One of the attractions of the investment trust sector is the way it regularly renews itself, backing its winners and cutting loose what doesn’t seem to work.

But I recently came across a really surprising set of statistics in an article by Ian Cowie on interactive investor. In it, he quoted Numis Securities:

Out of 326 funds launched between 2000 and 2009, some 254 no longer exist. That is an attrition rate of 78% and another 11 trusts (or 3% of the total) have adopted a realisation strategy, while seven trusts (2% of the total) have merged with another fund.

This means that only 54 trusts (or 16%) of investment trusts launched over the last decade survived to see out their second decade.

In other words, only one in six trusts launched in the 2000s is still with us today.

That’s amazing, even when you consider that the global financial crisis probably resulted in a major shakeout.

Wave of mutilation?

Numis reckons another wave of investment trust consolidation could be with us soon, courtesy of the disparities thrown up by the coronavirus crisis.

It highlights £200m in market cap as the magic number — below this level, many wealth managers are reluctant to recommend trusts due to liquidity concerns.

Of course, trusts below this level tend to be more expensive in terms of annual charges, as it’s not much cheaper in absolute terms to run a smaller fund.

They are often reluctant to buy back their shares to reduce any discount to net asset value, as this shrinks their market cap even more.

There’s a surprising number of trusts that fall into this group. Out of around 350 trusts, about 55 have a market cap of below £50m and another 115 are between £50m and £200m.

So less than £200m translates into half of all existing investment trusts. Collectively, these are valued at around £14bn, making them the same size as Scottish Mortgage.

Numis reckons the average discount for trusts below £200m in market cap is 20% and it’s 25% for those under £50m. There’s plenty of scope for mergers or acquisitions it would seem.

It’s started already

Announcements from two trusts earlier this week suggest the consolidation process is now underway.

On Monday, M&G said it had made several approaches to the board of UK Mortgages, most recently offering 67p per share, which would value the trust at £183m.

M&G’s latest offer represented a 21% premium to Friday’s closing price of 55p per share. But it’s still way short of UK Mortgages’ latest net asset value of 79.4p per share (as of the end of May).

UK Mortgages was launched in July 2015 and its shares traded at a small premium up until this time last year. Then it revealed it was dropping its 6p annual dividend target to 4.5p, causing its shares to slump to a double-digit discount.

Earlier this year, due to the widespread introduction of mortgage payment holidays, the annual run-rate for the dividend fell again, this time to 1.5p.

Since the hostile bid was revealed, UK Mortgages has said it will reinstate its 4.5p dividend target and it is also planning to buy back some of its shares. It’s not going down without a fight, it would appear.

However, UK Mortgages has rarely been in the black since it was listed. The AIC’s performance charts show the maximum share price return since inception was 4%, and that was back in October 2018.

Now, just over five years since the trust floated, shareholders are underwater by nearly 20%, even after the pop caused by this week’s unsolicited offer.

The second trust with news was HWSI Realisation, which jumped 90% on Wednesday morning after it recommended a 55.5p per share offer that valued it at £90m.

At the end of 2019, HWSI announced a strategic review and in February of this year, it proposed a managed wind-down.

Before this news, HWSI shareholders had been underwater by 41% since the trust floated in 2016. After the share price jump, they would now be in profit by some 12%.

Debt & leasing: the terrible twins

I’ve written before about my inherent caution and general dislike for these trusts that specialise in debt. I tend to lump in the leasing trusts in the same group.

My background is very much equities and I’ve always found fixed income hard to get my head around.

There are 40 trusts in the leasing and debt sectors right now and it looks ripe for further consolidation.

19 of these have market caps of between £50 and £200m, and 7 are valued at less than £50m. Only 2 trusts have market caps over £500m.

Here’s what each sub-sector invests in:

- Leasing — Provides asset finance. Four of the six funds lease passenger aircraft, one specialises in ships, and one in a wide variety of assets. Largest two trusts are Amedeo Air Four Plus and Tufton Oceanic Assets.

- Debt: Direct — Loans are made directly to corporates, institutions etc. Largest two trusts are Biopharma Credit and Pollen Street Secured Lending.

- Debt: Loans & Bonds — Invests in government or corporate debt that can be (relatively) easily traded on a public market. Largest three trusts are NB Global Floating Rate Income, CQS New City High Yield, and CVC Credit Partners European Opportunities.

- Debt: Structured Finance — Invests in more esoteric debt instruments like mortgage-backed securities and collateralised debt obligations (aka the debt version of juggling lit sticks of dynamite). Largest two trusts are Blackstone/GSO Loan Financing and Fair Oaks Income 2017.

- Debt: Property — Loans securely against specific properties. It’s worth noting that UK Mortgages isn’t included in this group as it sits under Structured Finance. Largest two trusts are Starwood European Real Estate and Real Estate Credit Investments.

The going gets tough

2020 has not been kind to these 40 trusts. Their collective market cap fell from £10bn to £7.8bn over the first six months of this year.

Most of the sub-sectors fell between 15% and 20% but the leasing sector, heavily linked to air travel, saw its value slump by 50%.

