It’s been a tough year for tiddlers. UK small-cap investment trusts are down by more than 10% since last August with the average discount widening slightly to 11.5%. Henderson Smaller Companies is one of three such funds that I hold and it’s down a little more than the sector as a whole.

It would seem that Henderson is in good company, however. Other long-term top performers like Rights & Issues, BlackRock Smaller Companies, and Acorn Income have all posted double-digit losses this past year.

Funds specialising in micro-caps have posted even worse numbers, with three of them losing their investors more than 20%. Miton UK Microcap wins the wooden spoon, with a loss of nearly 30%.

Brexit is a key factor, as you might have guessed. Small caps tend to be more domestically focused than blue-chip stocks. The weakness of the pound is increasing the cost of imports and there are concerns the UK economy could struggle for a little while.

Let the bad times roll

No type of investment performs year in, year out of course. UK small-cap funds have dominated the performance stats over the last two decades like no other sector. The fact that they appear to be temporarily out of favour makes them an even more appealing place to put money, in my uneducated view.

I’ve been slowly building up a position in Henderson Smaller Companies, BlackRock Smaller Companies, and Acorn Income the past few years.

Henderson is the last fund in my portfolio I’ve yet to dedicate an entire article to. Earlier in August, it released its full-year results, so it seems like a good time to rectify that omission.

Key stats for Henderson Smaller Companies

- Founded: 1887

- Manager: Neil Hermon (since late 2002)

- Ticker: HSL

- 10-year net asset return: +372%

- Benchmark: Numis Smaller Companies index

- Current price: 790p

- Indicated spread: 788p-792p (0.5%)

- Exchange market size: 500

- Market cap: £590m

- Discount to net assets: 12.5%

- Costs: 0.42% OCF and 1.11% KID

- Gearing: 9%

- Number of holdings: 105

- Current dividend and yield: 23p and 2.9%

- Results released: Jan (interims) and Aug (finals)

- Dividends paid: Mar, Oct

- Style: UK small-cap, well-diversified and typically ‘larger’ small-caps

- Links: Website and AIC page

A small-cap veteran

As you can see, this is another very old fund, with over 130 years of history behind it.

It was known as The Trustees Corporation for nearly a century. Then in 1982, it became TR Trustees and then TR Smaller Companies, before adopting its current name in 1997.

Neil Hermon has run the portfolio since he joined Henderson in 2002. In addition to this trust, Hermon manages four open-ended funds.

Prior to joining Henderson, Hermon qualified as an accountant at Ernst & Young and then ran small-cap funds at Morley Asset Management and General Accident. As he joined Ernst & Young in 1989, I would guess he is now in his early 50s.

I’d expect Hermon to be at the helm for a few more years yet, but I do seem to have fund managers retiring on me left, right and centre at the moment. He’ll probably be gone by Christmas knowing my luck!

Nevertheless, Hermon doesn’t seem the flashy type that will go off and set up an eponymous asset management firm, like the other Neil now regrets doing.

Indriatti van Hien was appointed as Deputy Fund Manager in 2016 (often a sign that a changeover at the top is in the offing). Both she and Hermon hold shares in Henderson Smaller Companies, although no figures are mentioned.

The trust’s chairman is Jamie Cayzer-Colvin, who sits on the board of Caledonia Investments, where he oversees the fund investment division.

Four of Henderson Smaller Companies’ six directors are women, which is unusual but not unwelcome.

Less reassuring, though, is the fact the six directors’ combined shareholdings are just £200,000.

Investing style

‘Small cap’ is one of those terms that means different things to different people.

In the case of Henderson Smaller Companies, it means anything outside of the FTSE 100.

With the smallest stocks in the FTSE 100 (Marks & Spencer and Centrica I was surprised to see) worth some £4bn, that’s quite a wide range of shares that Henderson can invest in.

The bulk of the portfolio is in what I would normally call mid-caps (the FTSE 250).

A quarter of the portfolio is invested in AIM companies, where the generous exemptions with regard to inheritance tax are looking increasingly ripe for change. That’s something that could knock the value of AIM shares, especially if its removal was swift rather than gradual.

Henderson has six months to sell stocks that graduate to the blue-chip index because they have grown too large, and recently sold out of both Melrose and GVC Holdings for just this reason.

There are just over 100 stocks in the portfolio right now, with the largest positions representing just over 3% of net assets. So it’s very well diversified compared to the concentrated portfolios that seem all the rage at the moment.

