back in 2014. Its largest trusts are F&C, TR Property, BMO Commercial Property, and BMO Global Smaller Companies, all of which have over £1bn of assets.

Bank of Montreal is quoted in Toronto and New York and valued at nearly £50bn. Its asset management division oversaw £227bn of investments as of the end of 2020, with just over £8bn of that in what they call responsible funds and 20 investment professionals dedicated to this part of its business.

However, although this was not mentioned in Acorn’s announcement, BMO recently announced it was selling the EMEA part (Europe, Middle East, and Africa) of its asset management business to Columbia Threadneedle in a deal expected to complete by the end of 2021. Columbia Threadneedle is owned by Ameriprise Financial, which is valued at around £20bn and also listed on the NYSE.

According to a note this week from Edison, what might happen to the other BMO trusts when this transaction completes hasn’t been made public yet.

The new management team

Back to the announcement text (my bold again):

The portfolio will be managed by Sacha El Khoury, with Nick Henderson as the named alternative. Both are members of BMO’s Responsible Global Equities team, with Sacha having joined BMO in 2009, and Nick in 2008.

Sacha El Khoury is a Portfolio Manager within the Global Equities team, Lead Portfolio Manager on the BMO Sustainable Opportunities European Equity Fund, and Alternate Portfolio Manager on the BMO Sustainable Opportunities Global Equity Fund. Sacha graduated with an MSc in Finance (with distinction) from City University, Cass Business School in 2009 and a BA in Economics (with a minor in Business Administration) from the American University of Beirut in 2007. Sacha is a CFA Charterholder.

Nick Henderson is a Portfolio Manager within the Global Equities team, Lead Portfolio Manager on the Sustainable Opportunities Global Equity Fund, winner of the 2019 Money Observer Best Global Growth Smaller Fund Award, Alternate Portfolio Manager of the BMO Responsible Global Equity Fund, the BMO SDG Engagement Global Equity Fund, and the BMO Sustainable Opportunities European Equity Fund. Prior to joining the firm, Nick graduated with a Bachelor of Science degree in Economics from the University of Bristol; he is a CFA Charterholder.

I’m assuming Alternate Portfolio Manager is more of a back-up resource rather than a deputy position but I’m not clear how much day-t0-day involvement it entails. But El Khoury and Henderson are alternates on each other’s funds so they are clearly working together quite closely already.

El Khoury graduated in 2007 and Henderson in 2008, making them mid-30s, and they’ve been with BMO for pretty much their entire careers.

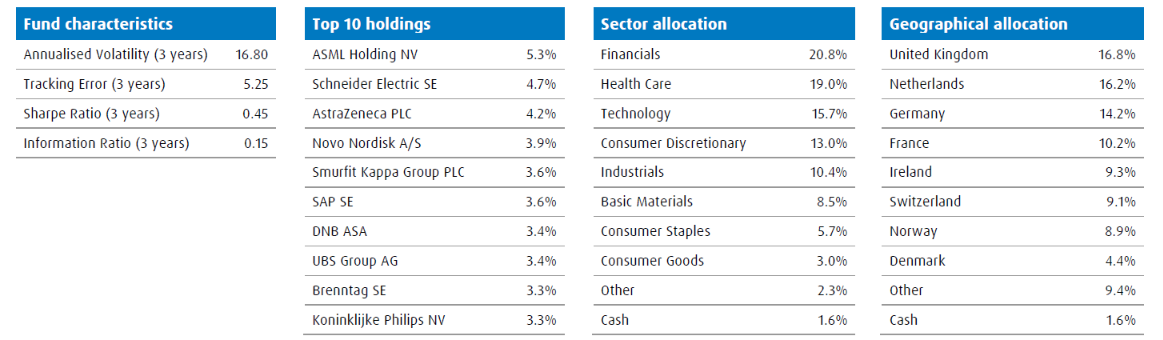

El Khoury, the proposed lead manager, has run the BMO Sustainable Opportunities European fund since it was rebranded in October 2019. It has €30m in assets and is up some 20-25% since she took the reins, broadly in line with global markets, but I’m not sure there’s too much that can be read into such a short albeit eventful period.

