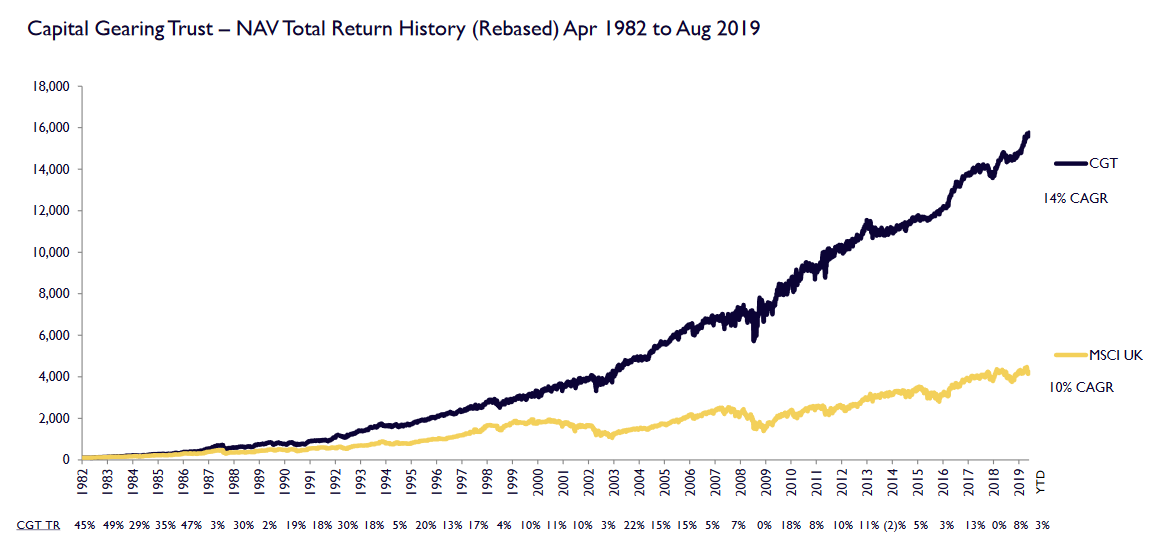

If you’re looking for an investment company that can bolster your portfolio’s defences then Capital Gearing Trust might fit the bill. Since Peter Spiller took over in 1982, it’s had just one down year in net asset value terms. Even then, it lost just 2.5%.

Capital Gearing Trust’s dual objectives are to:

- preserve shareholders’ real wealth; and

- to achieve absolute total return over the medium to longer term.

It’s achieved both with aplomb. The row below the chart (you can click to enlarge it) shows the return by year.

Since 1982, in addition to the 2.5% drop mentioned earlier, there have been two 0% years and five gains between 2 and 4%.

Double-digit gains have been posted in 22 out of 37 years.

It’s a truly outstanding record.

Key stats for Capital Gearing Trust

- Listed: 1973

- Manager: Peter Spiller (since 1982) / Alistair Laing (since 2010)

- Ticker: CGT

- Recent price: 4,310p

- 10-year net asset return: +85%

- Indicated spread: 4,300p-4,320p (0.5%)

- Exchange market size: 100

- Market cap: £454m

- Premium to net assets: 2.0% (NAV as of 18 Nov)

- Costs: 0.7% OCF, 1.0% KID

- Gearing: 3% cash as of 31 Oct 2019

- Current dividend and yield: 35p incl. 12p special / 0.8% incl. special

- Year-end: 5 April

- Results released: May (finals) and Nov (interims)

- Sector: Flexible Investment

- Wind-up vote: No, unlimited life

- Links: Website and AIC page

A slow start

Capital Gearing Trust may sound like it’s an industry veteran but it’s a little younger than you might expect.

Although it was incorporated in 1963, it was not listed on the London market until 1973 when it boasted a Major, a Lieutenant Colonel, and a Captain among its four directors.

It got off to a fairly inauspicious start, to say the least.

The annual accounts to April 1974 show net assets sliding from £0.7m to £0.2m. The company’s investments were £0.9m but it had debts of £0.7m, mostly in the form of mortgages.

Roll forward to April 1982 and its portfolio of other investment trusts and life assurance policies had grown to £1.5m. With debts around the same level, net assets had risen to £0.7m.

