Last weekend saw the first Mello Virtual investing conference, concentrating mainly on UK small-caps and trusts/funds. I very much enjoyed the physical version last year and I’d say this one was equally good.

Before I get into some of the interesting tidbits I picked up, though, some rambling thoughts on the overall event…

All change

This virtual conference was put together put speedily once it became apparent that the usual in-person version couldn’t go ahead as planned this summer.

Tickets were available for less than a tenner (a little cheaper than normal I think) and it proved so popular an extra day was added on the Friday, supplementing the main Saturday programme.

Most of the presentations were pre-recorded but there was usually the opportunity to join a live chat with the presenters afterwards or ask them questions on the company’s virtual stand.

There were also half a dozen live sessions each day on Zoom from the likes of John Baron, the Money Makers podcast, the Stockopedia Small-Cap Value Report, and Twin Petes Investing.

And both days closed with a BASH session (Buy, Avoid, Sell or Hold) where half a dozen luminaries chewed the fat on divisive small-cap shares, such as Boohoo, Games Workshop, Burford, and Plus500.

Most of the shares featured seemed to be Sell or Avoid as far as I remember, both among the panellists and in the snap poll of people watching.

Apparently 500 people in total viewed those two sessions and from comments made on the other live parts, decent numbers seemed to be tuning in.

Works for me

I’m not sure virtual conferences will totally replace physical ones, but there are definitely a number of advantages.

They are far easier to attend of course. I’m an hour from most of central London, where most of these events tend to get held, but I can imagine how frustrating it is for those who live further afield.

Another plus point is that you don’t run out of seat space or get interrupted by late arrivals or early leavers. What’s more, if something doesn’t appeal to you, it’s simple to duck out halfway without hurting people’s feelings!

I thought the Q&A sessions worked a lot better. You could submit questions at any time, as a thought occurred to you, and then the hosts were able to pick out a varied selection at the end.

In fact, a few of the sessions I was in overran a bit, as the questions kept on flowing in. This sometimes meant the next session was delayed a little.

Being able to flick between presentations very easily meant I probably saw more than I would have done at a physical event. However, you do miss out on the casual chats that take place around the venue during breaks.

It was surprisingly tiring, though. Watching presentations on a screen for several hours certainly taxes the grey matter!

Potted highlights

I think most of the content is being restricted to Mello ticket holders for a month before being made more publicly available.

Sandford DeLand Free Spirit

Sandford DeLand is best known for its UK Buffetology fund. Launched in 2011 and run by Keith Ashworth-Lord, UK Buffetology is top of 201 UK funds since inception with a return of 225%. The UK market is up some 60% over the same timeframe.

Sandford DeLand Free Spirit was a new name for me. This open-ended fund got going in early 2017 and is far smaller at just £13m versus UK Buffetology’s £1.3bn. However, it uses the same methodology of ‘Business Perspective Investing’ based on the teachings of Warren Buffett and Benjamin Graham.

It’s a smaller company fund although it does own some larger stocks (Unilever, RELX, LSE) to provide some liquidity. Its performance to date has been impressive — it’s up 34% over the last three years, versus -5% for the UK All Companies sector.

Free Spirit seems to have outpaced pretty much all the two dozen UK smaller company investment trusts over the last three years. The best performers have been JPMorgan Smaller Companies (up 34%) and BlackRock Throgmorton (up 42%), although they have both benefited from discount narrowing.

Neither of the Sandford DeLand funds are cheap, with ongoing charges of 1.2%. And despite being only 3 years old, Free Spirit is already on its second manager.

It was originally run by Rosemary Banyard, a long-term associate of Andy Brough, the small-cap specialist at Schroders. Banyard left Sandford DeLand last year and has since joined Downing. Incidentally, she was also presenting at Mello, with a well-received session on reading the fine print of annual reports.

Free Spirit is now run by Andrew Vaughan. He seems to have reshaped the portfolio a fair amount, cutting out some the overlap with UK Buffetology.

The fund has held up pretty well in 2020, down just 7%. That puts it 8th out of 249 UK open-ended funds. And only 3 out of 24 UK smaller company investment trusts have lost less than 15% (although discount widening has played a part in this).

So an interesting one to keep an eye on. With just 25 holdings, it’s a highly concentrated portfolio.

Vietnam Holding

I only caught part of this video but there were some interesting facts on Vietnam, particularly on how successful it’s been combating COVID-19.

For example, it was able to have just a 3-week lockdown and has gone 75 days without any community cases and zero deaths. And that’s with a population of 100 million.

Vietnam Holding is one of three investment trusts that specialise in Vietnam. It has net assets of £100m, which makes it by far the smallest of the three. It’s also the youngest, having been launched in 2006.

I think the other two Vietnam trusts have performed a little better over the long term, but the numbers aren’t that easy to analyse as Vietnam Enterprise shifted its listing from the Irish market to London after merging with another fund.

