The shipping empire turned investment trust Caledonia Investments (CLDN) is currently one of my biggest holdings. It’s one of a few listed funds that is still family controlled and it boasts a 51-year track record of increasing its dividend. What’s more, it’s beaten the UK market by a respectable margin since it became a fully fledged investment vehicle in 1987. Yet it persistently trades at a discount to net assets of around 20%. So, what gives?

Part of the problem is that Caledonia is pretty conservative in its outlook. And although it uses a UK benchmark, it’s usually, and correctly, lumped in with global investment trusts.

Certainly, other global investment trusts, most notably Scottish Mortgage (SMT), have been far more swashbuckling in their approach. That’s somewhat ironic perhaps, considering Caledonia’s higher-risk, sea-faring roots!

My initial stake in Caledonia dates back to 2011, and I’ve topped up my holding a number of times since. Up until a couple of years ago, it was pretty much keeping up with its global brethren. It seems that a large cash position and a low weighting of US stocks have held back its most recent returns.

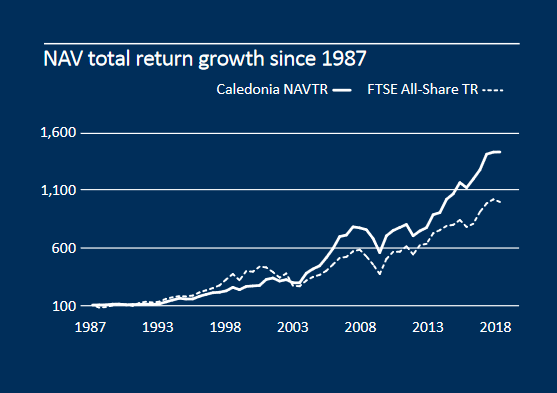

Caledonia’s performance

You can see this recent tail-off in Caledonia’s performance in the chart below. It’s also noticeable that it didn’t get off to an auspicious start, trailing the market for most of its first fifteen years.

Indeed, it’s main period of outperformance was probably 2000-2007, so that’s now over a decade ago. I suspect it wasn’t particularly overexposed to tech shares during the dot-com boom and subsequent bust.

In terms of hard figures, its record from 1987 to 2017 was a 9.6% average annual return. This compares to 8.1% for the FTSE All-Share and 3.3% for UK inflation.

Caledonia has three stated aims. The first is outperforming the UK market over rolling 10-year periods and UK inflation by 3-6% over shorter (undefined) periods. While it’s ahead since 1987, it’s slightly behind the market over the last 10 years.

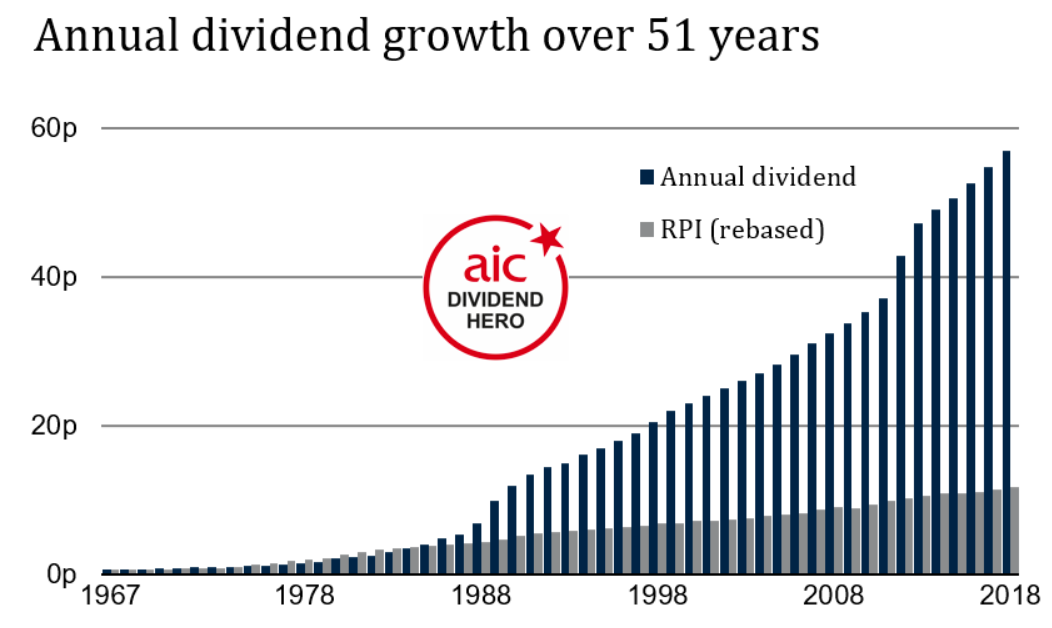

A (low-yielding) dividend hero

Caledonia’s second stated aim is to pay an increasing annual dividend. It seems to have ticked that box pretty comprehensively.

