Not only is Scottish Mortgage currently the biggest UK-listed investment trust with a market cap of over £10 billion, but it’s also been one of the best performers over the last few decades.

Scottish Mortgage is also one of the old guard of the investment trust sector, having been launched in 1909 as Straits Mortgage and Trust Company.

Originally, it provided loans to Malaysian rubber plantations. Now its top holdings are Amazon, Tesla, Tencent, and Alibaba, so you could say its Asian roots have come full circle.

It was renamed Scottish Mortgage and Trust Company in 1913 which was then shortened to just Scottish Mortgage in 2003.

The Baillie Bunch

From launch, Scottish Mortgage has been run by Baillie Gifford, an investment partnership based in Edinburgh with offices in 10 other locations including Buenos Aires, New York, and Shanghai. Around 60% of its customers are based outside of the UK.

Although Baillie Gifford has made quite a name for itself in the world of investment trusts, it’s just a small part of its business.

As of March 2020, Baillie Gifford managed £198 billion in assets, and it had 43 partners and around 1,300 staff. Only around 15% of its business relates to retail investors, with the rest of its clients being institutions.

Baillie Gifford runs 11 investment trusts that collectively have some £18 billion in assets.

Monks is the second biggest with £2.2 billion but the rest all have assets of less than £1 billion.

Five of its trusts have Baillie Gifford in the name and it also runs Edinburgh Worldwide, Schiehallion, Scottish American, and Pacific Horizon.

Baillie Gifford is clearly very proud of its Scottish heritage. It also prizes its long-term growth-orientated approach with its website saying it thinks in terms of decades rather than quarters.

Most of Baillie Gifford’s growth has been organic, rather than acquiring other fund management businesses. It profited from the rise of defined benefit pension schemes although that market has obviously now declined somewhat.

Its growing reputation has helped it win a couple of investment trust mandates in recent years, with Schroder UK Growth becoming Baillie Gifford UK Growth in 2018 and European Investment Trust turning into Baillie Gifford European Growth at the end of 2019.

A big feature of its investing style in recent years has been buying into privately-held businesses. This is due to its belief that many of the most promising young companies are joining the stock market much later in their development cycle than they used to.

Baillie Gifford’s private investments have included the likes of Alibaba, Spotify, Airbnb, Lyft, Slack, Dropbox, and SpaceX.

Key stats for Scottish Mortgage

Figures are as of 19 May 2020 unless otherwise stated:

- Founded: 1909

- Joint managers: James Anderson (since 2000) and Tom Slater (since 2015)

- Ticker: SMT

- Benchmark: FTSE All-World

- 10-year net asset value return: 493%

- Share price: 727p

- Indicated spread: 725p – 729p (0.6%)

- Exchange market size: 3,000

- Market cap: £10.6 billion

- Premium to net assets: 4.1%

- Costs: OCF 0.4%, KID 0.8%

- Net gearing: 9% as of 30 April 2020

- Current dividend and yield: 3.25p and 0.45%

- Results released: May (finals) and November (interims)

- Sector: Global (2nd out of 16 over the last 10 years)

- Links: Website and AIC page

Here’s how Scottish Mortgage describes itself:

Scottish Mortgage is a low-cost equity fund which invests on a global basis. Stocks are carefully selected for their strong growth prospects. The trust aims to outperform world stock market indices over a five-year rolling period.

The trust has a long term investment horizon and invests with real patience. The portfolio is driven by corporate attraction rather than index construction. The managers see themselves as owners of companies rather than renters of stocks.

The resolutely global approach taken by the trust is reflected in the current investment themes such as the speed of technological advances and how they can disrupt established business practices, and the re-emergence of China as an economic superpower.

An amazing track record

You almost run out of superlatives when looking at the recent performance of Scottish Mortgage and its fellow Baillie Gifford investment trusts.