Country-specific trusts are generally a little too specialised for my liking, but they may appeal to the more adventurous.

John Baron

As well as being an MP, John Baron provides a subscription service with 9 investment trust portfolios, two of which feature in his monthly column in the Investors Chronicle. The original two portfolios were started in 2009 and the others were launched from 2014 onwards.

He’s also the author of the FT’s guide to investment trusts. The publication of the second edition seems to have been continually pushed back, but Amazon reckons it should be out in a few weeks.

Baron kicked off his session highlighting last year’s report by Hendrik Bessembinder that suggested the vast majority of global stock market gains come from a tiny proportion of companies.

From the Irish Times…

The best-performing 306 companies (just 0.5 per cent of the total) accounted for almost three-quarters of the wealth created by stock markets over the last 29 years. The best-performing 811 firms – 1.33 per cent of the total – accounted for the entire amount.

I remember this report causing a stir last year although my impression is that it’s more a reflection of the very largest companies dominating market indices because of their sheer size.

It’s not that the other companies don’t do well, but they are too small to make much of an impact on the overall market.

The full report is in my further reading pile for a rainy day but seems to suggest 37% of stocks beat the market over a decade and 31% did so over the full survey period (1990-2018). That paints a rather different picture.

Baron said this report showed the need to be highly selective — he’s clearly not a fan of passive investing — but also the need to be well-diversified. I wasn’t sure quite how these two overlapped but his portfolios seem to reflect the latter.

His Growth Portfolio, for example, covers Bonds (9%), UK shares (27%), International shares (21%), Technology (15%), Renewables & Infrastructure (9%), Private Equity (3%), Commodities (3%), Biotech/Healthcare (6%), and Commercial Property (6%).

He’s moved into commodity trusts recently, highlighting their high yields and large discounts. It was the subject of his most recent Investors Chronicle column as well. His portfolios hold the two BlackRock commodity investment trusts and CQS City Natural Resources Growth & Income.

I held the CQS trust for several years, initially doing very well out of it and then suffering death by a thousand cuts. I cut it loose about three years ago and it looks like it’s lost about 10% since then, so I’m pleased I finally bit the bullet and sold out.

Being totally inept at market timing, I’ve decided that commodities are too hard, no doubt coloured by my experience with CQS. They seem to be either feast or famine. Gold, for example, has done very well this year. Oil rather less so.

Baron reckons commodity companies have cleaned up their act in recent years, with much better capital disciple and stronger balance sheets. He may be right, but I think I’ll fish elsewhere.

He’s still a fan of the technology sector, although he emphasised that was over the long term as the recent run-up in prices seemed excessive.

Smithson is a trust he’s been looking at since launch and may buy for some of his portfolios at some point. But he was more cautious about Hipgnosis, the music royalty specialist, wanting to see it establish more of a track record.

Lastly, Baron also reckoned there was a lot of bad news in the price of commercial property trusts, and he’s expecting them to bounce back at some point.

Pantheon International

I’ve got a soft spot for private equity but have never really looked closely at this fund.

It’s substantial, with assets of over £1.5bn and has returned a highly impressive 11.5% a year in net asset value terms over the last 30 years (the UK market has returned 7% a year).

It invests in other private equity funds rather than taking the direct investment approach which I tend to prefer. Private equity fees are eye-wateringly expensive and paying them twice in a single trust makes my toes curl.

But Pantheon may convince me otherwise. It certainly seems to have bested my holding in Princess Private Equity in recent times.

The presentation was pretty slick and seems to be available already on PIWorld.

Money Makers

The number of podcasts I follow seems to have mushroomed since the lockdown. Citywire’s Funds Fanatic, with Gavin Lumsden on trusts and Dan Grote on funds, is a must-listen for me as is Money Makers with Jonathan Davis and Winterflood’s Simon Elliott.

The live Money Makers session covered how trusts had performed in the first half of 2020, with all the UK sectors languising at the bottom of the pile.

I asked a question about why there were so few with a specific environmental/ESG focus. It seems like this may not be the case for much longer, with Davis saying he was aware of a number of companies looking to target this area.

Peter Pereira Gray / Welcome Trust

I think this was perhaps my favourite session of all and most of it consisted of a Q&A.

The Welcome Trust has a £27bn investment portfolio and it has returned an excellent 13.5% a year since 1985.

Peter Pereira Gray runs its investment team and has been with Welcome Trust for nearly 20 years.

‘Get very rich slowly’ is his mantra and it looks to ‘aggregate long-run real, growing cash flows’.

The trust is not afraid of risk, though, and has long been invested heavily in both technology and China.

For the last five years, its charitable expenditure has averaged about £1bn a year, so the need to fund instils a high level of discipline on the investment process.

Notably, £1bn is about 4% of its net assets, similar to the 4% sustainable withdrawal rate made popular by the FIRE movement.

