Smithson’s shares are up more than 50% since it floated in October 2018 and its share count has risen 52%. It’s now approaching £2bn in market cap and it’s already become one of the 20 largest UK investment trusts.

Last time I looked at Smithson, we were a couple of weeks shy of the lockdown here in the UK.

Its shares had been at an all-time high of 1,388p just a few weeks previously, up nearly 40% from their issue price.

But then markets fell substantially in the second half of February as the full impact of the coronavirus started to become apparent.

After a brief recovery, Smithson’s share price plunged 30% in just two weeks in early March. The usual premium of a few per cent turned into a 20% discount and the share price even touched 890p for a brief moment.

The recovery was equally dramatic. A new all-time high was posted just eight weeks after the sub-£9 low. By early July the shares had crossed the £15 barrier for the first time.

Key stats for Smithson Investment Trust

- Listed: 19 October 2018 at 1,000p

- Managers: Simon Barnard and Will Morgan — overseen by Terry Smith

- Ticker: SSON

- Benchmark: MSCI World Small and Mid-Cap Index (SMID) in £

- Recent price: 1,514p

- Indicated spread: 1,511p-1,517p (0.6%)

- Market cap: £1.89bn

- Premium to net assets: 3% as of 28 Jul 2020

- Costs: 1.0% OCF, 1.05% KID

- Cash/debt: 1.9% net cash as of 30 Jun 2020

- Dividend: Zippo

- Results released: Mar (finals) and Jul/Aug (interims)

- Sector: Global smaller companies (3rd out of 5 over 1 year)

- Links: Website and AIC page

An impressive 2020

Smithson has just released its interim results for the half-year to 30 June.

Its net asset value return was +15.3% even though its benchmark global small- and mid-cap index fell 4.7%.

In share price terms, it rose 13.3% with a 3.4% premium at the start of the period shrinking to 1.5% at the end.

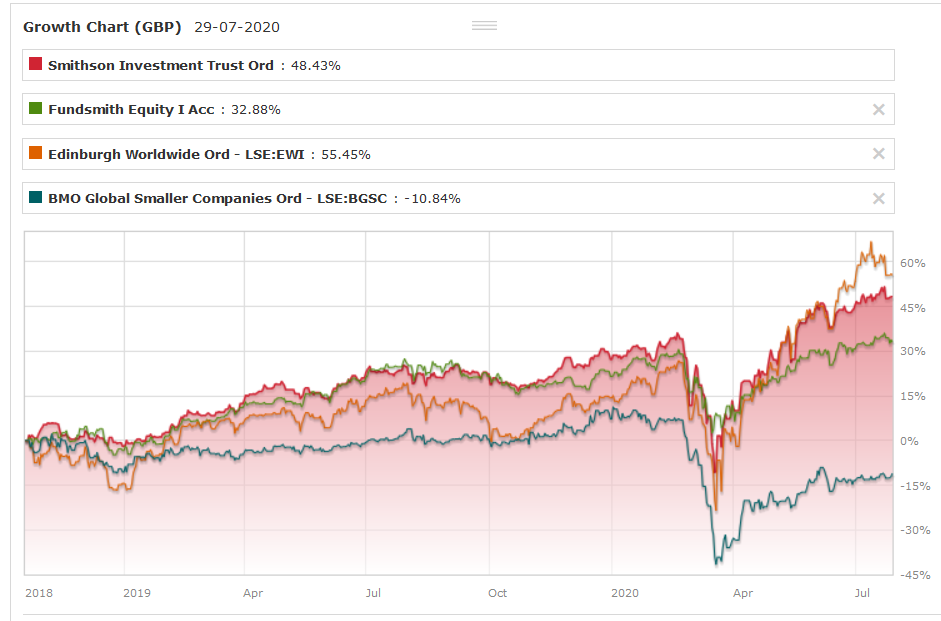

Since inception, its NAV was +44.8% versus its benchmark’s +6.6%. The shares were up 47% and have crept a little higher since.

That’s very impressive, although its performance year-to-date ranks 20 out of 299 ‘mainstream’ investment trusts covered by Trustnet.

Trusts like Pacific Horizon (+55%), Scottish Mortgage (+52%), and Baillie Gifford US Growth (+50%), all run by Baillie Gifford, have turned in far better numbers.