But the coronavirus isn’t the only problem here. A lot of the trusts were on shaky ground already, as the table below shows. The numbers in brackets indicate how many trusts are included in each performance figure:

| Sector | 1 year | 3 years | 5 years | 10 years |

|---|---|---|---|---|

| Leasing | (6) -53% | (5) -64% | (5) -58% | – |

| Debt: direct | (11) -14% | (10) -9% | (3) -3% | – |

| Debt: loans & bonds | (11) -6% | (10) -2% | (9) +13% | (5) +81% |

| Debt: structured finance | (8) -30% | (7) -26% | (6) +2% | (2) +259% |

| Debt: property | (4) -17% | (4) -8% | (3) +1% | (1) +99% |

| All 5 sectors: share price | (40) -21% | (36) -18% | (26) -7% | (8) +128% |

| All 5 sectors: NAV | -5% | +9% | +22% | +96% |

I’m using straightforward averages based on share price total return here rather than market-cap weighted. The figures are as of 30 June 2020.

Collectively, these trusts have lost money over the past one, three, and five years, with the leasing sub-sector being by far the worst performer.

Widening discounts are a big part of the story although, particularly in the case of the leasing funds, net asset values are only updated every 3-6 months, so they could well be tracking some way behind the actual situation.

Over the last few years, the yields on these trusts have typically been between 5 and 10%, so they have probably attracted large numbers of income seekers.

The average debt/leasing trust was on a discount of 20% as of 30 June. The loans and bonds sector enjoyed a mild 2% discount while direct lending (26%) and leasing (56%) were the widest.

In fairness, some of the worst-hit trusts have been taking action to try and resolve their issues. HWSI was in wind-up mode and I think three others in the direct lending sector are going through a similar process (SQN Secured Income, RDL, and SME Credit). This means they are gradually selling off their investments and no longer making any new purchases.

SQN Asset Finance in the leasing sector has just changed managers, with its main share class surviving a continuation vote but its C shareholders voting to wind down their part of the trust. The main share class will have another continuation vote next year.

The long-term picture

The 10-year stats for the debt trusts are a little more reassuring but there’s a wide range hidden with the average figures.

Two trusts have lost money over the last decade, the aptly named NB Distressed Debt (-18%) and the now tiny Carador Income (-8%).

Five trusts sit in a wide middle band of +72% to +156% and then there’s Volta Finance at +528%.

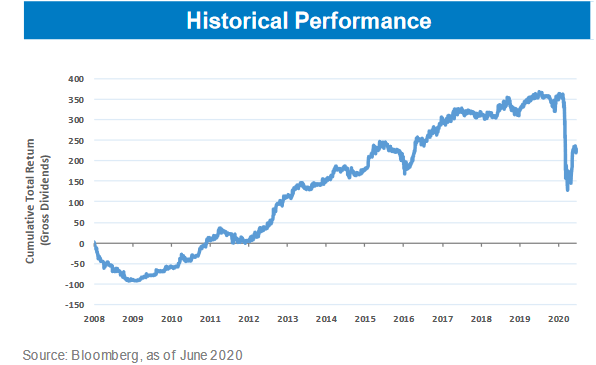

Volta is run by AXA and looks to provide leveraged exposure to “corporate credits; sovereign and quasi-sovereign debt; residential mortgage loans; commercial mortgage loans; automobile loans; student loans; credit card receivables; leases; and debt and equity interests in infrastructure projects”.

It’s at the high-risk end, therefore. Volta is down 20% over the last three years and it looks like it almost got wiped out completely in the global financial crisis.

Volta Finance performance chart

It’s worth remembering that most of these debt trusts aren’t very old.

Two trusts date back to the 1990s and five to the 2000s.

Half of the forty joined the market from 2013 to 2015, with only a couple of new trusts launching a year during the rest of the 2010s.

Therefore, the majority of them weren’t around during the global financial crisis or the euro debt crisis that came along a few years later. The coronavirus has provided their first major test and many have been found wanting.

Look at what you could have won

With such a wide range of investing briefs, it’s tough to come up with a single benchmark to measure their performance against.

Most of them don’t seem to invest in government bonds or investment-grade corporate debt to any great extent. As the AIC has said, “investors need to understand these companies present higher risks and rewards than mainstream bonds”.

But the passive funds investing in UK corporate bonds give us a crude idea of what we might expect. These have returned between 5% and 6% a year over both the last 5 and 10 years.

That suggests total return figures of +30% and +70%. Given the debt trusts invest a little further up the risk scale, I’d say we should be looking at maybe 40-50% over 5 years and 80-100% over 10 years.

Not many of the debt trusts can match these figures but Invesco Enhanced Income probably comes closest.

It’s the second-best 10-year performer returning 155% and has a decent 5-year record, too. 27% of its portfolio was in investment-grade bonds (A and BBB) as of June 2020, 55% was in BB and B-rated, and the rest was in lower-rated or unrated bonds.

Even with its small single-figure discount, with a market cap of £120m, this is another trust that’s been cited as ripe for consolidation.

