Scottish American Investment Company, often just called SAINTS, is the second-oldest investment trust and the only income-focused investment trust managed by Baillie Gifford.

It’s one of a handful of trusts in the Global Equity Income sector, alongside the likes of Murray International and JPMorgan Global Growth & Income.

Although Scottish American is mainly focused on equities, it has a sizeable portfolio of directly held UK commercial property, and also holds some fixed-income securities.

Key Stats For Scottish American Investment Company

Figures are as of 15 June 2020 unless otherwise stated:

- Founded: 1873

- Co-managers: James Dow and Toby Ross (since 2017)

- Management firm: Baillie Gifford

- Ticker: SAIN

- Benchmark: FTSE All-World

- 10-year net asset value return: 167%

- Share price: 404p

- Indicated spread: 403p – 405p (0.5%)

- Market cap: £615 million

- Premium to net assets: 5.6% (12 Jun)

- Costs: OCF 0.8%, KID 2.1%

- Net gearing: 13% as of 30 Apr 2020

- Historical dividend and yield: 11.875p and 2.9%, paid quarterly

- Results released: Feb (finals) and Aug (interims)

- Sector: Global (1st out of 5 over the last 10 years)

- Links: Website and AIC page

History

Scottish American was set up by an Edinburgh lawyer, William Menzies, in 1873.

Menzies was one of many individuals who were attracted by the growth potential of the US and the trust initially invested largely in railroad bonds before broadening its remit, first into other types of debt and then equities.

Government restrictions put in place during the two World Wars meant it had to invest much more in UK assets and they came to dominate its portfolio until quite recently.

Scottish American features extensively in John Newlands’ history of investment trusts — Put Not Your Trust In Money — which includes a calculation that someone investing £1,000 in 1873 would have had £70,000 by 1929, with their annual income growing from £40 to £3,000.

The trust was self-managed up until 1970 but then put Stewart Fund Managers in charge of its portfolio. Various successor firms followed. However, in late 2003, disappointed by its recent “modest dividend growth”, the directors appointed Baillie Gifford instead.

At the time, the portfolio was still very UK-focused with a benchmark consisting of 70% UK index and 30% global.

The benchmark was changed to 50% UK/50% global in 2009, as the weighting of UK assets gradually declined.

However, during the early 2010s, the UK focus was reduced substantially and a global index has been the trust’s benchmark since 2014.

Scottish American is one of the AIC’s Dividend Heroes, with a 40-year record of consecutive dividend increases. What’s more, it’s not cut its dividend since 1938.

Last year, somewhat sadly, it ditched its old ticker code of SCAM, deciding that SAIN was a more appropriate fit!

Promotion from within

There have been a few manager changes during Baillie Gifford’s tenure.

Patrick Edwardson ran the shop from 2004 to 2013. He was replaced by Dominic Neary, who was the lead manager from 2014 to 2017.

Then Toby Ross and James Dow took over in 2017.

Neary, Ross, and Dow all served as deputy managers for a few years before stepping up, as often seems to be the way with Baillie Gifford, so the transitions appear to have been fairly smooth.

Investment approach

Baillie Gifford is known for its emphasis on long-term growth and it takes a similar approach here:

Our investment approach has always been focused on finding high-quality, robust companies, that are capable of paying resilient dividends over time. We think we own through-cycle winners, not companies that are relying on a favourable economic backdrop in order to be able to grow. That’s why the biggest holdings in SAINTS’ equity portfolio are companies like Roche or Procter & Gamble or Deutsche Boerse, not Lloyds, or big oil companies.

We’ve been massively helped in our stock-picking by having a global universe of 4,500 dividend-paying stocks from around the world to choose from. And that’s made it much easier for us to avoid many of the areas that are causing so much disruption to dividends in the narrower UK market. But it also gives us a big diversification benefit – companies like Anta Sports, the Chinese Sportwear business, are already returning to work again, even while Europe remains in lock-down.

In our property portfolio, SAINTS is also biased towards strong tenants, with little exposure to the most challenged areas and the property manager has been increasing that resilience over the last few years, by reducing exposure to areas like restaurants or retail or pubs.

