Monks Investment Trust has seen a big upturn in its performance in recent years but a change at the top is due to take place next April.

It has £2.1 billion of assets, making Monks one of the larger trusts in the global sector. It’s run by Baillie Gifford and like many of its stablemates, it heavily favours the growth style of investing.

Key stats for Monks Investment Trust

Figures are as of 22 May 2020 unless otherwise stated:

- Founded: 1929

- Current manager: Charles Plowden (from Apr 2015 until Apr 2021)

- Next manager: Spencer Adair (from Apr 2021, currently deputy)

- Management firm: Baillie Gifford

- Ticker: MNKS

- Benchmark: FTSE All-World

- 10-year net asset value return: 258%

- Share price: 969p

- Indicated spread: 968p – 970p (0.2%)

- Exchange market size: 2,000

- Market cap: £2.2 billion

- Premium to net assets: 2.3%

- Costs: OCF 0.5%, KID 0.9%

- Net gearing: 6% as of 30 Apr 2020

- Historical dividend and yield: 1.85p and 0.2%

- Results released: Jun (finals) and Dec (interims)

- Sector: Global (4th out of 16 over the last 10 years)

- Links: Website and AIC page

A little history

Monks Investment Trust was set up in 1929. According to Wikipedia, it was one of three trusts run by a group of investors — the other two being called Friars and Abbots.

Baillie Gifford, whose own history I covered in a recent article on Scottish Mortgage, took over management of the three trusts in 1931. Friars and Abbots were then merged into Monks in 1968.

Befitting Baillie Gifford’s long-term outlook, the lead manager of Monks has changed relatively infrequently in recent years.

Douglas McDougall ran Monks between 1984 and 1999 and then was a director from 1999 to 2019.

Richard Burns headed things up from 1999 to 2006, with Gerald Smith doing the honours from 2006 to 2015.

Performance wobbles

Under Smith, Monks did pretty well for a while but then its performance fell back against the FTSE World Index.

From his appointment up until 2015, Monks share price return was up 67% compared to 95% for its benchmark.

According to articles of the time, Smith’s conservative style failed to keep up as the world recovered from the financial crisis.

Monks’ directors took action, with Smith being replaced by Charles Plowden.

From its 2015 annual report:

In 2013, the Board and the Managers undertook a thorough review of the causes of the Company’s relative underperformance in recent years. Actions were taken to improve performance, including the strengthening of the team managing the portfolio. Although there were some initial encouraging signs, performance did not improve markedly.

More recently, I have met a number of shareholders who wished to discuss the Company’s performance and portfolio management arrangements, independently of the Managers. During the course of these meetings, it became apparent to me that these shareholders supported the Board’s view that Baillie Gifford were held in high regard as investment trust managers, but that patience was waning with the existing portfolio management team.

Following further formal review, the Board took the decision to appoint a different portfolio management team within Baillie Gifford. As a result, since 27 March 2015 Monks has been managed by Charles Plowden, supported by Spencer Adair and Malcolm MacColl: they are all members of Baillie Gifford’s ‘Global Alpha’ investment team, which has a well-established process and strong performance record. They are all Partners at Baillie Gifford and have been working together since 2005.

Charles is one of two joint senior partners. It is important to note that the Company’s investment policy and objective have not altered as a result of this change in portfolio responsibilities. The Company’s goal remains long-term capital growth, by investing globally and principally in equities.

Picking up the pace

Monks’ returns have certainly improved since Plowden took charge.

In the five years to April 2020, Monks’ net asset value was up 87% compared to 56% for global markets. On a share price basis, the increase was 113%, thanks to a fairly sizeable discount becoming a small premium.

But earlier this month the news came that Plowden is going to retire in April 2021, shortly after he turns 60.

Spencer Adair is due to step up to become the lead manager of Monks. Malcolm MacColl will remain the deputy manager but he will also become the joint senior partner at Baillie Gifford.

Adair joined Baillie Gifford in 2000 and has been a partner with the firm since 2013. He graduated with a BSc in Medicine in 1997 and spent two years in clinical training before changing careers, so he’s probably in his mid-40s.

MacColl graduated at roughly the same time as Adair and is therefore likely to be a similar age.

Investing style

Here’s the one-paragraph summary:

Monks Investment Trust aims for long-term capital growth which takes priority over income. This is pursued through applying a patient approach to investment, principally from a differentiated, actively managed global equity portfolio containing a diversified range of growth stocks.

The latest interim report fleshes this out a bit more:

There are always reasons to be fearful and to worry about what might go wrong: ‘but what about Brexit?’, ‘what about Trade Wars?’, ‘what about Politics?’.

Rather than attempt to predict the unpredictable, the managers’ approach focuses instead on the fundamental merits of companies. They believe that companies with enduring competitive advantages and skilled management teams are likely to deliver superior long-term (5 years or more) returns for investors.

Dramatic headlines and short-term equity market oscillations are of little importance to the managers. Instead they seek to understand long-term structural trends which provide opportunities for future growth.