Citywire’s most recent Trust Watch round-up suggested a merger with City Merchants High Yield, run by the same team at Invesco and worth £180m, might not go amiss.

Both these trusts announced a manager reshuffle this morning, though, with two of their three co-managers stepping back after nearly 20 years and the third stepping up to be the main manager.

The M&G Credit Income trust, with around 80% in investment-grade bonds, looks like a lower-risk option than the two Invesco trusts. However, it’s only returned 1% in the 20 months since it launched. I’m surprised to see it plunged 30% at the height of the crisis in March although it had recovered most of those losses a few weeks later.

With an ongoing charge of 0.93%, it’s a lot more expensive than passive fixed-income funds and I think it’s tough to catch-up such a gap when investing in lower-risk/lower-return assets.

Summing up

I’ll probably need to up my allocation to fixed income at some point, but the passive government-debt route appeals to me much more, as I’m largely interested in balancing out see-sawing equity returns.

If you’re attracted by large discounts and looking at shorter-term opportunities, a different game entirely, then I’d say you need to look at the detail of continuation votes and tender offers to see if there’s a realistic route to these trusts getting back to their net asset value.

But there’s no guarantee that the net asset value won’t deteriorate while a trust goes through the process of winding up, as that can take a few years.

If you do get your timing right then, of course, there could be handsome rewards, as we’ve just seen with HWSI.

Another recent example is RDL Realisation. Had you bought it in April 2019 you would have been 60% ahead in just a few months. Its shares did fall back from that peak, but they are up a very respectable 20% so far in 2020.

But had you bought into RDL when its wind-down plan was unveiled in September 2018, you would still be in the red today, even if only by a few per cent.

It occurred to me that one play this sector might be through Miton Global Opportunities. Run by industry veteran Nick Greenwood, it’s a kind of special situations fund for investment trusts.

However, a glance through its portfolio as of April 2020 seemed to indicate it only held 0.4% in Tufton Oceanic Assets, the one leasing trust that hasn’t been a total disaster (it’s down 1% since launch in late 2017), and nothing from the other four debt sectors.

It seems I’m not the only person who thinks these trusts sit firmly in the ‘too hard’ pile.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Another good article IT Investor.

I agree a lot of these debt investment trusts look unsustainable, particularly the trusts involved with leasing. I had a look at some of them last year as a way of maximizing the yield from my portfolio, but thought better of it. Like you said, I cannot get my head around them.

I decided on the equity investment trust route, with a selection of some quality global trusts. The starting yield maybe smaller, but if they can keep dividend increases up (hopefully above inflation). After a few years the total amount of dividend received as a percentage of the original investment should be well above these debt trusts. Plus the added benefit of a larger market cap, lower fees and a proven formula.

I always think the only people making money are the managers for these sort of investments. I get my risk kicks through quality VCTs. My investment horizon is 50+ years for my children and 5-10 years for me so happy to sit these out.

Thanks Sephy, sounds like a good long-term move to me.

Yes J. I only touched on it in the article but most of these trusts seem to be pretty pricey, partly because they are quite small. The M&G one I mentioned seems to be one of the cheapest – most of the others are well over 1% withI some over 2%!

I suspect there will be a few other situations like UKML and HSWL where some folks make quick gains, but I lack the skills to spot them. There’s no need to play every game 🙂

I looked at some of these a while back, and concluded that they belonged in my ‘too hard’ pile.

Before I go on, I suppose the debt ‘elephant in the room’ is that when interest rates have gone down for 35 years, it’s arguably hard to know if a manager has been skilful or just lucky.

I admit trusts like Volta are tantalising – perhaps if you were a specialist in this space (i.e. where many don’t understand it) then you could do very well.

Twenty Four AM always seem to have a good reputation (and a well-aligned boutique) though TFIF has stumbled in the past few years. Again I’m sure an expert would be able to explain how conditions have changed to make the strategy not work any more.

And the CQS High Yield Trust always seemed to have a decent reputation, though again I don’t really understand the ins and outs of high yield risk-wise.

And finally I was intrigued by Chenavari’s Toro. They had explosive results with their hedge fund strategies post-2009 – one of which was then put into a closed-end fund, but again I suspect once rates got to near zero in about 2016 meant the strategy didn’t work as well.

Another of their hedge strategies rocketed up in March 2020, so they appear an impressive outfit – again it’s a case of knowing which of their strategies is appropriate for each environment.

I am happy to let others allocate to debt funds on my behalf as appropriate e.g. through Capital Gearing Trust. Incidentally if you’ve read the latest CGT quarterly, Peter Spiller also discusses the issue of size and ITs.

p.s. I’ve been listening to the Pixies lately too…

Thanks again for your insights, Tom. I’ve seen Volta riding high in the 10-year performance tables for a while now but never looked at it closely before. I was surprised to see just how poorly many of these funds did before the pandemic in an era, as you say, when rates were falling so much and you’d expect the wind to be at their back.

I was tempted to throw in a load more Pixies sub-headings: Broken Face, Gouge Away, I Bleed, and Where Is My Mind? might have been approriate here!