According to Scottish American, there are only some 250 dividend-paying stocks in the UK. That sounds a little low to me, but it’s certainly a much smaller pond in which to fish.

Dividend yields do tend to be a lot higher in the UK although many people believe UK companies have fallen into the trap of paying out too much in recent years, which is part of the reason they are now cutting back so drastically.

Here’s how Scottish American sees the coronavirus pandemic affecting its approach:

When it comes to making changes to the portfolio, we think it’s more important than ever that all our decisions as managers are guided by what’s best for SAINTS’ long-term income stream. This means we need to resist the temptation of apparently cheap, high-yielding stocks. The income may turn out to be illusory and often the long-term prospects look pretty poor. So we aren’t tempted to pile into the oil majors, or retailers, or go bargain-hunting in the banking sector.

Instead, we need to focus, at the individual company level, on where are the biggest long-term income growth opportunities? Who are the most adaptable management teams? Who’s going to emerge from this period of disruption stronger?

So with that as our guide, we have started to make a couple of changes to the portfolio. We’ve added to some of our favourite names, at more attractive valuations. We’ve also taken new holdings in a couple of businesses that we’ve admired for some time, where we think the market is now unduly focused on the short-term profit outlook. The great American asset manager T Rowe Price, for example, and Hargreaves Lansdown, which is the dominant savings platform in the UK.

And on the other side, we’ve moved on from a couple of stocks where our conviction in the long-term case had been ebbing, and which we think won’t emerge from this crisis stronger.

Taking this long-term view on income means Scottish American has a much lower dividend yield than most other income funds.

More surprisingly, its dividend payout hasn’t grown that much in recent years.

It was 9.05p in 2009 and 11.875p in 2019, representing average annual growth of 2.7%. However, its total return places it at the top of the Global Equity Income sector over that timeframe, although only five trusts have a 10-year record, so it’s a small field.

Scottish American had revenue reserves of £17m at the end of 2019, sufficient to cover just under a year of current dividends. It hasn’t explicitly said it would increase its dividends in 2020 although, in May, it did declare a quarterly dividend of 3p, up 2.6% on last year.

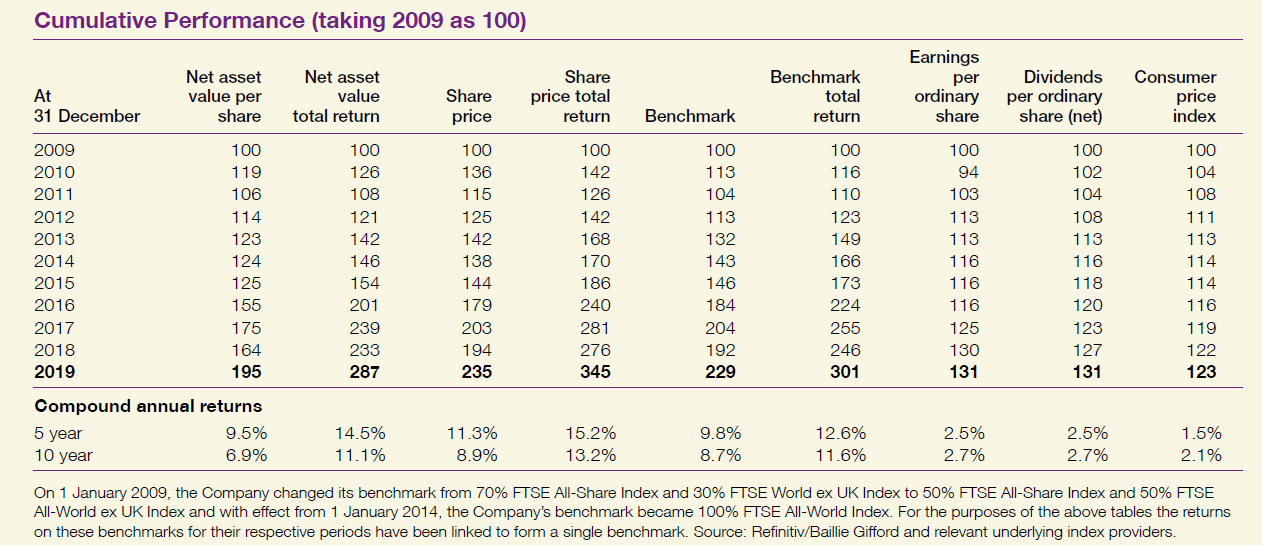

Track record

Here are some 10-year stats from the most recent annual report.

