Applications are now open for Smithson Investment Trust, the keenly anticipated new offering from Terry Smith’s Fundsmith. No doubt many people will be happy to take the plunge purely on the basis of the great run the Fundsmith Equity Fund has had. But here are a few things that I think are worth knowing before you make any decision.

1. Smithson is going to be extremely popular, so expect to be scaled back

Smithson Investment Trust is expected to raise £250m, making it just 1.5% the size of the £17bn Fundsmith Equity Fund. Given the number of satisfied investors the latter has and that the pitch for this new fund is basically “it’s just like Fundsmith, but the returns could be even more spectacular”, it’s hard to see anything but massive demand for this launch.

So, just how high might it be? I’m not sure if the figure will be published, but I wouldn’t be surprised to see demand top £500m. Could it even go as high as £750m?

The Prospectus tells us that the company could issue as many as 35 million shares if there is excess demand. With the initial share price set at £10, this would mean £350m could be absorbed. Therefore, you need to be prepared not to get the full amount you apply for.

Fundsmith says it will scale back applications at its discretion. Perhaps it will favour Fundsmith account holders? Typically, larger applications tend to be scaled back most. Smaller applications are often satisfied in full, but you can’t assume that will happen. It’s also entirely possible that Fundsmith could decide to close the launch early, should there be plenty of early applications.

Some folks try to game the system by applying for more than they want, in the expectation of being scaled back. That’s a dangerous tactic of course, and hardly cricket either.

(Update: on 9th October, Smithson said the issue size would be raised to £600m. So, I think this probably means there will be no scaling back)

2. It’s probably going to trade at a premium

The popularity of Fundsmith and the likely excess demand means that Smithson Investment Trust is likely to trade at a premium to its net asset value for a while.

The history of Fundsmith Emerging Equities gives an indication of what might happen. It traded at a premium of 7-8% for a year or so after its launch. It even exceeded 11% on occasion. The premium slipped a little after that, as its early performance failed to impress, but it’s rarely traded at a discount.

This means that if you’re looking to take an initial stake at launch and then add to your position later, you might have to pay a little extra.

3. You should definitely read the Smithson Owner’s Manual

There’s a lot of documentation with any fund launch or company IPO. Fundsmith produces an Owner’s Manual for all their funds, which is a great summary of how the fund is run and what you should expect. It’s only 16 pages. I’ll wait here while you read through it…

The same page I’ve linked above on the Smithson website also has a good presentation from the institutional roadshow. It runs to 31 pages and has a lot of information on the investable universe from which the portfolio will be picked. I’ve reproduced a lot of the most useful pages later in this article.

The Prospectus is much heavier going and comes in at 184 pages. But there are some useful snippets in there if there is a particular point of detail that you are interested in. Or if you want to write a blog post about the company!

Then there is the Key Information Document (KID). These have a section on potential performance (which is usually just pure speculation so it’s pretty much useless) and on costs (much more insightful).

4. The charges seem pretty fair overall

Talking of costs, Smithson Investment Trust is unusual as Fundsmith will absorb all the launch costs itself. These are typically 2-3%, so it’s a pretty big commitment. And it grabs a few favourable headlines of course.

There are ongoing costs, which Smithson estimates will be £2.7m if £250m is raised as planned. That’s 1.1% a year, and is mostly made up of the 0.9% management fee.

The KID tells us there could be an additional o.15% a year of transaction costs for buying and selling the underlying investments. So, the total costs anyone investing bears should be 1.25% a year.

I’d like lower charges of course, but these don’t seem too unreasonable, especially given the zero launch charge. However, from what I’ve read, it doesn’t look like the management fee percentage will reduce as the fund grows. That’s a shame, but Fundsmith has taken this approach with its main fund.

5. What’s in the Smithson investable universe

Fundsmith uses the same basic strategy with each of its funds. It creates a shortlist of companies that meet certain criteria: high gross profit margins, high return on capital employed (ROCE), high conversion of profits into cash etc. This is its investable universe, and it contains 83 companies for Smithson Investment Trust.

The portfolio is then selected from the investable universe. The names typically change over time, but not that much as far as I can tell.

I don’t think there is a full list of the 83 anywhere, but we now know a lot of their names. Here’s a selection:

Most of these are fairly well-established businesses, although Fever-tree stands out as one of the youngest. There are a fair few recognisable brand names in there, too.

