Manchester & London is an odd little thing. Majority-owned by the Sheppard family, it’s second only to Lindsell Train IT in the performance rankings of global trusts over the last five years.

It has achieved this by running a concentrated portfolio with particularly large positions in the likes of Amazon, Alphabet, Microsoft, and Alibaba. But it also uses options and it shorts baskets of low-quality shares.

The full story of Manchester & London goes back nearly five decades, though, and it’s a tale of both spectacular outperformance and underperformance.

Key Stats For Manchester & London

- Founded: 1971

- Listed: 1972-1982 and since 1997

- Ticker: MNL

- Manager: Mark Sheppard (aged 49)

- 10-year net asset return: 148%

- Benchmark used: MSCI UK Investable Market Index (similar to the FTSE 350)

- Current price: 571p

- Indicated spread: 562p – 580p (3.2%)

- Exchange market size: 750

- Results released: March (interim) and September (final)

- Market cap: £186m

- Net assets / premium: 605p/ 8.3% (as of 4 February)

- Costs: 0.8% OCF and 1.23% KID (KID includes the performance fee)

- Gearing: 25% (based on Leverage: Committed Basis)

- Current dividend and yield: 14p and 2.4%

- Dividends paid: February (final) and May (interim)

- Style: Global equities plus options and ETF baskets

- Links: Website and Morningstar

A little history

You might have noticed from the Key Stats section that Manchester & London has had two spells as a listed company.

Brian Sheppard, the father of current manager Mark Sheppard, co-founded the company in the early 1970s.

It spent a decade as a quoted entity before a complex series of deals in 1982 resulted in it giving up both its investment trust status and its stock market listing, and the Sheppard family acquiring a controlling interest of around 73%.

Manchester & London followed a very concentrated investment strategy over the next 15 years, often investing the vast majority of its portfolio in just a few shares. It was very successful during this period and its net assets rose from under £1m to £34m although it was often quite highly geared.

