Smithson Investment Trust (SSON) released an interim report this morning, giving us a decent look at what’s been happening in four and a half months since it joined the market. There was little in the way of surprises and it looks like everything is proceeding to plan.

[Update: for my thoughts on Smithson’s interim results released on 13 August 2019, click here]

I bought in at the IPO and topped up a few weeks later. It’s one of my smallest positions right now. However, I am intending to add a little more over the course of this year.

You can read the full statement here but let’s pull out a few items.

Smithson’s performance to date

You’ll probably recall that Smithson launched into a pretty choppy market last October.

And the performance stats from 19 October to 31 December bear witness to this. The net asset value fell 5.8% to 942.2p in those first two and a bit months.

However, that was slightly better than the MSCI World SMID index. This tracks global small and mid-cap stocks and Smithson is using it as its benchmark. It fell by 8.3%.

There’s very little that can be read into any performance data over such a short timescale. The only thing that would be a concern would be if Smithson had underperformed its benchmark significantly, but that hasn’t happened.

The performance since the end of 2018 has been pretty spectacular. Global markets have bounced back a lot, but Smithson’s net asset value soared to 1,078.8p as of 1 March. Therefore the net asset value is up nearly 8% since launch and 14.5% in the first two months of 2019.

I couldn’t find a figure for the MSCI World SMID for the year to date. But the FTSE Global Small-Cap index is up 11% in sterling terms. So, it seems likely that Smithson has increased its lead against its benchmark in 2019.

Again, it’s far too short a time period to draw any conclusions other than so far, so good, so keep it up.

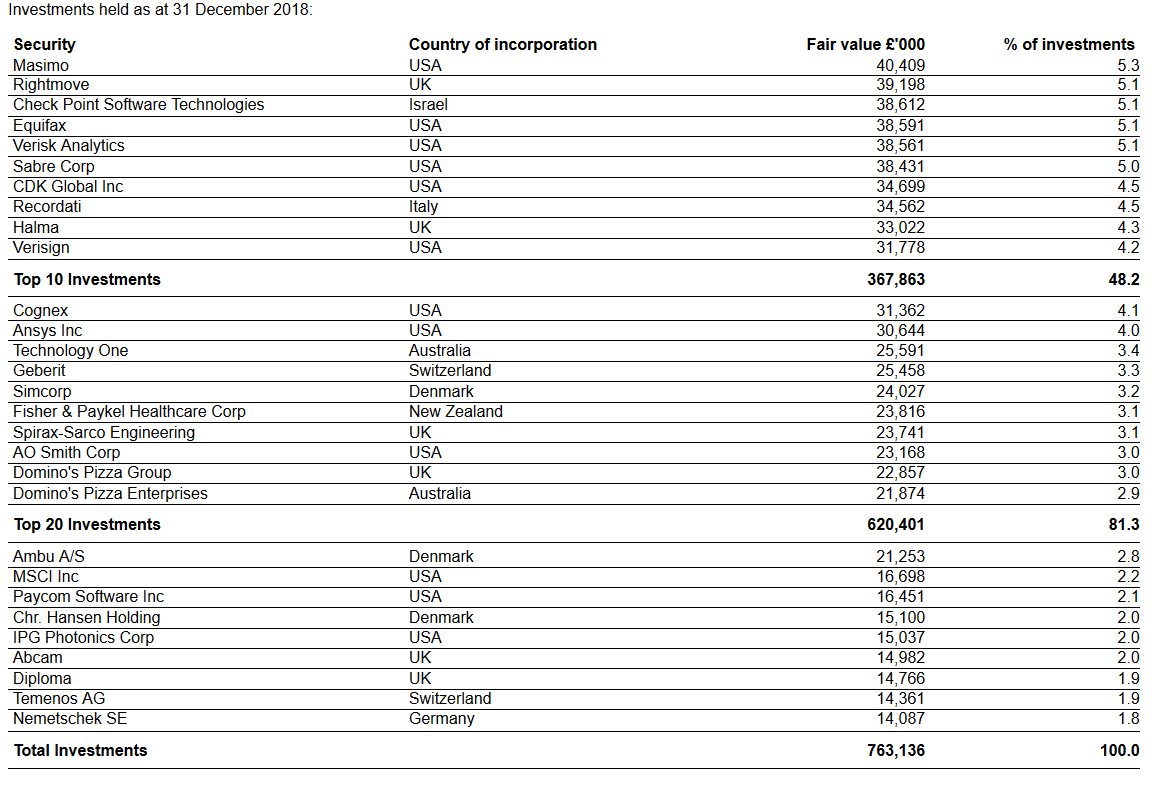

The full list of holdings

We’ve had the top 10 holdings published in monthly factsheets. This interim report revealed full details about the 29 stocks bought so far:

A lot of these names were revealed in the pre-listing presentations but it’s good to see the line-up in full.

With position sizes ranging from just under 2% to just over 5%, it would seem pretty well balanced. Every position is big enough to matter but not so big as to be a cause for concern.

