Gresham House Energy Storage is one of three renewable/infrastructure trusts that I hold. It’s the young pup of the trio, having listed late last year. Its progress has been a little bit slow to date, but it seems to be moving in the right direction.

I first covered this trust in an article last year, just after it floated, but didn’t take a position until this April.

Encouraged by what I have seen so far, and from attending the presentation given at the Mello event in May, I’ve since topped up, although it’s still a pretty small position.

This trust recently released its first set of results, so it’s time to check how things have progressed.

What it does

Gresham House Energy Storage Fund is one of only two London-listed trusts, Gore Street Energy Storage being the other, that are focused on using lithium-ion batteries to store surplus energy produced by renewable sources such as solar and wind power.

It’s not the most glamorous of activities, as the picture at the top of this article demonstrates. The batteries are housed in standard containers and tucked away on brownfield sites or industrial estates.

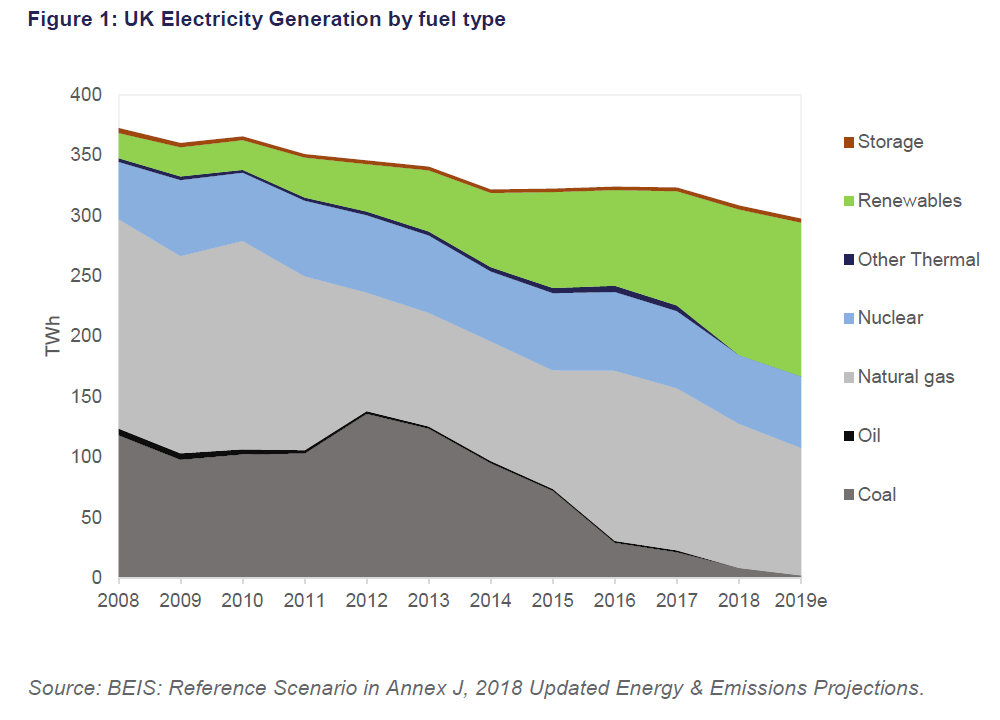

Renewable sources are providing a much greater proportion of the UK’s energy generation:

Of course, the energy generated from these sources is weather dependent. Solar is relatively steady and predictable but wind is much less so.

This means there is a need for storage systems to capture energy as and when it is produced so it can be used later when there is more demand.

Key stats for Gresham House Energy Storage

- Listed: November 2018 at 100p

- Manager: Ben Guest/Gresham House

- Ticker: GRID

- Benchmark: None mentioned

- Return target at IPO: Up to 15% a year, if geared up to 50%

- Recent price: 104.5p

- Indicated spread: 104p-105p (1.0%)

- Exchange market size: 1,000

- Market cap: £171m

- Premium to net assets: 3.8%

- Costs: OCF not yet published, 1.35% KID

- Gearing: 0% (still investing cash from IPO and placings)

- Current dividend and yield: 4.5p (2019 target) and 4.3%, 7p target for 2020

- Results released: Apr (finals) and Aug (interims)

- Dividends paid: Mar, Jun, Sep, Dec (only paid 2 since its IPO)

- Style: Renewable energy infrastructure

- Links: Website and AIC page

Getting technical

I covered this in a little more depth in my original article, but energy storage systems can make money in four ways:

FIRM FREQUENCY RESPONSE (FFR)

The firm provision to the National Grid of a dynamic (i.e. proportionate) response based on changes in the UK grid’s electrical frequency, by either rapidly importing or exporting power to help maintain a steady 50Hz frequency. This is related to the blackout on 9 August, when the frequency fell below 49Hz.

