I like impossible questions… and overly long article titles. The wildly gyrating share price of Lindsell Train Investment Trust has once again focused attention on its massive premium to net assets. How did it arise and is it justified?

The Hargreaves effect

The cause of the latest volatility was Hargreaves Lansdown announcing that it was removing two of Lindsell Train’s funds from its Wealth 50 list.

The Lindsell Train Investment Trust share price has gone from £1,952.50 on Thursday, 4th July to £1,280 as of today (Thursday, 1th July). That’s a drop of 35%, give or take.

Typically, this is an investment trust that sees 50-100 trades a day but the last few trading days have seen about 400-500 each.

Collectively, Lindsell Train’s funds own about 12% of Hargreaves Lansdown. The concern was this created a potential conflict of interest (as usual, Nick Train had a prompt and well-balanced take on the situation).

Lindsell Train Investment Trust (LTIT) has a significant holding in Lindsell Train Limited, the fund management firm that runs all of Lindsell Train’s funds. As of 30 June 2009, this holding accounted for an incredible 47% of LTIT’s assets.

It’s rare for an investment trust to have more than 10% in one position. Some even limit it to 5%.

47% of assets in one position is pretty much unheard of.

The theory is that exclusion from the Wealth 50 could hamper the hitherto rapid growth in Lindsell Train’s funds, and therefore in the valuation of Lindsell Train Limited.

Personally, I don’t think the exclusion from the Wealth 50 will have that great an impact in the long run. More and more people are now seeing such lists as a busted flush and Lindsell Train’s reputation should be enough to maintain a decent flow of funds through its doors.

That premium

Here’s how LTIT’s premium has changed over the past year:

Yes, the premium actually exceeded 100% for a brief time in May and June. And it’s rarely been less than 50% this past year.

LTIT’s premium first arose back in 2011, as far as I can tell. It was a sober 5-15% for a few years but started increasing in 2015, reaching 60-70% in late 2016.

The premium then actually dropped back for a while, and even went under 10% in late 2017 and early 2018, before its latest rise (and crash) shown in the chart above.

With LTIT’s share price at £1,280 per share and its latest net asset value being £1,068, that means the premium has shrunk from 83% to 20% in less than a week.

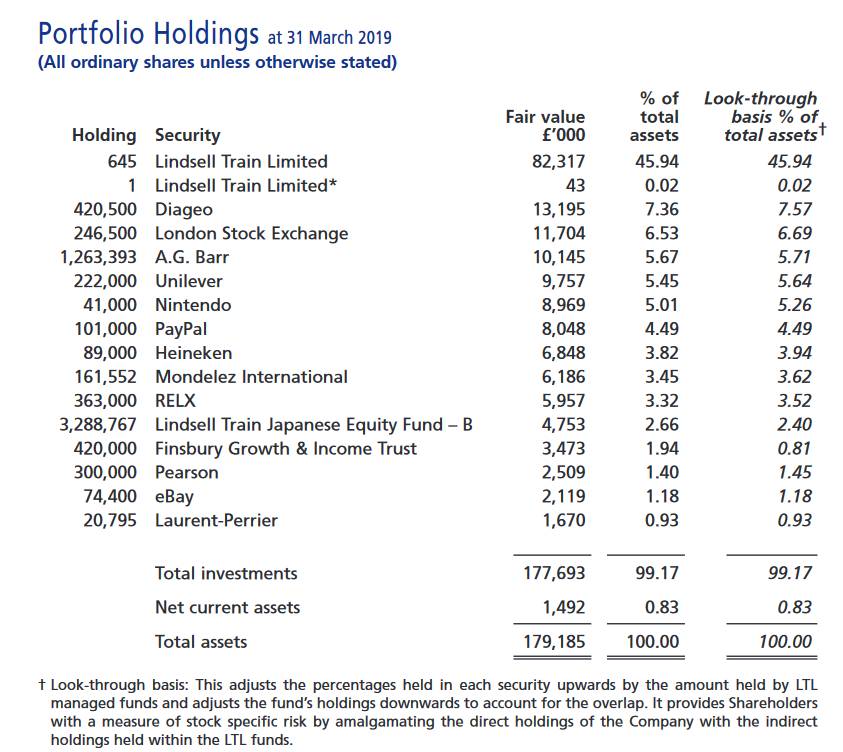

Lindsell Train Investment Trust’s portfolio

Here’s how LTIT’s portfolio is made up. I’ve used the version in the latest accounts, so it’s a few months old. But as Lindsell Train so rarely buys or sells investments, it’s likely to be much the same today.