It’s not been plain sailing for all these companies in the past few months. Both Domino’s companies appear to be having somewhat fractious relations with their franchisees at the moment. Equifax’s growth has disappointed and CDK has had to fire its CEO.

Abcam, one of the smallest positions, dropped nearly 20% on poorly received results just this morning. However, it’s recovered to just 10% down at the time of typing.

Even in a portfolio of just 29 companies, you would expect to see several struggling at any one time. So, nothing about this alarms me particularly. It’s good to see equal weight being given in the commentary to both good and bad performers.

I suspect the portfolio has changed very little since the end of 2018. The Smithson/Fundsmith strategy is largely to let these companies do their thing over a period of several years.

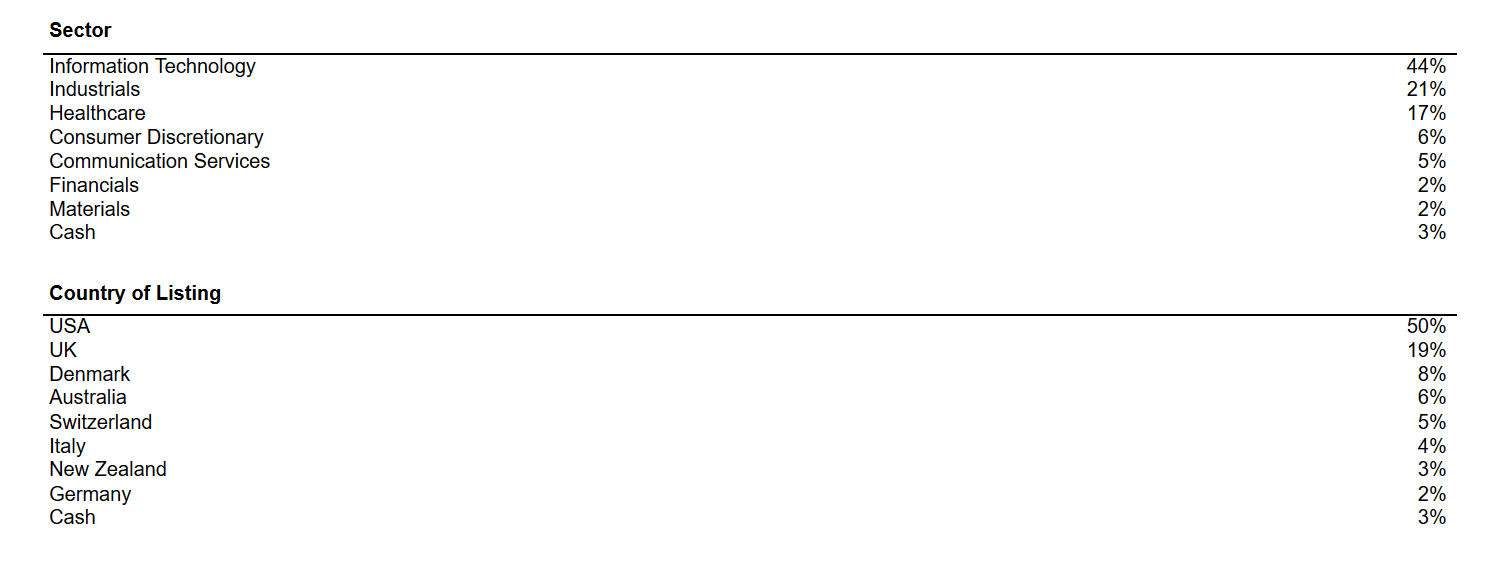

Too much tech?

One concern some investors have mentioned is the heavy technology weighting revealed in the first monthly factsheet. Here’s how the portfolio looked on a sector and country weighting at the end of 2018:

Smithson reckons the large IT weighting is a little misleading, though. Many of its holdings are software companies serving a wide variety of industries, meaning the sector classification is a bit subjective.

I’d tend to agree with that. But a high technology weighting wouldn’t really alarm me either, as I don’t have much specific tech exposure elsewhere across my portfolio.

Likewise, the high weightings for the US and the UK are ok with me.

Smithson included some data on the source of revenue rather than the country the company happens to be listed in. This looks more evenly spread, with the US at 39%, Europe at 36% and Asia Pacific at 18%.

