Herald Investment Trust boasts an impressive track record from backing smaller technology companies, many of which are based in the UK. But taking a more cautious approach than other tech funds, it has struggled to keep up during the past decade.

Key stats for Herald Investment Trust

- Listed: February 1994 (100p)

- Manager: Katie Potts (since launch, 61 years old)

- Ticker: HRI

- Benchmarks: Numis Smaller Companies including AIM and Russell 2000 Technology Index (in sterling)

- 10-year net asset value return: 257%

- Recent price: 1,364p

- Indicated spread: 1,360p – 1,368p (0.6%)

- Exchange market size: 750

- Market cap: £911m

- Discount to net assets: 15%

- Costs: OCF 1.1%, KID 1.3%

- Net cash and fixed interest: 13% as of 30 April 2020

- Current dividend and yield: Nil

- Results released: February/March (finals) and July/August (interims)

- Sector: Global Smaller Companies

- Links: Website and AIC page

A potted history

Herald joined the London market in February 1994, so it pre-dates Polar Capital Technology (December 1996) and Allianz Technology (December 1995). Whereas the latter two are pure tech funds, Herald still favours the old TMT moniker, with significant holdings in media and telecoms.

From Herald’s 2019 annual report:

The Company, founded in 1994 by Katie Potts, raised an initial £65m to invest in the UK and continental European TMT sector. Warrants were issued to initial investors on a 1 for 5 basis.

In 1996 a further £30m was raised to globalise the fund, thus bringing the total outside capital to £95m. Since 1996 no new capital has been raised, and the warrants have been repurchased or converted into ordinary shares.

The Company has operated an opportunistic buyback policy, which has offered large holders liquidity and helped to create value for existing shareholders. Since inception, the Company has completed buybacks to the value of £138m, bringing the net negative outside capital to £43m.

Over the history of the fund, net asset value per share on a total return basis has grown by 1,721.3% or 11.9% on an annualised basis.

As this snippet explains, the UK focus of the fund was dialled back a bit early on. Its first annual report shows 82% UK, 5% overseas, and 13% cash/fixed-interest.

By the end of 1999, the figures were UK 67%, overseas 32%, and cash/fixed interest of 1%.

The latest factsheet has the UK at 48%, overseas 38% (of which North America is 25%), and cash/fixed interest at 14%.

Warrants?

The issuing of warrants when a trust floats may come as a surprise to newer investors.

Back in the day, new investment trusts usually went straight to a discount, reflecting the fact that most existing trusts traded at a discount and floating a company knocked 2-3% off net assets before the first investment was made.

To encourage private investors to buy new issues, you were often given a few warrants on the side, allowing you to buy more shares at the IPO price at a later date.

Potts still runs the show

Katie Potts is still the fund’s manager today. She was a top-rated technology analyst at Barings and SG Warburg before setting up Herald Investment Management, the trust’s manager, in 1993.

Potts owns just over 40% of Herald Investment Management so she’s undoubtedly the key person here.

She also owns 448,095 shares of Herald Investment Trust (0.67% of its share capital) worth some £5.8m.

Encouragingly, she’s added more quite a few more shares over time. Picking a couple of annual reports at random, I see she owned 249,000 in 2009 and 330,000 in 2014.

The wider Herald business

Herald Investment Trust seems to be the main portfolio that Herald Investment Management looks after, with around £1bn in assets.

There is also an open-ended fund, Herald Worldwide Technology Fund, which mostly invests in the usual, larger US tech suspects. However, it only has assets of some £40m despite being launched in 1998.

Herald also manages two venture capital funds — worth a combined £50m — but these have been closed to new investors for some time now.

Herald Investment Trust owns 15.4% of Herald Investment Management but unlike the situation at Lindsell Train Investment Trust, this has very little impact on its overall valuation. Herald Investment Trust’s stake is reckoned to be worth £4.4m, so it’s only around 0.4% of its total assets.

