I decided to take up running on my 30th birthday after realising my 20s lifestyle, though not overly excessive, had given me a bit of a paunch.

I’ve drifted in and out of running over the (many) years since most recently jogging alongside my eldest as she did some Junior Park Runs before the pandemic shut everything down.

But one thing I’ve always struggled with is those uphill stretches.

And it seems my portfolio has a similar problem!

Although I’m up substantially over the last quarter, global markets have set a much better pace.

My numbers

Here’s how things looked as of 30 June 2020 using the unit method:

| Portfolio / Benchmark | H1 2020 | Q2 2020 | Q1 2020 | Since 1 Jan 2018 |

|---|---|---|---|---|

| My portfolio | -3.8% | +13.3% | -15.1% | +18.1% |

| Vanguard FTSE Global All Cap (fund) | -0.3% | +20.1% | -17.0% | +15.7% |

| Vanguard LifeStrategy 60 (fund) | +0.2% | +11.9% | -10.5% | +11.9% |

| Vanguard UK All-Share Index (fund) | -17.2% | +10.2% | -24.8% | -8.9% |

Having been a couple of percentage points ahead after the first three months of 2020, I’m now three and a half behind.

Boo!

My stretch aim is to beat global markets by 2-3 percentage points a year, so I’m a little behind on that measure, too. I still have a lead over global markets, but just a narrow one.

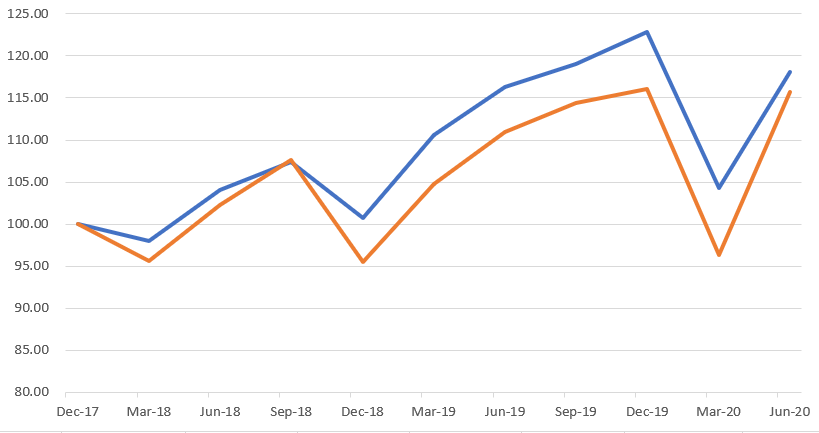

As you can see, my portfolio (blue) has tracked global markets (orange) pretty closely the past few years:

Of course, if you’d told me at the end of March that I would only be 4% down at the half-way point of the year, I wouldn’t have believed you.

The rebound in the second quarter still feels a bit too much to me but I’m not going to try and get all cute and attempt to time the market.

I dig into some of the individual performances later on in this piece, but my 30% underlying UK weighting probably hasn’t helped me this year, as the London market has disappointed yet again.

It’s been more than 18 months since I calculated that number, so it may be a little out of date now. But given I don’t buy and sell that often, I’d be surprised if it was that far off.

Pity the pound

After a little rally in the wake of last year’s General Election (which seems like a lifetime ago), it’s been a tough six months for the pound.

It went from 1.33 to 1.24 against the US dollar and saw similar falls against the Euro (1.18 to 1.10) and the Yen (144.5 to 133.4).

That’s boosted the performance of global markets when measured in sterling. While they were essentially flat in terms of pounds, they fell some 6% in terms of US dollars.

Put that way, perhaps the recovery in the markets is more reasonable. Certainly, there is an argument that the expectation of low interest rates for longer has boosted the multiples that people are prepared to pay for shares.