There is an upper limit of 5% of net assets for a single holding.

In addition, Henderson cannot own more than 10% of an individual company’s shares, although only six of its holdings exceed 3% and the largest is 6.3% (Safestyle).

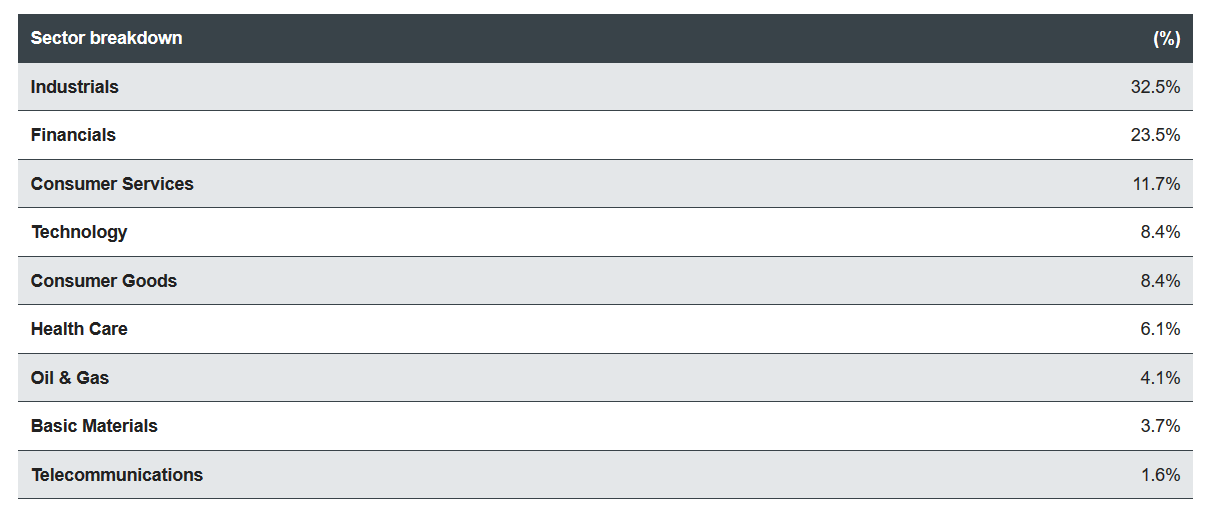

Sector split

The portfolio is invested over a number of sectors, but over half of it is under the vague heading of industrials and financials.

Here’s a more detailed breakdown:

From my point of view, there is a pleasingly low weighting in oil and zero in mining. For both ethical and financial reasons (most small companies in these sectors are speculative in the extreme), I hope this continues to be the case.

Henderson is generally a long-term holder:

Trading activity in the portfolio was consistent with an average holding period of five years. Our approach is to consider our investments as long term in nature and to avoid unnecessary turnover. The focus has been on adding stocks to the portfolio that have good growth prospects, sound financial characteristics and strong management, at a valuation level that does not reflect these strengths. Likewise we have been employing strong sell disciplines to cut out stocks that fail to meet these criteria.

Stock turnover does seem pretty low with about ten stocks coming in over the past year, including a few bought when they floated (such as AJ Bell and Codemasters) and a similar number departing the portfolio.

Half of the leavers were because of takeovers or elevation to the FTSE 100. The remainder were sold for operational or industry concerns, such as Elementis, NCC, Accesso and Ted Baker.