It’s a decent rather than a spectacular track record I’d say.

The share price return over the past decade has been flattered somewhat by the move from a discount to net asset value to a fairly consistent premium of between 3% and 7%.

Over the five years to April 2020, the net asset value return was 64% versus 55% for the FTSE All-World index.

The portfolio

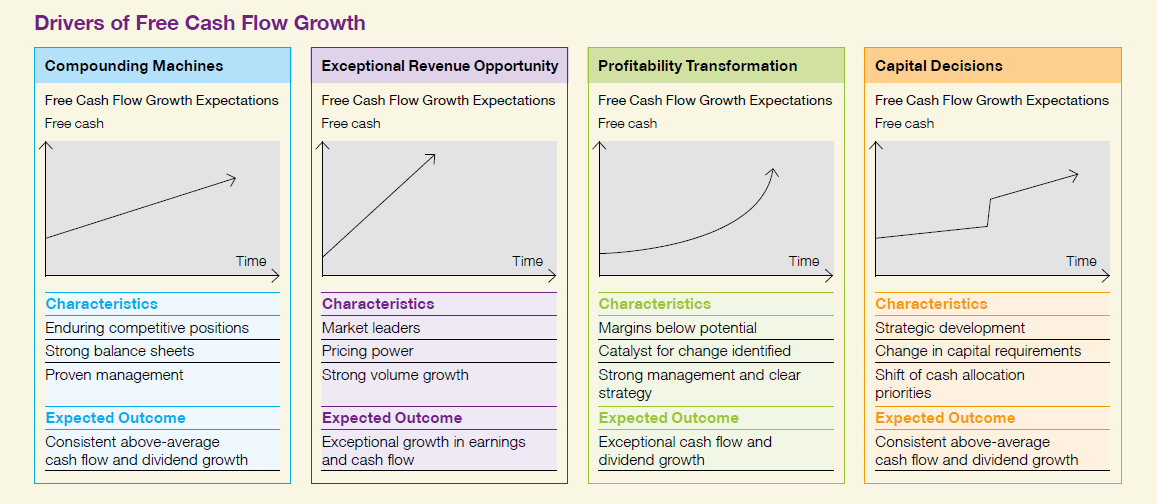

Baillie Gifford is very good at outlining the methodology behind the stock selection for its trusts.

Here are the four categories for Scottish American:

And this is how that breaks down by yield:

You can see that the blue compounding machines dominate the portfolio.

There are around 60 stocks in total, but only 6 of them at the last year-end yielded more than 5%. So, Scottish American certainly can’t be accused of hunting for yield.

The vast majority of positions are between 0.8% and 3% of assets, so most holdings are meaningful but nothing dominates to the same extent that Tesla and Amazon do at Scottish Mortgage.

Total assets can be broken down as:

- North American equities — 27%

- European equities — 26%

- Property — 14%

- UK equities — 12%

- Asian equities — 11%

- Other equities — 7%

- Fixed income — 2%

The largest UK holdings are Admiral, GlaxoSmithKline, Experian, British American Tobacco, Greencoat UK Wind, Rio Tinto, and Hargreaves Lansdown. That’s a fairly even mix of newer and more established businesses that seems to be reflected across the whole portfolio.

The biggest holdings, for example, include both Microsoft and Taiwan Semiconductor and Coca-Cola and PepsiCo.

The fact that it has a directly owned property portfolio surprised me a little. There are 16 UK properties worth a collective £85m. Five are pubs, but they only account for £10m.

The biggest two are a Kent holiday village and a TalkTalk data centre (both worth around £16m). There is also a nursing home, warehouse, supermarket, and a bowling alley.

It looks like this part of the portfolio has been a feature since before Baillie Gifford took over, and it has remained at roughly the same proportion of the portfolio throughout. It is managed by OLIM.

Gearing

Scottish American has an £80m debenture with an 8% coupon that runs until April 2022. This was taken out in tranches between 1997 and 2001 when interest rates were substantially higher.