Allianz Tech (+40%) and Biotech Growth (+35%) have also been star performers while Edinburgh Worldwide, which is also classed as Global Smaller Companies and is yet another Baillie Gifford trust, is up 36%.

Pulling ahead of Fundsmith Equity

After closing tracking the main Fundsmith Equity fund for its first 18 months or so of existence, Smithson has now opened up a bit of a lead.

This chart also shows that although Edinburgh Worldwide has had the better 2020, it’s only marginally ahead since Smithson was formed in October 2018.

I’ve also added in the BMO Global Smaller Companies trust. It’s been around since 1889, has a market cap of £700m, and has a pretty decent long-term track record. But it has struggled to make any headway since the start of 2017.

Turning up the trading

I suspect one reason Smithson has edged ahead of Fundsmith is that it’s traded more actively in 2020, as far as I am aware anyway.

Here’s some commentary from its half-year results:

During the stock market decline, as often happens in a bear market, there were short periods in which the market behaved slightly differently, and it therefore elicited different behaviour from us. Initially, there was blind panic in the market, when the share prices of almost all companies fell. During this period we purchased more shares of companies like Verisign, which manages and protects the dot com domain of the internet, Ansys which designs simulation software and Recordati which produces medications for rare diseases, which we thought were declining for no rational reason as they were unlikely to be affected by the crisis.

This was followed by a period when more logic prevailed, with those companies likely to suffer acutely from the crisis, such as travel and leisure, continuing to fall precipitously, while those likely to be less affected, or even benefit, stopped falling and even started increasing in price. It was during this period that we began selling shares for the first time since our sale of CDK Global in September 2019. This included some shares of several of our healthcare companies, such as Ambu, Fisher & Paykel Healthcare and Masimo, which had grown to position sizes in the portfolio which their increasing valuations no longer warranted.

At the same time, several of our more economically sensitive companies had fallen to levels that made them extremely attractive as long-term holdings, and we had little fear regarding their near-term survival given the large amount of cash they had available to them. The proceeds of the healthcare company share sales were therefore reinvested into these companies, among others.

Smithson said its portfolio turnover in the first half of 2020 was 20%, already well ahead of the 6% recorded for the whole of 2019.

It was good to see this didn’t result in a large increase in transaction costs, which Smithson said were just 0.02% of its net asset value (about £0.4m).

How Smithson’s portfolio has changed

You can see the effect of the trading done earlier in 2020 in this table listing Smithson’s holdings.

It shows how little many of its position sizes have changed despite a fairly wide range of individual returns.

| Holding | Jun 2020 | Dec 2019 | Dec 2018 |

|---|---|---|---|

| Fever-Tree Drinks | 6.0 | 3.9 | – |

| Verisk Analytics | 4.6 | 5.0 | 5.1 |

| Rightmove | 4.5 | 5.5 | 5.1 |

| Equifax | 4.4 | 4.9 | 5.1 |

| ANSYS | 4.4 | 4.8 | 4.0 |

| Masimo | 4.3 | 4.9 | 5.3 |

| Cognex | 4.3 | 3.5 | 4.1 |

| Domino’s Pizza Enterprises | 4.1 | 3.3 | 2.9 |

| IPG Photonics | 4.1 | 3.6 | 2.0 |

| Recordati | 4.1 | 3.9 | 4.5 |

| Domino’s Pizza Group | 3.6 | 4.2 | 3.0 |

| Halma | 3.4 | 3.9 | 4.3 |

| Verisign | 3.3 | 2.8 | 4.2 |

| Sabre | 3.3 | 4.9 | 5.0 |

| AO Smith | 3.1 | 3.0 | 3.0 |

| SimCorp | 3.1 | 3.5 | 3.2 |

| Geberit | 3.1 | 3.1 | 3.3 |

| MSCI | 3.1 | 2.8 | 2.2 |

| Qualys | 2.9 | – | – |

| Rational | 2.8 | – | – |

| Paycom Software | 2.7 | 2.4 | 2.1 |

| Check Point Software | 2.6 | 4.8 | 5.1 |

| Temenos | 2.6 | 2.5 | 1.9 |

| Fisher & Paykel | 2.6 | 3.4 | 3.1 |

| Technology One | 2.4 | 2.8 | 3.4 |

| Spirax-Sarco | 2.2 | 2.4 | 3.1 |

| Nemetschek | 2.0 | 1.8 | 1.8 |

| Ambu | 1.9 | 2.9 | 2.8 |

| Diploma | 1.8 | 2.5 | 1.9 |

| Chr. Hansen | 1.5 | 1.4 | 2.0 |

| Abcam | 1.2 | 1.6 | 2.0 |

| CDK Global | – | – | 4.5 |

CDK Global remains the only share to be sold in its entirety by Smithson, with Fever-Tree, Qualsys, and Rational the only additions.