Apart from the stake in Lindsell Train Limited (the single share shown above is an option), everything else is bog-standard equities.

As you can look at an investment trust’s portfolio and replicate any listed positions it has, there’s typically no reason for a standard equity fund to trade at a premium to its net assets.

If a manager is particularly well regarded, you might get a premium of up to 5%. Finsbury Growth & Income, the other investment trust managed by Lindsell Train and which has a number of the same holdings, trades at a premium of 0.6%.

That’s a long-winded way of saying that the entire premium for LTIT is basically down to the value of the Lindsell Train fund management business. Or at least what investors perceive it might be worth in future.

For simplicity, let’s assume LTIT’s stake in Lindsell Train Limited is officially valued at £100m (it was £99.3m in June 2019 so that’s pretty close).

Here’s what a range of premiums imply the valuation is actually worth:

| Premium | 0% | 20% | 50% | 80% | 100% |

|---|---|---|---|---|---|

| Implied value of LTIT’s holding | £100m | £143m | £206m | £270m | £313m |

A 100% premium means investors buying LTIT shares were assuming its stake in the fund management business is worth more than three times its official valuation.

Back to the early 2000s

Before we look at the official valuation that LTIT uses, let’s take a break from the number-crunching and roll back the years.

Lindsell Train Limited was set up in 2000 by Nick Train and Michael Lindsell. They worked together at a firm called GT Management in the 1990s, which was acquired by Invesco in 1998.

Initially, it just managed two investment trusts, LTIT and Finsbury Growth & Income.

LTIT’s initial portfolio looked very different from the way it does today:

30% was in US and UK government debt and a further 11% in Halifax/HBOS preference shares.

But you can see the beginnings of Lindsell Train’s focus and consumer goods and media brands, with the likes of Cadbury Schweppes, AG Barr (the maker of Irn Bru and the only listed investment still in the LTIT portfolio today), and Reuters.

Down near the bottom is Lindsell Train Limited, valued at just £0.6m and accounting for less than 3% of net assets.

The transformation begins

Lindsell Train Limited’s turnover exceeded £1m in the year ended 31 January 2002 but fell back below that level for the next few years. It didn’t top £1m again until the year ended 31 January 2006.

In 2004, Lindsell Train took over a Japanese open-ended fund. Then in 2006, it launched a UK open-ended fund and the scale of the business was transformed. This was followed by a global open-ended fund in 2011 (I’ve owned this fund since 2016, and it was the large premium on LTIT back then that prompted me to choose the global fund over the investment trust).

By January 2009, turnover had surged to £3.6m. The financial crisis caused a one-year blip, but turnover recovered and hit £8.0m by January 2012.

Since then…

| Year ended 31 Jan | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 |

|---|---|---|---|---|---|---|---|

| Turnover (£m) | 84.5 | 60.9 | 39.8 | 32.3 | 19.3 | 17.4 | 9.7 |

| Operating profit (£m) | 55.4 | 37.9 | 27.1 | 20.2 | 12.4 | 10.2 | 5.9 |

| Operating margin | 65.6% | 62.2% | 68.1% | 62.5% | 64.2% | 58.6% | 60.8% |

| Post-tax profit (£m) | 45.0 | 30.6 | 21.7 | 16.2 | 9.7 | 7.8 | 4.5 |

| Assets managed (£bn) | 16.3 | 13.2 | 9.0 | 6.1 | 5.0 | 3.4 | 2.4 |

| Turnover as % of assets managed | 0.57% | 0.55% | 0.53% | 0.58% | 0.46% | 0.60% | 0.44% |

What a fantastic business this has been, with turnover growing more than tenfold from 2012 to 2019. Operating profits did even better, going from £4.6m to £55.4m.

The UK and global funds are now the largest by a long distance, with £7.2bn and £8.4bn in assets respectively. Finsbury accounts for £1.7bn, the Japanese fund £0.4bn, while LTIT brings up the rear with £0.2bn.

Lindsell Train also runs funds for institutions (17 at the last count and with about £4bn in assets), bringing its total assets under management up to £21.6bn as of June 2019.

The current year to January 2020 will probably see turnover pass the £100m mark. It might even exceed £125m if markets continue to be buoyant, which could see operating profits in the region of £80m+.