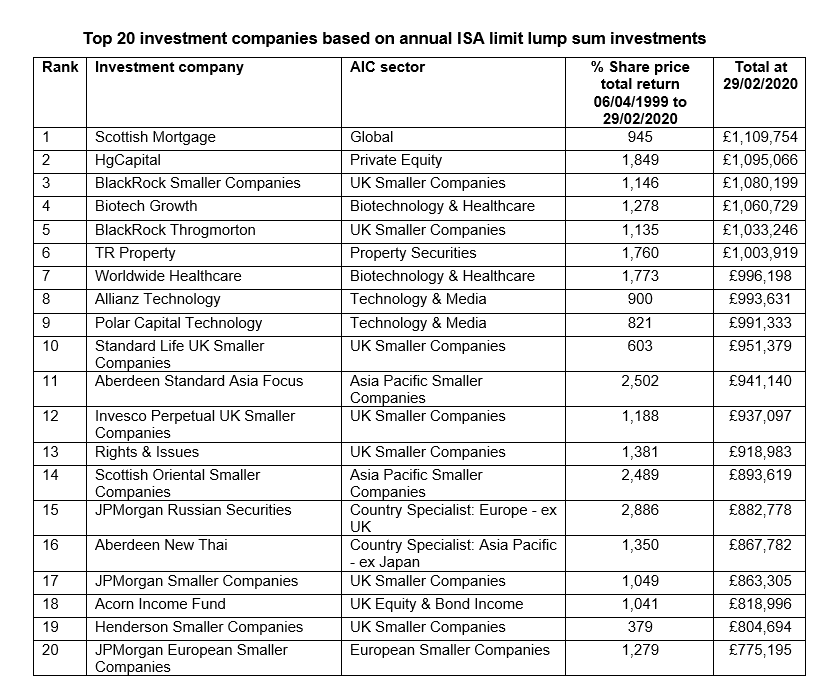

Here’s the AIC’s list of the top 20 trusts since ISAs were introduced in 1999. It shows how much you would have made if you had put a full ISA allowance into each trust at the start of each tax year:

Scottish Mortgage tops this list, albeit by a narrow margin. Despite not having the best overall percentage gain, the fact that most of its outperformance came in the 2010s propels it to the top of the pile.

However, its overall return is greater than both Polar Capital Technology and Allianz Technology, who both invest in similar companies to Scottish Mortgage.

The fact that Scottish Mortgage is the largest investment trust makes this achievement even more impressive.

It had nearly £2 billion in assets back in 1999 whereas many of the other trusts listed above were smaller and therefore much more nimble with heavily concentrated portfolios.

Although no other Baillie Gifford trust appears in this particular list, their recent collective performance has been outstanding.

The seven trusts Baillie Gifford has run for the past decade have returned an average of 113% and 315% over the last five and ten years respectively. That compares to 47% and 147% for all investment trusts.

Its ten trusts with a one-year record have returned an average of 11% with only three of those losing money over the past twelve months (two focussed on Japan and one on the UK). The average investment trust lost 3% over the same period.

Scottish Mortgage can’t currently claim the best 10-year record in the Global sector as Lindsell Train Investment Trust has done slightly better, courtesy of its hefty stake in the Lindsell Train fund management basis.

However, it’s far smaller, with a market cap of £240m, and its wildly oscillating premium to net assets can be rather unnerving.

My glaring omission

Although I am pretty happy with my overall portfolio, one glaring omission for a fan of investment trusts is the lack of anything from the Baillie Gifford stable.

I did own Pacific Horizon in the late 1990s and although it did nothing for several years after I sold, I think it’s now ten-bagged since we parted ways.

I’ve considered starting positions in both Edinburgh Worldwide and Scottish Mortgage in recent years but never taken the plunge. Like most people, my ‘I almost bought that’ portfolio is chock full of superstars!

I think the fact that I have sizeable positions in Fundsmith Equity, Lindsell Train Global and, to a lesser extent, Smithson has given me pause.

Although Baillie Gifford’s trusts have limited overlap when it comes to individual holdings, the prices of these funds do seem to be fairly closely correlated over longer periods and I’m a little hesitant to bet so much of the ranch on a similar investment style.

That said, since the launch of Lindsell Train Global in March 2011, Scottish Mortgage takes pole position with 492% (412% on a net asset basis), with Fundsmith on 375% and Lindsell Train at 306%.

Fundsmith and Scottish Mortgage were pretty much neck and neck at the end of 2019, but the latter’s stellar rise so far in 2020 has opened up a sizeable gap. It’s a good reminder of how quickly such performance stats can change.