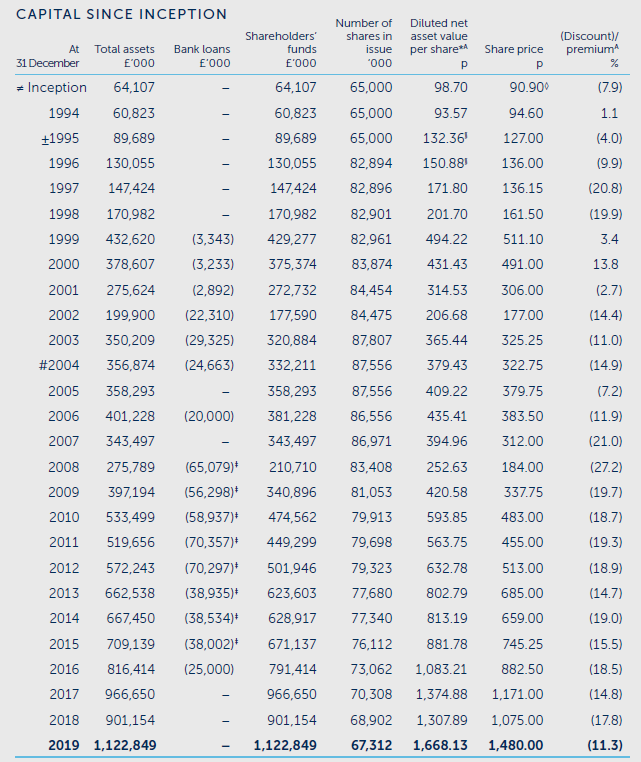

Track record

In common with many trusts that have had the same manager for a few decades, Herald’s annual report has a lot of excellent information on how the trust has done over the long term, its investing style, and details of its individual holdings.

For example, this table shows how assets have grown plus how the level of gearing and discount has varied:

Despite a strong long-term performance, we can see that the path has been pretty rocky for Herald at times, reflecting the fluctuating fortunes of the technology sector since the 1990s.

Herald’s share price grew five-fold from in the five years ended 31 December 1999. But a look at its annual report from that time reveals a fairly conservative list of holdings, with a distinct lack of glamour stocks and flighty loss-making dot coms.

ARM, where Herald was a very early investor, was then its second-largest position at just over 4% of net assets and Autonomy was also in its top 20, but that’s about it.

Its relatively conservative stance didn’t help it avoid the tech bust. Its share price topped £7 in both March and September 2000 before hitting a low of around 130p in September 2002. It took until 2014 before the share price exceeded £7 again.

In the global financial crisis, the share price peaked at 425p in July 2017 and hit a low of around 170p in December 2008.

Earlier this year, Herald went from £15 on 20 February to 897p on 19 March.

In other words, while this can be considered a cautious play relative to other tech funds, it still tends to at least as volatile as other equity trusts.

Sensible use of gearing…

Herald hasn’t been averse to using a bit of gearing over time, increasing its borrowings in 2002 just before markets bottomed.

The global financial crisis saw Herald’s borrowings fluctuate quite a bit. It built up £40m in net cash in late 2007 but invested this well before the financial crisis peaked in October/November 2008. In retrospect, Herald admitted it had moved too early as it thought a second wave down was possible but unlikely.

A £50m bank loan was taken out in April 2008 but the cash raised by this wasn’t invested until 2009, so the increase in borrowings shown at the end of 2008 is somewhat misleading.

Borrowings were halved in 2013 and then disappeared completely during 2017, reflecting Herald’s cautious nature in the face of ever-increasing company valuations.

All in all, it looks like Herald has been pretty savvy with its use of gearing over the years, borrowing more when valuations were lower and mostly scaling back at the right time.

… but a persistent discount

While most sizeable equity trusts have seen their discounts narrow over the last decade, that hasn’t been the case with Herald.

It’s enjoyed a premium every now and again, but the discount has bounced between 10% and 20% for most of the last 10 years.

So, while its current 15% discount looks attractive at first sight, it’s not unusually wide for Herald.

Herald has bought back a decent number of shares over the years, with its shares count falling steadily from 87.8m in 2003 to 67.3m by the end of 2019.

And of the £138m spent on buybacks since the trust launched, £95m has been in the last five years.

Since the end of 2019, though, only 345,000 shares have been repurchased, largely at prices around or above the current share price.