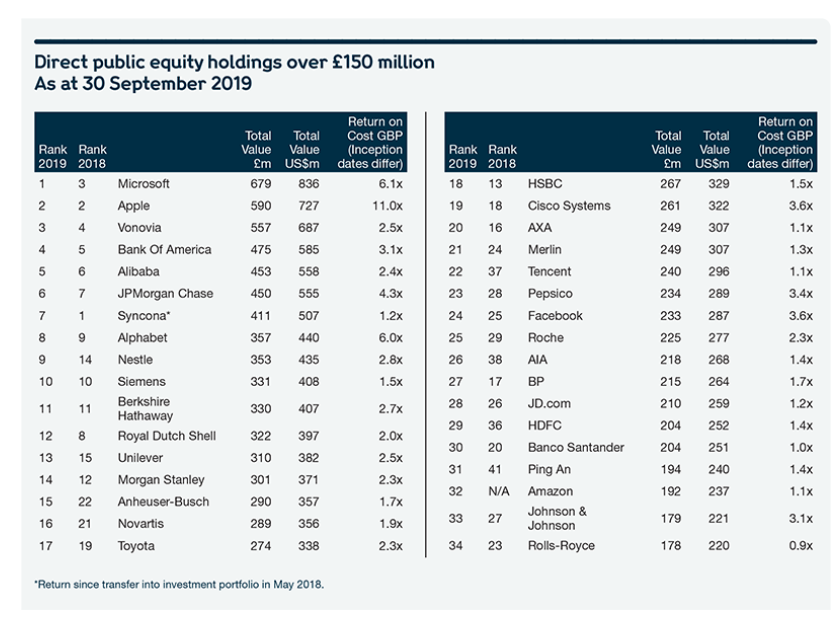

About 50% of the fund is in publicly listed companies. This is from last September but gives a good flavour of what Welcome Trust looks for:

Welcome Trust has been invested in many of these companies for a very long time and in the case of Alibaba, JD, Vonovia (a big holding in TR Property), Microsoft, Alphabet, PayPal, and Facebook, I think it has been invested well before these firms went public.

In fact, this very much reminded me of the approach that Scottish Mortgage seems to be pursuing, although Welcome Trust seems to have been doing it a lot longer.

At the end of 2019, apart from 50% in public companies, Welcome Trust held 10% in hedge funds, 28% in private equity, and 8% in property. Just 4% was in cash and bonds.

Gray likes to run his winners and he still thinks the tech sector has a big tailwind behind it. Like John Baron, he thought the recent gains might be overdone and it might take a little while for the underlying cash flows to catch up.

He said the Welcome Trust’s insight into healthcare matters meant he was alive to threat of COVID-19 much earlier than most investors. In fact, he said Welcome Trust probably traded more actively than it had done for 10 years earlier in 2020.

He’s not averse to using other investment firms for specialist areas. Although he’s ‘hugely motivated by fees’ he says some managers are worth paying up for. He focuses on net performance and looks at alignment rather than absolute fee levels.

I suspect I’ll be adding the Welcome Trust annual report to my reading list.

Mark Simpson / Excellent Investing

I remember Mark Simpson from the old Motley Fool discussion boards where he posted under the DangerSimpson moniker.

He had a great presentation on bad behavioural habits that hit home a little closer than I would have liked!

He emphasised how public statements about an investment make changing your mind about it a lot harder. That made me wonder if writing this blog could harm my returns!

The suggestion is to make more nuanced statements so you might find me sitting on the fence more in future.

Mark has written a very well-reviewed book called Excellent Investing, has started a YouTube channel, and co-hosts a twice-weekly share chat.

Summing up

There’s a lot to digest at these conferences.

I missed the Small Cap Value Report and Twin Petes live sessions and still have a few sessions from International Biotechnology Trust, Alliance Trust, Polar Capital, and Montanaro I hope to catch up on at some point.

The Mello team did a great job of pulling it together and being able to listen to some of it while doing things around the house kept me from losing too many brownie points.

Make sure you check out the Mello Events website for future events. Next up is a three-day in-person affair with trusts and funds on 30 November and (mostly) small-caps on 1 and 2 December.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Presumably, IT Investor, there is no way to access Wellcome Trust investment expertise in the way that , for instance, the wealthy families behind the Troy funds and the RIT trust sell their expertise to the private investor?

Thanks in advance.

Graham

I don’t think so, Graham. More useful for its general philosophy I’d say.

Hey IT Investor,

Interesting stuff here. I have dealings with The Wellcome through their charitable arm funding research. I’ve met some of their directors via this, who informed me of their excellent long-run (though I’ve not met anyone from their investment side). I suspect they, and other institutions, Scottish Mortgage, etc, get access to things we lowly investors just can’t.

Plenty of stuff I’m going to read further on thanks to this post.

The Shrink.

Thanks, Fire Shrink. I suspect that’s the case for most of their private equity and hedge fund investments, although I don’t think they mentioned how much this has juiced their returns over the years. The quoted portfolio is fairly mainstream stuff, though, I’d say.