Scottish Mortgage through the years

There is a book which covers the first 100 years of Baillie Gifford which might interest any Scottish Mortgage superfans. The earliest set of accounts I could find, however, is from 1986.

Back then, as with many trusts, its headline strategy was somewhat vague. It aimed “to achieve maximum growth in both capital values and dividends”, “investing internationally”, and “mainly in strong businesses with good prospects for growth”.

According to the AIC, it was the best performing large non-specialist investment trust of the previous five years. It had assets of £500 million even then.

In 1986, Baillie Gifford as a whole only managed £1.3 billion and had 50 staff, so Scottish Mortgage represented almost 40% of its business rather than the 5% it does today.

Back then, Scottish Mortgage’s portfolio was split 40% UK, 23% US, 21% Japan, and 16% Europe and it consisted of 120 holdings.

The management charge came to a chunky 1.4%, based on 0.12% of assets plus 5% of that year’s income. And the management agreement had a five-year notice period!

The notice period came down to three years and then one year during the 1990s and the income element disappeared in 1999. The management charge became 0.32% of net assets, much the same level it is today.

Max Ward, who now runs Independent Investment Trust, ran Scottish Mortgage from April 1987 to March 2000. Net assets grew from £567 million to £1,928 million under his stewardship and the trust returned an average of 15.2% a year from 1990 to 2000.

That sounds excellent but this was a time of very high equity returns and the trust’s benchmark (50% FTSE All-Share and 50% FTSE World ex-UK) wasn’t far behind at 14.4% a year.

New brooms take charge

James Anderson, the current joint manager, took over in April 2000. He turns 61 this year, has been with Baillie Gifford since 1983 and was made a partner in 1987. He chaired Baillie Gifford’s International Growth Portfolio Group from its inception in 2003 until July 2019.

Tom Slater, the other joint manager, has been with Baillie Gifford since leaving university in 2000, so is probably in his early 40s. He worked as Deputy Manager for Scottish Mortgage from 2010 to 2015, before being made joint manager, and has been a Baillie Gifford partner since 2012.

The Scottish Mortgage of 2000, when Anderson took the reins, looked quite different from today.

43% of its assets were invested in UK-listed companies with just 15% in the US. Its largest positions were Vodafone AirTouch (6.7%), BP Amoco (2.6%), Nokia (2.4%), Glaxo Wellcome (2.0%), and Shell T&T (1.9%).

Lloyds, RBOS, and HSBC were also large positions. The portfolio also included SAP, Microsoft, Intel, and Sun Microsystems, but there was much more telecom than tech.

The dotcom bust took its toll and net asset value per share fell by just over half from 549p to 268p over the next three years.

But a change was already underway. The number of holdings fell from 163 in 2000 to 101 by 2005. This was also the year that the top 30 positions accounted for more than half the portfolio for the first time.

The number of companies fell further still to 75 by 2007 and it has remained at roughly this level since.

The percentage invested in the UK was down to 25% and the trust’s benchmark was switched from 50% UK / 50% ex-UK to 100% FTSE All-World.

We’ve been expecting you, Mr Bezos

2007 was also the year an internet-based retailer called Amazon first appeared in the list of top 30 holdings, representing 1.3% of the trust’s assets. eBay was the second-largest position and SAP was in the top 30, too.

However, Scottish Mortgage was also riding the commodity wave of the time with Vale (iron ore), Gazprom, and Petrobas among its top positions.

The financial crisis of 2008/09 savaged the trust’s returns, as you might expect. The year to March 2009, ironically Scottish Mortgage’s centenary year, saw its net asset value per share drop by 41%.

Anderson said in that year’s annual report that, “the crisis of 2008-09 will come to be seen as the defining event in the decline of the West and rise of China”. And he’s since backed up that view by taking significant positions in a number of well-known Chinese companies.

As of March 2009, UK equities accounted for just 11% of the portfolio with Amazon the second-largest holding (4.5%) and Google the sixth (3.2%).

Although technology stocks still only accounted for around 10% of Scottish Mortgage’s portfolio, this figure had doubled by 2011 with Baidu and Tencent becoming large positions.