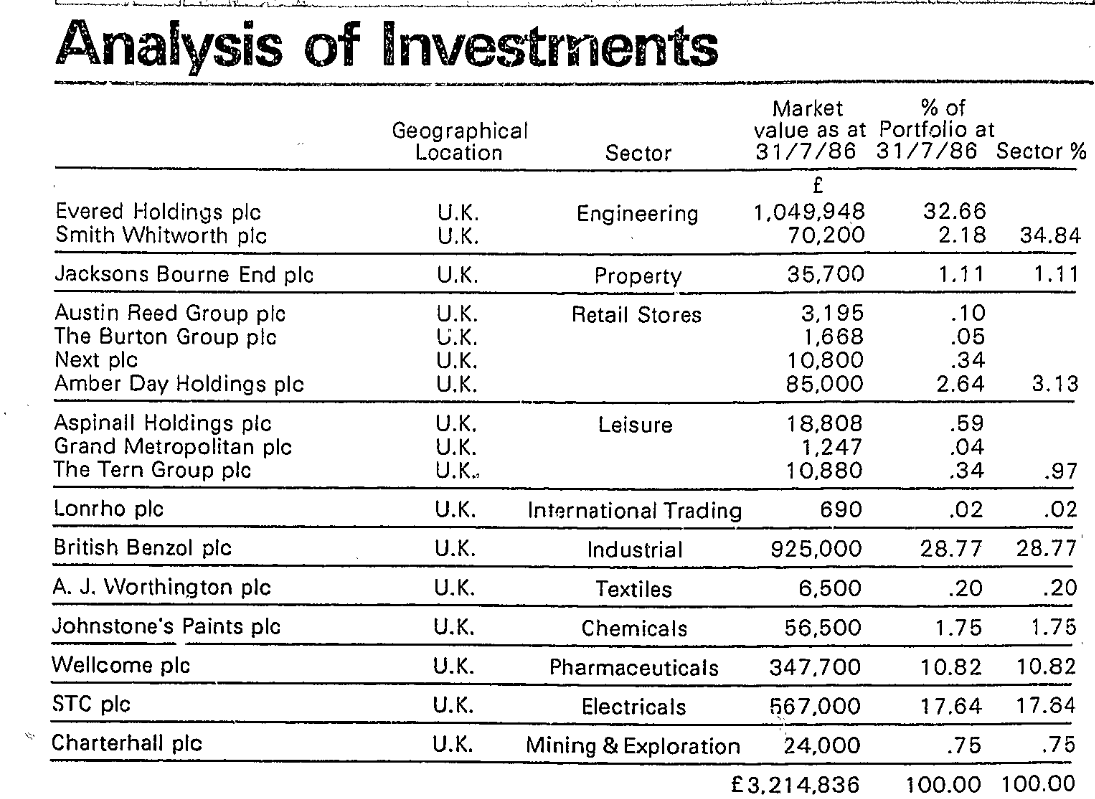

Here’s a copy of its 1986 portfolio, the earliest I could find. It shows 4 major holdings plus a sprinkling of minor positions:

Manchester & London rejoined the market in late 1997, with the Sheppards still having a controlling interest. They still own around 58% today, a stake worth just north of £100m, via an unlisted vehicle called M&M Investment Company.

The Sheppards regularly buy and sell shares in Manchester & London, presumably in order to ensure there is reasonable liquidity available. And just last week, Mark Sheppard subscribed for new shares worth £7.6m.

Brian Sheppard was Chairman until 1997 and remained as a director until 2013 when he retired at the age of 79. Lord Lee of Trafford, perhaps most famous as the first ISA millionaire, served on the board from 2000 to 2005.

Change at the top

It’s unclear to me exactly when Mark Sheppard took over as the main investment manager. Morningstar has him listed as “since 1997” but LinkedIn reckons he worked for other firms up until 2003.

Articles on Manchester & London are pretty thin on the ground, but a Questor tip from March 2017 says Sheppard was appointed about three years previously.

That would tie in with a fairly major shift in the trust’s investing strategy towards technology companies (more on this later), although I also found a piece from March 2013 where Mark Sheppard is lamenting shorting the S&P too early!

Regardless of when he took over, we do know that Sheppard is currently being assisted by Richard Morgan and Brett Miller, thanks to the trust’s somewhat cheesy website.

The trio also run a small open-ended fund called M&L Global Digital & Technology that was launched in 2016. Although this fund shares many positions with Manchester & London, it only has assets of around £6m.

And Sheppard previously ran a private wealth management business, but this was sold to Tilney in 2017.

Rollercoaster performance

I can’t find any data for the performance of Manchester & London during its first period as a listed company, but its second spell certainly didn’t start well.

After rejoining the London market in December 1997, its share price remained at much the same level, around 270p, for most of 1998 and 1999. So it largely missed out on the gains arising from the TMT bubble.

As of July 2000, the portfolio consisted of around 46% in BAE Systems warrants, 14% each in AEA Technology (the privatised Atomic Energy Authority), Pearson, and Andrew Sykes, plus 7% in TDG and 4% in PZ Cussons (then called Paterson Zochonis).

Nevertheless, Manchester & London still got caught in the early 2000s bear market, with its share price roughly halving to 140p by the end of 2002.

Then things picked up, with the share price climbing over £4 by 2006. PZ Cussons, Royal Dutch Shell, Mouchel Parkman, Gazprom, Standard Chartered, and Rank its then-largest holdings.

As you might expect, the financial crisis caused a brief hiccup, but the share price was back above £4 again by early 2011.

PZ Cussons was still the biggest holding at around 18%, but the portfolio now had a larger number of positions albeit with over a third of its net assets in energy and mining.

Global markets continued their recovery over the next few years but energy and mining stocks fell from favour. Manchester & London’s share price slid back to 225p by the end of 2014, with its stake in PZ Cussons now accounting for around 25% of assets.

Twisting towards technology

The interim report published in March 2015 revealed a major shift in thinking towards what Sheppard has since called ‘Long The Future’:

We believe that two key challenges have significantly altered the traditional equity valuation framework. Firstly, technology has rapidly disrupted many business models, turning what were once classic value plays into value traps.

Secondly, a global disinflationary environment has squeezed yields to the point where some high quality corporate debt issues have even gone into negative yield territory. This has a bullish read across for the equity of these “bond proxy” equities even though they may not appear inexpensive against traditional valuation metrics.

Both these factors have caused large valuation differentials, which may deepen further. However, for now, we are no longer tempted by these value plays.

We have repositioned in the opposite direction – moving overweight Technology, Healthcare and Consumer stocks (with bond proxy like cash flows).