So, admittedly during a very tough time for UK equities, Capital Gearing’s net assets were broadly unchanged for its first nine years as a listed company.

Peter Spiller then took over as manager and things began to improve, helped of course by the roaring bull market of the 1980s and 1990s.

Riding the big bull

By April 1990, net assets had risen to £5.5m.

The mortgages were gradually being paid off, so the level of borrowing was now far lower. The portfolio was mostly investment trusts with split-capital funds accounting for around two-thirds of the total.

Move forward another decade to the year 2000 and net assets were now £23m.

Investment trusts still accounted for lion’s share of its portfolio — £20m out £23m — but it had become a lot more defensive with around 20% of its underlying assets in fixed income and 50% in zero dividend preference shares.

It was around this time that Spiller left his other job as a partner at Cazenove and helped set up CG Asset Management (CGAM).

CGAM runs four open-ended funds in addition to Capital Gearing Trust, managing just over £2bn in total. Its founding principles are simply but effectively put as:

- The client comes first

- Don’t be greedy

- Have fun!

Dealing with the financial crisis

Capital Gearing’s reports for the years ending April 2008 and April 2009 make interesting reading now that we’re armed with the knowledge of massive hindsight. In the former, there is a comment that certainly hasn’t aged well:

“what is credible is that the problems associated specifically with the sub-prime market in the US are now solved, at least in the banking system, by the large amount of equity raised; for hedge funds, whose accounting is less rigorous, there may still be problems yet to be disclosed.”

Capital Gearing maintained its very defensive stance, though, resulting in an unchanged level of net assets over the next twelve months. The share price rose, though, with a 0% discount becoming an 11% premium.

The portfolio today

Capital Gearing’s approach is “long-only investment in quoted closed-ended funds and other collective investment vehicles, bonds, commodities and cash, as considered appropriate”.

It has no country or sector restraints and it can borrow up to 20% of net assets although I don’t think its portfolio has been geared for a long time.

Spiller has remained very bearish over the past two decades. This 35-minute interview from three years ago adds a lot of colour if you want it. This AIC interview is a much shorter version. And this research note from Quoted Data has lots of useful data points on both Capital Gearing Trust and the wider CGAM strategy.

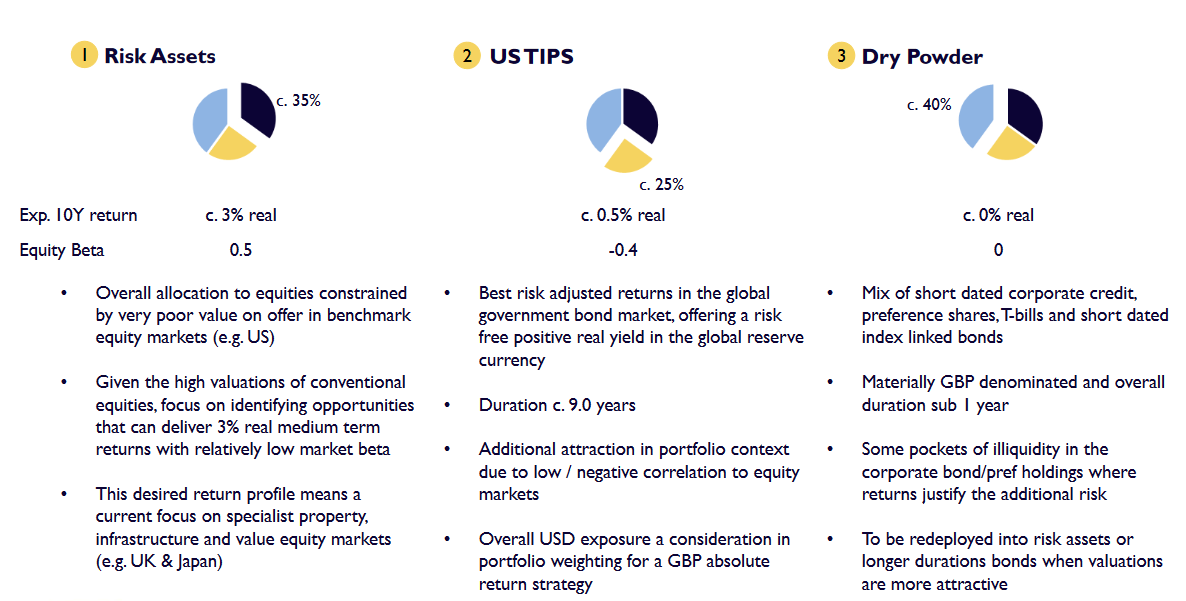

The CAGM team believes real returns in most assets are likely to be very low over the medium term, with inflation likely to re-emerge at some point.

