We all have stories about investments that got away. One of mine concerns a technology investment trust that I ditched a long time ago.

In April 2001, I bought a chunk of Henderson Technology Trust. I thought my timing was pretty good, as the bear market in tech shares was already a year old by then, making a rebound seem likely. Of course, the bear continued to growl for two more years.

Henderson Technology was in the process of leaving the Henderson stable at the time. Shortly after, it became Polar Capital Technology. I came across an old file of contract notes at the weekend and I can see that I paid 258p per share.

Fast forward to 2004 and I was becoming more attracted to the simplicity of index-tracking funds. While tech shares had recovered a little, I felt I needed a little more diversification.

Of course, things looked very different in the world of tech back in 2004. Microsoft was busy fighting various anti-trust battles in the US and in Europe. A company called Google joined the stock market that year and another called Facebook was founded.

It was three years before the launch of the iPhone and a decade before the term ‘FANG Stocks’ had even been created. Amazon’s market cap was $15bn (it’s now $800bn) and Netflix’s was $500m (now $150bn).

Polar Capital got the boot for 166.25p per share (a loss of about 35% over three years) and I switched the money into an ETF tracking the European market.

Oops!

Feast or famine with sector funds

It actually took several more years for the Polar Capital Technology share price to recover to what I initially paid for it.

Indeed, looking at its long-term performance provides a good illustration of how sector funds like this can stay out of fashion for several years.

By the end of 2008, its share price had sunk to about 100p. But two years later the share price passed my 2001 buy price and it’s never looked back. It reached nearly £14 last summer. It’s slipped a little since, but the shares are still north of £12.

If I had continued holding since 2001, I reckon I would have made 9% a year, but with all those gains coming from 2010 to 2019. Sticking with sector-specific funds throughout all the ups and downs can be really tough.

Of course, the FTSE All-Share was flat from 2001 and 2010 as well, but at least its constituents paid out dividends each year to ease the pain.

Had I not sold this trust in April 2004, my gains from that point on would have been around 14% a year. The European ETF got switched into other investments at some point, making the sums a bit gnarly. But I’m pretty sure I would have been better off sticking with the tech fund.

I’ve been reshaping my portfolio these last couple of years and one of the questions I’ve been considering is whether to reintroduce some specific technology exposure. (I do hold HgCapital Trust, which is a private equity fund that specialises in technology, so I am not a complete luddite.)

On the one hand, technology is obviously the future. My own life and my spending patterns are becoming increasingly digital. On the other, tech has had a stellar run and could be set for a prolonged period of lower returns, especially with the increased regulatory scrutiny the sector is getting.

Six runners and riders

All things considered, I reckon that big tech shares are looking a little bit more sensibly priced than they were 12 months ago. Therefore, it seems like a good time to review the state of play and see what’s on offer.

There are six trusts that stand out for me. In terms of pure technology funds, there is Polar Capital Technology (censored mutterings) and there’s also Allianz Technology. The latter is about a quarter of the size of the former.

The AIC technology sector contains a couple of more specialised funds: Hipgnosis Songs and Augmentum Fintech (in which RIT Capital Partners has a 20% stake). These both have assets of around £100m but only joined the market in 2018. While they are both interesting in their own way, they are not really what I’m looking for here.

Herald Investment Trust may be though. It sits in an AIC sector called Small Media, Comms and IT. Herald has been very ably managed by Katie Potts since it launched in 1994 and it has much more of a UK focus than either Polar or Allianz.

There are three global funds that are worth considering I think, two of which are run by Baillie Gifford. Strictly speaking, of course, they are not technology funds but they have such a strong tech focus it would seem churlish to exclude them.

The mammoth Scottish Mortgage needs no introduction. Edinburgh Worldwide is less well-known than its Baillie Gifford stablemate. Lastly, there’s Manchester & London, which is by some distance the smallest of the six.

If there are any tech funds you think I’ve left out, please let me know in the comments section at the end of the article. I did briefly think of adding Woodford Patient Capital to this list, but it only has a four-year track record and has lots of extra baggage to consider right now.

