Since Zehrid Osmani took over Martin Currie Global Portfolio just over two years ago, it’s become one of the best-performing global investment trusts.

Of course, two years is a very short period to judge any investment. Although, as it includes the dip in the last quarter of 2018 and this year’s COVID-19 shakeout, you could argue we’ve packed in a whole decade of events!

The raw stats

Let’s start by looking at the trust’s recent record compared to the competition.

Martin Currie Global Portfolio is up 32% in net asset value terms since October 2018.

That compares pretty well against Lindsell Train Global (13%), Fundsmith (31%), Blue Whale Growth (39%), Mid Wynd (26%), Monks (39%), and Manchester & London (29%).

Scottish Mortgage (93%) blows them all away, as you might expect, but Martin Currie Global Portfolio is definitely in the chasing pack.

The more conservative global trusts, such as Bankers, F&C, Brunner, and Alliance are up between 5% and 13% over this same time period and the Vanguard FTSE Global All Cap tracker I use to measure global markets is up 12%.

Long-term performance

The long-term performance of Martin Currie Global Portfolio isn’t too bad either.

As it only launched in 1999, I didn’t include it in my review of 20 global trusts from a few months ago. But it returned 5.0% a year in the 2000s and 12.6% a year in the 2010s.

That puts it ahead of world markets in both decades, as they returned 2.5% and 11.6% a year respectively.

Over the last ten years, Martin Currie Global Portfolio sits third out of sixteen on a net asset value basis, behind Scottish Mortgage and Lindsell Train Investment Trust but ahead of both Mid Wynd and Monks.

In other words, however you slice and dice the data, this trust puts in a very respectable performance.

Key Stats for Martin Currie Global Portfolio

- Listed: 1999

- Manager: Zehrid Osmani (since Oct 2018, age 46)

- Management group: Martin Currie

- Ticker: MNP

- 10-year net asset return: +223%

- Benchmark: MSCI All Country World Index

- Current price: 348p (as of 26 Oct 2020)

- Indicated spread: 346p-350p (1.1%)

- Market cap: £286m

- Net asset value: 346.6p (as of 23 Oct 2020)

- Premium to net asset value: 1.3% (as of 23 Oct 2020)

- Costs: 0.6% OCF without performance fee, 1.5% OCF with performance fee, 1.1% KID

- Management fee: 0.4% of NAV plus a 12.5% performance fee

- Net cash: 0.4% (as of 30 Sep 2020)

- Number of holdings: 30

- Current dividend and yield: 4.6p and 1.3%

- Results released: Mar (finals) and Sep (interims)

- Dividends paid: Jan, Apr, Jul, Oct

- Continuation vote: None, trust life is indefinite and it has a zero discount policy

- Sector: Global (3rd out of 16 over 10 years)

- Links: Website — AIC page — Edison reports — Kepler reports

History

Edinburgh-based Martin Currie, the trust’s management firm, has been around since 1881. It was originally an accountancy partnership but started to manage client portfolios in the 1920s.

However, after an expansion push, Martin Currie ran into problems in 2012. It was fined by regulators and posted the first loss in its then 130-year history.

It ended up being bought by the much-larger US firm Legg Mason in 2014, which was in turn bought by the even-larger Franklin Templeton in 2020.

Despite the double change of ownership, Martin Currie has been maintained as a separate brand. It runs around £11bn of assets, so it’s a tiny part of Franklin Templeton which has $1.4 trillion under management.

Martin Currie used to have a much bigger presence among UK-listed investment trusts. The trust’s 2005 accounts list nine other investment companies that Martin Currie managed at the time.

As we move towards the tail end of 2020, Martin Currie Global Portfolio is the sole survivor.

Martin Currie Asia Unconstrained was rolled into an open-ended fund in 2019 and the investment mandate to run Securities Trust Of Scotland was lost to Troy Asset Management (Personal Assets, Troy Income & Growth, and Trojan Fund) a few months ago.

How the trust has changed

Martin Currie Global Portfolio was created after the reconstruction of Scottish Eastern Investment Trust in 1999. Scottish Eastern had long-been Martin Currie’s flagship trust and dated back to 1924.