ASSET OPTIMISATION

Projects are ‘optimised’ to maximise income from the wholesale market and the balancing mechanism, through which National Grid balances supply and demand within each half hour, i.e. buying power at times of excess supply and selling power during periods of high demand.

CAPACITY MARKET

Introduced as part of the UK Government’s Electricity Market Reform in 2014. It pays generators a fixed fee for every hour they are available to deliver power when called to do so. This was suspended in November 2018, a few days after the IPO, following an EU court ruling and is yet to reopen.

GRID PAYMENTS AT TIMES OF PEAK DEMAND

“Triads” are paid by National Grid to generators during the three half hours of highest annual demand. Payments are decreasing through 2021 as regulations change, however, several locations will continue to earn attractive income from Triads. Other grid payments can also be earned for generating during daily peaks. Amounts are specific to each project.

FFR has reportedly been the main revenue earner for Gresham House Energy Storage to date, but it’s Asset Optimisation that is expected to be the major money-spinner (70%+ of revenues) in future years.

While the idea is that energy can be bought cheaply when generation is high and then sold at a higher price when there is peak demand, it looks like the timing of that buying and selling will be set by external parties. From the latest results:

The Manager has gone through an extensive process to select the best asset optimisation firms in the market. Their aim is to identify a number of potential partners. We have identified the strengths a trading counterparty needs; from balance sheet strength to the intelligence of their trading algorithms to a very deep knowledge of their industry.

An initial set of counterparties has been identified and the strongest performers will be given the opportunity to grow with us. The entities contracted so far are mostly very well known in the electricity marketplace although credible new entrants are also being considered for future capacity.

This ups the risk a little further. It’s essentially a brand new and untested business model that the company is proposing.

Noriker Power, which I believe has helped Gresham House Energy Storage design and build all its facilities to date, is another key third party to be aware of. The trust has just bought 5% of its shares for £0.4m to help “consolidate their strategic alliance”.

