Smithson, Fundsmith’s global small-cap investment trust, has had an eventful 2020. Its wild movements are a perfect example of why trusts can be a little bit tougher to own than other funds when the market goes through a rocky patch.

Between 19 February and 28 February, Smithson’s shares plunged 18% as markets struggled to assess what impact the coronavirus might have on the global economy.

Smithson’s net asset value (NAV) fell by 11.5% over the same period and its shares briefly traded at a discount for the very first time.

It’s a useful reminder that investment trusts can see magnified falls when investors take fright. Discounts often widen at times like these, as we saw during the global financial crisis.

Since the end of February, Smithson shares have bounced back, slumped again, and rebounded a little.

It’s hard to keep up these days…

Key stats for Smithson

- Listed: October 2018 at 1,000p

- Managers: Simon Barnard and Will Morgan — overseen by Terry Smith

- Ticker: SSON

- Benchmark: MSCI World Small and Mid-Cap Index (SMID) in £

- Recent price: 1,262p

- Indicated spread: 1,258p-1,266p (0.6%)

- Exchange market size: 2,000

- Market cap: £1.5bn

- Premium to net assets: 1.5% (4 March 2020)

- Costs: 1.0% OCF, 1.1% KID

- Gearing: Nil, 0.5% net cash as at 28 Feb 2020

- Current dividend: Nil

- Results released: Feb (finals) and Aug (interims)

- Sector: Global smaller companies (1st out of 5 over 1 year)

- Links: Website and AIC page

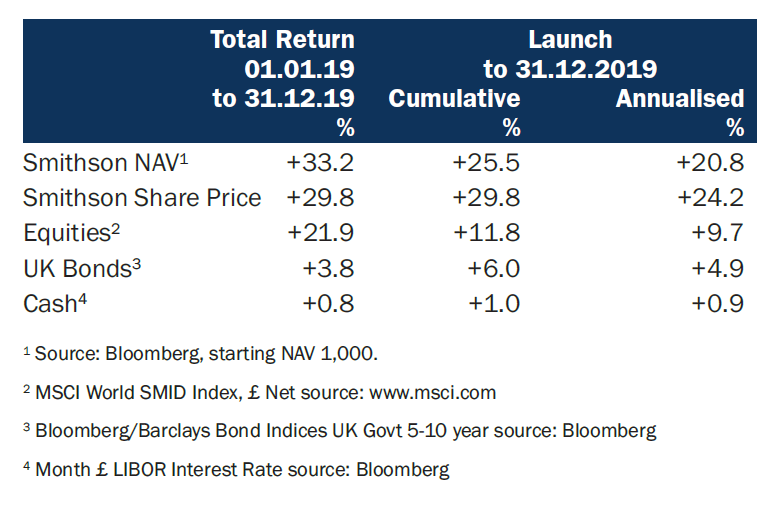

The end of February saw the publication of Smithson’s first full set of accounts, so let’s check on its overall progress.

An impressive performance to date

It’s still early days but Smithson has done very well so far:

The February 2020 factsheet shows Smithson’s NAV had declined by 4.5% year-to-date while the MSCI World SMID had fallen by 7.6%. So Smithson’s lead has widened a little more since the end of 2019.

Of course, these figures are already rather dated but let’s stick with for the moment.

On an annualised basis, to the end of February 2020, Smithson was 11.7% ahead of its benchmark. I would be very surprised if that level of outperformance continued in the long term.

I’d regard a 5% lead as excellent once we got to the 5-year mark. Fundsmith Equity has a 6.3% annualised lead over its benchmark over nine and a bit years.