Resource shares and other old economy stocks started to feature less and less in the list of top holdings.

Illumina and Intuitive Surgical were added to the portfolio soon after. Alibaba and Facebook appeared in the top 30 in 2013, followed by Tesla in 2014.

Never sell your winners

I was a little surprised at just how long Amazon has been a top holding for Scottish Mortgage. I think it’s consistently been in the top two or three since 2009 and its position size has been in the range of 7-10% since 2011.

Based on Amazon’s share price of $180 in March 2011, Scottish Mortgage’s stake of £167 million consisted of 1.5 million shares.

Had Scottish Mortgage kept them all of these shares, at a price of $1,950 in March 2020, its Amazon stake would have been worth £2.4 billion, rather than the £850 million shown in its latest accounts.

So it appears that Scottish Mortgage has sold two-thirds of its Amazon position over the last decade.

Amazon’s share price has since risen to $2,450, In theory at least, Scottish Mortgage’s stake could have been worth £3 billion!

Tesla tantrums

Tesla, led by the colourful Elon Musk, very much seems to divide investors and seems to put a few people off investing in Scottish Mortgage, too.

Tesla has been in Scottish Mortgage’s top ten holdings for a while now and it became its second-largest holding in 2017.

Although Tesla’s share price slipped back in 2019 on funding concerns, it had regained the second slot by March 2020 with an 8.6% position size.

By the end of April 2020, though, it had leapfrogged Amazon to become Scottish Mortgage’s largest position at 11.3% of net assets. While Amazon’s share price rose 27% in April, Tesla was up 49%!

At a market cap of $150 billion, I think it’s now valued more than any single company in the FTSE 100, which is quite incredible.

I’m very much a fence-sitter when it comes to Tesla and Musk, as I can see both sides of the story. I suspect Scottish Mortgage might start selling down its position a little, as it has done in the past with Amazon, should Tesla’s share price climb much further.

The rest of the portfolio

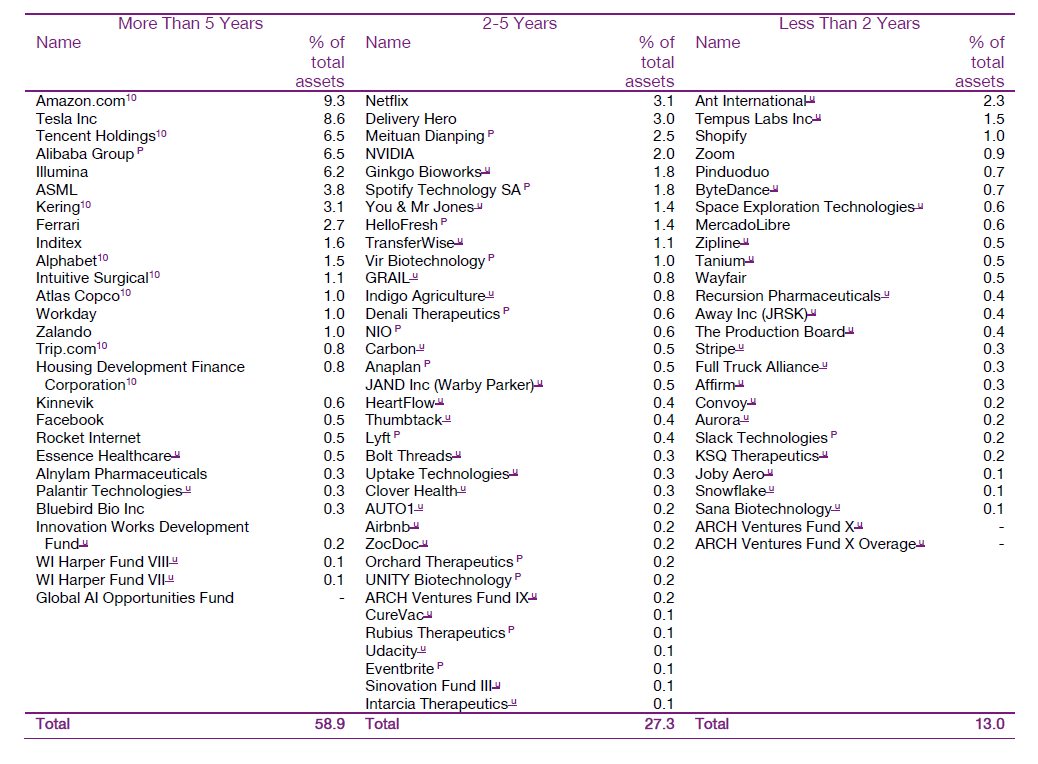

Here’s Scottish Mortgage’s portfolio as of March 2020, split by how long each position has been held:

The annual report for 2020 had yet to be published when I wrote this, but the September 2019 interim report shows 55% of the portfolio in the US, 22% in Europe, 20% in China, and just 3% in the UK.

There were 89 separate holdings, with the top 30 accounting for 80% of net assets.

45 holdings were unlisted companies although they only accounted for 20% of net assets. Only five unlisted business accounted for more than 1% of net assets with Ant Financial the largest at 2.3%.

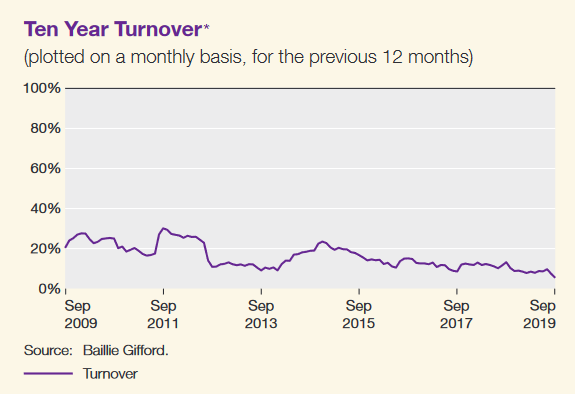

Overall, portfolio turnover seems to be very low, which I prefer to see. The April 2020 factsheet says it was just 8% over the past 12 months and the following chart shows portfolio turnover has fallen quite considerably the past few years.

In the year ended March 2020, outright sales included Baidu (once its largest position), Funding Circle, Grubhub, Home24, Renishaw, SurveyMonkey, and Tableau Software.

The unlisted question

Scottish Mortgage is proposing to lift its self-imposed limit on unlisted positions from 25% to 30%.

A fair amount of its latest results statement was dedicated to the reasoning behind this move.

For example, this chart shows how the proportion of unlisted investments has increased in recent years. The blue line is the percentage in unlisted companies while the yellow one is unlisted plus those that were unlisted when Scottish Mortgage first invested but are now public companies:

Alibaba was Scottish Mortgage’s first unlisted investment in 2012 and I think it’s also been its most successful to date. Alibaba floated in 2014 and now accounts for 6% of net assets.

Other unlisted investments that floated, and so make up the difference between the blue and yellow lines in the chart above, include Spotify, Meituan, Anaplan, Vir, and Slack.

As a holder of a few private equity investment trusts, unlisted positions don’t tend to trouble me too much. They’ve clearly added to Scottish Mortgage’s returns in recent years and I’d expect them to creep up to around 25% in the next few years, with the remaining 5% left to provide some flexibility.

They are increasing the overall risk level of the portfolio a little, given they are much harder to sell than quoted companies. But Baillie Gifford seems to be taking a measured approach and they are following a similar strategy with other trusts like Edinburgh Worldwide, US Growth, and Schiehallion.

Charges, gearing, and discounts

Scottish Mortgage’s charges are among the lowest of all investment trusts. Its annual management fee is 0.3% on the first £4 billion of total assets less current liabilities and 0.25% thereafter.

Given Scottish Mortgage’s huge size that still equates to £24 million a year in fees.

The main difference between the ongoing charge figure and the cost figure in the Key Information Document relates to 0.4% for borrowing costs.

Gearing is currently around 10% of net assets and I think it’s been at roughly that level since 2017. In the ten years prior to that, it seemed to average around 15%.

For pretty much all of the 2000s and up until 2014, Scottish Mortgage traded at a discount of between 10 and 15%. It moved to a small premium in 2014/5, as folks began to take heed of its strong outperformance, and it’s remained at a premium of a few per cent pretty much ever since.