20,000 shares were bought back on 2 March, followed by 20,000 on 27 March, then 100,000 on 21 April. Only the middle of those three transactions was significantly below the current share price.

Maybe it’s too easy to be critical here, given the benefit of hindsight. But Herald’s discount exceeded 20% for the latter half of March, spiking to 29%, so it seems a little odd that they didn’t take more advantage of that given the trust’s large net cash position.

That said, in its AGM statement in mid-April, Herald said, “The Manager has not yet aggressively purchased stock in the belief that there will be a stream of follow on fundraisings for investee companies which have already started to occur, and that good buying opportunities will occur in coming months.”

Portfolio overview

Herald’s full list of investments as of December 2019 runs to several pages — it has 288 individual holdings! That’s unusually high, even for a sizeable small-cap trust.

But this has been a long-term feature of this trust. It had well over 100 holdings back in 1996 and around 250 in 2000.

The top 20 run from GB Group at 3.9% of assets to Bango at 0.9% and account for around 30% of the portfolio.

The top 50 holdings account for around half of the portfolio, so there is an extremely long tail of very small positions.

Herald is covered by Quoted Data, which has produced several research notes on it over the past few years, the latest being published in April 2020.

Quoted Data reckons the larger position sizes are usually a factor of past share price growth rather than Herald taking a large position when first buying into a company.

On the bias to the UK it says:

This reflects Katie’s belief that the UK technology sector is more vibrant than Europe’s; UK stocks are, generally, more reasonably valued than US ones; and Asian stocks generally have inferior business models (frequently they are providing outsourced manufacturing services to larger tech companies and often have little pricing power).

Size and sector breakdowns

Size-wise, about 55% of Herald’s portfolio has a market cap of $1bn or lower. 28% is valued between $1bn and $3bn with the remaining 17% over $3bn. However, the median market cap is around $200m, reflecting the long tail of smaller position sizes.

Herald’s policy is to only start or add to positions valued at less than $3bn. But Potts has often lamented the fact that UK firms tend to get bought out rather than growing to multi-billion pound enterprises, effectively robbing Herald of some potential gains.

There’s a wider mix of sectors that you might expect for a tech fund, especially when it comes to its UK holdings. That might be the reason Herald was recently shifted by the AIC from its technology sector to global smaller companies. It seems slightly better placed in the former I’d say, but I can see the logic of its new home.

About two-thirds of the UK holdings are AIM-listed rather than on the main market, representing about one-third of its overall portfolio. There’s a lot of dross on AIM but Herald largely seems to avoid the loss-making cash guzzlers that give this junior market a bad name.

Here’s a breakdown by sector and region (you can click to enlarge it):

Potts seems comfortable with Herald’s positioning in respect of COVID-19. She highlights that the key is not to panic and that the current crisis always seems the worst.

Herald plans to “stick to quality management teams who can navigate the challenges” and believes the tech sector is “relatively better positioned due to modest leverage, the high element of recurring revenues and exposure to digital trends”.

At its AGM in mid-April, it said, “to date, only a modest number [of holdings] have been materially affected and many investee companies are experiencing increased demand.”

No dividends for several years

Herald paid a small dividend from 1996 through to 2013, skipping a year in 2011 and paying a special in 2009.

But the amount paid only rose from 0.65p in 1996 to 1.0p in 2013, so it’s never been a significant factor in the trust’s overall returns.

Nothing has been paid out since 2013 and that seems unlikely to change for the time being.

In 2019, dividends received and the income from fixed-income securities came to £11.7m, which was roughly the same amount as the trust’s operating expenses.

A little cheeky on the cost front

Herald isn’t massively expensive but it’s pretty disappointing that its management charge seems to have remained at 1% of net assets since it was launched over 25 years ago.

Net assets rose 17 times from 1994 to 2019 but none of the economies of scale this has generated have found their way into the pockets of shareholders.

Both Polar Capital Technology and Allianz Technology have tiered management fees, reducing as the size of the trust increases. Unlike Herald, they do have performance fees, so their overall costs are broadly similar.

Skin in the game

As mentioned earlier, Potts owns nearly £6m of Herald, which is excellent to see. Her holdings are only disclosed in the annual reports, as far as I can tell, so may have changed since the end of 2019.