Assets under management have already risen by more than £5bn in 5 months, boosted by rebounding markets and a surge of cash inflows. The latter is no doubt partly due to the troubles of Mr Woodford.

To generate all this cash, Lindsell Train Limited has just 18 employees. Woodford, once of a similar size in terms of assets managed, reportedly has 44 while Fundsmith has 28.

Putting pressure on the premium

A couple of decisions Lindsell Train has taken have also boosted the premium that LTIT trades at.

Firstly, LTIT doesn’t issue new shares. It had 200,000 in issue back in 2001 and has exactly the same number today.

Most investment trusts that trade at a premium issue new shares on a fairly regular basis. This can help to soak up investor demand and ensure the premium doesn’t get too big.

The risk with too big a premium is that it can cause the share price to collapse should a fund fall out of relative favour. No one likes that, especially as it normally goes hand in hand with a fall in net asset value as well.

Secondly, Lindsell Train has committed to not materially diluting LTIT’s stake in Lindsell Train Limited. LTIT started with 666 shares and it still has 645 today.

Overall, LTIT owns 24.3% of Lindsell Train Limited, Train and Lindsell’s families own 36.3% each, and employees the remaining 3.2%.

I’m not sure when this commitment was first made, but I wonder what would happen if you could travel back in time and told Lindsell and Train that this stake would account for nearly half of net assets. Would they have still made the same commitment?

However, you have to admire them for sticking to their principles on both of these matters.

Despite its success, LTIT is still pretty small

LTIT’s market cap is around £260m although it reached £400m for a brief time recently. That’s on the small side for an investment trust, so that ratchets up the pressure a bit more.

The shares don’t seem to be particularly tightly held. Nick Train, Michael Lindsell and Finsbury Growth & Income own 16% collectively. But among the biggest holders are clients of Hargreaves Lansdown (17%), Alliance Trust (5%), AJ Bell, and Interactive Investor (both 4%).

The exchange market size for LTIT is just 2 shares, meaning market makers are not obliged to honour the quoted bid and offer spreads for deals of 3 or more shares.

I suspect there may even be a few folks that don’t wish to sell because they have a sizeable capital gains liability. In its first eighteen and a bit years, LTIT has risen 23 times and it was up 487% in the five years to May 2019.