For example, the managers observe growing opportunities which are fuelled by increasing computing power, an explosion of data and improving global connectivity. These factors are increasingly impacting companies across the healthcare, financial and enterprise sectors, in addition to the more familiar consumer applications.

That’s very much in tune with my investment philosophy of not trying to time the market. And I’m partial to the thematic approach, too.

The portfolio

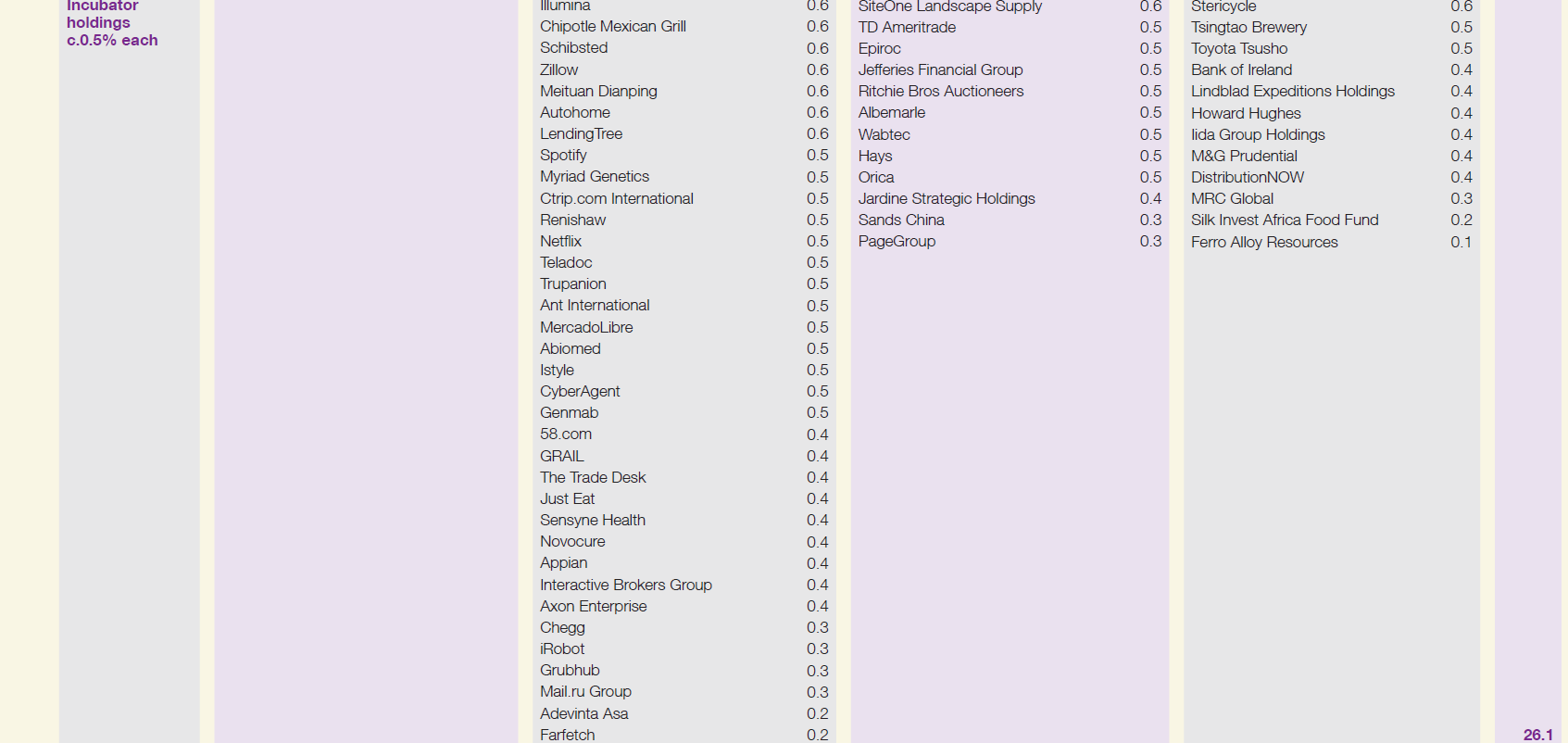

As of April 2020, Monks had around 120 listed holdings and 3 unlisted investments.

Direct unlisted investments account for just 1.1% of net assets, which is much lower than the likes of other Baillie Gifford funds such as Scottish Mortgage, Edinburgh Worldwide, and Baillie Gifford US Growth.

However, Monks also has a 2.3% position in Schiehallion, which exclusively invests in unquoted businesses. Its self-imposed limit on unquoted investments is 5% (whereas Scottish Mortgage is increasing its limit from 25% to 30%).

