Independent Investment Trust is one of those funds that I have been aware of for quite a while but never got round to digging into properly. Its shares are up 500% over the last 10 years, so perhaps I need to re-examine my priorities!

About twelve months ago, Independent Investment Trust started climbing to an extremely large premium. It even topped 20% for a while. That premium has disappeared in the last couple of months, so I thought it was worth checking out what on earth has been happening.

A potted history

For the uninitiated, Independent Investment Trust is a concentrated equity fund that was set up in 2000. Its fund manager is the very well-spoken Max Ward.

Ward worked at Baillie Gifford from 1971 to 2000 and was made a partner there in 1975. He headed its UK equity department for nearly 20 years and spent his last 11 years there managing a little-known fund called Scottish Mortgage. I wonder what happened to that!

Independent sits in the global sector but over 90% of the fund is invested in the UK. 3% is in cash and 2% apiece in Asia, North America and Europe. That sector classification strikes some people as odd, but Ward apparently wants to retain an element of flexibility when it comes to choosing investments.

That’s fine with me, although I know some people find these situations less tolerable, especially when a largely domestic fund ends up getting compared to a global benchmark. Personally, I think it’s a reminder that we always need to dig under the covers to see what a fund really does.

No spring chicken

As you may have guessed, Ward is not a young man. Indeed, he turns 70 next August. A key question for investors is therefore how long does he plan to continue and who might replace him?

Well, the payroll of Independent consists of just two people: Ward and Vivien Judge, the office manager. They certainly run a lean ship and you can tell no money has been wasted on its website or producing its annual reports. I like that!

Ward’s salary also seems pretty low. In City terms, anyway. His current contract is £200,000 a year. It increased from £100,000 to £150,000 in 2011 and from £150,000 to £200,000 in 2016. The three non-executives collect £99,000 between them.

It’s no surprise that the fund’s overall expenses are so low then. The ongoing charge is a mere 0.25%, which is truly excellent and pretty much tracker-fund level.

A few investment trusts are similarly cheap. They tend to be much larger and so have more opportunities to benefit from economies of scale. Independent has £350m in assets, so it’s a relative minnow in the world of investment trusts.

Expect “a decent burial”

An interview on Citywire from December 2017 sums up the succession plan pretty well:

Well I would like to carry on running Independent for as long as I am fit to do so … I still get a huge buzz out of going into work, I like to think I can still compete at this level. And for as long as that remains the case, I would like to keep on doing it.

When we floated the Independent … shareholders were told that in the event that I was no longer able or willing to run the fund, it would be given a decent burial. And the board have felt that that should remain the case. So there are no succession plans.

What will happen when I’m no longer willing or able to do it is that shareholders will be given a choice of taking their money in cash or rolling over into some vehicle chosen by the board which will allow them to roll forward their capital gains.

So, it’s unlikely this fund will be with us 20 years from now, in its current form anyway. But it looks like shareholders will have options, and it should carry on for several years yet.

Why the large premium arose

It seems there were three reasons why Independent Investment Trust shot to that incredible 20% premium.

First, its small size. Its excellent track record probably attracted hordes of performance chasers. Lots of people hunting down a limited number of shares often results in price spikes.

Secondly, the directors apparently wanted to keep the fund below €500m in size. This was to avoid having to comply with a load of additional EU regulations. So, unlike other funds that go to a premium, they didn’t issue more shares to meet demand.

Last, its shares are pretty tightly held, limiting the supply of shares available for us mere mortals even further.

I am more relaxed than most when it comes to buying or holding funds at a premium. But when it comes to funds like Independent that directly hold mainstream shares, I reckon a premium of more than a few per cent should be avoided.

When you have assets that aren’t valued that frequently, e.g. infrastructure, premiums are more understandable. Likewise, when you have a large asset that is hard to value precisely, such as Lindsell Train Investment Trust’s stake in the Lindsell Train fund management business, it may also make some sense.

Trash talk

In the absence of issuing new shares as a means to reduce the premium, the board of Independent Investment Trust started to trash talk their own fund. To be more precise, they publicly dissed the large premium it was trading at.

They also sold a fair amount of the shares they held in the fund, mostly during a 3-month spell from mid-February to mid-May, when the premium was at its most extreme.

As you can see, they all still hold a sizeable stake. Indeed, it’s pleasing that all the directors are significant holders.

| Director | Shares held in Nov 2017 | Sold since | Stake remaining |

|---|---|---|---|

| Max Ward | 4,160,000 | 303,000 | 7.0% |

| Douglas McDougall | 8,551,250 | 551,750 | 14.4% |

| James Ferguson | 965,000 | 65,000 | 1.6% |

| The Hon. Robert Laing | 860,000 | 50,000 | 1.5% |

Note that the above table has been created by me trawling through about three dozen RNS releases. I may have missed some or cocked up with the maths!

It’s not clear what punctured the premium balloon, as it didn’t start to deflate until August. It was probably a combination of the above plus some enthusiasm waning in respect of the fund’s largest holdings.