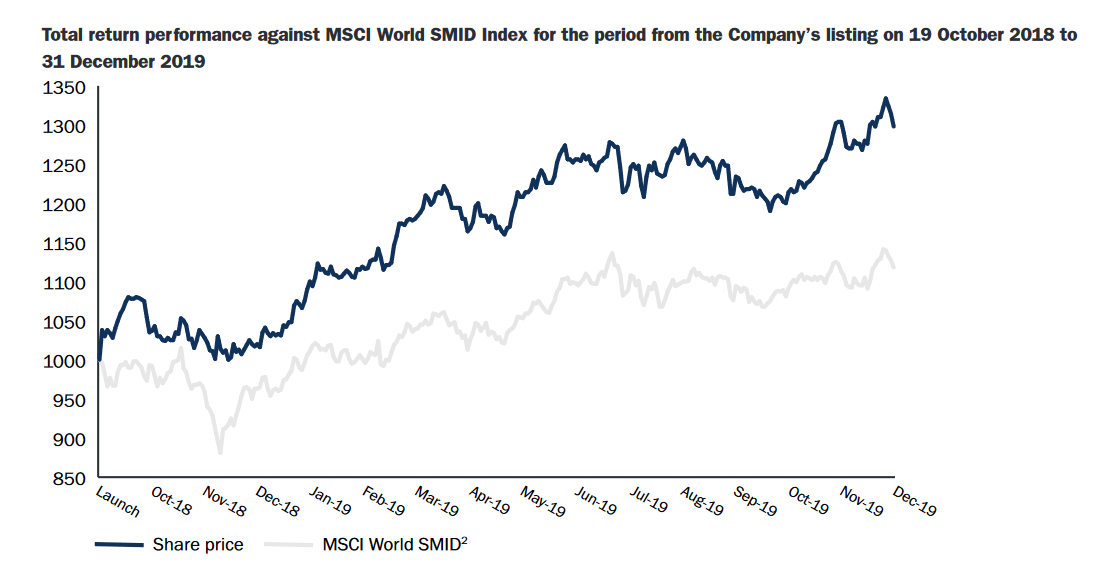

This chart shows how the Smithson share price and its benchmark have diverged in a little more detail:

Just eyeballing the chart, we can see that the decline in late 2018 helped Smithson as its shares held pretty firm during the worst of the market falls back then.

And the gap grew bigger in the last quarter of 2019 as well, although this time it was Smithson doing well while the SMID mostly tread water.

I remember Terry Smith commented at last year’s Fundsmith Emerging Equities AGM that, in his experience at least, outperformance often came in little spurts like this, with funds largely matching the market most of the rest of the time.

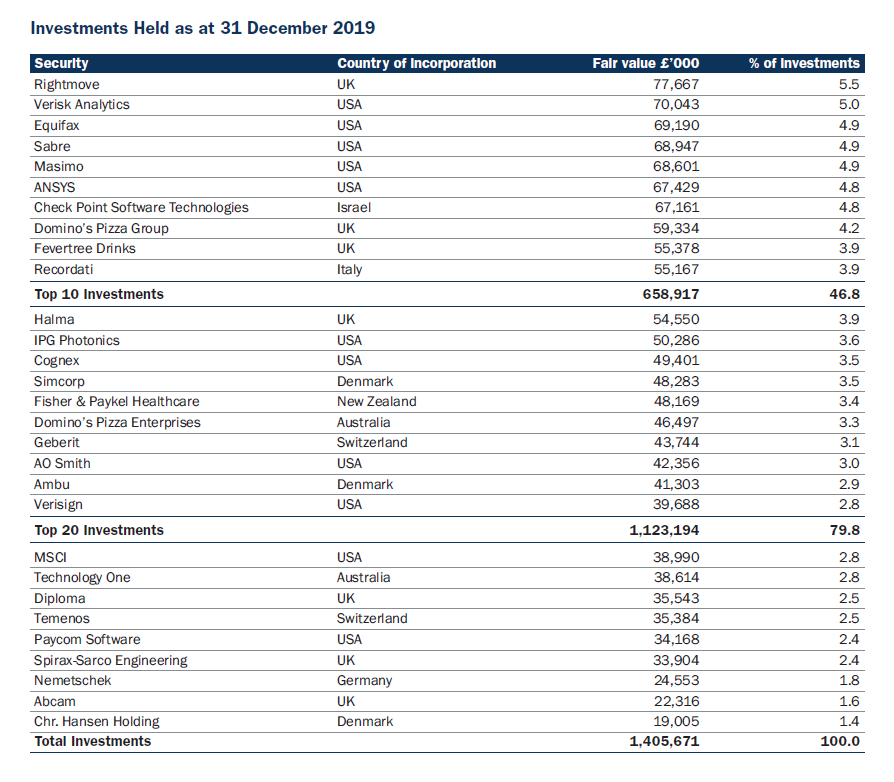

The portfolio

Little has changed here throughout 2019, apart from the usual justling of positions:

There are 29 holdings in total, with position sizes varying from 1.4% to 5.5%.

Rightmove has since vacated the top spot, switching places with Verisk.

Sabre is worth a mention, as it has since dropped out of the top 10 entirely. It was Smithson’s second-largest position when the first factsheet was published for November 2018 and has been a regular in the top 10 ever since.

A quick look at its business description reveals the reason: Sabre is the largest global distribution systems provider for air bookings in North America.

Sabre’s share price has fallen from $22 to $13 these past few weeks and it’s currently investing heavily to boost both its profitability and the size of its addressable market come 2024.

Splitting down the portfolio

As we’ve seen before with Smithson, and indeed the main Fundsmith fund, the country and sector splits aren’t that informative.

Many of its businesses are global, so the country of listing can be somewhat misleading.

Likewise, 40% in Technology and 40% split between Industrials and Healthcare doesn’t give that much insight into the individual businesses Smithson holds, due to the broad definitions of these sectors.

But comparing Smithson the MSCI World is somewhat revealing. Information Technology is 25 percentage points higher in Smithson and Healthcare nearly 10%, with the difference made up by a lack of financials, property, materials, energy and utilities.