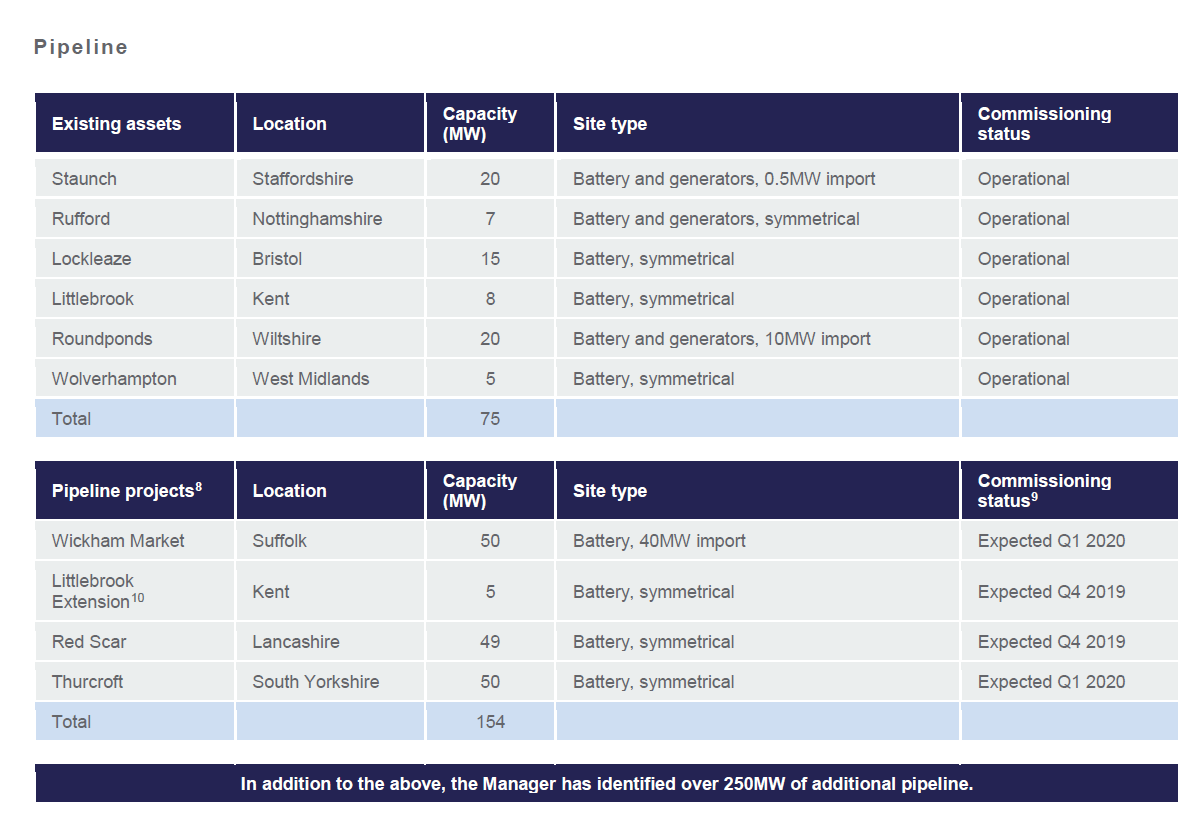

The portfolio

Gresham Energy Storage Fund has six facilities at the moment with plans to extend one and add a further three in the near future:

One thing I didn’t appreciate last year was the advantage of having symmetrical systems where energy can be exported and imported at the same rate. This appears to be needed for Asset Optimisation and should eliminate the need for engines and other technologies on these sites.

The Roundponds facility is to be made symmetrical, although no target date is mentioned. The Staunch facility is the oldest, commissioned in early 2017, but there don’t appear to be any immediate plans to make this symmetrical.

Among the pipeline assets, Wickham Market is the only non-symmetrical facility, but no explanation is given as to why this is the case.

The three new facilities are more than twice the size of anything in the existing portfolio, so they represent a major step up in scale. They should be more cost-efficient although it’s interesting to note that one of its existing sites is being expanded. It’s not clear how feasible this would be across the rest of the portfolio.

Overall, capacity is expected to triple to 229MW over the next six months or so, which Gresham House reckons will make it the UK’s largest battery portfolio.

Operationally, there doesn’t appear to have been any major issues so far. However, I couldn’t see any specific KPIs mentioned in these results so it’s not clear how management is monitoring performance. I would have expected some downtime measures, for example.

They do seem to be keeping themselves busy, though, with projects such as replacing diesel engines with gas at Staunch and upgrading batteries at many sites so that they discharge over a longer period of up to 1.5 hours.

Lease extensions have also been gained at three sites, which is something I like to see and that Bluefield Solar (one of my other holdings) has also been keen on. I assume these lease extensions account for most of the 1.91p uplift in Project NPV shown below:

I did find this chart a little puzzling.

Interest income looked high to me, although I subsequently saw that interest on facility construction loans is being received at an interest rate of 8%. And I wasn’t sure why TRIAD merited a separate mention but there was nothing for FFR.

The cost of new facilities

The first 70MW of capacity the trust bought cost £57.2m and the 5MW at Wolverhampton another £3.5m. So the average acquisition cost has so far been £0.81m per MW.

The immediate pipeline of 154MW could, therefore, cost around £125m, or hopefully a little less if economies of scale are beginning to kick in.

Gresham House Energy Storage had net cash of £63m as of 30 June 2019 with a further £15m raised in a placing in July. Further fundraisings seem pretty much nailed on, although some £19m has been lent by the trust to help build some new facilities. I would assume this reduces the net cash outlay at the point of purchase.

Gresham House Energy Storage has raised £50m at 101p and £15m at 105p, representing small discounts to the share price each time.

In fact, apart from a brief spurt to 109p just before the second placing, it’s remarkable how steady the share price has been in its first year. It’s spent most of the time in a narrow band from 102p to 105p.

Slower progress than expected

It’s interesting to compare the current plans against the pre-IPO pipeline.

Wolverhampton, acquired just a few weeks ago, was initially expected to join the portfolio in the last quarter of 2018.

Red Scar, which sounds like a Marvel villain to me, and Thurcroft were originally pencilled in for the second quarter of 2019.

And a 28MW non-symmetrical facility in Hereford seems to vanished from the pipeline entirely. It was last mentioned in the March 2019 factsheet.

The mysterious Project “I”, an 80MW facility to be located in Lincolnshire, was gone by the time the first factsheet was produced at the end of January 2019. It was at an earlier stage, though, with just heads of terms agreed. Wickham Market joined the pipeline at the same time.

Here’s the explanation for the various delays:

As the Fund’s mandate is to wait and acquire projects after commissioning, there has been a natural pause before acquiring further projects post-IPO, as a result of lead times in ordering equipment, engaging engineering contractors, arriving at the optimum final designs and confirming these with the planning authorities.