To reflect this view, they own selected equities and bonds where they see the most value plus a high percentage of ‘dry powder’ that can be deployed should prices crash and general valuations become more attractive.

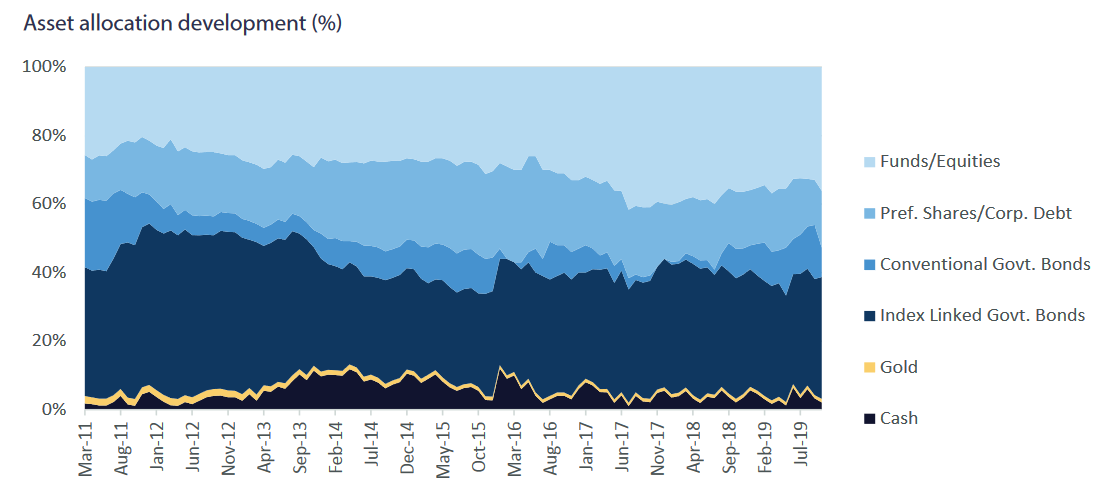

The level of index-linked bonds and cash (i.e. the dry powder) has ranged between around 35% and 50% of net assets for a while now:

Here’s the latest portfolio breakdown with some additional detail in brackets:

- Index-linked government bonds: 33% (mostly US, some UK)

- Conventional government bonds: 16% (all UK)

- Funds/equities – equities: 15% (e.g. UK/US/Japan/Emerging Vanguard ETFs, Investor AB, North Atlantic Smaller Companies)

- Preference shares and corporate debt: 13% (mostly short-dated and UK)

- Fund/equities – property: 12% (e.g. Vonovia, Deutsche Wohnen, Castellum, Grainger, Tritax Big Box)

- Fund/equities – loans: 3%

- Fund/equities – infrastructure: 3% (e.g. Renewables Infrastructure Group, Greencoat Renewables)

- Cash: 3%

- Fund/equities – private equity: 1%

- Gold: 1%

So, even though nominal fund/equity exposure is about a third of net assets, more than half this amount is in alternative assets like property and infrastructure.

The full portfolio listing as of October 2019 has 190 separate positions, so there’s a pretty long tail of minor holdings.

Management and directors

Spiller is now 71 and is reckoned to be the longest-serving fund manager in the entire industry, so it’s no surprise to see that the team running Capital Gearing has been bolstered in recent years.

Alastair Laing (42 years old) has co-managed the fund since 2010 having previously been at HgCapital and Deloitte. Chris Clothier (40 years old) joined in 2015.

I haven’t seen any specific details of when Spiller might retire but the ground has been laid for some time now, which is excellent to see.