And looking at Fundsmith Equity, Smithson only has some 4% in Consumer Staples versus Fundsmith’s 32%, with Information Technology and Industrials making up most of the difference.

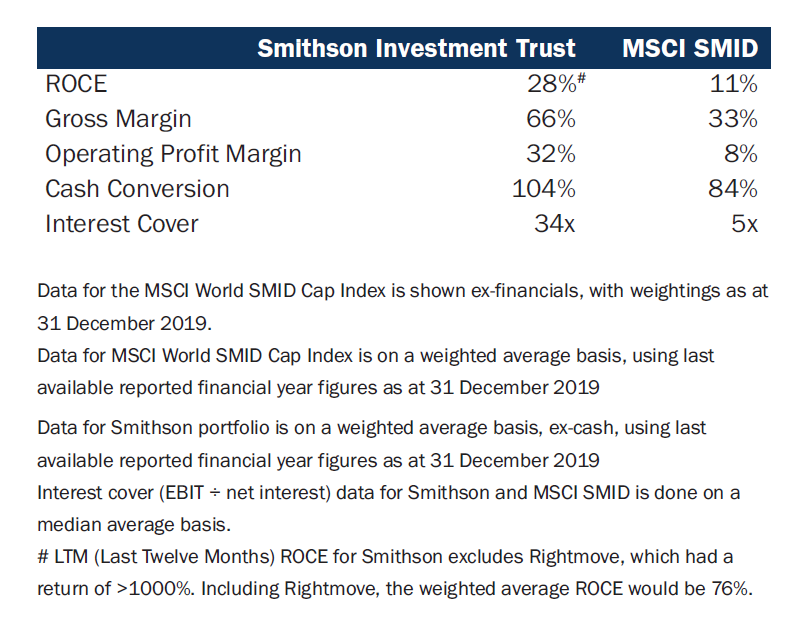

Smithson also provides the usual Fundsmith portfolio look-through:

The main thing that caught my eye here was the footnote about Rightmove’s incredibly high return on capital employed figure.

Some investors have reportedly been uncomfortable with the large size of this position, thinking that Rightmove is very sensitive to the state of the UK economy. But Smithson points out that Rightmove receives “a fixed monthly subscription fee irrespective of the number or value of the houses advertised”.

Smithson added materially to its position in early 2019 when the Rightmove share price fell on Brexit deadline concerns.

Rightmove floated in March 2006 at the equivalent of 33.5p (it had a ten for one share split in 2018). It’s now over £6, representing growth of over 23% a year.

One in, one out

One of Fundsmith’s three investing tenets is to “Do Nothing”, i.e. minimise the level of buying and selling within a portfolio.

Smithson has largely achieved this, having sold only one position (CDK Global in September 2019) and bought one (Fevertree from July 2019) in its first eighteen months of existence (once its initial portfolio was set up).

It raised £40m from selling CDK and probably spent around £60m on Fevertree so that’s a very low portfolio turnover compared to its £1.5bn of assets.

CDK Global was another top 10 position before it fell from grace. A management change in late 2018 prompted a shift in strategy and a promising new product turned out to be, well, not so promising after all.

Fevertree is yet to cover itself in glory. Its share price was probably £21/£22 when Smithson started building its position and it even broke into the top 10 positions in November 2019.

That didn’t last long, though, with it dropping out by January 2020. Fevertree’s recent trading update showing flat UK revenue growth for 2019 and has knocked the shares down to £13.

Interestingly, Fevertree made two appearances in the illustrative stocks section of Smithson’s IPO presentation, so its eventual inclusion in the portfolio shouldn’t have been a great surprise.

Nick Train has recently added Fevertree to Finsbury Growth & Income, so Smithson isn’t the only trust to be lured in. And it’s long been a favourite of Max Ward at Independent Investment Trust.

Don’t expect a dividend anytime soon

For reasons I don’t recall, I spent a little time speculating on what level of dividend Smithson might pay last time I wrote about it.

I estimated 1p per share and it turns out I was only 1p out.

The underlying yield of the portfolio is roughly the same as the trust’s operating expenses so there’s unlikely to be a dividend in the near future. It has said that it does not intend to pay dividends from capital.

Gearing up?

Smithson has generally run with a 3-4% cash position throughout 2019, but it had reduced this to 2% by the end of the year and to 0.5% in February 2020.

I think that’s the lowest cash position it has had to date so there may have some buying during the February market decline.

The portfolio can be geared up to 15% so there could be some borrowing utilised as well. Personally, I would want to see it used sparingly.

Charges

Smithson’s basic management fee is 0.9% and other admin charges only take this up to 1.0%.

That doesn’t sound too bad but Fundsmith has earned £12.5m already from Smithson (up to the end of 2019). Other admin costs were £1.4m, as were transactions costs charged to capital.

