Caledonia, the £2bn investment trust run by the Cayzer family, has been on a bit of a buying spree recently. Its latest purchase, a firm that runs family offices for the mega-rich, takes its collection of unquoted investments and private equity funds to nearly 60% of net assets.

I first bought Caledonia about 8 years ago. Its share price stumbled soon afterwards, no doubt in a deliberate attempt to annoy me, but it has returned nearly 140% since the end of 2012.

That’s about double the return of its main benchmark, the FTSE All-Share, so we’re back on speaking terms.

I’ve topped up my holding quite a few times over the years but trimmed it back recently as my position size seemed to be getting a little toppy.

My Caledonia concerns

Last September, I profiled Caledonia in one of my first articles for this blog. Looking back, I can see I had a few reservations, although as it was one of my earliest efforts, it wasn’t a great article!

I was lamenting the fact that the large discount seemed to be persisting, its performance had stalled a little relative to other global trusts with a heavier US weighting, and that its costs were surprisingly high.

Caledonia’s 2019

The year to 31 March 2019 was actually a pretty good one for Caledonia.

The dividend was increased by 4%, a little higher than in the last few years and notching up a 52nd consecutive annual dividend increase.

On a total-return basis, net asset value increased by 11% and the share price by 15% as the discount narrowed a little bit to 17%. That beat both of Caledonia’s benchmarks, the FTSE All-Share (6%) and RPI plus 3-6%.

Net assets crept above £2bn for the first time, so the Cayzer family’s 48.5% stake saw them enter Bloomberg’s Billionaire index.

And the Caledonia share price held up pretty well at the end of 2018, suggesting its current crop of investments could be a bit less volatile than equities as a whole.

Earlier this year, the AIC shifted Caledonia over from the Global sector to Flexible. This might help the fund’s profile a bit, now it’s grouped with the likes of RIT Capital Partners, Personal Assets, Ruffer, Capital Gearing, and Hansa, although many of these are arguably more conservatively run with substantial fixed-income positions.

The canny Cayzers

Caledonia measures its performance from 1987 when it was effectively spun out from British & Commonwealth. The latter collapsed soon afterwards when it bought Atlantic Computers which turned out to have serious accounting irregularities.

But Caledonia’s performance for its first fifteen years was decidedly lacklustre. You can see from this chart that by the early 2000s, it was trailing the UK market by a fairly wide margin.

This led to dissent from a few members of the Cayzer family who wanted the firm restructured.

Tim Ingram, the first non-family CEO, was appointed in 2002 and Caledonia was officially converted into an investment trust in 2003.

A year later in 2004, at a cost of £88m, the disgruntled part of the family was bought out via a special dividend.

Caledonia’s performance under Ingram was very good, though. He retired in 2010 and over the eight years he was in charge, Caledonia more than doubled the UK market’s return.

Will Wyatt has run things since. He is the great-great-grandson of Charles Cayzer, who founded Clan Line Steamers, the family’s original shipping business, in 1878.

Wyatt has been on the Caledonia board since 2005 and prior to that worked at Close Brothers, the merchant bank in which Caledonia held a large stake for many decades.

Cayzers in control

Two other Cayzers sit on the board, who are both cousins of Wyatt.

Jamie Cayzer-Colvin is an executive director and oversees fund investments (he’s also the non-executive Chairman of Henderson Smaller Companies) while Charles Cayzer is a non-executive and also the chairman of Cayzer Trust Co., which holds the majority of the family’s Caledonia shares.

In terms of specific shares held as part of the Cayzer family’s 48.5% total, Wyatt owns some £35m and Jamie Cayzer-Colvin around £11.5m.

Age-wise, you’d expect them to hang for a little longer, with Wyatt aged 51 and Cayzer-Colvin 54.

Caledonia’s returns at the end of Ingram’s tenure and at the start of Wyatt’s weren’t that great relative to the UK market. It lagged the recovery by a wide margin in the year to March 2010 and its discount to net assets widened significantly in 2012.

I think its long-held preference for financial stocks were a major reason for this. More recently, as I mentioned earlier, the performance has been much better. Financials are now around 16% of its portfolio and real estate 2%, which I think is lower than it was a decade ago.