Here’s a summary of the European fund’s main positions from its latest factsheet:

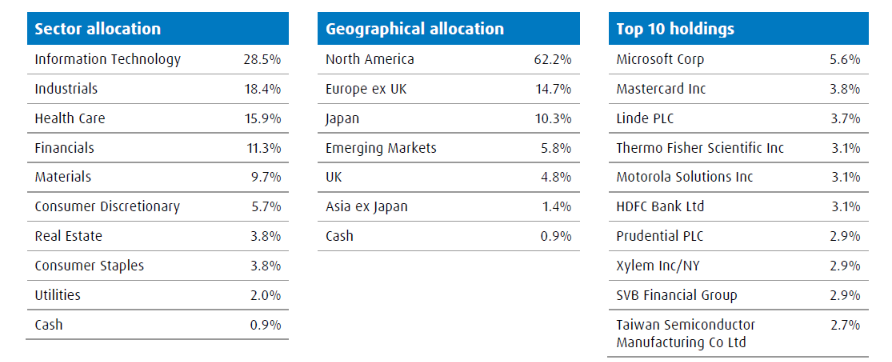

The Global fund run by Henderson is a little larger at £70m in assets but I’m not sure how long he has managed it for. It’s a percentage point behind world markets over one year but ten ahead over three years.

I believe there’s a collegiate approach at BMO so the holdings of the Global fund might give a better indication of what could be in the revised Acorn portfolio:

If you want a little more colour, El Khoury has written a few thought pieces that are reproduced on the BMO website and I also found this 14-minute video on YouTube where she discusses the philosophy behind the European fund.

As outlined in the video, there are six themes. The percentages indicate the relative weighing as of January 2021:

- Health & Wellbeing – 32%

- Digital Empowerment – 18%

- Sustainable Finance – 15%

- Sustainable Cities – 15%

- Resource Efficiency – 11%

- Connect & Protect – 7%

I’m getting strong Keystone Positive Change vibes here although the company choices seem much more reserved. From the two top 10s reproduced above, I think only ASML and Xylem are currently held by Keystone.

The new (lower) charges

It looks like there could be a meaningful reduction here due to the switch from charging a percentage of total assets to net assets:

The management fee will fall from 0.7% on the gross assets of the Company to 0.65% on the net assets of the Company and the performance fee is removed entirely.

Other operational cost savings are expected, including no additional fees associated with investment research or AIFM services. Furthermore, BMO’s management fee will be waived for the first six months of appointment.

In summary

I have to admit to being a little unimpressed when first reading Acorn’s announcement but I became more interested once I dug a little deeper.

A slightly less racy Keystone could be a decent fit in my portfolio and allow me to get to know this area of investing a little better as it’s still relatively new to me.

There’s a lot we don’t know yet about the proposed changes of course. Although there should be more information in the circular, sometimes these documents don’t add an awful lot in the way of useful detail.

I’d like to know a little more about the track record of the two managers, as open-ended funds can be notoriously opaque about such things. And given they haven’t been running their funds for that long, a bit more on the overall performance of BMO’s responsible funds over time would be handy.

How the balance is being struck between growth and income could do with some clarification, too. The level of yield suggests to me it’s heavily tilted towards the latter.

Acorn’s year-end is December with its interim report usually produced a week or two after its AGM in August. I suspect that might be delayed a little this year, as that interim report would seem like a good opportunity for BMO’s new managers to introduce the new strategy and the initial portfolio.

Right now I’m still in wait and see mode with this holding. It’s a small position at a fairly large discount so if the vote doesn’t go through there should be some downside protection as the fund would presumably get wound down somewhere close to its net asset value.

If I had to bet, I would say the policy change will get approved but it could be a close call.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Very interesting, and subjective. Personally it feels inappropriate to make such a violent style change – stick broadly with what the shareholders sign up for. To be frank – the best thing for shareholders would probably have been to merge it with another UK Sml Cos trust, but then the Board are putting themselves out of a job…

The BMO Global Sustainable fund looks really uninspiring to me – why choose anything but an exceptional fund with exceptional (and aligned) managers. It’s so rare for giant fund houses like this to have inspiring, free-thinking managers/funds.