Spiller owns some 0.4m shares, worth some £17m, having increased his holding by about a third a few years ago.

The trust’s directors own around 42,000 shares (£1.8m). That figure includes Alastair Laing, who is a non-exec. He owns 14,623 (£0.6m).

Spiller was a director from 1986 until 2014 but no longer sits on the board.

The discount control policy

Spiller has been critical of other investment trusts in the past for letting their premiums or discounts get too large. However, it wasn’t until 2015, after a prolonged period when Capital Gearing’s premium was around 10%, that it put its own house in order.

Its discount control policy aims to keep the share price around the same level as its net asset value, buying shares when they are at a discount and issuing more if there are at a premium.

It’s largely been the latter these past four years with the share count more than tripling from 2.9m to 10.6m. Capital Gearing’s market cap has risen from just under £100m to just over £450m — its share price has increased by 30% over this period.

Normally, such a rapid rise in the share count would be concerning. But Capital Gearing treads so carefully and most of the assets it buys are extremely liquid, so it’s been able to invest the cash raised from these new shares with relative ease.

Charges

CG Asset Management Limited receives an annual management fee based on:

- 0.6% of net assets up to £120m;

- 0.45% between £120m and £500m; and

- 0.3% over £500m.

The last of these tiers is yet to kick in, but it looks like it will do soon, thanks to the new shares being issued.

These tiered rates have helped push the ongoing charges figure down to 0.7%, which seems fairly reasonable for a fund of this size. The basic management fee was 0.85% on gross assets a decade ago, so there has been a noticeable move down since then.

Dividends

Although the ‘Gearing’ in Capital Gearing Trust seems a little redundant these days, it’s definitely a trust that aims for capital growth rather than prioritising income.

The basic dividend has risen steadily over the last 20 years from 5p to 23p, being held in three years and increased in all the others. But the basic yield works out at just 0.5%.

Special dividends were paid in 1992, 1998 and every year from 2003 to 2012. They reappeared in 2018 (6p) and 2019 (12p).

Dividends are paid annually in July.

Summing up

It’s hard to argue with the numbers Spiller has delivered, whatever you think of his bearish views.

I’m a long-term bull by nature (i.e. I think that markets tend to rise over time but not in any predictable fashion) and I’m not looking to time the market.

But as I get wrinklier, I want to get a bit more defensive and I’m increasingly drawn to funds like Capital Gearing Trust.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Nice write-up IT (as always).

I have been transitioning my portfolio to fossil-free this year and unfortunately I had to sell my holding of this trust to complete the process due to its weighting to the FTSE100 ETF.

I have been in correspondence with Mr Laing trying to persuade them to avoid the oil companies but I get the feeling they are not (yet) so switched on to the threats from climate. That said, I was pleased to see the addition of the renewables earlier this year but I suspect that was purely for income rather than a concern for the environment.

Thanks, DIY. Yes, I would suspect a fund like CGT is probably going to be a laggard when it comes to full-on environmentally friendly investing. I didn’t pick up any references to it when reading their recent reports.

Thanks for the comprehensive writeup.

I noticed that the manager also launched an equivalent open ended fund (CG Absolute Return Fund). Would be interested to hear your thoughts on this vs. the trust. Performance seems to be very similar but from what I’ve gathered, the open ended fund prefers ETFs over ITs for size? For the same risk profile, the open ended fund would save a bit of entry cost from savings in stamp duty.

@PK — It looks like the open-ended fund has underperformed the investment trust by about 2% in total since it launched in May 2016, so I guess that needs to be weighed up against any stamp duty savings. However, that 2% gap only seemed to open up in the last few months so it may not be permanent and there have been periods when the open-ended fund has been ahead by a similar margin.

I guess it’s also worth considering that if CGT ever got more bullish (which seems a distant prospect for the foreseeable future!) and decided to use its borrowing powers then you would expect the open-ended fund to lag behind a little at that point. That’s assuming, of course, that CGT called the markets correctly and was right to gear up.

Quoted Data has reviewed both CGT and the Absolute Return fund a few times in the same research note so it might be worth looking at those to see if they highlight any other differences. I didn’t see much on a quick review.

https://quoteddata.com/company/capital-gearing-cgt/