Tech trusts compared

Here’s a side-by-side comparison:

| Trust | Assets | (Disc)/ prem | Holdings | US | UK | 10yr NAV | Launched | Charge |

|---|---|---|---|---|---|---|---|---|

| Allianz Technology (ATT) | £493m | (2) | 70 | 86% | 3% | +655% | 1995 | 1.2% |

| Edinburgh Worldwide (EWI) | £565m | 0 | 105 | 62% | 17% | +478% | 1998 | 0.8% |

| Herald (HRI) | £990m | (15) | 285 | 52% | 25% | +476% | 1994 | 1.1% |

| Manchester & London (MNL) | £138m | (2) | 24 | 73% | 0% | +121% | 1972 | 1.0% |

| Polar Capital Technology (PCT) | £1.8bn | (6) | 114 | 65% | 2% | +651% | 1996 | 1.8% |

| Scottish Mortgage (SMT) | £7.9bn | 3 | 83 | 51% | 3% | +688% | 1909 | 0.4% |

Note: Charge is the ongoing charge including performance fee. Other data is as of 28 February 2019 and latest factsheets.

The fact that most of these funds trade at a discount, albeit a small one, was a little unexpected given their gains over the past decade. Herald is by far the cheapest on this measure and has consistently traded at a discount of 15%-20% for a long time now.

With the exception of Manchester & London, most of these funds have a large number of holdings. Although, as you can see from the tables I’ve included later in this article, some of their top 10 positions can be pretty chunky.

Performance-wise there is little to choose between the two main tech funds and Scottish Mortgage over the last 10 years. I was little surprised Scottish Mortgage had such a relatively low US weighting, but then it does have 24% in Chinese stocks (e.g. Tencent, Alibaba, and Baidu).

Edinburgh Worldwide and Herald, with higher UK weightings, haven’t done quite as well. Manchester & London lags a long way behind in the performance stakes, but then it only really made the switch to tech shares in the last few years.

When it comes to charges, it’s no surprise to see that the two Baillie Gifford funds are the cheapest. Polar is by some distance the most expensive, with its performance fee being the main reason.

I left gearing out of my table, but most of these trusts seem to hold a small net cash position. The two Baillie Gifford funds carry a little bit of borrowing, though.

Dividends aplenty

Only joking! Tech is not a sector for income seekers.

Scottish Mortgage yields about 0.6% and Manchester & London 2.7% (paid out of capital as far as I can tell) but that’s your lot here.

Edinburgh and Herald paid out a small dividend up until 2013, but I don’t think either Allianz or Polar have ever paid a dividend (although I haven’t checked all the way back to their launch dates).

Biggest holdings

I thought I’d look at each fund’s biggest holdings, to see what sort of overlap there is. I’ve grabbed screenshots from the latest factsheets so there is a hotchpotch of formats below. You can click on each image if you want to enlarge it.