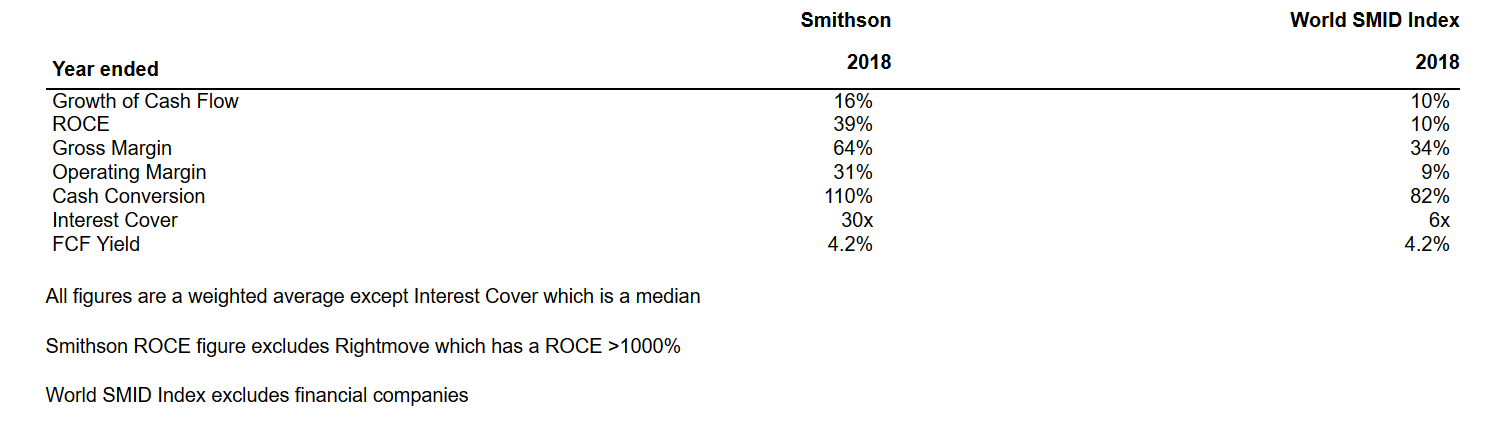

Feel the quality

Fundsmith likes to compare its investments across the wider market on a number of key metrics. Smithson is doing the same thing:

As you would expect, the portfolio looks healthy on all these measures. However, it’s good to see that the FCF Yield (free cash flow yield) is the same for both the portfolio companies and the wider market.

In other words, the companies in the portfolio don’t seem to be more expensive, despite looking more attractive on other metrics.

Too big for its boots already?

One concern is that Smithson might become too large, too quickly.

It was set up because Fundsmith Equity had grown too big to invest in some companies. Smithson’s target range is companies valued at £500m to £15bn, although it expects the average to be £7bn.

Smithson began life with 82.25m shares, valuing the company initially at £823m. However, the original plan was to raise just £250m.

As Smithson has generally traded at a premium since launch, it’s taken advantage of this by issuing lots of additional shares.

It now has 89.1m, so that’s an increase of more than 8% since it floated. It makes the market cap £989m at the current share price of 1,110p. Put another way, it’s now four times the size it was initially intended to be.

If Smithson wanted to take a 5% position in a company, it would now need to buy a stake of around £50m. That would represent 10% of a £500m company. That’s hard to do without affecting the share price. And hard to get out of should something go wrong.

So is the bottom end of Smithson’s investable universe already beginning to shrink?

Under the placing programme set out in the Prospectus, the number of shares could increase further to 105m, which would increase the size of the trust to almost £1.2bn,

I regard this as something to keep an eye on rather than a major worry right now. Looking at its UK investments, Domino’s at £1.1bn and Diploma at £1.5bn are the smallest, so there’s a little breathing space there.

What’s more, the IPO proceeds were pretty much all invested in 24 days, suggesting liquidity wasn’t a problem when the initial positions were built up.

A tiny dividend on the way?

I wasn’t expecting much of a dividend from Smithson and it looks like any payout will be pretty minimal. They are some basic numbers in this report that we can extrapolate to make a very rough estimate.

The dividend income in the first two a bit months (£2.5m) suggests an underlying yield of about 1.6% from the companies in the portfolio.

Costs come off this number, leaving an underlying revenue per share of about 3p-4p on an annualised basis.

Investment trust rules dictate that at least 85% of net income should be paid out to investors, meaning the full-year dividend could be 2.5p-3.5p.

That’s a tiny yield of 0.25% to 0.35%. Don’t spend it all at once!

What comes next?

I suspect we’ll get confirmation of a small annual payout when the first set of full-year results are released in February 2020.

That should be followed by the company’s first AGM in March 2020, where presumably we’ll get to see the two fund managers give a formal presentation and answer questions. It will be interesting to see how much of a presence Terry Smith has at this event.

Before all that, in late July 2019 or early August 2019, we should get half-year results. I wouldn’t expect those to contain a lot more detail than we got today.

All told, I thought this was a pretty encouraging update. All the right sort of things seem to be said and I expect to hold Smithson for a long time to come.

Encouragingly, the premium over net assets seems to have eased in recent weeks. It hit 12.4% in December but now seems more settled at between 3-5%, making a little top-up more appealing.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Hmm, arguably a safer bet now than when it was under the cosh in December, given the discount has closed so dramatically.

Of course safer is all relative. 🙂

For stock pickers like me it’s tempting to use the Smithson holdings as a watch list. (Must investigate Abcam!)

You wouldn’t top-up when it’s at a double-digit premium, would you? 🙂 I know LTI fans have done so repeatedly with great success, but of course that holds a certain fast-growing unlisted fund manager… 😉

Nah, a double-digit premium for a straightforward equity investment trust would make me a little queasy I think 🙂