The market value of this debt is some £10m more than its book value, so this causes several pence difference in its net asset value calculation depending on which measure you prefer. However, this difference should narrow over the next couple of year as the repayment date approaches.

The good news is that a private refinancing deal for this debenture has already been agreed, at a fixed rate of 3.12% a year. £40m will be repayable in 2045 and the other £40m in 2049.

Net gearing levels reduced throughout the 2010s as Scottish American’s portfolio grew in size but no new borrowings were taken out.

Gearing was just over 30% at the start of the last decade but is now just 13%.

In recent years, the value of the property held, net cash, and fixed income has usually exceeded the amount due via the debenture.

Charges

Baillie Gifford trusts are usually pretty cheap and there is a 0.45% management charge at Scottish American. That’s pretty good for a £600m trust.

There’s no performance fee or lower-charge tiers as the value of assets increase (although that may be introduced at some stage I suspect).

The property portfolio is subject to a 0.5% management charge.

The two management fees came to £3m last year with another £1.25m for general administrative costs. That resulted in an ongoing charge of 0.77%.

The Key Information Document charge of 2.1% is noticeably higher. 0.2% was due to portfolio transaction costs but the lion’s share of the difference (1.0%) is due to the £5.6m of interest payments due on the debenture.

Skin in the game

The six directors owned 72,000 shares between them at the last year-end, currently worth £0.3m. That’s disappointingly low.

Peter Moon, on the board since 2005 and Chairman since 2016, owns 15,000 while Lord Macpherson owns 45,000 (up from 30,000 the previous year).

Two of the directors were only appointed in 2019, so their lower holdings are more understandable.

Eric Hagman has been on the board since 2005, yet only had 2,000 shares at the last year-end. He seems to have bought 29,700 in May 2020, though, which is rather more encouraging!

The holdings of Ross, Dow, and other Baillie Gifford staff aren’t disclosed, which seems to be a common approach across all of Baillie Gifford’s trusts.

Both co-managers are relatively young. Ross joined Baillie Gifford in 2006, having just graduated from Cambridge. Dow graduated in 2000 and spent some time at The Scotsman, where he was Economics Editor, before joining Baillie Gifford in 2004.

Ross and Dow also work together on a couple of Baillie Gifford’s open-ended funds: Global Income Growth (£500m) and Responsible Global Equity Income Fund (£80m), which both have very similar portfolios to Scottish American.

Dow is also one of four managers on the Multi-Asset Income Fund (£60m).

Citywire hosted a ‘dividend crisis’ webinar last month if you want to see Toby Ross in action, extolling the virtues of income investing beyond the UK.

Summing up

As with most Baillie Gifford trusts I’ve looked at recently, there seem to be many more pros than cons.

At the time of writing, Scottish American was down 4% so far in 2020, pretty much in line with a global tracker.

However, although its recent performance has been better, its record since 2004 against its main competition is more middling.

Since Baillie Gifford took the reins, Scottish American’s total return has been 419%. That compares to 392% for Murray International and 473% for JPMorgan Global Growth & Income.

Scottish American has done better than most UK-focused equity income trusts, though, with City Of London up just 247% over the same period. It trails the UK sector leader, Nick Train’s Finsbury Growth & Income, which has risen 705%.

I’m still thinking of tweaking my collection of global trusts, having decided they were a bit too similar a few weeks ago. Scottish American is still in the mix for that but doesn’t seem radically different from what I already have.

My preference for investment inactivity seems likely to prevail therefore. Nevertheless, it’s always useful to have back-up ideas should the unexpected happen!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Well written, as per usual! At the moment I’m having a look for value-based trusts for diversification, am I right in thinking these are fairly uncommon? Certainly most value based open ended funds seem to only concentrate on the UK!

Thanks Ben.

I wouldn’t say there are a great deal of value-focused investment trusts around but it’s somewhat of a loose term so it depends how you are defining it.

Among the global trusts, Scottish Investment Trust, AVI Global, Seneca Global G&I and Murray International seem the most likely candidates off the top of my head, with maybe RIT and Caledonia having a bit of both growth and value. Then there’s the likes of Personal Assets, Ruffer, and Capital Gearing, which have dialled down their equity exposure significantly in recent years, for those who want fixed-income exposure as well.