Overall, since 1987, Caledonia has returned about 9% a year while the FTSE All-Share weighs in at 7.5%.

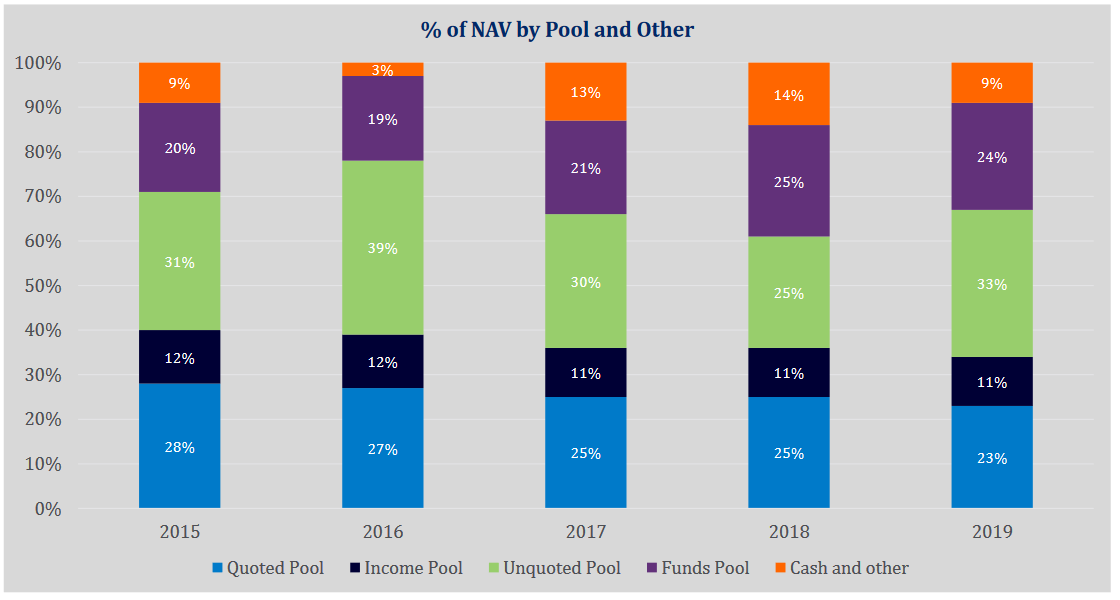

The pool strategy

Wyatt refined Caledonia’s strategy so that individual managers were responsible for distinct pools of capital. Originally there were six pools, but Asia and Property have since been folded into the remaining four:

| Pool | Range of NAV | Target return |

|---|---|---|

| Unquoted | 35-45% | 14% pa |

| Quoted | 25-40% | 10% pa |

| Funds | 15-20% | 12.5% pa |

| Income | 15-20% | 7.0% pa |

| Cash | -10% to 10% | n/a |

The ranges are only rough guidelines it would seem, as Caledonia’s actual allocation has been a little different these past few years.

Since the year-end, we’ve learned that Caledonia’s acquisition of a 37% stake in Stonehage Fleming has been approved. This will cost an initial £89m with another £21m depending on its performance over the next two years.

This shifts the asset mix, with unquoted moving up to 38% and cash down to 4%. However, the Funds pool breaks down into 20% US and Asian private equity funds and 3% in quoted funds.

This means Caledonia’s total investment in unquoted and private equity is now at 58%. I suspect that’s the highest it’s ever been.

