Whenever I see an investment trust trading at a discount of nearly 50%, my spidey sense starts tingling. There’s either a great opportunity… or great danger. Tetragon Financial Group is one such example. Having seen it mentioned in enthusiastic terms a few times in recent months, I decided it was worthy of a closer look.

Considering my last article highlighted the hidden risks of alternative asset funds, there’s more than a touch of irony here. While Tetragon is classed as ‘Flexible’ by the AIC, it invests in a wide array of what are usually considered alternatives.

Nevertheless, I find writing these articles is a great way to learn more about a potential investment. Even if I ultimately decide it’s not for me, I always find it a worthwhile exercise.

Certainly, there is a lot about Tetragon that many will find off-putting. Its corporate governance is horrendous (all the voting shares are controlled by its co-founders) and its charges are eye-watering. It also has complexity in spades.

That’s a lot to get past, but it might just be worth the effort…

What it does

Tetragon was set up as a Guernsey company in 2005 and became publicly listed in 2007. However, it did so via the Amsterdam Euronext exchange, for reasons I haven’t been able to ascertain.

It joined the London market in 2015 with the ticker TFG and is quoted in US dollars.

All its financial information is in US dollars, too, as are its dividends. A sterling-quoted class of share (TFGS) was introduced in April 2018.

What Tetragon invests in is perhaps best described in the first video from its most recent investor day:

- 25% in various asset management businesses covering include equities, debt, property and infrastructure.

- 40% invested with those same asset management businesses.

- 10% invested in external funds.

- 10% held directly in various listed investments.

- 15% in cash.

The figures have shifted a little since, but not too much.

Asset management is an inherently attractive business model, with fees charged on a percentage of assets managed whereas costs don’t tend to grow in the same proportion. That’s not always great for us investors of course!

Key stats for Tetragon Financial Group

- Founded: 2005

- Listed: Amsterdam Euronext (2007), London (2015)

- Co-founders/key players: Paddy Dear (58) and Reade Griffith (53)

- Tickers: TFG ($) and TFGS (£)

- 10-year net asset return: +257%

- Current price: $12.35 / 978p

- Indicated spread: $12.25-$12.45 (1.6%), 964p-992p (2.9%)

- Exchange market size: 1,000

- Corporate governance red alert: 10 voting shares controlled by Dear and Griffith, all listed shares are non-voting

- Results released: end of Feb, end of Jul

- Market cap: $1.2bn / £940m

- Net assets / discount to net assets: $22.48 / 45%

- Costs: 2.0% OCF and 5.7% KID

- Gearing: zero, 12% cash as of 31 Dec 2018

- Current dividend and yield: 71.6c and 5.8%

- Dividends paid: Mar, May, Aug, Nov

- Style: Range of assets including private equity, debt, infrastructure and property