Ben – I suppose one could argue that Pershing Holdings is a ‘value investment’ if not having a value-focused style, given it’s on over a 30% discount. Of course, is there a catalyst to realise that value? (I don’t know but suspect not).

Obviously, the definition of Value is more tricky than ever, it means so many different things to different people. My quick take is that the acceleration of technological disruption is creating more Value Traps, and it feels that there’s not much that looks ‘cheap’ that’s not a Value Trap.

There is always the odd Special Situation (annual reports of funds like AVI Global are good for e.g. discounted Holding Co ideas) but I’m not sure whether there is enough ‘value’ about for a fund.

Thanks, IT Investor for the write-up. Feels a bit like Baillie-Gifford-lite to me – no great appeal I can see!

Thanks both, yes I should have clarified that I meant trusts where the manager (s) use a value-based style rather than a growth-based one. I’ve looked at a couple of the ones mentioned but definitely not all of them so will have a look, thanks.

Apologies for this belated comment to your interesting dissection of SAINTS.

I’ve thought about Scottish American for some time but the expensive debenture and its purely UK-focused property portfolio (which feels out of place in a global income fund) have put me off.

I recently invested in a couple of open-ended global income funds:

i) Liontrust Global Dividend which has been on a strong run since the change of manager to the memorably named Storm Uru in August 2017.

The manager gave an interesting presentation on the “Brighttalk” channel a few weeks ago (you will need to register with Brighttalk, I think):

https://www.brighttalk.com/webcast/706/418792?utm_source=brighttalk-portal&utm_medium=web&utm_content=liontrust&utm_campaign=webcasts-search-results-feed

ii) TB Chawton Global Equity Income which was launched in May 2019 and is at/near the top of the IA Global Equity Income sector since then, although early days of course.

These latter two OEICs are more total return than purely income focused and thus lower yielding than Murray International and JGGI, but in capital terms they have outperformed the global equity income ITs over 6 months, 12 months and in Liontrust’s case 3 years.

Thanks, David.

I think the debenture issue is working itself out now, especially now it has been refinanced early. It’s got less than two years left to run, so there’s only around £3m in interest charges left to pay.

The property portfolio is an oddity, though, and it’s yet to be revalued in 2020. The fact that it predates Baillie Gifford taking over management of the trust surprised me as well.

Not familiar with either of those funds you mention but the top ten holdings look pretty promising in both cases.

Very good post. I was thinking of using SAINTS as a long term vehicle for regular investing for my kids. We are talking a period of 15 to 20 years. Have you any thoughts on this or would you suggest another alternative.

I have about 5% in SAIN and while it will never shoot the lights out its growth-oriented performance has been very solid compared to most generalist or income international funds and it gives me some quarterly income in my SIPP. It has also done a lot better than other income funds like CTY that have chased high yield and lost capital by buying ex-growth dogs. I see it as a low risk counterbalance to my other investments which are generally high risk, and am adding to it slowly as I am nearing 60 and gradually de-risking.

Like you, I find the property element a bit strange and random. As it seems to be in retail/leisure I wouldn’t be surprised to see a valuation hit on it. I’m surprised they never sold it off, especially as with a third party manager it is fees on fees.

I take some reassurance from the high yield end of the portfolio including two of my own direct equity holdings, RIO and BATS.

Thanks Andrew. Nick gives a good summary above I think.

However, I’m always reluctant to comment on whether funds or trusts are suitable for others, not being authorised to provide financial advice.

For my own purposes, I went for a cheap global index tracker for both my children so the strategy could continue largely unmonitored if for some reason I wasn’t around to keep an eye on it.

Global investment trusts would probably be my second choice although I probably would go for a small group of them rather than a single trust, assuming it was cost-effective to do so.

It’s also worth bearing in mind that most Baillie Gifford funds have had a very good run recently and obviously there’s no guarantee that will continue. Saints is probably the lowest-risk BG trust, though, given its global diversification and income focus.

Lastly, SAINTS managers are both young compared to most other trusts, but they may not be managing the fund for as long as 15-20 years, so that’s another area that may need watching.