Major markets around the world

Here’s how some of the main markets around the world have done, measured in US dollars and on a total return basis:

- China: +4.4%

- US: -2.3%

- Japan: -6.8%

- Germany: -7.0%

- Canada: -11.6%

- Australia: -12.8%

- France: -15.5%

- India: -16.0%

- Italy: -17.9%

- UK: -22.9%

- Russia: -25.6%

- Brazil: -39.0%

The UK wasn’t the worst performing market by any means, but it was definitely below average.

Changing one of my benchmarks

In recent reviews, I’ve used the Lifestrategy 100 fund as my main benchmark. With its higher UK weighting, I felt it was a fairer measure than an ordinary global tracker.

On further reflection, I don’t think that holds water. It’s not a fund that I would choose to invest in, given its current UK weighting, so I’m reverting to a global tracker as my main yardstick.

For my comparison table, I’ve added the Lifestrategy 60 fund (60% equities and 40% bonds) instead.

As I get older, and my focus moves more toward keeping what I already have, I think this better represents the default investment I might eventually choose should I decide I no longer want to be an active investor.

In some ways, the UK index fund represents the investor I used to be. The global tracker is the investor I am now. Lifestrategy 60 represents the investor I might become in 10-20 years when I’m fully retired.

Monevator’s Slow and Steady portfolio has been very useful here, but the Lifestrategy 60 fund seems like a quick and easy solution for measurement purposes. It’s still a little biased to UK equities, but much less so than the 100 version.

My performance by holding

Here’s how my individual holdings have done so far this year. Note that my position sizes vary quite a lot.

| Holding | H1 | Q1 |

|---|---|---|

| Smithson | +13.3% | -10.9% |

| Fundsmith Equity | +7.7% | -7.9% |

| Gresham House Energy Storage | +4.0% | -13.6% |

| HICL Infrastructure | +3.7% | -4.0% |

| Lindsell Train Global | +3.4% | -10.9% |

| Vanguard All-World ETF | -0.3% | -15.4% |

| JPMorgan Global G&I | -1.1% | -15.5% |

| Bluefield Solar Income | -2.1% | -9.6% |

| Baronsmead Venture Trust | -3.4% | -16.3% |

| HG Capital | -6.8% | -12.1% |

| Princess Private Equity | -12.8% | -17.9% |

| RIT Capital Partners | -14.7% | -14.6% |

| Caledonia | -14.9% | -22.2% |

| Murray International | -18.7% | -30.6% |

| BlackRock Smaller Companies | -24.3% | -34.6% |

| Henderson Smaller Companies | -28.7% | -36.4% |

| Acorn Income | -33.5% | -33.5% |

I think that’s the widest range of numbers since I first broke down my performance into individual holdings.

Largely, the trusts and funds that held up best in the first quarter have done the best in the second as well.

The fact that investment trusts discounts have widened this year has had an impact.

For my portfolio, I’ve gone from a weighted premium of 0.6% to a discount of 2.0%, so that’s quite a swing. RIT Capital Partners, Caledonia, and Princess Private Equity have been the biggest contributors to this.

But I don’t regard this as an excuse. Looking back, only four of my trusts traded at a discount at the end of 2019, so it seems fairer to say they got a little ahead of themselves. The current situation is perhaps a fairer reflection of normal discount conditions, if there is such a thing.

Having side bets on private equity and UK small caps has dragged me down. But I expect them to be volatile, so I’m not particularly concerned. Acorn Income’s exposure to UK small-caps, high level of gearing, and widening discount has resulted in it being my worst performer.

My trio of ‘cautious’ global trusts — RIT, Caledonia, and Murray — have been the main issue for me in 2020. Had they performed in line with global markets, I think I would have been only 1% behind this year.

I looked at the long-term performance of 20 global trusts a few weeks ago, concluding that these three might be a little too similar and a little shake-up wouldn’t go amiss.

Set against that is my desire to gradually dial down my overall risk and being wary of getting too aggressive at the wrong time. When you see that Scottish Mortgage is up 55% year to date, with the various technology and biotech/healthcare trusts not too far behind, it’s tempting to wait for a better entry point!