Rational is a German producer of automated professional ovens for restaurants and mass catering venues. Its latest product, the ‘SelfCookingCenter’, recognises the size, shape and consistency of the food and can control the cooking process to achieve the desired result programmed by the chef.

US-based Qualys is a security software company, providing identification, security and vulnerability management across all remote devices attached to a corporate network.

Fever-Tree makes bubbly drinks. Tasty ones, though.

Top and bottom performers

Smithson’s top three contributors in the half-year were, unsurprisingly, all healthcare-related.

Ambu contributed 2.8% despite only being a 2.9% position at the start of the year.

Fisher & Paykel contributed 1.5% (from an initial 3.4%) while Masimo chipped in with 2.5% (from 4.9%).

All three of these ended the period with smaller position sizes than they started, as their position sizes were trimmed.

Domino’s Pizza Enterprises, the franchisee firm for Australia, New Zealand, Belgium, France, The Netherlands, Germany, Denmark Luxembourg, and Japan, was responsible for 1.3%. Its share price is up around 40% year-to-date as it was able to keep many of its stores open.

On the downside, Sabre, the travel software company, was by far the biggest detractor at 3.0%.

Four UK-based companies rounded out the worst five performers, namely Rightmove (-0.9%), Diploma (-0.4%), Domino’s Pizza Group (-0.1%), and Abcam (0.0%).

Given how far the UK market has lagged behind this year, that’s not a great shock.

But to have only four companies out of 31 holdings to have contributed negative returns during the first half of 2020 looks like a pretty strong vote of confidence for the quality and durability of Smithson’s portfolio.

Will Smithson ever gear up?

Smithson seems to have had a cash position of between 1% and 4% most of the time it’s been listed.

Of course, the judicious use of gearing is one advantage investment trusts have over their open-ended cousins and perhaps it’s another way Smithson may be able to edge ahead of Fundsmith Equity over time.

Smithson has the authority to gear itself up to 15%, so it will be interesting to see when, if ever, this is deployed.

At the end of March 2020, cash represented just 0.1% of net assets. Perhaps gearing might have been used if share prices hadn’t recovered so quickly from that point.

The ever-rising share count

One of my concerns has been the large number of shares issued by Smithson since it floated.

As with many popular trusts, this is done to limit the size of the premium to its net asset value, meaning the share price should be less volatile and the shares easier to trade.

Existing shareholders also benefit from the fact that shares are issued just above their net asset value.

But some folks would argue it’s the investment management firms that benefit most, as their fees are calculated as a fixed percentage of the amount of money managed.

Here’s how Smithson’s share count has changed over time:

| Date | Shares issued (m) |

|---|---|

| As of 19 Oct 2018 | 82 |

| To Dec 2018 | 2 |

| To Jun 2019 | 20 |

| To Dec 2019 | 10 |

| To Jun 2020 | 9 |

| Jul 2020 | 2 |

| As of 29 Jul 2020 | 125 |

It seems incredible now but the original aim when Smithson started marketing itself to investors was 25m shares at £10. It ended up with over three times that amount.

Smithson only started issuing shares in mid-December 2018. But things really got going in the first half of 2019, although the rate of new shares being issued has roughly halved since then.

The second half of 2019 and the first half of 2020 saw a similar rate of issue, given the process stopped for most of March 2020 when there was often a discount.

Let’s say the average share price has been £12.50 since Smithson floated and shares have been issued at an average 3% premium. That suggests an extra £16m has been raised for existing shareholders from all the share issuance to date.

Smithson’s management fee is a flat 0.9%. Net assets would be £1.22bn rather than £1.85bn if no new shares had been issued and the annualised fee would be £11m rather than £16.7m.