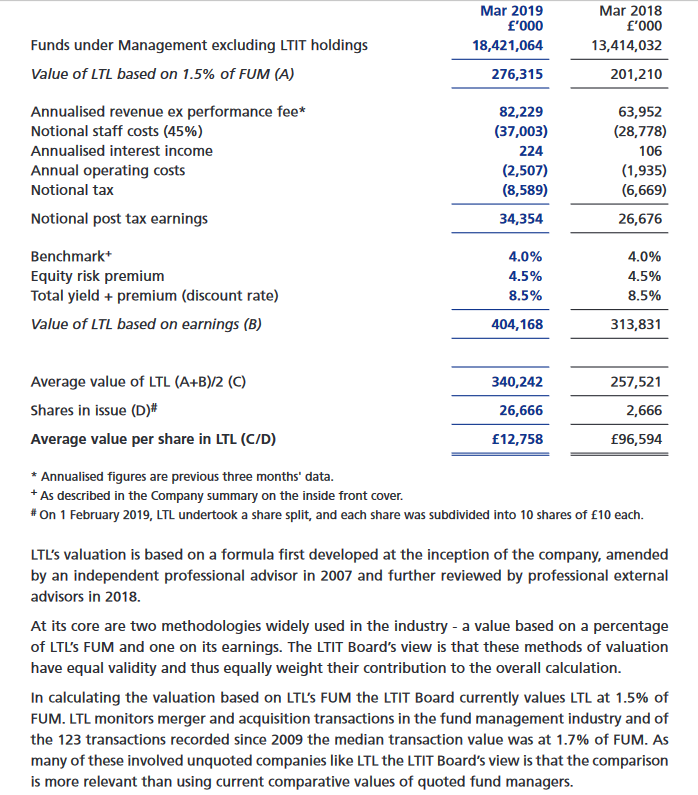

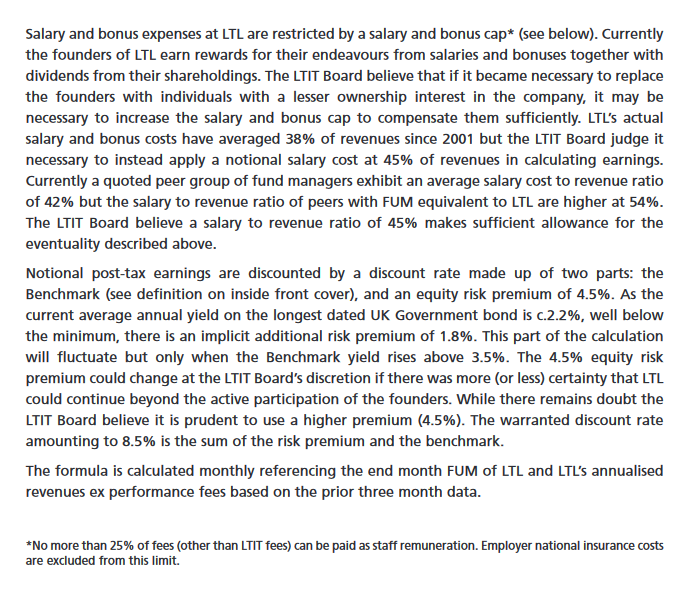

Lindsell Train Limited’s official valuation

The last piece of the puzzle is the official valuation. It’s laid out in a pleasing amount of detail in Appendix 1 of LTIT’s accounts.

Let’s look at how it is calculated and how frequently it is updated. If it seems to be on the cautious side, then paying a premium for LTIT is more understandable.

I’ve reproduced the relevant sections below for completeness but the tl;dr version is that it takes the average of two valuation measures.

One is based on assets managed, the other on a multiple of earnings (adjusted for higher staff costs that would be needed to run the business in Nick Train and Michael Lindsell’s absence).

And the valuation is updated monthly, which I was a little surprised to see at first.

I thought it might be quarterly or even six-monthly, meaning the valuation was always a little bit behind events. But monthly makes sense given the size of the holding and the ease of which fresh numbers can be plugged in.

There’s a fairly widely used rule of thumb that 2% of assets under management is a reasonable valuation for a fund management business.

LTIT uses 1.5%, which is a lot more conservative, citing the fact that comparable unlisted businesses have gone for 1.7% over the past decade.

I suspect the last, say, three years would see that comparative a bit higher, perhaps even 2%. But without seeing the breakdown of the number of transactions and their multiples is hard to know for sure.

The earnings multiple calculation seems about right I would say. Excluding all performance fees from the earnings calculation is perhaps a little cautious, but understandable. They accounted for about 10% of revenues in the year ended January 2019.

The 8.5% discount rate is the same as applying a profit multiple (P/E ratio) of 11.8. Adjusting a business’s profits for what might happen when its majority owners depart is standard practice.

If Lindsell and Train sold the business, it seems unlikely they would hang around for too long on the payroll. They certainly don’t need the money!

The issue of succession

Lindsell is 59 and Train is 60. Michael Lim, the chief operating officer, is 63 while Jane Orr, Head of Marketing, is 60. You could see them all departing within 5 years, although I suspect they wouldn’t all go at the same time.

The investment staff recently increased from 5 to 6 (that’s including Lindsell and Train). James Bullock is the heir apparent and has been co-managing the Global Fund since 2015.

However, you could argue that the sloth-like pace at which Lindsell Train buys and sells its investments makes succession a little less of a concern.

True, there is plenty of trading activity as the open-ended funds grow in size, but I expect there is a pretty good understanding within the investment team of what makes up the Lindsell Train special sauce.

So, a sensible premium is?

Let’s say we bump up the valuation assumptions to 2% of assets under management and use the likely adjusted profits for the current year to January 2020 rather than historical numbers.

This might give you a value of £450m to £500m for the entire firm and perhaps £110m to £120m for LTIT’s 24.3% stake. It’s finger in the air stuff, admittedly.

With LTIT’s holding valued at £100m as of June 2019, that’s not a significant difference. It suggests to me that paying a premium of up to 10% LTIT’s net asset value looks reasonable.

The current premium of 20% isn’t that far off this of course. But paying much more than this would be a turn-off for me, especially given the fact I already have largeish position sizes in Lindsell Train Global and Fundsmith. I wouldn’t want to become overexposed to this style of investing given its great run in recent years.

To its credit, it’s worth pointing out that LTIT regularly warns about the excessive premium in its results and in its monthly commentary.