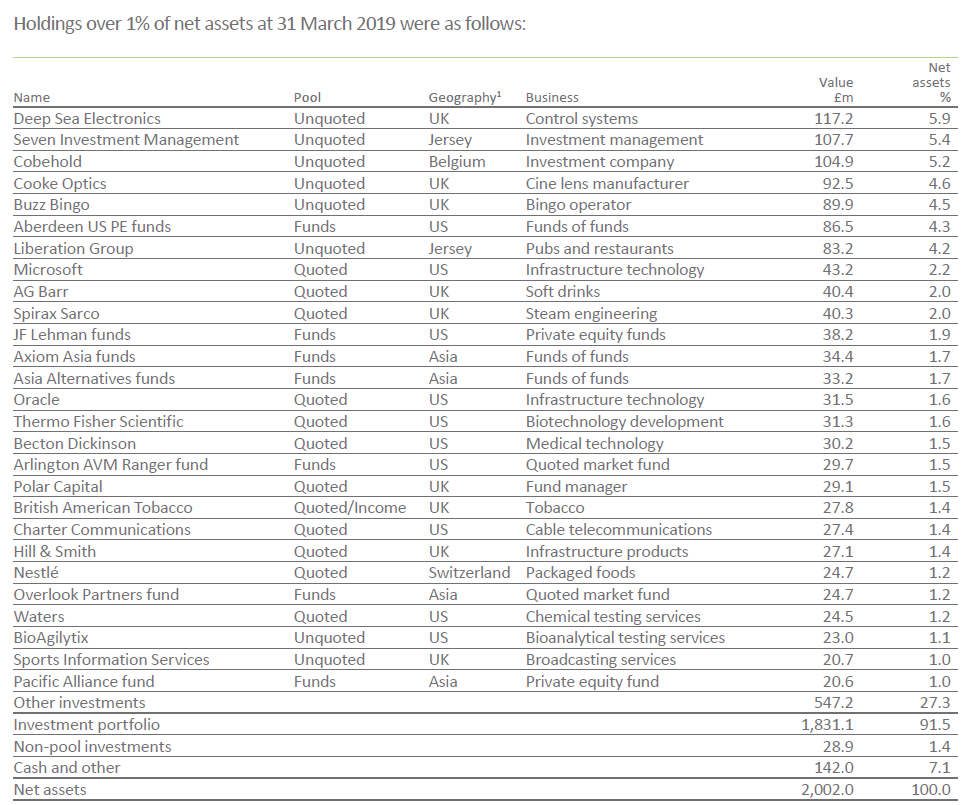

The combined portfolio

Here’s the list of Caledonia’s major investments just prior to the Stonehage Fleming purchase. Luckily, it has been selling down its stake in AG Barr, prior to the drinks group’s profit warning in mid-July.

Pool #1: Unquoted

Caledonia now has seven stakes in unquoted businesses valued at between £80m and £120m (4-6% of net assets each). In five of these, it owns around 90% or more (Cobehold and Stonehage Fleming being the exceptions).

Its newer investments, like Cooke Optics, BioAgilytix, and Deep Sea Electronics, are much more technology orientated, while recent disposals have been of more traditional businesses like care homes and caravan parks.

Old school investments that Caledonia still has — Buzz Bingo, formerly Gala, and Liberation (20 pubs in Jersey and Guernsey) — have both been written down a little.

Caledonia says it struggled to find businesses for decent prices up until recently, hence the reason the Unquoted pool dipped as low as 25% not that long ago.

It’s too early to say whether its latest purchases will turn out well, although Caledonia has highlighted the fact they will need both time and more money to realise their potential.

Pool #2: Quoted

The Quoted pool has benefitted from its large weighting (57%) towards US stocks, Microsoft being a star performer. The UK (35%) and Europe (8%) make up the balance.

Most of the major investments are Wyatt vintage, with only AG Barr (1977) and Polar Capital (2001) predating his stint as CEO.

Pool #3: Funds

This has been a great performer in recent years, but the high weighting towards private equity funds means there are commitments to future fundraisings. These totalled £330m as of March 2019 but will be phased over a number of years.

Caledonia has an unused £250m banking facility plus £80m in net cash to help fund these if needed.

The current Funds pool is weighted 55% US, 41% Asia, and 4% UK.

Pool #4: Income

The income pool is the runt of the litter right now, so I’m pretty glad it only accounts for 11% of net assets. Hopefully, it will stay below its 15-20% target range.

UK stocks dominate here, accounting for 74%, with the likes of Lloyds, Tritax Big Box REIT, GlaxoSmithKline, Imperial Brands, and Direct Line being the best-known names. The remainder is Europe (21%) and the US (5%).

Up until recently, this pool was called Income & Growth. The ‘Growth’ bit seems to have been dropped, presumably because there wasn’t any!