Like many of today’s global investment trusts, Martin Currie Global Portfolio has evolved over the last two decades after initially being mostly focused on UK shares.

In 2007, the maximum proportion of the portfolio in international stocks was raised from 25% to 50%. But the trust continued to benchmark itself against the FTSE All-Share index.

In 2011, a global mandate was adopted, the unquoted part of the portfolio was sold off, and the benchmark was changed to the FTSE World Index. The trust’s name was tweaked from Martin Currie Portfolio to Martin Currie Global Portfolio to help emphasise the new focus.

In February 2020, the benchmark became the MSCI All Country World Index as the trust’s directors reckoned this index better reflected the larger emerging markets, such as China and India.

Tom Walker was the manager of the trust from 2000 up until his retirement from Martin Currie in 2018.

Zehrid Osmani was recruited from BlackRock as Walker’s replacement, initially becoming co-manager for a few months before fully taking charge in October 2018. He is head of the Global Long-Term Unconstrained team at Martin Currie, running other funds and mandates using a similar investment approach.

Even before Osmani took over, the trust’s portfolio had started to become more concentrated. In 2016, it contained 60 companies but this had reduced to 47 by the time Walker departed.

As of 30 September 2020, the number of holdings had shrunk to 30.

Investment strategy

The trust’s objective is simply to achieve “long-term capital growth in excess of the total return from the MSCI All Country World index”.

It outlines its policy as:

- investing in predominantly blue-chip equities with a market capitalisation in excess of $3 billion;

- investing predominantly in quality growth companies with superior share price appreciation potential based on attractive ROIC (return on invested capital), balance sheet strength and ESG credentials; and

- a high conviction portfolio typically with 25-40 stocks, with a view to holding stocks over a long time horizon.

The recent Edison report sheds a little more light on its investment process. It says companies are screened down to “a research pipeline of 90+ names … with a combination of quality, sustainable growth and an attractive valuation”.

A systematic risk assessment is made across industry and company-specific factors, plus environmental, social, and governance (ESG). Favoured companies are likely to have “a dominant position and pricing power in a market with high barriers to entry and low disruption risk”.

On a portfolio level, geographic revenues and profits are analysed rather than focusing on the country where the share is listed. End users are also looked at, focusing on the split between consumers, businesses, and governments as well as by sectors and industries.