Portfolio details

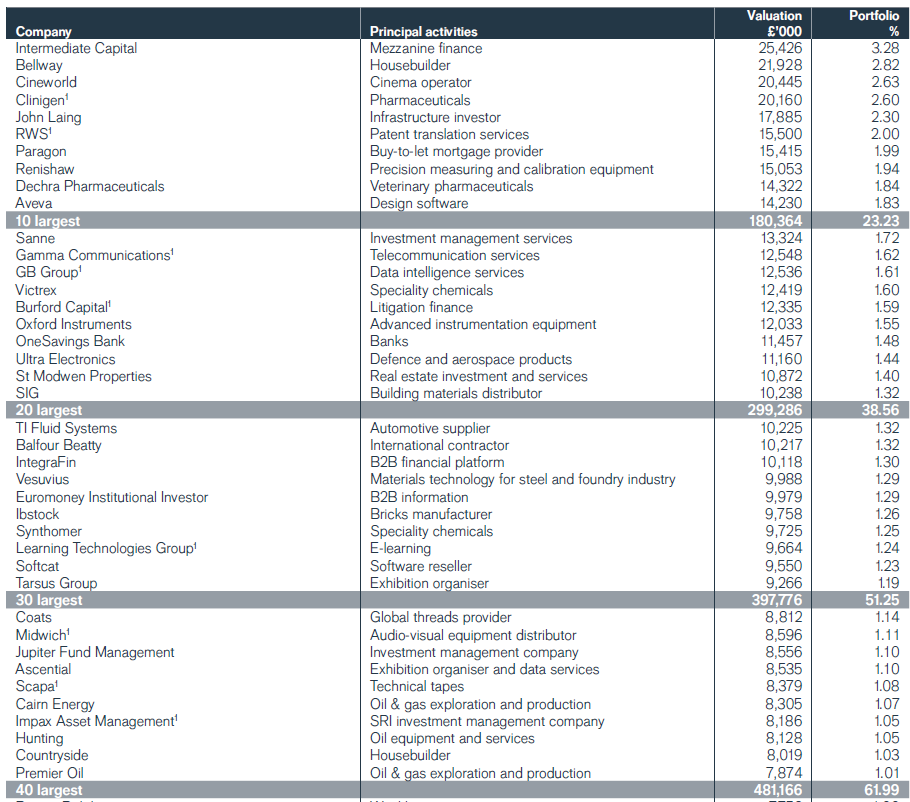

Here are the top 40 positions as of 31 May 2019:

It seems like a decent and diverse collection of businesses to me.

RWS and Aveva were big winners for the portfolio last year, while Renishaw, Just Group, and Victoria were the biggest losers. Renishaw remains in the top 10 and Just Group is now the 59th biggest holding at 0.7%. Victoria has been shown the door.

One thing I did notice was the inclusion of Burford Capital, a Woodford and Invesco favourite that was savaged in a shorting attack by Muddy Waters last week.

Henderson’s position size in Burford was 1.6%, so this should have limited the damage somewhat, assuming it is still in the portfolio.

Rip-roaring returns

Performance under Hermon appears to have been excellent. I couldn’t find exact figures, but the recent results say he has beaten his benchmark in 14 out of 16 years since taking charge.

Last year was one of the two exceptions, but the underperformance was just 0.3%.

The dividend for Henderson Smaller Companies has been increased in all 16 years as well.

The benchmark used is a little bit of an issue, though. The Numis Smaller Companies Index is fairly well known and it covers the lowest 10% of the UK market as measured by market value.

Henderson’s sweet spot is companies that are a little larger than this. Indeed, of the top 10 positions it holds, only one (Paragon) is included in the Numis Smaller Companies Index!

I’m not sure there is an easy answer to this, though. A composite of the FTSE 250, FTSE Smallcap, and FTSE AIM100 indices might be a better fit. But it would also be a bit messy.

There is a 15% performance fee payable for returns over the trust’s benchmark. So, I’d be interested to know there was a material difference if that composite measure was used instead.

