This crisis has posed many questions we’ve never faced before as investors. One of them is what to do about the prospect of a massive decrease in dividend payouts.

It’s long been accepted that the income received from shares, as far as the UK stock market goes anyway, tends to be less volatile than prices.

According to figures from the Barclays Equity Gilt study, since the early 1930s, dividends have only fallen in 15 calendar years in the UK. And only on two occasions — 1998 and 2009 — has the fall exceeded 10%.

However, Monevator recently featured the latest Dividend Monitor report from Link Asset Services. It suggests that UK payouts could fall between 27% (best case) and 51% (worst case) in 2020.

Link thinks there should be a recovery in 2021 but UK dividends might still be 10-30% below the levels they were in 2019.

We’re still in the early stages of this crisis, so these figures could change of course.

Banks, insurers, housebuilders, travel, mining, and general retail are likely to see the biggest cuts. What happens to the oil sector, i.e. BP and Shell, makes up much of the difference between the best and worst-case scenarios.

Looking further afield

I haven’t seen any similar forecasts for global dividends yet although I’ve seen mention of cuts of 25% in the US and up to 50% in Europe.

Janus Henderson does produce a global dividend report but the last one was dated February 2020, just before the crisis started to affect markets.

For what it’s worth, it forecasted a 4% increase in 2020 to $1.4 trillion. I think the next update is expected in mid-May, so that will certainly make for interesting reading!

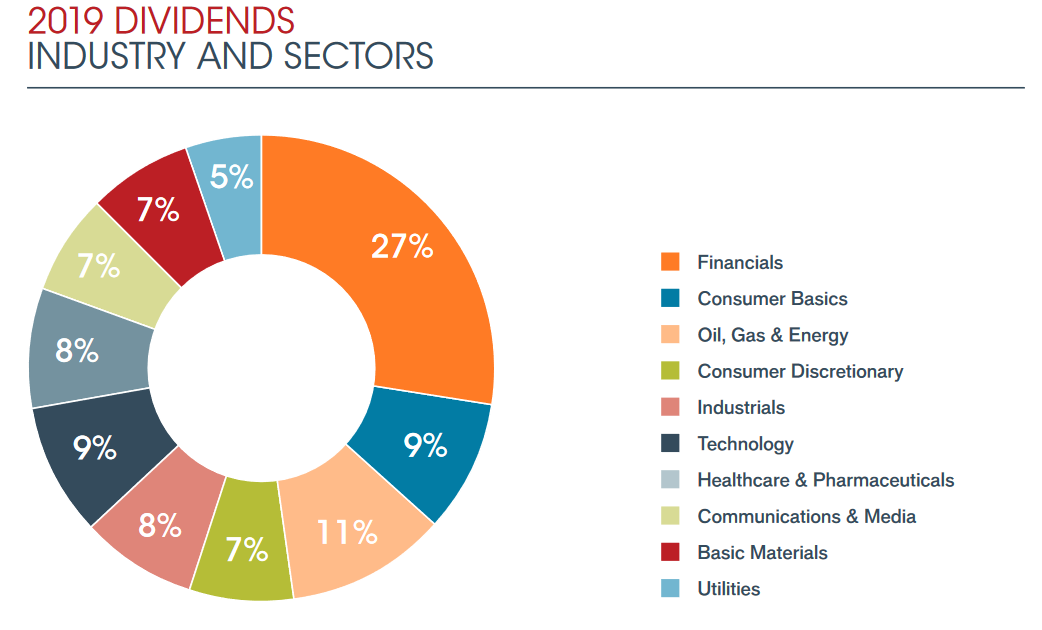

The most recent Janus Henderson report does provide some interesting nuggets. It shows how global dividends have risen by 7% a year, on average, over the last decade.

It’s not been a smooth ride, though, with payouts flat in US dollar terms for three years from 2014 to 2017, with decent growth both before and after that time.

It also highlights the high level of dividends paid by UK companies. UK-listed firms make up around 5% of the global market cap but 8% of global income.

And it has this useful split of the major dividend-paying sectors:

Given all this, a cut of 25-50% in global dividends, similar to what’s predicted in the UK, seems like a reasonable guess at this point. And 2021 dividends will probably be lower than 2019’s.

That’s arguably the easy part, though. While investment trust dividends depend on their underlying investments, they are a number of other factors to consider.

Keeping income back for rainy days

Many investors know that trusts have the ability to smooth out their dividends as they are allowed to retain up to 15% of their income each year.

These amounts get added to what is called their revenue reserve and can then be used to help fund future dividends.

However, it’s important to realise that the revenue reserve is just an accounting concept. It’s not represented by a ring-fenced pot of cash.

So while a trust can legally tap its revenue reserves to prevent it from cutting its dividend, if it doesn’t have cash set aside then it may have to sell some of its underlying investments and/or increase its level of borrowing.

You can look at a trust’s accounts to see what revenue reserves it has. And the ever-useful AIC website provides a summary on its main information page for each trust, just below the list of its most recent dividend payments.

For example, the AIC page for Murray International shows it has revenue reserves of £76m which should cover 1.1 times the most recent annual payout.

A look at its accounts shows this was the situation as of 31 December 2019. Since that time, a further dividend of £15.5m was paid in February and another £22.6m is due in May. Of course, the trust would have received more dividends from its investments.

How substantial are revenue reserves?