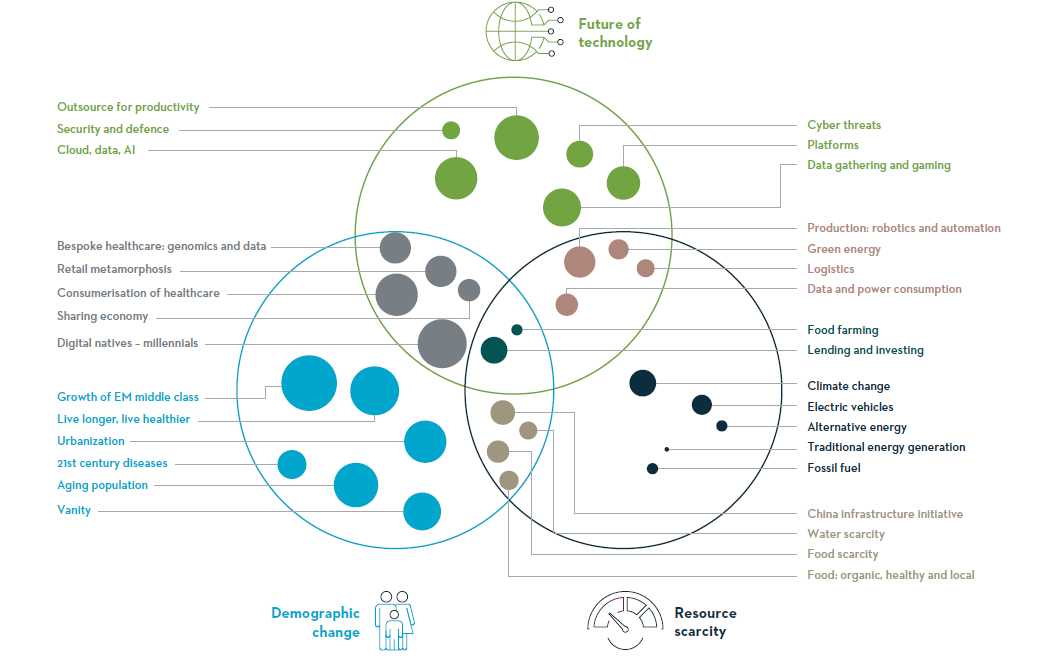

Similar to Mid Wynd, there is a thematic overlay to the portfolio as well. There are three high-level areas:

- the future of technology;

- demographic change; and

- resource scarcity.

Themes within these areas include cybersecurity, robotics/automation, telemedicine and home care, infrastructure spending, and electric vehicles.

Here’s a fancy infographic from the trust’s accounts showing how these themes fit together:

I’m not sure if the dot sizes represent the perceived opportunity, portfolio exposure, or something else entirely.

Watching the many videos Osmani has appeared in recently, on the AIC channel in particular, certainly gives the impression that he and his team are both meticulous and highly detailed in their approach.

There’s probably a bit more focus on macro-economic events than I personally like to see, such as a recent video presentation on the US election. But it’s still thoughtful stuff and more concerned with mild course correction than wholesale portfolio changes.

Portfolio

The full portfolio only seems to be published in the trust’s annual accounts so the last complete list is as of 31 January 2020.

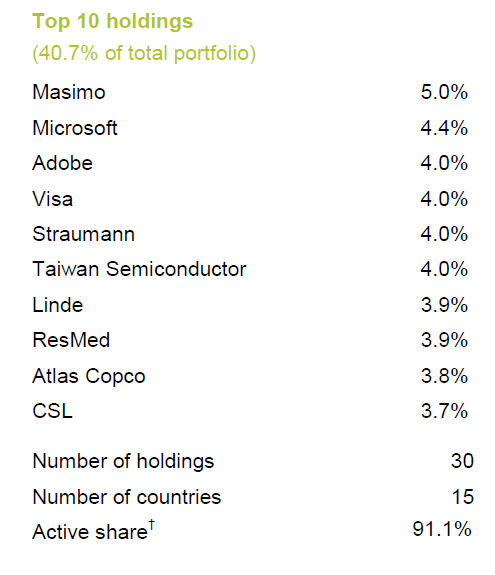

Here’s the latest top ten, as of the end of September:

It’s one of the most evenly distributed portfolios I’ve come across in terms of position size.

As of 31 January 2020, the smallest holding accounted for 1.7%. Half the position sizes were between 1.7% and 3.0% and the other half were between 3.0% and 5.0%.

So every position matters but there are no very large position sizes that you tend to find with other global trusts that follow a similarily concentrated approach. Most of these seem to have a number of positions clustered around the 10% level.

Osmani radically changed the portfolio when he took over. Of the 47 companies held in early 2018, only five (VISA, Atlas Copco, AIA, Taiwan Semiconductor, and Alibaba) still appear to be owned today.

The likes of Apple and Facebook have been replaced by Microsoft and Adobe. Various holdings in tobacco, oil & gas, plus large financial institutions like JPMorgan Chase and AIG have also been jettisoned.

A recent blog post from Osmani outlined his reasons for generally steering clear of the FAANG stocks of Facebook, Apple, Amazon, Netflix and Google (Alphabet). Essentially it boils down to competitive and regulatory concerns. There’s more on this topic in this interactive investor podcast from a few months ago.

Outside the current top ten are several well-known names such as Adidas, Ferrari, Starbucks, L’Oreal, Accenture, and Tencent.

Recent additions to the portfolio are Veeva, Illumina and Ansys, while Unilever, Spirax-Sarco, Align, Waters, Beazley, and ADP have been sold.

Portfolio turnover using my crude measure of investments sold divided by average market value of the portfolio was 80% in the year ended January 2019 and 36% in the year ended January 2020.

The first of these two years included the manager change from Walker to Osmani, so that’s why it was substantially higher.