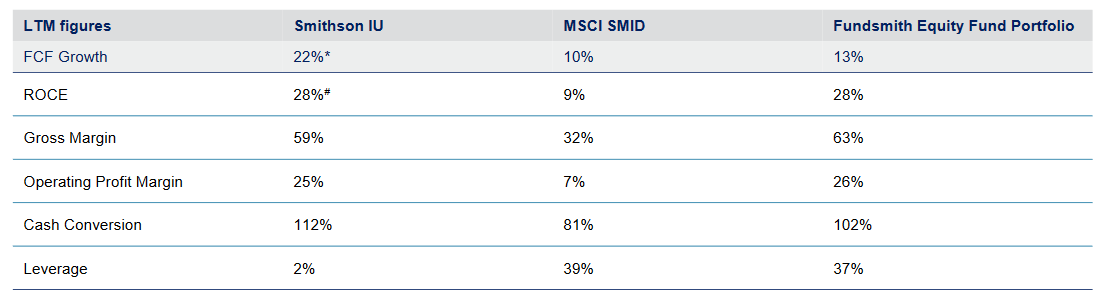

Here’s how the investable universe compares on a number of key financial metrics. LTM stands for the last twelve months by the way.

So Smithson companies look pretty similar to those invested in by Fundsmith Equity. They have been growing a lot more quickly recently, but I’d expect that gap to be a little narrower over longer periods. Interestingly, they seem to have much less in the way of debt. Perhaps that’s because many larger companies are encouraged to borrow to juice their returns a little.

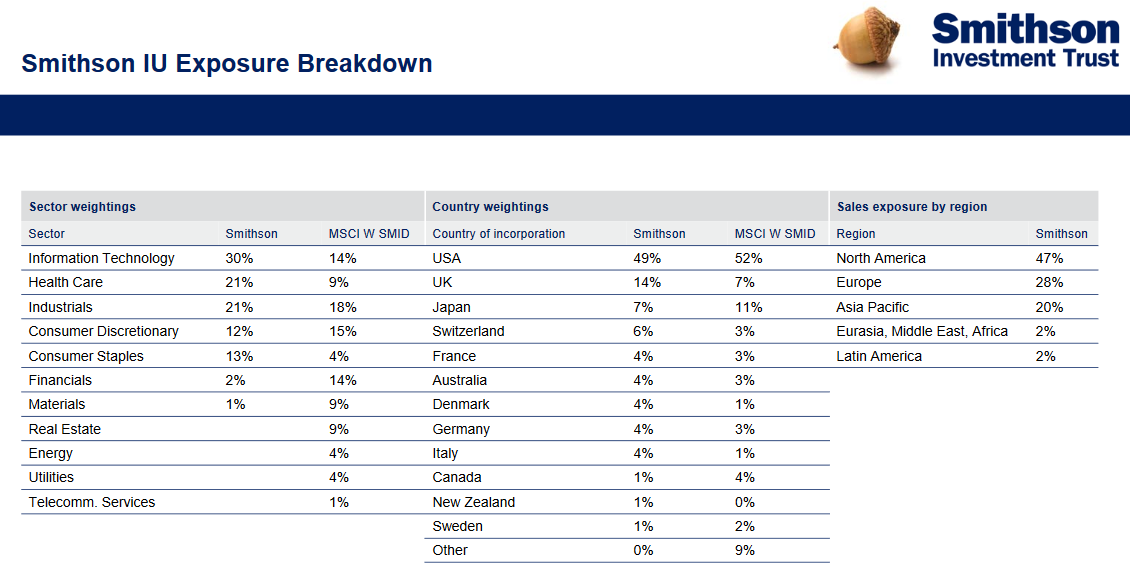

Last of all in this image-laden section, here is how the investable universe breaks down on a sector and country basis.

What’s not included in probably most relevant here. Cyclical sectors like banking and financial services, mining, energy and property are off the menu. Regulated utilities are also not wanted.

There’s a heavy US weighting as you would expect. The UK punches above its weight, as does much of Europe. Japan and Canada are heavy with unfavoured sectors. I suspect most of Other is China.