PZ Cussons was reduced down to 12% (and disappeared completely soon afterwards), while positions of between 1% and 4% were opened in Apple, Google, Polar Capital Technology, Scottish Mortgage, Baidu, eBay, ARM, and a couple of 3D printing companies.

Come the 2016 annual report and Amazon, Alphabet, and Facebook accounted for 3 of the top 4 positions at around 5% each.

A year later and the plain-looking annual report had been jazzed up with a few stock technology images. The top 10 positions were now pretty much all tech-related — Amazon, Alphabet, and Facebook were up to 9%, with Microsoft, Tencent, and Alibaba not far behind.

Onto 2018 and the highly concentrated nature of Manchester & London’s past portfolios had returned. Amazon (20%), Alphabet (16%), Microsoft (15%), and Alibaba (13%) dominated, with Apple the next largest (5%).

I think the 2019 annual report, published last September, was the first to explicitly outline the strategy of shorting poor-quality stocks.

Some 9% of net assets were devoted to shorting baskets of stocks with undesirable traits — such as BBB Downgrade, Weak Pricing Power, Weak Balance Sheets, and Declining Margins.

On a less reassuring note, I also noticed that the 2019 annual report uses a long-term performance chart that starts in July 2002, pretty much the post-flotation low for the share price and excluding the poor performance from 1997 to 2002.

A terrific turnaround

From a low of around 225p in early 2015, when the new investing strategy was unveiled, Manchester & London’s share price has since risen to nearly £6.

The discount on the shares had widened from around 10% at the start of the 2010s to over 20% by 2016. But once the portfolio performance began to pick up, the discount narrowed quite quickly.

In fact, Manchester & London has sometimes even traded at a small premium in the last couple of years, although a single-figure discount has been the norm.

It’s worth noting that its net asset value is only updated weekly. Given the volatile nature of its main investments, the NAV figure can date rather quickly when the market gets a bit excitable.

The trust seems to be getting a bit more press attention now its five-year performance looks more eye-catching.

James Carthew featured Manchester & London in his Citywire column a few months ago and earlier this month it made an appearance in the weekly Z-list of cheap trusts after its discount rose to 8%.

However, it doesn’t seem to get paid research from Kepler, Edison, or Quoted Data and is not a member of the AIC.

The current portfolio

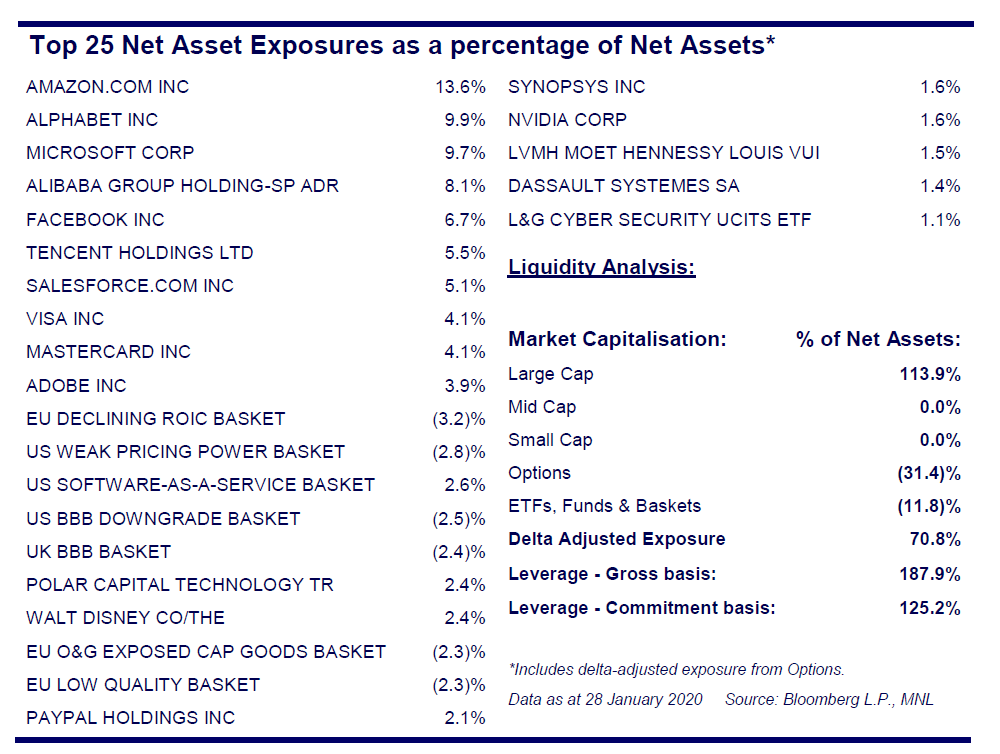

The latest factsheet suggests its portfolio has become marginally less top-heavy. But the top 5 positions still account for 48% of net assets:

Not being much of a trader, I must say I find this table a little tough to follow. There’s no explanation on how the options position is made up, and the delta and leverage figures could benefit from some added detail.

There doesn’t seem to be a factsheet archive on the trust’s website, so I’m not clear how this liquidity profile has changed recently. There is a note on derivatives in the last set of annual accounts, but the net position seems a lot smaller.

Polar Capital Technology seems to be the only major remaining trust holding. Worldwide Healthcare Trust and Pacific Horizon were holdings in recent years, while Scottish Mortgage was sold in October 2019 over concerns that its high level of unquoted positions might restrict its ability to invest in other opportunities.

Dividends

Manchester & London’s yield is a little higher than you might expect given the make-up of its portfolio.

The payout was cut from 13.75p in 2014 to 6p in 2015, following the strategic shift away from higher-yielding positions. But it’s since climbed back up to 14p.

Special dividends of varying amounts were paid from 2014 through to 2017, but the trust seems to have reverted to a more usual interim/final split in the past two years.

Charges

The basic management fee is 0.5% of net assets.

A performance fee was introduced in May 2018, with an additional 0.25% being payable should the trust beat its benchmark over the previous 36 months.

This took total expenses to £1.5m for the last financial year, with an additional £1.1m in finance costs.

For a fund with £200m in assets, that doesn’t look too outrageous although a few other self-managed trusts are considerably cheaper.

The performance fee seems rather generous, though, given the benchmark is basically the UK market and the fund is almost entirely invested in the US.

Summing up

I found Manchester & London fascinating to look at. Part of the reason for that is I have a sneaky feeling that I briefly worked in the same office as Mark Sheppard a very long time ago.

You certainly can’t fault this trust’s performance in the last five years. Although Manchester & London was a little later than most in jumping on the technology bandwagon, it’s stayed the course and reaped the rewards.

It’s sometimes described as a Scottish Mortgage wannabe, but its style seems more akin to a fund like Polar Capital Technology that mostly sticks with the largest tech companies.

Indeed, in its latest AGM presentation, its performance is compared to Polar Capital Technology, Scottish Mortgage, Fundsmith, and Lindsell Train Investment Trust, so it certainly sees itself as belonging in exalted company.

This has been a volatile fund in the past, relative to the wider market, and it’s hard to see that changing anytime soon given the very concentrated nature of its portfolio and the type of companies it holds.

I still find the options/leverage figures it gives confusing, being a little unfamiliar with the technical terms involved. So I’m not really clear what the true level of gearing is here, relative to other similar funds, and what additional risks this method of financing might be adding.

A prolonged downturn in technology stocks, which will occur at some point, would actually be quite useful in that regard. Not only might it provide a decent entry point, but it should also shed light on how risky this trust actually is.

Complexity is usually a bit of a turn-off for me, but the large stake held by the Sheppard family does provide some reassurance on this front. That said, while most family-owned investment trusts take a pretty cautious approach (such as RIT, Caledonia, Hansa etc), Manchester & London does seem to be at the other end of the scale.

I might keep an eye on this trust to see how it develops from here. Given his relatively young age compared to most managers, Sheppard looks like he might be around for a little while.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Article re Manchester & London.

Highly appreciate the interest. Great article.

But why do we not meet up in Q2 to go through the points you need clarification on. For example, in reality there were 3 eras not 2.

Mark Sheppard.

Many thanks for the offer Mark – very kind of you. Will be in touch.

A very insightful and detailed article. I am invested in Manchester & London so I’d be interested to read your thoughts after your meeting with Mark.

Kepler has just published a reserarch note on M&L for those interested in finding out more about this trust…

https://www.trustintelligence.co.uk/investor/articles/manchester-london-retail-may-2020