Four of the six directors own several thousand shares each, worth roughly £100,000 apiece, so that’s another positive for me.

Julian Cazalet, who was Chairman for 10 years until he retired in April 2019, owned 150,000 shares at that time.

Henrietta Marsh, who was only appointed in September 2019, doesn’t seem to have bought any shares yet.

Stephanie Eastment, appointed in December 2018, seems to have been the only director to have bought any shares in 2020, adding another 500 shares at the cost of £7,000 and taking her holding to 2,500.

The succession question

While I love to see fund managers with a long tenure, the question of who runs the show next often needs considering.

Potts is only in her early 60s so could be around for some time yet. Indeed, it’s not unusual to see managers with hefty ownership stakes stick around well past the standard retirement age.

Fraser Elms, the trust’s Deputy Manager, seems the obvious candidate to replace Potts should she decide to stand down. He has worked for Herald for 20 years and runs the Far East part of Herald’s portfolio. But he’s not mentioned in the latest annual report so I suspect no change at the top is deemed imminent.

Two other investment professionals on Herald’s team — Taymour Ezzat and Hao Luo — have been with the firm since 2004 while Bob Johnston was recruited in 2016 to set up a US office (having previously worked alongside with Herald for 15 years).

All in all, there seems to be some bench strength here even though Potts is undoubtedly the main figure.

Against the competition

No one seems to invest in exactly the same fashion as Herald but it makes sense to compare their record against UK smaller company trusts and the two main tech trusts.

I’ve managed to get data both for 10 and 25 years, based on share price returns with dividends reinvested.

Selected tech and small-cap trusts

| Trust | Ticker | Launched | Total assets (£m) | 10 years % | 25 years % |

|---|---|---|---|---|---|

| Herald | HRI | 1994 | 1,030 | 246 | 1,478 |

| BlackRock Smaller | BRSC | 1906 | 706 | 329 | 1,589 |

| BlackRock Throgmorton | THRG | 1962 | 499 | 322 | 760 |

| Henderson Smaller | HSL | 1887 | 678 | 301 | 469 |

| Invesco Perpetual UK Smaller | IPU | 1988 | 150 | 254 | 1,564 |

| Montanaro UK Smaller | MTU | 1995 | 224 | 177 | 995 |

| Oryx International Growth | OIG | 1995 | 158 | 404 | 767 |

| Rights & Issues | RIII | 1962 | 129 | 393 | 3,281 |

| Standard Life UK Smaller | SLS | 1993 | 512 | 287 | 545 |

| Allianz Technology | ATT | 1995 | 689 | 512 | * 1,750 |

| Polar Capital Technology | PCT | 1996 | 2,356 | 469 | * 1,658 |

The figures for Allianz and Polar actually start from January 1997 so don’t measure a full 25 years, hence the asterisks next to their figures. Over the same timeframe, Herald is up 950%.

Interestingly, Herald, Polar and Allianz were pretty much neck and neck until the Brexit vote in 2016. Since then, Allianz and Polar have raced ahead, thanks to the strong performance of big US tech stocks.

A few UK smaller company funds without a specific tech focus have bested Herald as well, but overall its long-term performance has been highly impressive.

Summing up

While I can see a few negatives here (e.g. the lack of a fee reduction and the recent reluctance for buybacks), it’s hard to argue with Herald’s long-term performance and Potts is clearly held in very high regard.

Indeed, it’s a trust that I’ve had marked down as a potential purchase for a while now, maybe adding it alongside one of Polar or Allianz as a tech basket.

I think the fact I’m generally looking to de-risk my portfolio over the next several years has kept me from pulling the trigger, but a hefty share price fall, if markets were to slip back again, may prove too tempting.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Great write up, thanks.

You’ve got some dates mixed up in the gearing section.

Thanks Mark. I’ve now corrected those dates – cheers for highlighting that.

Thanks a forensic study but with the UK and Europe in the mire USA and Asia is surely the place to look for tech investments.

Thanks Nigel. Herald has just over a third of its investments in North America/Asia so it does have a fairly significant presence in those markets as well. But I suspect many investors combine Herald with other tech trusts/funds to get the geographical balance they desire.