That seems reasonable. With the step-up in scale, I’d much rather a little extra time was taken to get things right.

Red Scar began construction in July and is expected to be commissioned in November. The other three pipeline projects should all begin construction by the end of October.

How big is the energy storage market?

A very good question.

The trust has previously referenced research from Pöyry and Imperial College London dated May 2017 that “indicated total UK storage capacity rising from approximately 2.9GW in 2020 to 20.3GW in 2030 in the central case, with a high case seeing as much as 35GW of storage capacity by 2030”.

However, it also said that “Bloomberg has identified a total of just 694MW commissioned as at 31 March 2019”, so the 2020 estimate of 2.9GW looks a little bullish, to say the least.

These latest results include an internal estimate from Gresham House that the market could grow fifteenfold to 10GW in the next five years.

It looks like Gresham House Energy Storage has a fairly chunky market share right now, although it’s not clear to me who its main competitors are. Gore Street has just 30MW, although it’s looking to expand by a further 100MW in Northern Ireland and 60MW in the Republic of Ireland.

It’s worth noting that energy storage systems aren’t the only way to deal with temporary excess capacity from renewables. The trust’s Prospectus says other “flexible generation solutions including interconnectors with other countries, Demand Side Response, gas and diesel peakers, pumped storage” could also play their part.

However, the events of 9 August seem to reinforce the need for energy storage systems. Apparently, the batteries already in use prevented the outage that day from being even worse.

Dividends

Gresham House Energy Storage expects to pay 4.5p of dividends in respect of 2019, 7.0p for 2020, and then rising steadily after that. Dividends are to be paid quarterly.

June’s payment, the first, was 1.4p and a further 1.1p is due on 20 September. I’m expecting to see 1.0p paid out in December and March to hit the 2019 target.

It looks like the payments were front-loaded a little to avoid paying out too much before the first placing of £50m. Or perhaps this represents the seasonal trend that the trust’s income has.

There is apparently “ample” cash flow to pay the 2019 target, due to the performance of the battery portfolio so far. The 2020 total is quite a bit larger, so may depend on the pipeline projects being completed on schedule.

Charges

Somewhat unusually, I couldn’t find an official ongoing cost figure (OCF) for this fund.

We do know that its basic management charge is 1% for the first £250m of assets, 0.9% for £250m-£500m and 0.8% above that level.

The Key Information Document says costs are 1.35%, and I would expect the OCF to be around this level.

The four directors currently receive £190,000 a year between them. That’s a little on the high side compared to some funds I have looked at recently, but not worringly so.

Skin in the game

The four directors win no prizes here, with just 5,000 shares each.

David Stephenson, the FT’s Adventurous Investor, is one of the directors and wrote a couple of articles about the fund for his blog when it first joined the market. He hasn’t written about it in detail since, as far as I can tell anyway, although I imagine doing so could be considered a conflict of interest.

The lead fund manager, Ben Guest, who I believe Gresham House bought the initial battery portfolio off, owns 13.5 million shares. Part of his holding appears to be held through a company called Lux Energy.

He owns around 9.0% of the total share capital right now but has been diluted since the IPO as I don’t think he bought any new shares in either of the two placings.

I’m not too worried that Guest didn’t add to what must be a fairly major position for him, although any significant sale would ring alarm bells. He’s locked in until November 2020 and is 46 years old, so you would expect him to hang around for a little while yet.

Guest’s deputies are Bozkurt Aydinoglu, who gave the Mello presentation I linked to earlier, and Gareth Owen. They both worked for several years with Guest at Hazel Capital, which Guest founded prior to joining Gresham House. They are 48 and 44 respectively.

In conclusion

It’s very early days for this investment but I’m happy with it so far. The premium it trades at is a lot lower than other renewable infrastructure trusts, but I think that’s to be expected.

I would definitely class this trust as well above average risk, given its limited track record and the newness of this type of business concept.

On the surface, it seems relatively simple: stack up some batteries, plug them into the grid, and then sit back and collect the cash. But I expect the devil is very much in the detail.

The energy market in the UK is fiendishly complicated and the fact that Gore Street Storage has struggled to convince investors and is now looking to expand in Ireland suggests this is a position I’ll need to watch more closely than most.

There’s political risk, too, as the ownership status of National Grid could change if a Labour government gets elected.

And I’d certainly like to see a lot more information on the underlying performance of its battery portfolio, especially now that it’s about to triple in size.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.