Since September 2014, shares have been issued to ensure the trust’s premium doesn’t get too racy. It looks like the share count has increased some 20% over the past five years as a result.

Skin in the game

As of March 2019, the last annual report currently available, the five directors owned around £2 million of shares, although two-thirds of those were held by just one of them (Justin Dowley).

Three of the five own in excess of £100,000 with Chairman Fiona McBain the smallest shareholder with around 6,000 shares. McBain has been a director since 2009 and Chairman since 2017.

For some reason, it had completely passed me by that the excellent Professor John Kay has been a director of this trust since 2008. He is retiring from the Board at the AGM in June and is due to be replaced by Professor Amar Bhidé from Tufts University, who specialises in “economic innovation and entrepreneurship”.

However, one thing I did find disappointing from reviewing the accounts was the lack of any information regarding the number of shares held by Anderson, Slater, or Baillie Gifford staff.

A ‘modest’ dividend

Although Scottish Mortgage ranks as one of the AIC’s Dividend Heroes, with 38 consecutive years of increases, its yield is a mere 0.5%. It describes its distribution policy as “modest but progressive”.

Half of its 2020 dividend of 3.25p per share had to be taken from capital rather than income, reflecting the low-yielding nature of its underlying investments.

For what it’s worth, the dividend has increased at an average rate of some 6% a year over the last two decades.

Summing up

Scottish Mortgage’s website and annual reports are well worth a read to get a fuller flavour of its investing style. Despite this being one of my longest articles to date, I feel like I’ve only really scratched the surface here.

Tom Slater seems to be interviewed fairly regularly, such as on Citywire’s new Fund Fanatic podcast and twice so far this year at Brewin Dolphin. And the AIC published this internal interview earlier this week.

Given his higher profile, I would expect Slater to take over from Anderson sometime in the next few years.

It was recently announced that Anderson was stepping back from Baillie Gifford’s Long Term Global Growth team to “focus on research, the task he enjoys the most”. However, it was confirmed that he will continue to co-manage Scottish Mortgage and its International Concentrated Growth Strategy and solely manage the Vanguard International Growth fund.

When Anderson does depart, I’d expect Scottish Mortgage to take such a change in its stride, given the infrastructure and support provided by the wider Baillie Gifford operation.

Under Anderson’s watch, from March 2000 to March 2020, Scottish Mortgage returned 11% a year.

While that’s actually less than Max Ward achieved in the 1990s, it splits down into 4.3% a year for his first ten years (with those two major bear markets) and 18.2% a year for his second decade.

The trust’s benchmark returned 3% a year in the 2000s and 8.6% in the 2010s, so Scottish Mortgage maintained a slender lead during Anderson’s first decade before racing ahead in the second.

And such has been the strength of Scottish Mortgage’s performance over the last seven weeks, its overall average has been dragged up to 12.3% a year.

Scottish Mortgage looks to be in a great overall position, even after its strong gains so far this year. But I would expect a decade of lower returns (and less strong outperformance) over the next decade compared to the 2010s.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Thanks for the extensive review. Great content.

Nice write-up as ever IT.

I have held this trust in my portfolio for a few years and made a tidy return on my initial investment. However, last year I noted it had added Musk’s SpaceX to its holdings and therefore decided it was no longer for me.

I guess we all have a line somewhere in the sand that cannot be crossed!

Thanks M!

And thanks DIY! SpaceX seems to be just 0.6% of the portfolio so it’s a pretty small constituent. But I would agree that we all have to decide where our own particular lines should go!

Thanks a great review. I have been a lucky shareholder for a number of years and plan to continue.

Great article and a well run fund, its just a little late in the cycle for my tastes.

Would love to hear of people’s idea of the next Scottish mortgage trust for the next decade coming from ?

@Frozzer “just a little late in the cycle for my tastes”

Yes, there’s certainly a chance that tech stocks could have a softer period after such a great run. I didn’t touch on that particularly in the article as I thought I’d waffled on enough already!

Kepler did a note this week looking at this very thing…

https://www.trustintelligence.co.uk/investor/articles/riding-for-a-fall-retail-may-2020#