- Links: Website and AIC page

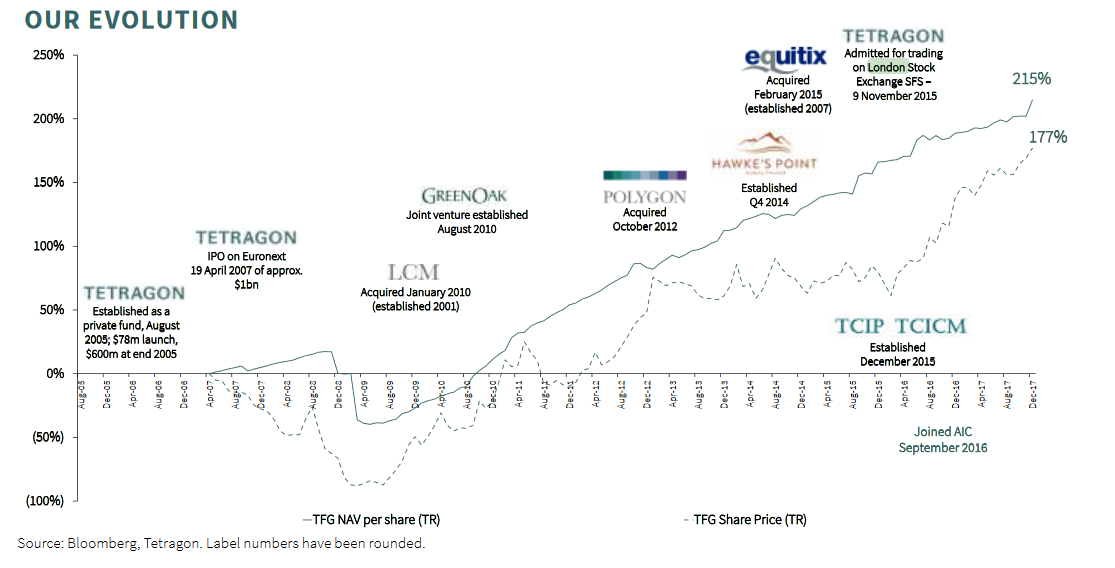

A chequered history

You can read more about Tetragon’s back story in this excellent Wexboy post from 2013, so I’ll just summarise some of the juicy bits here. (This 2016 Forbes article adds some more recent colour).

Tetragon was set up by Jeffrey Herlyn, Michael Rosenberg, David Wishnow, Reade Griffith, Alexander Jackson and Paddy Dear, some of whom founded an investment firm called Polygon in 2002.

Wexboy described Polygon as “a high profile firm in the boom years, with a top reputation as an aggressive credit, convertible, event-driven & special situations investor”. Both it and Tetragon nearly blew up in the financial crisis a decade ago.

Five of the six Tetragon co-founders remain on the investment committee today. Alexander Jackson left under a cloud in 2011 over a strategy disagreement and his place on the committee is now occupied by Stephen Prince.

Dear (the smooth talker) and Griffith (the bruiser) are the main players, owning roughly 4% and 13% of Tetragon’s shares.

Wishnow, Herlyn and Rosenberg own another 2% between them, with other Tetragon/Polygon employees owning a further 8%.

That means an impressive 27% of the shares are held by insiders – they are definitely eating their own cooking.

Prior to the financial crisis, Tetragon seems to have mostly invested in debt instruments such as, eek, collateralised loan obligations (CLOs). You can probably guess what happened.

Although its net asset value dropped from $10 at launch to a low of around $5 in early 2009, Tetragon’s share price actually fell below $1 for a brief time. The discount to net assets at that point was in excess of 90%.

Reinvention

Following this humbling episode, Tetragon’s managers decided to broaden their brief, looking for other types of assets.

They also decided to take ownership stakes in asset management companies. It looks like it was a disagreement over this strategy change that led to Jackson leaving.

The strategy change was also what attracted Wexboy’s attention in 2013 and he still seems to own the shares from what I can tell. Looking at his posts, he also understands the exotic instruments that Tetragon invests in much better than I will ever do.

The chart below shows Tetragon’s share price and net asset value history, and also the asset management groups it has acquired along the way:

While the net asset value has risen to over $22, the share price has struggled to keep up.

The discount narrowed from 90% to 40% by the end of 2009, but it’s largely bounced between 30% and 50% ever since.

The asset management companies

| Name | Asset | Funds under management $bn | Valuation $m |

|---|---|---|---|

| LCM | Bank loans | 7.4 | 155 |

| GreenOak | Property | 9.4 | 209 |

| Polygon | Hedge fund/ private equity | 1.5 | 55 |

| Equitix | Infrastructure | 3.7 | 231 |

| Hawke’s Point | Mining finance | 0.02 | 1 |

| TCIP | CLO equity | 0.6 | 10 |

Note: funds under management as of June 2018, valuation as per December 2018 factsheet.

You’ll see Polygon in the mix. Tetragon’s founders essentially bought themselves out of their original firm along the way, pocketing a pretty juicy sum according to Wexboy’s calculations.

You might recognise the name Equitix as well, as it was involved in the buy out of John Laing Infrastructure Fund (JLIF) last year.

There’s also another business called TCICM which is connected to TCI. However, it doesn’t seem to be included separately in the valuation numbers, despite managing $3bn of assets, so I’ve left it out of this table.

Equitix and GreenOak are the only two firms not wholly owned by Tetragon:

- The Equitix stake is 85%, with the rest held by its Equitix’s own management. Tetragon’s holding is expected to reduce to 75% over time, presumably due to share awards to management and employees.

- GreenOak is a minority holding of 23%.

The valuations of both of these firms seem to have risen substantially in the latter half of 2018.