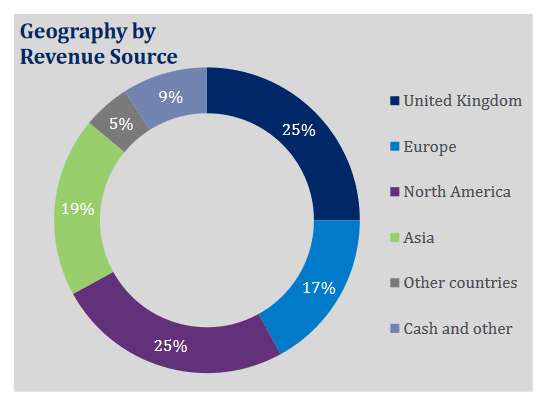

The geographic look through

Caledonia provides various geographical analyses of its holdings. Let’s use this one:

There’s very roughly an even split between the UK, the US, Europe, and Asia.

Given that, I’m not wholly convinced the FTSE All-Share remains the best benchmark to measure the company’s returns. I’ve certainly got more global in my outlook in recent years, and Caledonia has been casting its net wide for far longer.

Now that global trackers are becoming more widely available, the argument that UK investors prefer the FTSE All-Share as their key benchmark is far less valid.

Personally, I’d prefer to see a hybrid measure, maybe 25% UK and 75% Global ex-UK, and see how Caledonia fares against that.

The question of executive pay

While I know annual reports have become bloated due to corporate governance concerns in recent years, Caledonia’s latest still surprised me.

Out of 100 pages, 17 were devoted to the Directors’ Remuneration Report. That’s nearly a fifth of the entire publication!

If it takes 17 pages to explain director pay, then it’s a pretty safe bet that they are getting paid way too much. And Caledonia seems to be very generous.

Wyatt gets £540,000 in basic pay, while the new Finance Director and Jamie Cayzer-Colvin split £700,000 between them. Pension contributions add another 15% and there is a short-term bonus of 100% of basic pay plus a long-term one of 150%.

So, Wyatt can earn nearly £2m a year and the other two executives around £1.25m each. Non-execs take home nearly £400,000, so that makes nearly £5m if all targets are met.

A bonus that’s far too easy to get

Half of the short-term bonus relates to specific objectives with the remainder plus all the long-term one being performance-based.

The performance element starts off with a 10% award at a 3% annual return ratcheting up to 100% for a 10% annual return. Part of Jamie Cayzer-Colvin’s bonus is strapped to the Funds pool which has a slightly higher bonus range (6% to 13.5%).

The main range of 3-10% seems set far too low to me. In the last seven years, Wyatt has earned 90% or more of his short-term bonus and 85% or more of his long-term bonus on five occasions.

Total director pay may amount to ‘just’ 0.25% of net assets. But with stock markets returning 8-10% historically on average a year, getting a full bonus for that level seems ridiculous.

Overall charges

Caledonia’s ongoing charges figure for last year was 0.92% but leaps to 3.3% once you factor in transaction costs, underlying fund costs, and base the percentage on market cap rather than net asset value.

This grates, although it’s made easier to bear by the performance of the Fund pool.

On the plus side, at least Caledonia makes some effort to explain the difference between the two main cost measures, although it could do more do break it down into specific amounts.

Summing up

I’m coming to terms with the fact that Caledonia may always trade at a notable discount.

It seems to be narrowing very gradually, but I could see the company becoming more popular with investors once its poor run in 2011-12 drops out of the 10-year performance figures. That’s assuming its performance over the next few years remains decent of course.

With the Cayzer family holding slowly increasing over time, a significant buyback programme seems unlikely, as it would take their stake above 50%.

The Income pool remains a bit of a bugbear for me, but at the current level of 11% of net assets, I can live with it.

Likewise when it comes to the high underlying charges and executive pay.

However, my position size is still fairly large, so I suspect I may decrease a bit more over the next couple of years in favour of sector investments in renewables, and perhaps tech or biotech.

I’d like to think this will be one of the more resilient holdings come the next major market wobble. That’s becoming increasingly important to me at my stage of life, especially as I don’t believe you can time the market with major jumps in and out of shares.

That said, its track record during the wobbles of 2000-3 and 2008-9 is a little mixed. It did very well with the former but took longer to recover from the latter.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.