A limit on growth

There’s an interesting commentary from Michael Lindsell on how big Lindsell Train’s funds might be able to get given their current investment strategy. It was published in May 2019, just before fund liquidity become such a hot topic of discussion.

Based on a self-imposed 15% limit in any individual company, the maximum size of the Global fund could be £15bn, a little under twice its current level of £8.4bn. So, there’s room for more growth, but certainly not at the pace that we’ve seen the past seven years.

The companies that Lindsell Train invests in may continue to do well, but it’s not inconceivable that the UK and Global fund could be closed to new money at some time in the not too distant future. That would limit the growth prospects for Lindsell Train Limited.

If you’re a long-term holder of LTIT, I’d love to hear your thoughts on the premium it trades at and whether it’s affected the position size you’ve had over the years.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Many thanks for this post and especially links; I think I’d signed up recently for your newsletter by following one in the excellent Monevator weekend reading. Although I’ve been d-i-y investing for some 20-odd years, having been ‘forced’ to leap in by a catastrophic concatenation of personal circumstances, it was just around the time when it became feasible to do so online even for the ignorant and impecunious. I hadn’t a clue, and then had no idea that financial bloggers were a thing (maybe any blogs). There was much to learn, only possible by doing it.

I did all my research through Trustnet, which at the time appeared least biased (before it offered live accounts, in other words), set up dealing accounts all over the place, including with Alliance Trust Savings for a brand-new SIPP, and Hargreaves Lansdown. I had a bit of a run-in with the latter over their handling of some zeroes but kept the account because of their then-extensive in-house ‘research’ and (despite the fees) I still find their site the most user-friendly even today. The original partnership was MUCH smaller of course but already very sales-oriented, and way back then it was possible to believe that it had a policy of supporting small managers and slightly more niche investments as well as we humble investors. In the early days of the LT open-ended funds, they were certainly hard to buy elsewhere, especially Japan.

I’m honestly not sure which of the LT vehicles was my first – I’ve used all, in various accounts at various times on various terms. Quite early on I decided that the SIPP by definition should be long-term (I’d soon realised how much trading was costing) and had started buying a few ‘family office’ type ITs such as RCP and CLDN. I read an interview with Nick Train, to the effect that the most reliable source of income was consols at around 2%, which set the benchmark for LTI. I think when I bought the first tranche it was 3 in number and the whole lot cost me around £500, which seemed a massive amount for so few shares. Sadly without venturing into the loft I’ve no record as to any discount or premium, but suspect that such a bold move could only have been possible if the former was reasonable – I still won’t buy at a premium. As far as I remember, around the time of that interview, the Government was redeeming War Loan stock, possibly and/or the said consols – I’ve an idea that the point he was making was that they were no longer available, and LTI would offer an alternative. He seemed a decent chap, remarkably honourable for a fund manager – in a much later manager’s report, he said he was ‘mortified’ that something or other had been disappointing. We’ve all been there. Interestingly the commentary you provide is consonant with that, and I’m really looking forward to hearing from the Crown Prince at some later stage.

Not much happened for a while, but from time to time ATS did free share purchases and I added a couple of shares now and again, always at a higher price than the last time. As RDR came and went all the providers changed their fee structures, I moved the SIPP elsewhere, partly in specie, and then again to AJ Bell not long ago. They seemed not to know what LTI was, thought that somehow I’d got hold of a share that’s not publicly available and took months to buy it, which was worrisome, but the LT site is as you say very transparent. I still have my holding and have never sold any. When it was queried by AJ Bell, I explained that I’d kept it in case I ever wanted to take my 25% tax-free as I’d only have to sell one holding, such was then the premium. I’m now watching hawklike in case it drops to NAV … .

I didn’t take up the share offer when HL went public, being still wary of the firm’s behaviour (see above). A few years back, commentary on its annual report said that it had made 64% profit, which seems astronomical to me. I’d already noticed that post-RDR as it all shook out, one or other of the LT open-ended funds was cheaper to own through HL than through any of my other accounts, and assumed that this was simply because of the size of HL’s nominee holding – this seems to be confirmed by the recent announcement of the reduction in OCF by making available that particular class of share. LT’s fees do appear to have increased generally over the years, possibly resulting from the demands of RDR, but I do owe the firm much deep gratitude for the increase in my (theoretical) net worth. I’d noticed that size does matter, and apart from LTI have diligently applied Michael Lindsell’s principles to my modest mite. It was good to be reminded of this, thank you again.

Sorry about the length!