About 15% of the portfolio was sold in the six months ended July 2020, so that suggests portfolio turnover could be settling around 30-40% a year.

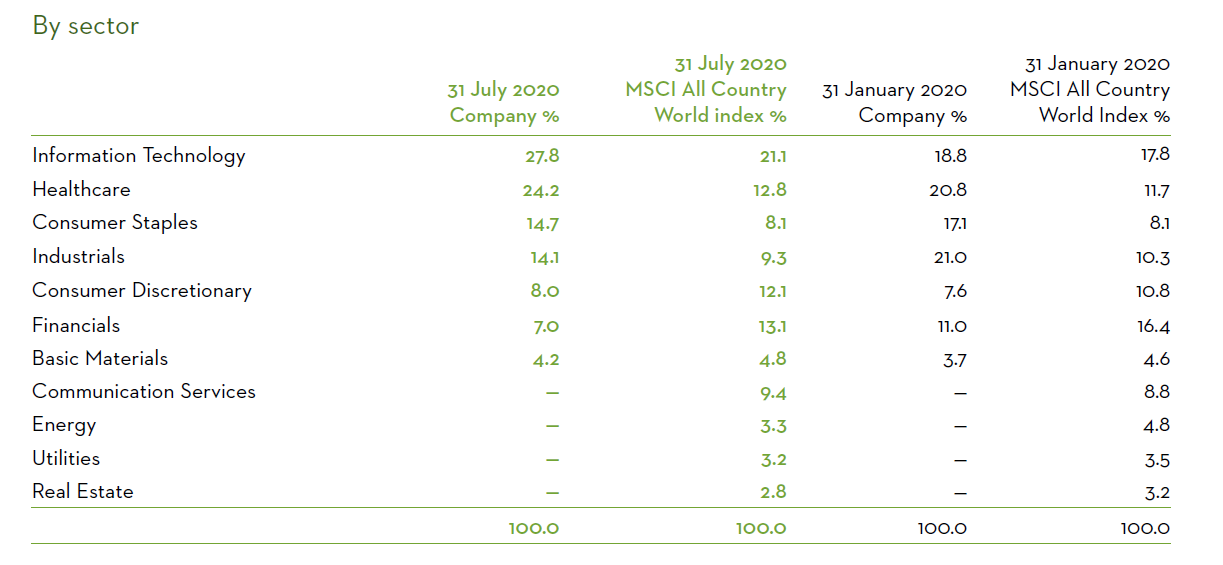

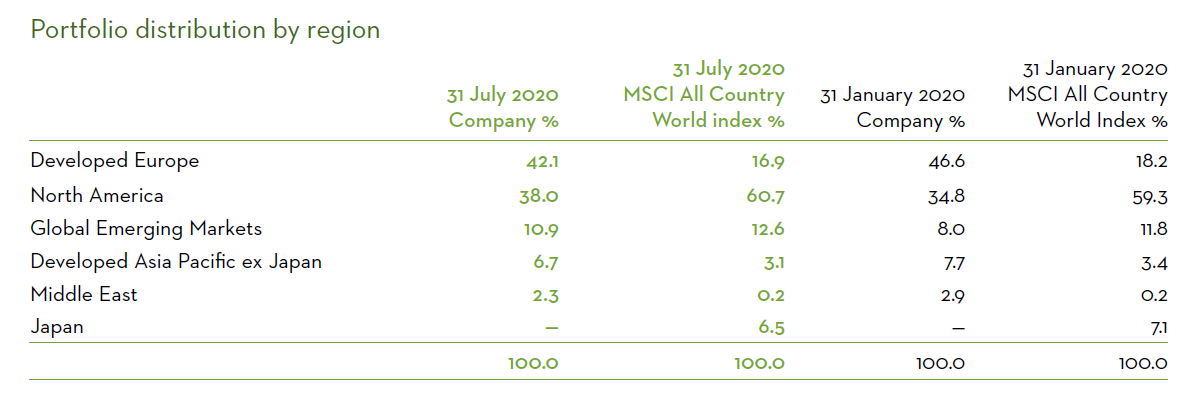

Sector and country mix

The following tables show some further portfolio analysis:

This is fairly standard for trusts following a concentrated ‘quality’ approach, leaning heavily towards newer, disruptive industries and away from more mature sectors.