Caledonia is one of the leading dividend heroes as defined by the AIC, the industry body for investment trusts. Only City of London (which I also own), Bankers, and Alliance Trust can boast a longer record, and they only outmatch Caledonia by a single year.

A 100p per share special dividend was paid in 2017, and further ones could be paid should there be surplus funds. As far as I can tell, only two other special dividends have been paid previously: 70p in 2000 and 30p in 1997. So, I wouldn’t count on them becoming a frequent occurrence.

Despite the long track record of increases, the current yield on last year’s 57p per share dividend is only 2.0%. As a percentage of net assets, the yield is just 1.7%.

Recent dividend growth (that special dividend apart) has been a little pedestrian. After a 16% increase in 2012 and a 10% jump the year after, the last five years have seen an average of just 3%.

The popularity of income investing has surged in recent years. And some funds even have stated dividend targets, paid out from capital if needed. Caledonia’s low yield is therefore perhaps another reason why its discount has steadfastly refused to narrow.

Caledonia’s third and final aim is to “manage investment risk consistent with long-term wealth generation”. That seems pretty meaningless to me, so I’m going to ignore it!

Meet the Cayzers

The Cayzer family control 48.5% of Caledonia’s shares, mostly through the Cayzer Family Trust Ltd. A little history is worth recounting at this stage.

Charles Cayzer set up the Clan Line in 1878. I don’t think it was part of the inspiration for the 70s BBC TV serial The Onedin Line, but it shared its Liverpool roots. It had 100 ships by 1916 but suffered many losses during both World Wars.

The Clan Line merged with the Union Castle Line in the 1950s, forming British & Commonwealth Holdings. The Cayzers injected their holding in British & Commonwealth into a company called Foreign Railways Investment Trust, renaming it Caledonia Investments.

Caledonia joined the stock market in 1960. Over the next few decades, British & Commonwealth stopped building ships and used the cash flow from shipping to expand into hotels, engineering, chemicals, financial services and airlines. Caledonia’s holding reduced from high 40% to the low 30% during this period.

The Cayzers sold out completely from British & Commonwealth in 1987, effectively starting again with Caledonia Investments as their main investing vehicle. That proved to be very prescient. The following year British & Commonwealth bought Atlantic Computers, only to fall into administration in 1990 after significant accounting irregularities were discovered.

So that is a long-winded explanation as to why Caledonia’s track record effectively starts in 1987, despite its 51-year record of rising dividends.

Wyatt takes the reins

Another bit of history worth mentioning is a fairly major shift in strategy following the appointment of Will Wyatt as CEO in 2010. In fact, I think it was articles covering this that first piqued my interest in Caledonia.

Up until this time, Caledonia had a strong sector focus, most notably in financial services. It had stakes in Rathbones, Fleming, Close Brothers (where Wyatt was recruited from in 1997) and Polar Capital.

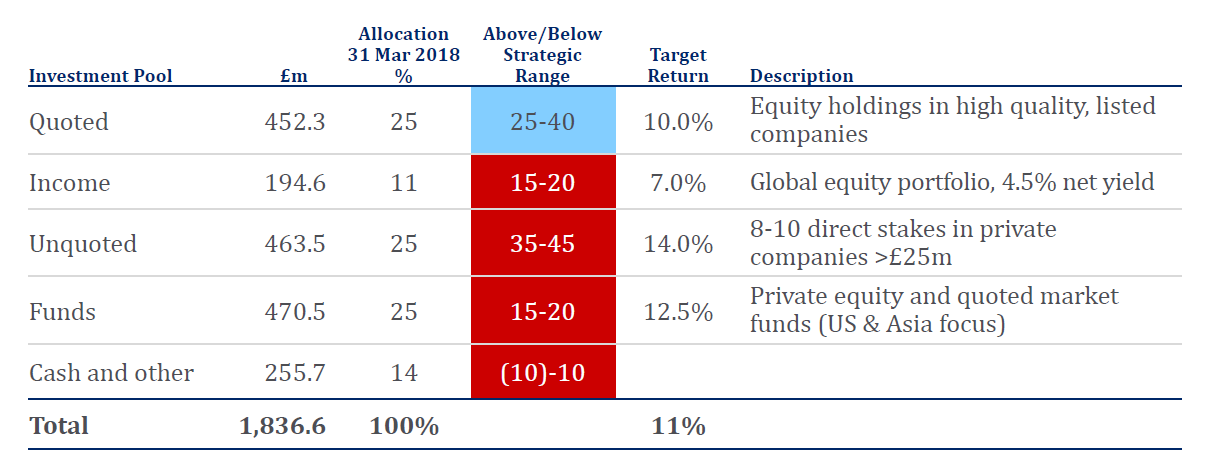

These are Caledonia’s investment themes now:

The split between quoted, unquoted and funds has shades of RIT Capital Partners, although RIT has more in funds and less in the way of directly listed investments.