I would be very surprised if e.g. Fundsmith or Smithson haven’t outperformed the global BMO trust over the next 5 years. Sometimes it’s better just to add to your best ideas…

Yes, violent is a good word to describe the change here and that’s certainly irked people from the comments I’ve seen so far.

I haven’t paid a great deal of attention to manager changes in the past but we’ve seen a rash of them recently. Edinburgh and Temple Bar were more subtle shifts, broadly keeping the same style, but Witan Pacific to BGCG was a more marked change. This proposed change from Acorn and Keystone have seen the geographic focus move from UK to global plus the sustainable angle on top, so they really are complete reinventions.

At least with Acorn, shareholders get to vote on the policy change and the continuation. I suspect if shareholders do vote to wind-up then merging with another small-cap trust would then become one of the possible exit routes.

Boards not wanting to put themselves out a job is a potential risk of course, although many of them have multiple directorships and shorter terms are becoming more commonplace so I’m not sure how big a factor it is in practice. And I suspect board members that do seem to cling on too much may find it harder to get future directorships.

I’d say the make-up of my portfolio is driving a lot of my decision here. A shift to something more global is probably what I would have done anyway and having quite a lot in Fundsmith/SSON/LTG already means I’m happy to diversify a bit with a different fund management house. But this definitely in the experimental pile so I can see how it develops.

It’s interesting that both Acorn and Keystone are moving away from the UK just as there seems to be increasing positivity about the relative value available from UK equities.

I’m surprised the yield may be so high, given the type of companies likely to be held, but it will distinguish it from Keystone, which will yield nearly zero, I believe.

I bought Keystone for exposure to Baillie Gifford’s style and their track record with growth and I don’t think I’d be tempted by Acorn.

I hold Chelverton UK Dividend for small company, highly geared, high income and I wonder whether some shareholders may migrate to them? It’s been volatile, but recent performance has been excellent.

Hi Nick, yes I suspect you could be right about some people moving over to Chelverton. It has the same ZDP structure, was also launched in 1999, but is not quite as highly geared. Perhaps more importantly, it doesn’t have the complication of the income portfolio that Acorn has. I believe its yield has been lower than Acorn in the past (as has its dividend growth in recent years) but it looks a lot more sustainable (!) given the level of revenue reserves Chelverton has.

The timing of shifting away from the UK could backfire of course but, on the other hand, many folks have been saying the UK is undervalued for a long, long time now. Year-to-date, I think the UK is up 10% vs 5% for global, so 2021 could be the first year in several where the UK comes out meaningfully ahead.

However, I guess you could also argue that we have too many UK-focused equity trusts relative to global ones and these mandate changes can help address that balance a little.

Only a couple of weeks to go now until the continuation vote at the AGM on Tuesday 10th August however there is still no sign of the circular setting out more details on the proposed manager change. Disappointing, to say the least. Have to say that I’ve become more minded to vote against the trust continuing, especially as the discount has started to widen out again.

A change of plan it would seem! It looks like major shareholders weren’t that keen on the BMO proposal, given the discount didn’t narrow much if at all, and other expressions of interest have since been received.

“An announcement with further details on the future of the Company will be published as soon as practicable and expected to be no later than mid-September. Thereafter, the Company expects to publish a circular in relation to the Board’s proposals for the future of the Company, including a notice convening the Extraordinary and Annual General Meetings.”

Third interim dividend has been held at 5.75p as a sop, after earlier indications it was likely to be cut, but all a bit of a shambles really. Still minded to hold until we have a better idea of the next steps as not keen on selling out on a near-20% discount with a continuation vote looming.

https://investegate.co.uk/acorn-income-fund–aif-/prn/dividend-declaration-and-update-on-future-of-the-company/20210812070000P1220/

A further update today…

https://www.investegate.co.uk/acorn-income-fund/prn/update-on-future-of-the-company/20210901110349P1588/

Shaereholders have the option to roll-over into Unicorn UK Income, an open-ended fund with the same managers and a two-thirds match of holdings, or elect to take cash close to NAV at the time of liquidation.

Better outcome than before I’d say and the market seems to agree with the shares now up some 10%. The bid price of 400p is still an 11% discount to the NAV on 27 August so my current plan is to sit tight and take the cash option in due course.