Martin Currie Global Portfolio has a much higher proportion of European-listed stocks than you typically see, though. With Beazley, Unilever, and Spirax-Sarco all being ejected in 2020, I don’t think any UK-listed holdings remain.

On a look-through basis, the geographic nature of the portfolio’s revenues and profits are probably similar to other global trusts although I suspect Osmani prefers the lower valuations that a European listing usually entails.

Global emerging markets consist of Taiwan Semiconductor, Alibaba, and Tencent. Developed Asia is AIA (Hong Kong/Insurance) and CSL (Australia/Healthcare). The Middle East holding is Israel’s CyberArk Software.

Both the industry and regional mix have changed significantly under Osmani’s management, with the portfolio matching its benchmark a lot more closely under Walker.

Discount control

Martin Currie Global Portfolio instigated a zero discount policy in 2013 and it seems to have been pretty successful. It’s rare that this trust trades at a discount or premium of more than a couple of percentage points.

Generally, the trust has been a net buyer of its own shares since the policy was introduced. The number of shares in issue has fallen from 104m to 82m over this time.

Dividends

Income generation isn’t a priority at this trust and there’s no formal dividend policy in place.

Although the payout steadily increased in most years from 1999 through to 2016, it’s remained flat at 4.2p per share since then.

A switch from semi-annual to quarterly dividends was made in 2013 and the payout in recent years has been three interims of 0.9p in July, October, and January plus a final of 1.5p in April.

The annual dividend payout has totalled £3.5m for the last two years and hasn’t been covered by the trust’s net income. But there are distributable reserves in excess of £70m, so it seems unlikely the dividend will be reduced.

Gearing

Gearing of up to 20% of net asset value is allowed but, according to Edison, no gearing has been employed by the trust since 2008. There doesn’t appear to be any borrowing facilities in place at the moment.

The trust seems to operate with a small cash balance most of the time. It was 1% at the start of 2020 and just over 3% at the end of February 2020 as COVID concerns mounted.

Net cash was less than 2% by the end of March 2020 and has fallen under 1% since.

Charges

The basic ongoing charge comes in at 0.6%, which is very competitive for a sub £300m investment trust.

However, the performance fee, which is excluded from that basic figure, changes things radically, taking the total charge up to 1.5%.

[UPDATE: On 19 Jan 2021, it was announced the performance fee was to be scrapped in favour of a tiered charge structure of 0.5% up to assets of £300m and 0.35% above that level.]

Martin Currie is entitled to 12.5% of any outperformance of its benchmark on a net asset value basis. The first 1% of outperformance in any period is disregarded and the maximum fee is capped at 1% of net asset value.

That means any outperformance greater than 9% in a single period triggers no additional performance fee payment.

I’m fairly ambivalent about performance fees, especially when they are used against a specialist benchmark that you’d expect to produce better long-term returns than global markets.

But here it does make Martin Currie Global Portfolio look quite expensive next to the likes of Fundsmith (1.0% all-in) and Lindsell Train Global (0.5%). It also makes it the most expensive global investment trust, where 0.5% to 0.75% is fairly typical for trusts of a similar size.

As far as I can tell, the performance fee has been in place since the trust launched in 1999. However, it was tweaked in 2018, prior to which it was 15% if the benchmark rose and 7.5% if it fell. The base management fee was reduced from 0.5% to 0.4% at the same time.

Somewhat unusually the costs laid out in the Key Information Document are lower than the full ongoing charge.

The KID costs break down into:

- Portfolio transaction costs – 0.26%

- Other ongoing costs – 0.62%

- Performance fee – 0.24%

I think the lower performance fee element shown in the KID is because this calculation uses the year to 31 January 2019, which only covered a few months of Osmani’s reshuffled and better-performing portfolio.

Skin in the game

Four out of the five directors own a combined 87,000 shares, with a market value of £0.3m.