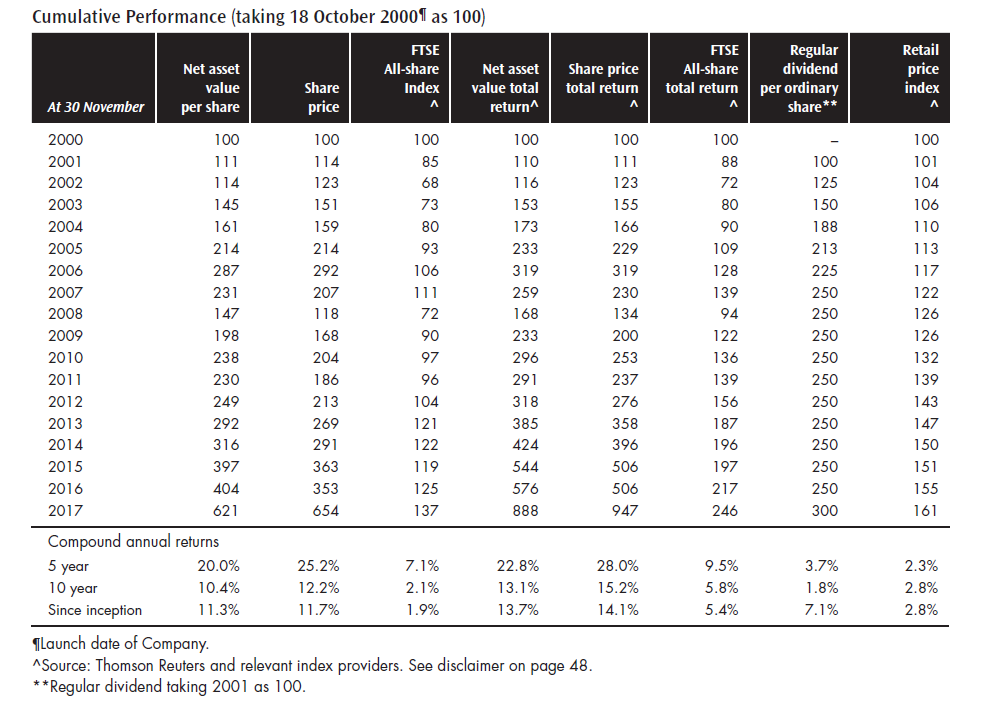

Independent Investment Trust’s track record

I think this performance summary from last year’s annual report is worth sharing. It’s great to see funds that go back all the way to their launch date when it’s practical to do so.

You might be able to tell from comparing the net asset and share price total return columns that this fund has often traded at the extremes when it comes to premiums and discount.

In its first few years, a premium was fairly commonplace. But then the financial crisis intervened. Ward says the fund “could not have been more poorly positioned”. It had a lot of property-related stocks, including banks and house builders, and double-digit levels of gearing.

Compare the November 2006 share price of 292p to the 118p from two years later. Ouch!

Ward says, understandably, he was over cautious for a number of years following this. Double-digit levels of gearing were replaced with double-digit levels of cash up until 2014. A 2013 regulatory change has also restricted what the fund can do when it comes to borrowing. Independent says it is “not permitted to employ gearing whilst it continues to be a small registered UK Alternative Investment Fund Manager (AIFM)”. That’s a new one on me, I have to say.

Ward also admits he’s no good at predicting short-term market movements. No one is, of course, but few people are prepared to admit it! But this means Independent is unlikely to be a fund that’s going to go heavily into cash because its manager thinks a crash is around the corner.

The portfolio today

Given Ward’s financial crisis comments, you might expect Independent’s portfolio to be a housing-free zone.

Far from it. Sector-wise, it’s his second biggest holding at 17%. Technology leads the way with 26% and Travel & Leisure takes bronze with 16%. On housing, Ward cites the chronic undersupply of housing and planning regulations giving larger house builders a huge competitive advantage as the main reasons for his bullishness.

Drilling down to individual stocks, Fevertree represents 12% and Blue Prism 11%. Other notable holdings are Ashtead and Redrow (both 6%), Herald Investment Trust, Midwich and On The Beach (all 5%), Crest Nicholson and FDM (both 4%), and Seeing Machines (3%).

The top 10 holdings, therefore, account for 62% of total assets – or at least they did as of 30 June. Many of these share prices have headed south since, so the next portfolio list might look a little different.

But the entire portfolio only has 36 holdings, so it’s certainly a concentrated affair.

Partial to new issues

One thing that struck me is that Ward has got a lot of newly listed companies in his line-up. This is mentioned in the commentary covering its recent results, but it wasn’t something I was aware of prior to this review.

Fevertree and Blue Prism have both been exceptional performers arising from this strategy. But there are a few turkeys in there as well. Independent had stakes in Luceco, Footasylum, Alfa Software and Quiz. All of these have been far from glorious, although you would expect to see a high percentage of misfires with such an investment approach. Expect a bumpy ride if you board this train!

In fact, looking at the list of holdings from 5 years ago, it’s amazing to see how little has survived. I only see 4 stocks held back then that were still held in June 2018. Gone are the miners, oil producers, the tobacco firms, drug giants and utilities. In fact, the 2013 version of Independent Investment Trust almost seems like a closet tracker!

Independent cites its long-standing holding of Herald Investment Trust as giving it the confidence to begin reshaping its portfolio from 2014 onwards. With Ward then aged 65, it’s great to see he was still looking to reinvent himself in search of better returns. So far, it’s definitely paid off.

Not much of a dividend

As you may have already guessed, Independent is not an income-orientated fund. Therefore, I’ll keep this section short.

The dividend remained at 5p from 2007 all the way through to 2016, although special dividends of between 0.6p and 3p were paid in most years.

Last year’s distribution was 6p plus a 2p special, giving a yield of 0.9% (or 1.2% including the special payout).

There’s a lot to like with Independent

I definitely found myself warming to both this fund and its manager while researching this article and I am going to put Independent Investment Trust on my unofficial watch list.

I like funds that make a real effort to do something a little different but remain humble when doing so. And the low costs are also a great indicator of where their priorities lie.

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!