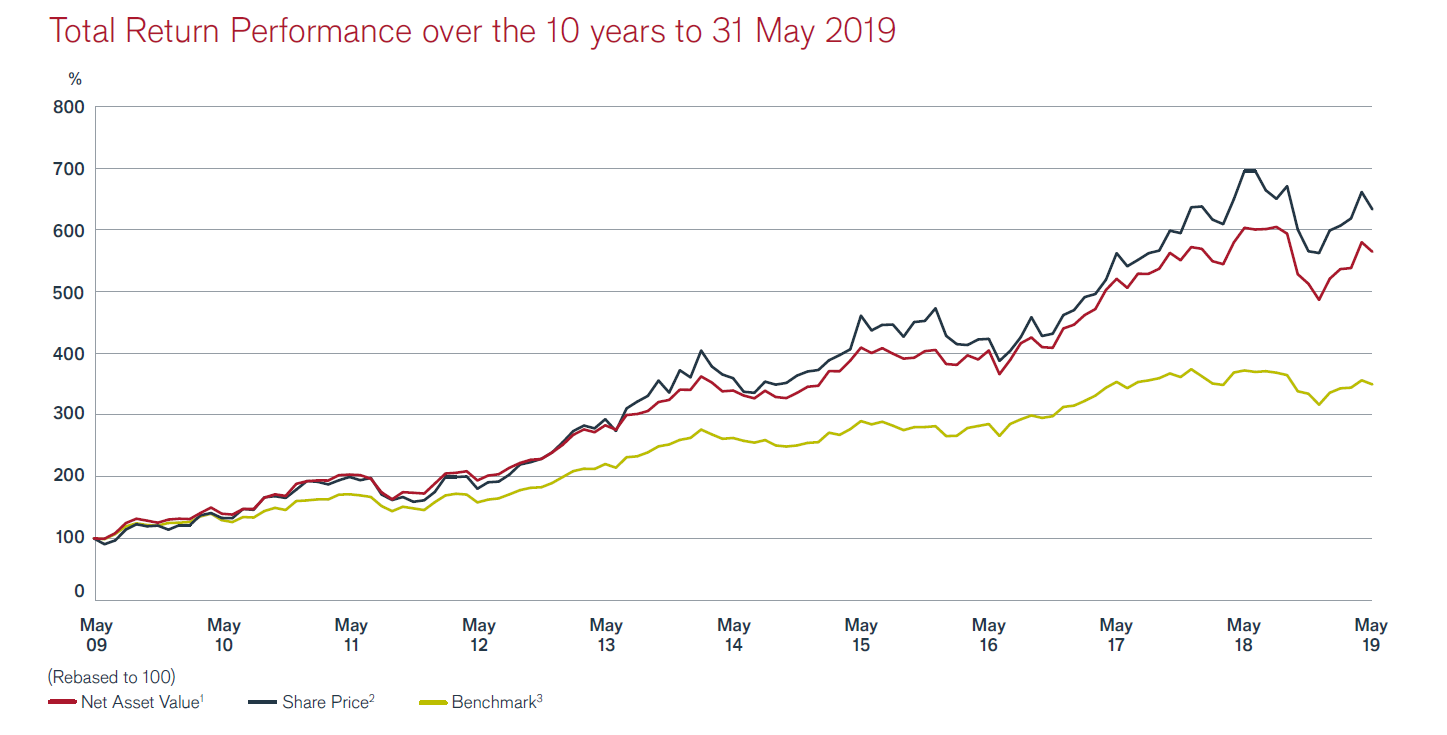

Compared against other small-cap investment trusts, Henderson has done well in performance terms. The sector average over the ten years to May 2019 was 346% on a net asset basis while Henderson posted 481%. The Numis Smaller Companies index rose a mere 250%.

You can see what difference the start point makes, though. The ten-year return to early August 2019 for Henderson Smaller Companies is 372%, as it misses out the start of the recovery from the financial crisis in the Spring of 2009.

Gearing up and down

In such a strongly rising market, the fact that investment trusts can use gearing should mean they outperform their benchmarks. That’s assuming their costs aren’t excessive and the benchmark is a sensible comparative.

Gearing took 0.5% off returns in the year to May 2019 but added 0.3% in the previous twelve-month period.

Henderson Smaller Companies can gear up to 30%, according to its Investment Policy, but gearing over 10% seems to be relatively unusual.

Currently, there are £90m of borrowing facilities in place, which is equivalent to 13-14% of net assets. Total borrowings at the last year end were somewhat lower, at £59m.

Fees look fair

Despite my niggle about the benchmark for the performance fee, the overall costs for this fund seem pretty reasonable.

The basic management charge is just 0.35% and there is a combined cap of 0.9% when any performance fee is payable.

Directors’ fees total just £150,000 and range from £24,000 up to £35,000. The latest annual increase was just £500 each, and the Articles limit total fees to £200,000.

The ongoing cost figure excluding performance fees has fallen from 0.58% to 0.42% over the last ten years. In six of those ten years, a performance fee has been payable, usually raising costs to the 1% mark.

The costs in the Key Information Document aren’t significantly higher. The 1.11% in the latest version includes 0.36% for performance fees and 0.12% in transaction costs (more evidence that this is a fairly low turnover portfolio).

Why ‘strong and robust’?

Well, these seem to be among Henderson’s favourite words.

Strong and its derivatives are mentioned 22 times in its latest results. Robust and robustly feature 9 times.

But it seems a fair description. To me, this seems to be a well-diversified and balanced portfolio, with a sensible level of gearing.

It fishes in safer waters, as far as small caps go. Despite that, it’s consistently among the top-performing UK small-cap funds and its costs are competitive to boot.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.