Legg Mason Inc/Martin Currie Investment Management own 6% of the trust’s shares, presumably via other funds that it controls. However, there is no information on the collective stakes held by Martin Currie employees or by Osmani himself.

Neil Gaskell is the longest-serving board member, having been appointed in 2011 and Chairman since 2012. The other board members were appointed in 2013, 2016, 2016, and 2019.

There seems to be a decent mix of experience on the board, with a few other board appointments at other investment trusts but no one who looks stretched too thinly.

The appointment of Martin Currie as investment managers is reviewed by the board on an annual basis.

Summing up

Osmani seems to have done an excellent job of reinvigorating this investment trust, turning it from a decent one to a potentially great one. It’s still early days, of course, but he’s relatively young as trust managers go.

Originally an academy footballer at Paris St Germain, he started his investing career at Scottish Investment Trust before taking on roles at Scottish Widows, Commerzbank Securities, UBS Warburg and Credit Lyonnais. He then spent 10 years at BlackRock before joining Martin Currie.

Perhaps the biggest risk is that he gets snapped up by someone with deeper pockets or moves further up the larger Franklin Templeton structure.

My other concern would be that performance fee, which does make this trust look pretty expensive when compared to other global trusts.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Thanks for keeping up the high standard and thoroughness of your posts.

This is a fascinating one. The portfolio is pretty top notch. I have also been very impressed by the USA OEIC he manages.

Minus points for being at a big institution (who knows when he might leave) and concern that he may be managing too many different funds. And, as you say, the management fee.

I got the sense that there is a higher portfolio turnover than I’d like. As with Blue Whale, it will take some time for me to believe that they can consistently do this well, as the vast majority can’t, and the smart money often doesn’t bother.

Also, beyond all the marketing blurb, I don’t REALLY understand his investment philosophy, though if it’s just ‘buy good companies’ he seems to be doing that well.

Finally, the more funds being run a la Fundsmith (i.e. 30 quality holdings) the better in most respects, but there is a small fear that it adds to certain companies’ valuations being gradually driven to dangerous ‘Nifty 50’ extremes.

Thanks for this article, very interesting, I am debating to buy it.

Btw can I ask for your opinion of Henderson International Income Trust?

Another great article – many thanks!

This one has been on my watchlist for a while now.

I like:

* Active share component

* Less dominated by US than other global ITs

* Performance under his stewardship thus far

* Thematic approach

Concerned by:

* Fees (performance)

* short track record

Still watching this one closely …

Thanks David and tom!

@M — I’ve never really looked at HINT in any detail I’m afraid. It seems to have suffered the fate of many trusts that have been underweight the US over the last few years and underperformed global markets somewhat, similar to my holdings of RCP and CLDN. Just looking down its latest full portfolio, it seems to hold quite a mixed bag of companies but that’s just a first impression from a very quick pass.

Thanks for the article, very interesting as usual. But this seems to be essentially a trust newly created two years ago by Osmani inside an old “wrapper” with only the name remaining the same. In which case, surely any older performance statistics are no longer relevant.

Hi David,

Yes, I think that’s a fair point. It’s difficult for outsiders to know exactly how much a trust changes when a new manager takes charge.

Some of the larger firms have a strong culture and changes can be made almost seamlessly, especially where the new manager serves as a deputy to the old one for several years beforehand.

But in this case, it does almost seem like a new trust given how many of the holdings were sold off and the fact Osmani came in from elsewhere. However, it’s worth noting that a number of holdings were only sold earlier this year so Osmani did keep a few more legacy positions for eighteen months or so and then re-assessed their prospects in light of COVID.

I still like to look at older performance stats to get a feel for how the fund management firm has performed over the long term. I think a firm that has been able to appoint a succession of good managers has a better chance of continuing to do so in the future.

The restructuring of this IT has me baffled and worried

I have a small holding and could accept the reduction in yield in the present climate but could not believe the holding that were sold and the massive buy up of tobacco shares .

This now is a IT to dispose off

Hi REd — you’ve confused me a bit. Are you talking about Martin Currie Global Portfolio restructuring (I can’t see that it has, not recently anyway) or another trust?