Thanks, Lindsey. I can hardly complain about lengthy comments when I post lengthy articles myself! It’s great to hear other investing stories, though, especially those who have stayed the course like you have and been duly rewarded.

I remember first becoming a client of HL in the 90s through its association with Analyst magazine — it’s incredible how far the firm has come since then.

The LTI share price seemed to drop to 1,200p soon after I published this piece, but it’s already rebounded to over 1,400p less than a day later. So neither of us may get the chance to buy at a discount for a little while I suspect.

Nick Train has just said this in the latest monthly commentary for LTIT:

Mike and I are significant personal shareholders in LTIT and have not sold a share since flotation, 2001 – and have no intention of doing so. However, we have not added to our holdings for many years. This is because we have always believed that the independent directors’ valuation of LTL within your company is fair. Our longstanding view has been that if we purchased shares above the price of the published NAV we would thereby be signalling that we thought the directors’ valuation was too cautious. We don’t.

We reiterate last month’s comments that our plans for succession are still at an early stage. Therefore simply comparing the value of LTL to quoted fund management groups without taking account of succession risk, as some investors seem inclined to do, is misleading. It is for this reason that we have held off from buying more shares in LTIT (although we continue to personally invest in our other LTL-managed funds).

Nonetheless, I think it’s important to say – though without making any irrevocable commitment today – that if we ever again have the opportunity to buy LTIT shares on such terms, we’d absolutely love to do so. Mike and I remain committed to the company we established, enjoy our work, are continuing to build up a strong investment team around us and believe our investment approach, consistently applied, should deliver satisfactory returns to investors over time.

Thanks for this thorough overview of a truly unique investment trust.

How to handle the share price is a proper conundrum. My instinct is that one either A) slowly starts to sell when the premium gets really silly e.g. 75%? in the hope that one can buy them back at a lower price in the future or B) buys more when the premium gets to the teens or lower. If your holding gets too big later on you can reduce at a profit.

Of course this year was a great example of the problems of timing – if you sold at a 75% premium, it then kept on going up for a while, making you feel very frustrated.

The issue of the funds closing is also very interesting, if probably some way off. I suppose the optimstic view is that in the meantime global companies get bigger and bigger, resulting in them revising the figure up (you’re probably aware of how EM smaller co funds have tended to react to this i.e. increasing the maximum market cap of companies they can own).

There is also the succession issue – my instinct again is that this will be tricky, no matter how talented Bulloch etc are (and I do believe in them) as it is very tricky to replace the halo effect created by larger-than-life founders such as Train and Lindsell.

On a separate note, it would be fascinating at this point to see Lindsell Train ‘doing a Smithson’. Their only small/mid-caps I can think of now are A.G. Barr and the champagne.

To sum up, I very much hope that the Trust keeps performing and the premium stays steady and not too crazy.

I admire Lindsell and Train so much for their integrity and fiduciary duty to clients, and I think its good for the industry to have examples like this. If only there were more fund managers like them.

p.s. Forgive the pedantry – you said that A.G. Barr was the only listed equity surviving from the first Annual Report – I think you’ll see Nintendo is still there as well (and arguably Cadburys has survived in the form of Mondelez, but that’s getting really silly!).

Good spot, TB. Not sure how I missed Nintendo!

And as far as I can tell they kept the Kraft Foods’ shares that were part of the Cadbury offer back in 2010, so that one seems a fair shout as well.

“It suggests to me that paying a premium of up to 10% LTIT’s net asset value looks reasonable.”

The last time that Nick Train & Michael Lindsell bought shares in LTIT was in 2012 when they were at a premium of 8%. Train recently said that he would love to buy more shares on the same terms so your limit of 10% looks spot on.

How are you feeling about the Premium (or Discount possibly) now?!

(it’s bouncing around at lunchtime, got down to 1050, but seems to be back up to 1080/90 now. Who’s selling? What do they know? etc. etc.).

@tom_grlla

I just bought some today. Couldn’t resist and snagged some at £1060!

Seems like a good price, Henry. Last NAV was £1,072 as of 31 Jan 2020, but I doubt it’s moved that much since the Global fund has been pretty flat in February.

Both the main UK and Global funds saw outflows in January it would seem. The former went from £6,727m to £6,562m (but most of this was due to unit price falls) and the latter from £8,444m to £8,235m (despite flat performance). I guess some folks think this trend may persist and the value of Lindsell Train Limited could fall as a result.