Monks’ largest position is Amazon.com (4.2%). The rest of its top ten includes the likes of Naspers, Alphabet, Alibaba, Microsoft, and Mastercard, all with position sizes of between 2 and 3%

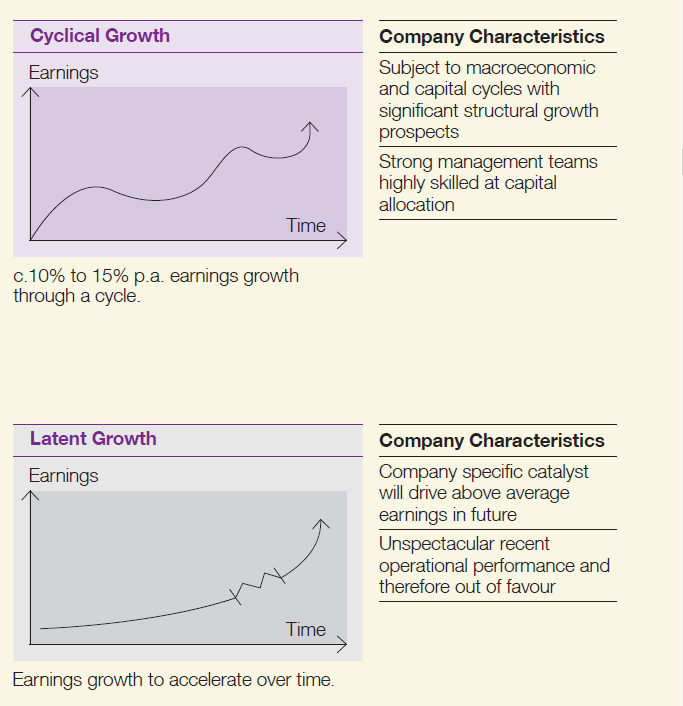

There are some good charts in Monks’ annual reports that illustrate how the portfolio breaks down into four groups.

And this is how that gets reflected in the portfolio, as of last October. You can click the images to enlarge them if necessary:

So, Rapid Growth and Growth Stalwarts are the main two categories, accounting for 70% of net assets. Rapid Growth is also the category with by far the most individual positions.

Geographically, North America is the biggest region at 49%. Europe and the UK account for 20% and there is 17% in emerging markets.

Sector-wise, Financials is the largest at 25%, followed by Consumer Services (19%), Technology (18%), and Healthcare (14%).

Annual portfolio turnover is relatively low, coming in at 16% in the most recent interim report.

Active share, a measure of how much its portfolio overlaps with its benchmark index, comes in at 87%. 0% would represent an index tracker and 100% would mean there is no overlap whatsoever.

By way of comparison, Fundsmith Equity has an active share of 90% and Scottish Mortgage 92%.

The overlap with Scottish Mortgage

Monks is sometimes considered to be a watered-down Scottish Mortgage and there is certainly some truth to that.

It’s more conservative in a number of ways, such as having slightly less gearing, half as many again individual positions, and nowhere near Scottish Mortgage’s 20% bet on unlisted investments.

Among their major holdings, there are nine companies that both trusts hold. The main ones are Amazon, Tesla, Illumina, Alphabet and Netflix.

In most cases, Monks has a far smaller position than Scottish Mortgage. For example, it has 1.2% in Tesla compared to the 11.3% held by Scottish Mortgage.

Together, these 9 jointly-held companies account for 16% of Monks’ portfolio and 43% of Scottish Mortgage’s.

There are a few other overlaps among the minor holdings that might drag these figures up to roughly 20% and 50% respectively.

Skin in the game

Monks has seven directors, most of whom own a decent number of shares.

Five of them own a collective £2.7m, with Professor Sir Nigel Shadbolt and Claire Boyle (only appointed on 1 May 2020) having no shares.

It’s worth noting that Douglas McDougall, the former manager of Monks who retired from the Board last September, had 1.4m shares worth approximately £13m at the time.

As with Scottish Mortgage, disappointingly there doesn’t seem to be any information on the shares held by Plowden, Adair, or MacColl.

Gearing, charges, and dividends

Monks sometimes had a small net cash position when it was run by Smith, but since Plowden’s team took charge it seems to have consistently been around the 6-7% level.

As with most of Baillie Gifford’s trusts, total charges are pretty reasonable at 0.5%. Although with £2bn+ in predominantly listed equities, I wouldn’t call it spectacularly cheap.

The annual management fee is 0.45% on the first £750 million of total assets, 0.33% on the next £1 billion of total assets and 0.30% on anything above that. There’s no performance fee.

As is often the case, the difference between the costs in Key Information Document and the standard ongoing charge figure is due to interest costs.

There’s little in the way of dividends here. The payout was cut from 3.95p (then a yield of less than 1%) to 1.5p after Plowden’s team rejigged the portfolio in 2015.

The dividend, now paid in one instalment, has since crept up to 1.85p. It is likely to be increased a little more when Monks reports its full-year results in June but the yield is just 0.2%.

Summing up

Since the 1990s began, Monks has been one of the top-performing global investment trusts, returning around 11% a year, similar to the likes of Mid Wynd and Bankers.

It’s been two to three percentage points a year ahead of world markets, depending on your choice of index. What’s more, it seems to have performed pretty consistently, with much the same lead in each of the last three decades.

Fund manager changes always make me a little twitchy, but they have to happen now and again.

I prefer to see a long-standing deputy step up when things have been going well, and that’s the case here. The broader success of Baillie Gifford adds some additional comfort that Monks can continue to prosper.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.