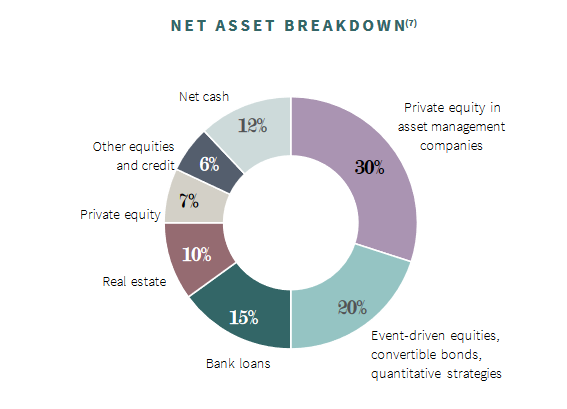

Other investments

Here’s how the remainder of Tetragon’s net assets are made up, as per its latest factsheet:

You might recall that Tetragon invests in funds run by the asset managers it owns. In fact, this seems to be mostly restricted to Polygon and GreenOak, which make up the majority of the event-driven equity and real estate categories.

What is an event-driven equity strategy you may ask? Basically, it’s a hedge fund looking to exploit pricing anomalies that can arise with announcements like corporate results, mergers, acquisitions, spin-offs, or under conditions of financial distress.

Depending on your point of view this is either the height of investment sophistication powered by complex computer algorithms or educated guesswork.

This same chart also illustrates how much Tetragon has changed over the last several years. In Wexboy’s 2013 piece, debt investments accounted for more than 70% of net asset value. Now bank loans and convertible bonds are around 20%.

On a geographic basis, over 90% is invested in the US and Europe, in roughly equal proportions. Financial complexity is largely a Western disease it would seem.

Despite the fact Tetragon is ungeared at the trust level, with 12% in cash, it’s worth remembering there could be a lot of debt in its underlying investments, particularly its bank loans/CLOs of course.

Added to that, most of its portfolio is difficult to value, not having a direct quote you can grab off Yahoo Finance or the London Stock Exchange website. It’s valued by an independent firm using ‘reasonable assumptions’.

The strategy of investing in both asset managers and their funds represents a doubling down of sorts, too. If these funds struggle, not only might Tetragon’s direct investment in them take a hit, the valuation of the fund managers it owns could suffer as well.

Different but repeatable

Paddy Dear describes Tetragon’s investment process as doing something different (i.e. giving the opportunity to earn better than average returns, or alpha in the jargon of the investment world) while also making the generation of ideas repeatable over time.

You can see this in action with the array of asset management firms being built up. Tetragon uses its knowledge of the industry to help each discrete operation grow and thrive.

Other types of alternative asset could be added to the mix in future. There doesn’t seem to be anything on the horizon at present, but management no doubt plays their cards close to the chest on matters like this.

At some stage, the aim is for the asset management side of Tetragon’s business to be listed itself, although there’s no timescale given for when this might happen.

Tetragon’s stated performance aim is 10-15% a year over the long term “across various credit, equity, interest rate, inflation and real estate cycles”.

To date, it’s managed just over 11% since it listed, so that’s at the bottom end of this range, despite the tailwinds enjoyed for the last decade (OK, it nearly got wiped out just before that).

That dastardly discount

Tetragon seems to be at pains to make itself more shareholder-friendly these days.

It’s held investor days, making cuddly references to the likes of Warren Buffett and Charlie Munger.

It’s introduced that sterling-based quote for TFGS.

It even touts itself as a low-risk, conservative investor, which seems somewhat of a stretch to put it mildly.

It has also bought back a lot of its shares in recent years. From listing to 30 June 2018, Tetragon spent $610m on share repurchases compared to $590 on dividends. A further $50m tender offer was completed last month.

Yet the big discount refuses to heal.

From owning Caledonia for many years, I know that big discounts like this can persist for ages. Sometimes they close, but it’s often not clear exactly why. Ultimately, it’s just more people buying its shares of course.

In Tetragon’s case, I think the combination of the lack of voting powers for its listed shares and its high charges are the two main things that need to be addressed for the discount to narrow. The latter seems particularly perverse to me, given the large insider ownership.

Those eye-watering charges

The management fee is 1.5% plus a performance fee of 25% over the hurdle rate.

1.5% is pretty punchy these days but the performance fee is a real kick in the teeth.

The hurdle rate is US dollar three-month LIBOR plus 2.65%. With that definition of LIBOR currently at 2.7% that makes the hurdle rate 5.35% right now. So it’s about half the bottom level of the target range of 10-15%.

Low interest rates have certainly helped to rake in the performance dollars since the financial crisis. The original hurdle rate, based on the same formula, was 8%.

You could say that the current low hurdle rate effectively turns the 1.5% management fee into a 3.0% total fee.