I scoured the AIC’s interactive stats to get an overview. It indicates just over four-fifths of investment trusts pay out a dividend.

Of those that do pay a dividend, it reckons 62% have some level of revenue reserve. That was a bit lower than I was expecting but not all trusts explicitly list out their revenue reserves in their accounts and so are effectively excluded from this number.

Some investment trusts are over a century old and therefore have had ample time to build up a hearty revenue reserve.

Others, especially those which invest in alternative assets and offer a higher income, are less than a decade old and don’t have much of a buffer.

However, it does seem that where a trust does have a revenue reserve, it’s usually pretty chunky.

55% of trusts that pay a dividend have a revenue reserve covering at least 0.5 times their most recent annual payout. So that means only 7% have a reserve between 0 and 0.5 years.

An impressive 45% have reserves of at least 1 times their latest annual dividend.

13% have at least 2 times.

If we assume dividends fall by a third this year and take two more years to get back to 2019 levels, then a trust needs about 0.5 years in revenue reserves to see it over.

A large proportion have at least 0.5 years. Indeed, we’ve seen quite a few trusts already saying that they expect to maintain or even increase their dividends this year.

A report from JPMorgan Cazenove reckons UK Equity Income trusts are pretty well placed with 1.2 years in revenue reserves but this might reduce to as little as 0.4 years after 2020’s cuts. A note from Kepler came to broadly similar conclusions.

There’s also a useful thread on the Lemonfool discussion boards highlighting the various investment companies that have made recent announcements about the sustainability of their dividends.

I reckon sectors like infrastructure and renewable energy should be ok, as their assets should still be producing much the same level of income as before.

However, I wouldn’t be surprised if a fair number of the trusts specialising in property and debt hit a rocky patch. A few of them have already held up their hands and cancelled their payouts.

UK Smaller Companies, one of my personal crushes, could be another area of difficulty. However, with a wider mix of industries and less dividend concentration among small caps than the FTSE 100, taking a high-level view is trickier. The yield on these funds tends to be pretty low anyway.

Private equity and VCTs are another hard call. I believe the level of dividends is often dependent on a steady stream of company sales rather than the underlying income produced by its investments.

Slower growth going forward?

It’s hard to argue with trusts tapping into revenue reserves to maintain their dividends. If they’re not going to use them now, when are they?

But I suspect that they’ll want to build them back up again over the next several years. This could mean we see slower dividend growth from many income-orientated trusts for quite some time.

This hopefully won’t come as a shock to anyone. Trust dividends ultimately depend on the income being paid by their underlying investments. The path can be smoothed but it still travels in the same direction.

I suspect a lot will come down to the directors of individual trusts. They can take a view on the make-up of their shareholder base and decide how to prioritise the level of dividend relative to the make-up of their portfolio and their cash/debt position.

The Dividend Heroes, those that have increased their payouts for 20 years or more, may feel a little extra pressure. However, a fair few of those with the longest records don’t offer a particularly high yield.

Paying dividends out of capital

Several years back, the rules governing investment trusts were changed so that they could pay dividends out of capital gains as well as any income received.

I don’t have a definitive list of which trusts do this but I think there are a few dozen. Many of them say they will pay out a fixed percentage of their net assets on a set date each year and it will be interesting to see if any change their plans faced with net asset value declines of 20% or even more.

We could also see some trusts with low revenue reserves decide to tap their capital accounts for the first time. I think shareholder approval is required for this but perhaps a simple vote by a trust’s directors will suffice.

17 April update – Invesco Perpetual UK Smaller Companies has ditched its 4% dividend target based on its share price as of 31 January (unfortunate timing with that cut-off date) and is looking to pay at least 2% of its 31 January 2021 share price.

Summing up

Dividends can be very divisive.

Some investors love them while others prefer to worship at the altar of total returns. The latter group is more than happy to sell shares if they need cash from their portfolios.

I’d say I’m somewhere in the middle.

About a third of my holdings yield more than 5% but roughly the same amount yield 2% or less. I think my average yield works out at 2.5%.

While I do like being able to reinvest dividends on a regular basis, I try not to reach for yield or only do it in a limited way.

Right now, it certainly looks like the average investment trust is well placed to at least maintain its dividends this year, despite all that’s been happening.

And it’s been good to see many of them have come out with specific statements to reassure their investors rather than waiting for their next formal results announcement.

Stay safe!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

https://www.retirementace.co.uk/2020/04/will-investment-trust-dividends-hold.html is worth a look too

I think investors may have slightly too much of a psychological bias towards dividends.

OK, an IT might be able to continue paying a dividend, but if that is paid from reserves, it essentially reduces the NAV of the trust and hence the valuation of the trust should drop.

Selling a few shares of an investment should produce exactly the same result.

From a tax perspective, if the assets have to be held in a taxed account, more people are likely to benefit from capital gains, rather than dividends, as the capital gains tax allowance is larger @ £12300 v just a £2000 tax free dividend allowance. Ideally, of course, if you hold assets in a taxed account, you use both allowances.

Then, for any higher rate taxpayer, the rate of tax on capital gains is lower than that for dividends. This is reversed for a basic rate taxpayer.

Thanks for this useful roundup. I may be guilty of reaching for yield. I will be pleased if my current portfolio yield of 6.10% is actually all paid out over the next year. I’m most concerned about my high yield bond trust and my commercial property trust. I think the equity income trusts should probably hold up for at least one year.