I can’t say I’m that bothered that most of the allocations are outside of its stated strategic range, although it does perhaps give an indication of which direction Caledonia is most likely to move in. Expect to see a little less in the way of funds and cash, but perhaps a little more in income investments and unquoted.

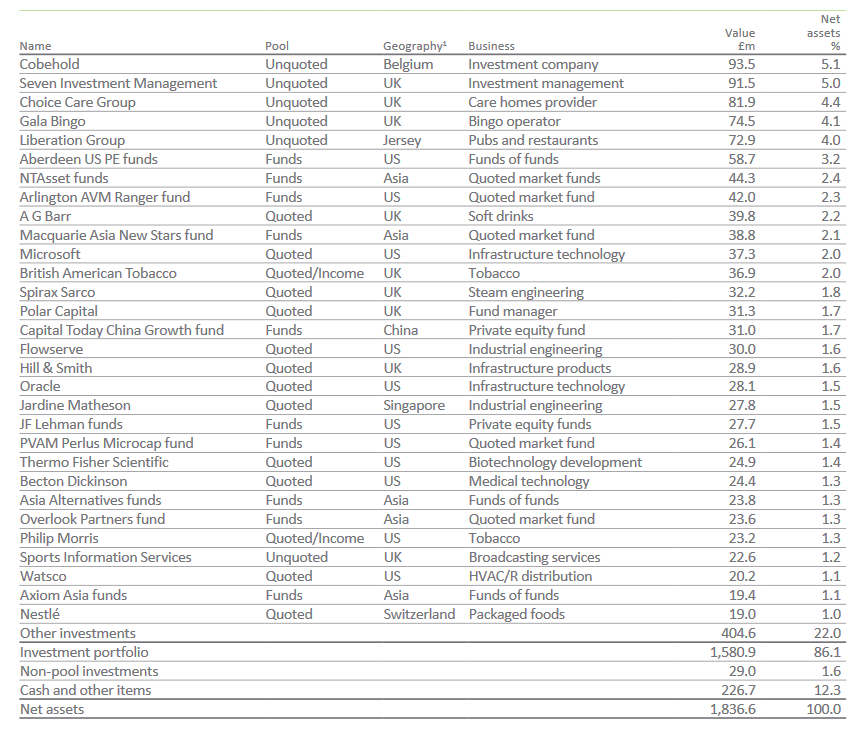

Breaking it down a little further, these are Caledonia’s top investments as of 31 March 2018:

Long-term holding Polar Capital remains in the mix. Close Brothers was sold a couple of years ago, though, having been a core holding since 1987. Most of Caledonia’s other main investments have been made since the shift in strategy, with Spirax-Sparco often mentioned in glowing terms.

This summer, Caledonia invested £92.5m in a majority stake in Cooke Optics. Follow-up investments of £14m have been made in both Gala Bingo and Seven Investment Management, too. But Caledonia still retains a pretty large cash position, due to concerns about the UK and US economies.

Should opportunities arise, Caledonia looks pretty well placed to pounce. As well as its cash position, it also has access to £250m of borrowing facilities.

The challenge of costs

Caledonia’s stated ongoing charge last year was 0.9%, which seems fairly reasonable on the face of it. Total management expenses charged to the profit and loss account were £23m, which was about 1.25% of year-end net assets.

Turn to the much-maligned Key Information Document and total charges, including those made by the funds Caledonia invests in, and the figure leaps to 2.5%.

I’ve been somewhat glib about fund costs in the past, and I often need to refresh my memory about which type of costs are included in the various different definitions. However, I suspect it’s something I will be focusing more on in the future.

With Caledonia, I’m surprised there is such a big gap between the headline and KID figures. The latter breaks down into 0.07% for trading costs, 0.26% for performance fees and a staggering 2.16% for other. With a quarter of its money invested in funds, you’d expect the underlying costs to bump up its expenses, but not by that much.

It would be good to see a breakdown of this ‘other’ figure in future KIDs. The Caledonia annual report also seems very light on the discussion of costs as well. So black marks all round on this front.

Still a fan, for the most part

I still like Caledonia Investments, despite its weaker performance of late compared to other global investment trusts. As I alluded to earlier, that seems to be down to a low US weighting and sitting on cash. There doesn’t seem to be an underlying problem with the investments it’s selecting.

Its share price tends to be a bit less volatile than the UK market, which appeals to me, and I like the look of its current slate of unquoted investments. I am planning to cut down my position size a little, but that’s something I’m doing across my entire portfolio. I will, however, be keeping an eye on its costs. A prolonged period of poor performance could see it get the chop entirely, depending on the reasons why.

I’m not expecting the discount to narrow particularly unless Caledonia takes specific action to address it. I’d like to see a little more action on that front. The presence of the Cayzer family means the likelihood of activist shaking things up seems pretty low.

The company’s website is a good source of information for further reading, particularly the Capital Markets Day presentation from last year.

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!