But then that’s pretty much what I said in the first half of 2019 and that didn’t turn out to be a great call.

Part of my hesitation may also be having too many options to choose from. Most of the global and sector trusts I’ve looked at in the past 18 months have looked pretty decent. The perils of writing an investing blog!

In other words, I have a little more thinking to do before deciding whether to pull the trigger here.

Limited dividend damage… so far

Much has been made of the savage cutting of UK dividends due to the pandemic.

And almost as much has been made of the ability of investment trusts to ride this out by using their revenue reserves.

I think this point is a little overegged as revenue reserves usually aren’t represented by a fenced-off block of cash. In practice, some of the underlying investments are sold or gearing is increased to make sure the dividend isn’t cut.

And as trusts can pay out of capital reserves these days, it’s arguably even less relevant.

While most trusts will be able to continue paying dividends, this could be at the expense of lower growth for the next few years.

For my purposes, I tend to reinvest dividends, so any decrease is an inconvenience rather than an emergency. But within the next decade or so, I suspect I’ll move to a situation where I’m using dividends for income, supplemented by share sales if needed.

Out of my own holdings, only Princess Private Equity has announced a cut so far.

It’s a chunky one, though, as the 2020 dividend is likely to half that of 2019. In part, this was because of the expectation that it may need to provide funding to some of its investments, although that is apparently less likely now.

HICL has ditched its dividend target of 8.45p for the coming year, sticking with last year’s 8.25p. It was targeting 8.65p for the year to March 2022, but this is now under review and seems very likely to be revised down.

And Bluefield has scrapped its plan to link its dividends to RPI. In its place will be a progressive dividend policy. It should pay 8.0p over the next year, which is an increase on this year’s 7.9p but below the 8.1p the previous RPI uplift would have implied.

Bluefield has also formally announced that it’s changing its investment policy, allowing some non-solar (up to 25%), some non-UK (up to 10%), and some solar development (up to 5%). This should help combat the headwind of lower domestic power prices, so it’s made me a little more comfortable about its prospects.

All my other trusts have stuck to their proposed payment schedules as far as I can see. But that may change as the rest of 2020 unfolds.

What I’ve bought

Pre the crash, I added to Acorn Income, Bluefield Solar Income, and Smithson.

From mid-March to mid-April, I bought more of the same three trusts, plus HICL Infrastructure, Gresham House Energy Storage, Murray International, Princess Private Equity, Henderson Smaller Companies, and BlackRock Smaller Companies.

And I bought a little more BlackRock Smaller Companies last week.

All of these purchases were small top-ups. In the case of the infrastructure and UK small-cap trusts, I’ve been building up to a decent position size over the last couple of years and that’s largely complete now. With Princess and Murray, I took advantage of what seemed to be unusually high discounts.

I haven’t sold anything this year. In fact, the last time I sold anything was City of London Investment Trust in June 2019, when I deployed the cash across several existing positions.

The wider world of investment trusts

Let’s round things off with a quick look at the IT sector.

The average trust discount went from 1.4% at the end of 2019 to 8.5% at the end of the first quarter. It’s since narrowed again to 5.0%.

Average gearing levels remained at 9%, up from 7% at the start of the year but largely the same as they were at the end of the first quarter.

Performance-wise, of the 474 investment companies with returns data on Trustnet, 106 are in positive territory and 27 are up by more than 20%. Baillie Gifford US Growth is the best mainstream performer, up by 60%.

At the other end, 132 are down by more than 20% and 13 have fallen by 50% or more. DP Aircraft 1 takes the wooden spoon – it’s down 81%.

The new issue market for trusts has completely frozen, as you might imagine. Nippon Active Value raised just over £100m when it joined the market in February. It may turn out to be 2020’s only new issue!