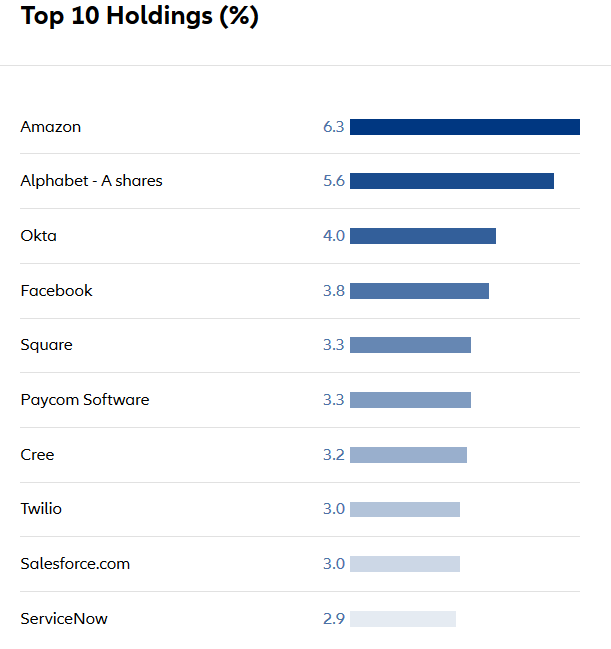

Allianz Technology

Edinburgh Worldwide

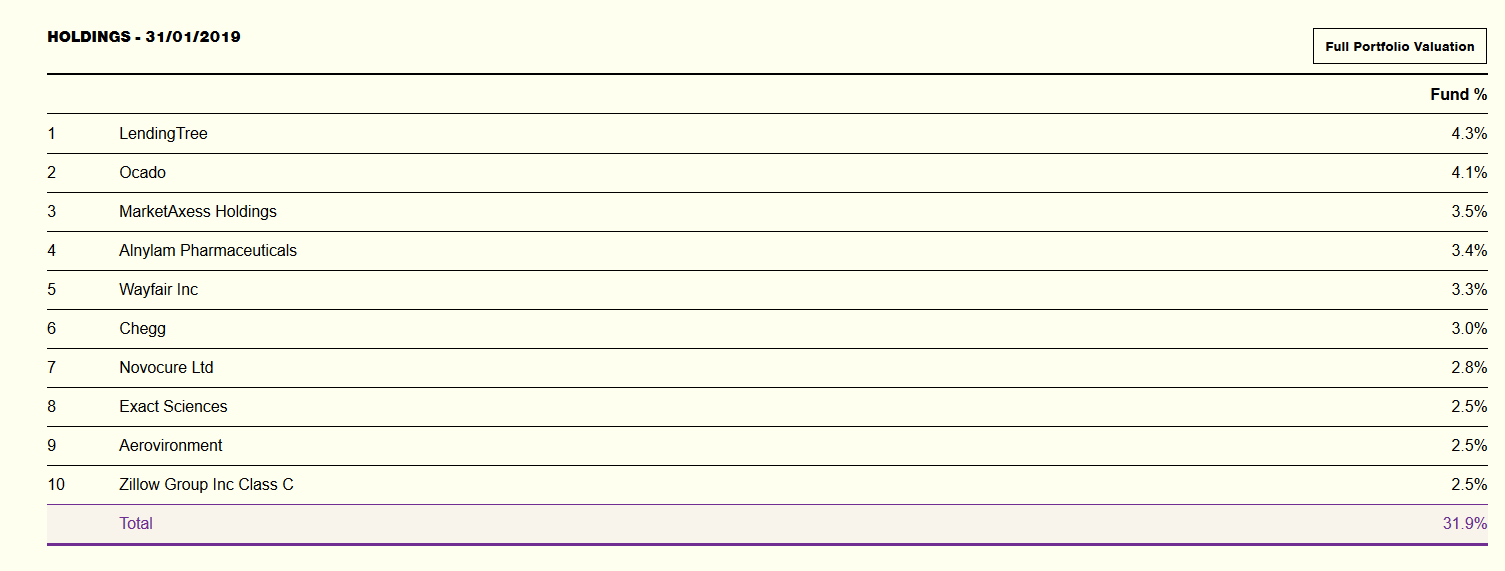

Herald

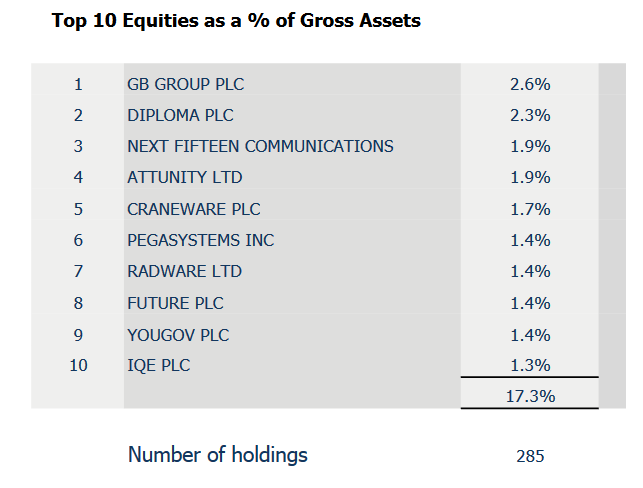

Manchester & London

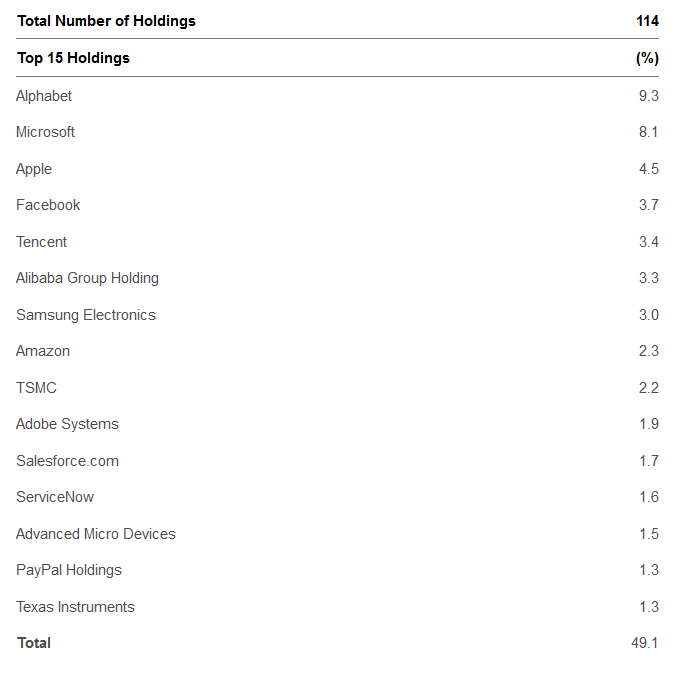

Polar Capital Technology

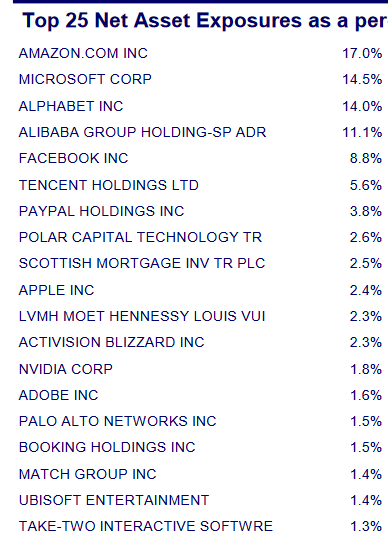

Scottish Mortgage

Polar Capital and Manchester & London arguably have the most orthodox set of holdings, although the latter is much more concentrated with 65% in its top 5 positions. It also holds 5% of its assets in Scottish Mortgage and Polar Capital, which also invest in many of the same companies, effectively nudging that 65% a little higher.

I quite like Allianz’s approach with a mixture of tech giants and up-and-coming firms like Twilio, Square and Okta. Its manager is based in San Francisco, close to the legendary Silicon Valley.

Both Edinburgh & Herald concentrate on smaller companies, so there’s a case to be made for holding one of them plus one of the more mainstream funds. Edinburgh also has a penchant for biotechnology — this sector makes up about 16% of its portfolio.

It’s also worth noting that Scottish Mortgage has 16% of its assets in unquoted companies, with small stakes in the likes of Airbnb, Lyft, SpaceX, and Slack alongside a lot more companies I’m not particularly familiar with.

Edinburgh Worldwide has 4% in unquoteds and Herald has 2% (but is considering adding more). The other three don’t seem to own anything much in the way of private companies.

Overweight in the US

One thing worth considering when it comes to tech trusts is your existing exposure to the US market.

The US had a great run in the last 10 years, mainly because it’s home to the vast majority of big technology companies.

A few months ago, I calculated the US weighting of my portfolio to be 44% compared to 55% for the FTSE All-World index. So a little extra Stateside sauce shouldn’t be too much of an issue for me.

This chart from Ben Carlson at A Wealth Of Common Sense (essential reading if you’re not familiar with it) provides a useful long-term perspective of how US stocks have performed relative to the rest of the world these past five decades.

You can see the lead has changed a few times, but the US market has raced ahead in the last 10 years, so it wouldn’t be surprising the rest of the world regained some ground. I’d be reticent about increasing my overall US weighting much beyond, say, 50%.

A tentative toe?

I’m tempted to tiptoe back into technology and also to add some specific biotech exposure (an article on this will no doubt follow at some point). And I have a holding in City of London Investment Trust that is kind of earmarked for new investment opportunities like this.

Right now, I would say Allianz and Herald appeal the most, but I want to look at them more closely before pulling the trigger. A cheaper entry would be ideal, but I suspect I am most likely to drip in cash over the next few years.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.