So the percentage gain is definitely far greater for the investment manager. Some of them pass on economies of scale with tiered or lower fees.

But that’s not the way Fundsmith plays this game.

The shrinking universe

My main concern is that a much larger Smithson might have trouble investing in the smallest companies or selling out of them when required.

Smithson’s target range is companies valued between £500m and £15bn. When it listed there were 83 companies in its ‘investable universe’ although that number might be a little different now.

Its current position sizes are mostly between 2% and 5%. A 2% position for Smithson in a £1bn company means an investment of £37m – so that would mean owning just under 4% of the company in question.

That should be relatively easy to trade in and out of, but it seems unlikely shares below £1bn are going to be top ten holdings.

I’m not sure how many companies in the investable universe are valued below £1bn, but there must be a few.

Should Smithson get to the £4-5bn range – a nice problem to have of course – then this issue could become more significant.

I’m fairly relaxed at the moment especially as it’s already been raised as a potential issue in management commentary.

And it could be I’m overthinking things here. Maybe raising the maximum size to £25bn at some stage gets rid of this issue, for example?

But Smithson is already 50% larger than the next biggest trust in the admittedly sparsely populated Global Smaller Companies sector. And Herald, the trust in question, has well over 200 holdings compared to Smithson’s 31.

Summing up

After taking a small position at the flotation, I’ve taken several nibbles of Smithson since.

I think my average price is 1,185p, paying a high of 1,362p this February (oops!) and a low of 939p just over a month later.

My position size feels about right now, so I’m not intending to buy any more for the time being. Although another large market fall accompanied by a sizeable discount might tempt me. My Fundsmith Equity position remains much larger than the one I have in Smithson.

Up 50% from its issue price after two savage sell-offs at the end of 2018 and earlier this year is certainly an impressive start.

And on an annualised basis its net asset value has risen 24.4% while its benchmark has declined by 3.9%. However, there’s no way that size differential can continue over the long term.

Fundsmith is up an annualised 18.1% as it nears the end of its first decade while its benchmark is up 11.4%. A similar level of outperformance for Smithson at the same stage of its life would be an excellent achievement.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Same I took 1500 at launch and took a bigger bite on the way back from the bottom. Its rewarded me well but Im keeping an eye on it. Its not a buy and forget yet.

IT Investor Thanks for your excellent review of Smithson which is very useful. Like you I don’t see myself investing here soon. I think it is disappointing that the Fund Manager has increased the number of shares in issue and has not reduced the level of the their charges which as you state is par for the course from Terry Smith and Fundsmith. This contrasts with Baillie Gifford who have consistently reduced their charges as the Fund size grew. Is part of their good performance down to charging a premium to new shareholders ?

There is a second point that I would make as to whether there are adequate numbers of quality smaller companies to invest in the £500 million to £15 Billion range that you point out in the article Smithson likes to invest in . So is this type of Fund going to be constrained by available investee companies going forward and can it therefore increase the share capital size,, which as stated above is part of it’s strategy, only if it invests more in the same target companies. The number of investee companies at 31 in number is quite small so this makes me wonder going forward.

Agreed J. Very few funds/trusts are buy and forget I’d say and it’s still early days for Smithson’s managers.

Thanks GI. Difficult to say how much issuing shares at a premium has added to performance. Maybe between 1% and 1.5% since the fund launched? Not insignificant, therefore, but not a massive factor either.

Personally, I’m not too worried about the small number of companies in the SSON portfolio as I’ve got a few funds that take a similar approach. But it does mean investors need to consider whether the trust can buy and sell its holdings in the quantities it wants, and the larger the trust gets the more difficult that’s likely to become. So I’ll definitely be watching to see what they say on this in future statements/results/presentations etc.

Love to read a follow up on Smithson.

How many more shares can Terry Smith issue?

As for moving to BG strategy of reduced fees I see no chance. Buy and hold?

Hi Sophia — Have replied to your tweet as well but in case you haven’t seen it yet, I did another piece on Smithson following its 2020 full-year results that were issued in March.

https://www.itinvestor.co.uk/2021/03/how-big-can-smithson-get/

I wouldn’t say my view has changed much since then. We had the 2021 half-year results last month and quality-type shares favoured by Fundsmith have had a better run in the last few months after a more difficult patch from February to May.

Hope that helps!