Terry Smith has form for keeping his management fees unchanged as funds under management mushroom. And there’s little doubt that Smithson is highly profitable for Fundsmith.

It’s incredible to think that the initial target was just £250m for its IPO. Smithson ended up raising £822.5m and the number of shares has increased by 44% since then.

I’d still like to see a tiered performance fee introduced here but it’s safe to say that I’m not holding my breath.

There was a fee reduction at Fundsmith Emerging Equities Trust recently, from 1.25% to 1.0%. But this seemed to be a reflection of FEET adopting a Smithson-like operating structure with Terry Smith (Fundsmith’s most expensive resource, as he calls himself) having far less day-to-day involvement in running the portfolio.

Skin in the game

The 3 directors of Smithson still own the same 35,000 shares between them.

Terry Smith and other Fundsmith employees own just over 3 million shares. Their combined stake has dropped from 3.6% to 2.6% over the course of 2019 as the trust’s share count increased.

According to the Smithson prospectus, 2.5 million was to be owned by Smith with around 0.5 million held by other folks. There was a one-year lock-in period which would have expired in October 2019.

Size matters

Capacity and illiquidity concerns are front of mind with trusts like this at the moment so it’s worth revisiting the numbers here.

Smithson says its target range is £500m to £15bn but it expects its ‘average’ company to be worth £7bn. It’s around that level now.

Its smallest UK-listed companies are Domino’s (£1.3bn) and Fevertree (£1.5bn) so I would estimate it owns about 4% and 2% of these companies’ shares respectively. That doesn’t ring any alarm bells.

But it already seems somewhat unlikely that a top 10 position could be built in a sub-£1bn company. A 4% position for Smithson, enough to make its top 10, would require buying 6% of a £1bn company and 12% of a £500m one.

If, and it seems a big if in current market conditions, Smithson continued its performance of around 15% a year and issued new shares at much the same rate, it could be a £5bn trust in around five years. That could make sizeable positions tricky in anything valued under £2bn.

Smithson does address this in its annual report to be fair:

We feel this issuance process can continue for several years before the performance of the Company is affected by its increased size. As a closed-ended fund, we will never be forced to liquidate positions to meet investor redemptions. However, if the size of the Company is starting to have an impact on the way we wish to run it, we will request that the Board of the Company stop issuing new shares.

I think this is something to be mindful of, but I’m comfortable with the current situation.

Summing up

I’ve continued to add to Smithson since buying at its IPO back in 2018.

And I confess the recent market fall tempted me once more, although I missed the sharp fall right at the end of February. Smithson says it isn’t any good at market timing and I’m probably even worse!

I’ve got no idea how long for or to what extent the coronavirus will continue to affect markets and the global economy. So my overall strategy is largely unchanged, namely to keep dribbling in cash to my portfolio as it becomes available, tweaking position sizes as I do so.

I plan to add a little bit more Smithson over the next few months, bringing it up to roughly the same percentage in my portfolio as my other small-cap investment trusts, particularly if I can catch it at a discount.

Its AGM is being held on 30 March 2020 and there should be a presentation from manager Simon Barnard. It will be interesting to see the dynamic between Smith and Barnard at the meeting. [As it turned out, this presentation was online-only and can now be viewed at https://www.smithson.co.uk/tv — the Q&A session in the last 10-15 minutes is the most interesting bit in my view].

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Thanks for another comprehensive update. I have been regretting not buying at IPO, but the price today makes me feel better about not piling in over the past year. Though who knows what happens from here.

On a broader note, I was surprised/interested/disappointed to see Capital Gearing down by so much today. My best guess is that the size of it now means that people have been using it for liquidity, and are selling today to raise cash for bargains.

It’s also amazing to think how LTI at 1060 seemed like such an extraordinary bargain a few weeks ago.

And to go even broader, it’s been easy to forget that the boom of the past 5 years has made most investment trusts go to such historically tight discounts – I presume that they will start to go back to more usual ones, which could be brutal for those who bought in the past few years.

Thanks Tom.

I don’t think SSON dropped below the £10 IPO price in the last quarter of 2018, but the premium was a bit chunkier then as they hadn’t really started issuing extra shares.

But it’s down to 1,060p right now so the IPO price is within touching distance given 5% daily swings seem to be the new normal.

CGT is a little odd. I make CGT/PNL/RICA all down around 3% year to date before today’s move. But whereas RICA is up a little today, both PNL and CGT have fallen a fair bit.

I’m anticipating wider discounts for most trusts as well, although with a lot of NAV info a bit behind events the numbers are jumping around a bit right now.

For example, looking at the AIC data for Global trusts, a weighted premium of 1% at the end of December had turned into a 5% discount by the end of February. The most recent daily figure (11 March) suggests the discount had reduced to 1%, which is surprising.