Fees are charged on asset value as well, so are much larger when stated as a percentage of the share price. The Key Information Document has them at 5.66%.

As a final poke in the eye, hat-tip to Wexboy on this as I didn’t spot it, there is no high water mark element to the performance fee.

In other words, previous losses are not assessed when each calculation is made. So performance fees would have been paid for the recovery in net asset value from $5 to $10 a decade ago, rather than only becoming payable once the net asset value exceeded the $10 level at listing.

Interestingly, the high level of fees even resulted in a couple of shareholder lawsuits a few years back, although both were unsuccessful. Daniel Silverstein led the first, Leon Cooperman the second.

Discounts with benefits

The hefty discount has some advantages of course.

It provides an element of downside protection for any investment, on the basis that it would seem more likely to narrow than to widen over a long timescale.

It makes those share repurchases a fantastic use of the money generated by its asset management operations. You’re buying £1 for little more than 50p.

And it magnifies the dividend yield. Relative to net assets, the yield is 3.2% but the hefty discount the share price sits at bumps this up to 5.8%.

Here’s how that dividend has grown over time, assuming an 18c fourth payment is made for 2018:

| Year | US cents |

|---|---|

| 2007 | 45.0 |

| 2008 | 48.0 |

| 2009 | 15.0 |

| 2010 | 31.0 |

| 2011 | 39.5 |

| 2012 | 47.0 |

| 2013 | 56.5 |

| 2014 | 61.8 |

| 2015 | 64.8 |

| 2016 | 67.3 |

| 2017 | 70.0 |

| 2018 | 71.8 |

That’s quite a hit during the financial crisis, although you’d hope the business is a little more resilient in its current form. It’s notable that dividend growth in the last few years has been much more sedate.

There are four sides to every story

If you’ve read this far, thank you for your patience, as I realise I’ve covered a lot of ground here.

This feels like the sort of investment I shouldn’t be making: high charges, only being able to buy non-voting shares, and it’s basically a hedge fund (which usually means excess pay and mediocre returns at best).

Indeed, at times, I felt dirty just writing this post.

But that near-6% yield is attractive, as is the potential kicker of the discount narrowing over time.

The net asset value return over the last 10 years is also impressive. True, it’s off a low base, but it’s rarely fallen and when it has, the decreases have been minor (although sometimes such steadiness is a classic warning sign).

The share price has been much more volatile than the net asset value, as you might suspect.

In terms of assets managed, Tetragon is ranked in the top twenty of all investment trusts. It’s a substantial operation.

And when it comes to the pound value of stakes held by investment trust management teams, it’s second only to RIT Capital Partners.

The 2018 results are due out on 28 February, so that should give me plenty of time to let this idea settle before I do anything rash!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Fabulous article, thanks for your thoughts and reference to further reading.

I am a recent buyer of TFGS (3% of portfolio) and did so not blind to the downsides you rightly highlight but on a (hopefully) balanced view of the investment case. For me the case for buying, in a diversified portfolio, is as follows:

– Substantial insider ownership

– Share tenders and buybacks

– Quarterly dividend and yield allowing income to be reinvested at 47% discount to NAV

– Substantial holding by BTEM (which I also hold) 5.4% of its portfolio

– Strong NAV returns over 3, 5 and 10 years

Thanks for those kind words, Richard.

I wasn’t aware BTEM was a major holder – interesting information!

Interesting writeup, I remember when Wexboy first started rattling on about this it all sounded very exotic. 😉

But eek, 5.66% effective fees — and I presume (haven’t looked at the accounts) that this does not include the extra fees on the 50% of NAV it is running with other companies. (Sometimes you see fee waivers but I’d be surprised to see it here. :))

Let’s generously call those 1.5%, and we could be looking at 7% fees here.

I think that discount makes sense! Perhaps it also makes the investment worth a punt at this price, but I can’t see why it would close, except in a wind-up or acquisition, which isn’t beyond the realms of possibility I suppose.

Yes, those fees are definitely off-putting. They are from the KID so unfortunately there’s not a breakdown of how it’s made up (other than 2.65% for management and 2.98% for performance) . I think it does include underlying fees paid to other companies but I’m not entirely sure. Not sure how the fees it pays to the asset managers it owns are accounted for however. Mind-bending stuff these cost figures sometimes!

@ITInvestor — Indeed! I would ask my fee maven buddy The Accumulator to take a look, but I suspect his head explodes if it encounters fee settings above 5%. 😉