6. There’s a fair overlap with Fundsmith Equity

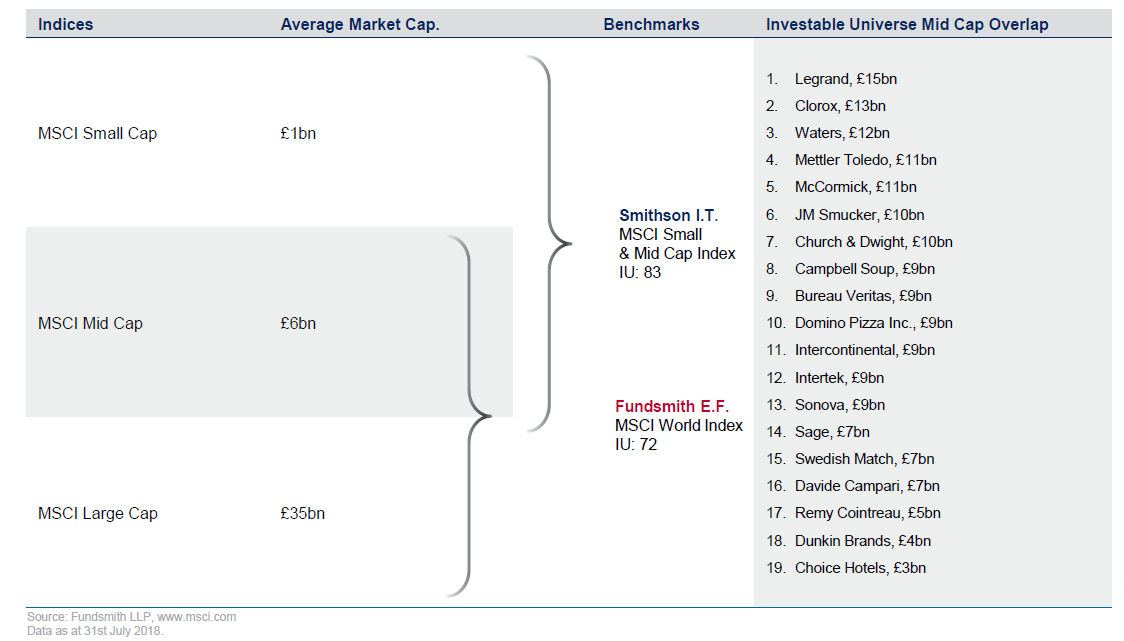

One thing I hadn’t appreciated was that the investable universe has a fair bit of overlap with the main Fundsmith Equity Fund. In fact, 19 of the 83 companies are shared between the two funds, so that’s nearly a quarter.

Perhaps I shouldn’t have been too surprised, as the companies Smithson is looking at range from £500m to £15bn whereas Fundsmith looks to start at £3bn.

I don’t think this is too much of an issue. Smithson’s smaller size means that it should be able to take a more meaningful position in these overlaps. If Fundsmith wants to take a 3% weighting it would need to invest £500m, which would certainly move the share price in many of these companies.

7. Terry Smith isn’t running Smithson, but he is investing in it

Smithson Investment Trust will be run by two whippersnappers that recently joined Fundsmith from Goldman Sachs.

Simon Barnard (14 years) and Will Morgan (17) spent their entire pre-Funsmith careers with Goldman. Of the many people that approach Fundsmith for jobs, they stood out as they both had their entire liquids net worths in the Fundsmith Equity Fund. This obviously appealed to Terry Smith, although it does raise the question about whether they should know a little more about diversification!

Barnard and Morgan seem to be avoiding the limelight so far, but hopefully, we’ll hear a little more from them soon. They will be assisted in their research efforts by Jonathan Imlah, a technology specialist. It’s worth noting that the two managers don’t get much of a mention in the prospectus. They are first introduced on page 43 and then get a one paragraph career summary some ten pages later. I was hoping for rather more than that!

It’s unclear how much Terry Smith will be involved, but Fundsmith seems to a very tightly knit organisation. Smith, a fit-looking 65 years of age, looks like he will be the driving force for many years to come. And I suspect little gets past him for long.

Smith will be personally investing £25m in Smithson Investment Trust, with other Fundsmith employees buying £5m. Some may see this as a show of faith. From a purely selfish point of view, I wish he wasn’t taking such a large chunk of the available shares!

8. Key dates to be aware of

There should be a few weeks to think about this one. If you are applying directly then you have until 1 pm on Friday 12 October to submit your paperwork. However, as I mentioned earlier, it’s not unheard of for new issues to close early if there is plenty of demand, although you normally get a little warning that this is going to happen.

If you go through a broker, then you might find that they set a slightly earlier deadline, but most of them are pretty good at making this clear.

Those investing should find out their allocation on Wednesday 17 October.

The shares start trading at 8 am on Friday 19 October and the ticker will be SSON. They should appear in online broker accounts pretty much straight away, but it might take up to two weeks for share certificates to be sent out.

9. Don’t expect much in the way of dividends

You don’t invest in Fundsmith funds for income. Indeed, Terry Smith is pretty disparaging of those who look for a high payout rate from their investments. He insists total return is more important, and that people can always sell a chunk of their holdings if necessary.

Smithson will tread the same path, unsurprisingly. It’s investing in high-growth companies, and you would both expect and want them to be reinvesting in their own businesses rather than paying out dividends.

There may be a token dividend from Smithson, but I would be astonished if the yield was north of 1%.

10. It might offer a little downside protection

Rude though it seeems, shares don’t always go up. When they do fall, we want the ones we hold to fare better than most.

In my initial article on Smithson Investment Trust a couple of weeks ago, I warned about the dangers of relying too much on performance backtests. However, one thing that has caught my eye was how resilient Smithson companies have been in the last two major bear markets.

We should be ready with a pinch of salt, as it’s difficult to know which companies would have actually been in the investable universe during these two periods. Some of the 83 did not exist or would have been too small. Others might not have qualified based on their financial performance at the time.

That being said, the current crop of companies under consideration seems to have held up fairly respectably. That might be because they don’t have much in the way of debt and Fundsmith tends to avoid cyclical companies. On the flipside, you would generally expect them to be fairly highly priced, and such stocks often fall further when sentiment turns.

I’m still planning to invest in this one, and promise not to mention anything to do with Fundsmith for at least the next week.

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!