But many trusts trading at premiums have raised money by issuing new shares, either as part of their ongoing discount/premium control policy or as larger one-off fundraising efforts.

Plenty of value-based trusts and sectors like debt, leasing, and property have all really struggled this year. A few might not make it to 2021 you suspect and several manager changes have been announced. But I think that’s healthy and a vital part of how the investment trust sector regularly renews itself.

Thank you!

Finally, I’ve just realised it’s two years and a day since I published my first article for this blog. I’m still a little surprised at how many people are reading my ramblings.

My page view numbers for the first month were pretty pitiful — less than a 100 in fact — but they’ve grown almost 250 times since then.

Many thanks to everyone who’s been reading, posting comments, and linking to my posts!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

One of my favourite Kate Bush tracks!

Looks like a very mixed bag there IT. You expect volatility from the smaller companies but I would have wanted a better result from RIT which offers capital preservation!

I seem to remember comparing the FTSE performance with global sometime last year which revealed that the FTSE has been underperforming for at least the past decade. In recent times I would thing the drag will have been a high exposure to the likes of BP and Shell and I don’t see that side of the market recovering. In fact BP look like they will be overtaken by Orsted before much longer!

Good luck with the rest of the year…

Great album as well.

RIT certainly hasn’t done as well as I’d like, although it was only down some 5% on a NAV basis as it swung for a premium to a discount. I’d say it’s more focused on limiting downside rather than capital preservation like CGT, RICA and PNL. But as long as the big tech stocks are in vogue, it’s going to lag behind I suspect, although it’s not alone in that.

With the UK market, the heavy oil/gas and financial components of the FTSE have definitely been a factor. And most retailers and utilities have struggled recently as well. I’m pleased I cut City of London loose, as that’s down 20% this year.

I think the FTSE and S&P were fairly similar in performance terms from the late 1990s up until 2013/2014 but the gap has grown ever wider since then. It looks Germany, Japan, and Europe as a whole have had similar trouble keeping up though.

https://ftalphaville.ft.com/2018/11/15/1542266674000/The-future-of-the-FTSE-100/

Hounds of Love surely was her best album…

That article was September 2018, a little further back than I remember. It seems to be around 2013 that the divergence begins and tech must have a big part to play.

http://diyinvestoruk.blogspot.com/2018/09/uk-v-global-investment-returns.html

Yes, with you on CTY. I offloaded in H2 2018 around the time that I started to build my ‘green’ portfolio…no regrets!

Ive been a long time fan of ITs since having a number of small savings schemes. They have done me proud and have helped fund a number of life events. Ive now put together long term global IT portfolios for my very young children SIPPs so a 50+ year outlook. I like the established historical ITs and RIT being one.

Congrats on the decent performance. It’s interesting to see what I think of as the ‘new gen’ e.g. Fundsmith/Smithson & Lindsell doing much better than the ‘old gen’ e.g. RIT, Caledonia, Murray International, which were pretty dependable in the 00s.

It’s what makes fund picking so tricky – trying to work out if this is temporary, or if the ‘old gen’ are done with because e.g. they’re old and rich and lack the hunger now, or if their style is no longer working etc. etc.

Ditto it’s a shock seeing the UK Smlr Cos which have been such stalwarts (I always liked SLS and RIII who have had very divergent performance more recently). I wonder if they’ll revive once Brexit uncertainty is cleared?

But more broadly, I am slowly reducing my overall European exposure, given that the Tech game seems to be done so much better in the US and China – there was a piece recently suggesting this was due to the reduced regulations for entrepreneurs compared with Europe. To clarify – I’m not saying I’m following the tech herd – but pretty much every company needs to be a tech company to survive now.

Good luck for H2!

Thanks Tom. A little less than decent I’d say but no disgrace.

Agreed on the changing of the guard – something I go back and forth on regularly! Less surprised about UK Smaller Companies as I would expect that to be a volatile sector, especially now with its domestic focus.