Impax Environmental Markets is one of three funds in the AIC’s Environmental sector. It is both the largest (with assets of £600m) and the oldest (having launched in 2002).

Diy investor (uk) bought this fund last October and it’s been on my list to write up since then.

A little history

While Impax Environmental dates back to 2002, its fund manager, Impax Asset Management (Impax AM), has been going a little longer.

It was set up in 1998 and has been listed on AIM since 2001, making it very early to the party when it comes to environmental investing.

Impax AM is currently valued at £300m and it manages £14.5bn of assets in total. Therefore, Impax Environmental accounts for 4% of its total assets and it is the only investment trust it runs.

Ian Simm, Impax AM’s founder and CEO, presented at Mello earlier this year if you want to see more details on its fund management business and the broader case for environmental investing.

Key stats for Impax Environmental Markets

- Listed: February 2002 at 100p

- Managers: Jon Forster and Bruce Jenkyn-Jones (both since launch)

- Ticker: IEM

- 10-year net asset return: +191%

- Benchmarks: MSCI All Country World Index and FTSE Environmental Technology

- Recent price: 308p

- Indicated spread: 307p-309p (0.6%)

- Exchange market size: 1,500

- Market cap: £580m

- Premium to net assets: 2.1%

- Costs: 1.05% OCF and 1.48% KID

- Gearing (net): 2%

- Number of holdings: 63

- Current dividend and yield: 3p and 1.0%

- Results released: Apr (finals) and Aug (interims)

- Dividend paid: May

- Style: Global environmental focused on resource efficiency

- Continuation votes: every 3 years, most recently in May 2019 with 100% support

- Links: Website and AIC page

The mystery of ESG

One of the criticisms levelled at environmental, social, and governance (ESG) investing is that it’s a massively broad church.

One person’s no-go area is another’s shoulder shrug.

So it makes sense to start with how Impax Environmental describes its remit:

The Company’s objective is to enable investors to benefit from growth in the markets for cleaner or more efficient delivery of basic services of energy, water and waste.

Investments are made predominantly in quoted companies which provide, utilise, implement or advise upon technology-based systems, products or services in environmental markets, particularly those of alternative energy and energy efficiency, water treatment and pollution control, and waste technology and resource management (which includes sustainable food, agriculture and forestry).

I like the specifics given here and the fact it’s backing companies that are pro-active rather than just avoiding unethical businesses. And I also like the emphasis on technology.

One problem you can have with themed investments like this is that many industry players could be units within much larger global companies. You can’t invest in the bits you want without buying all the other gubbins that surrounds it.

Impax avoids this by concentrating on ‘pure plays’. They should generate “at least 50% of their revenues from sales of environmental products or services in the energy efficiency, renewable energy, water, waste or sustainable food markets”.

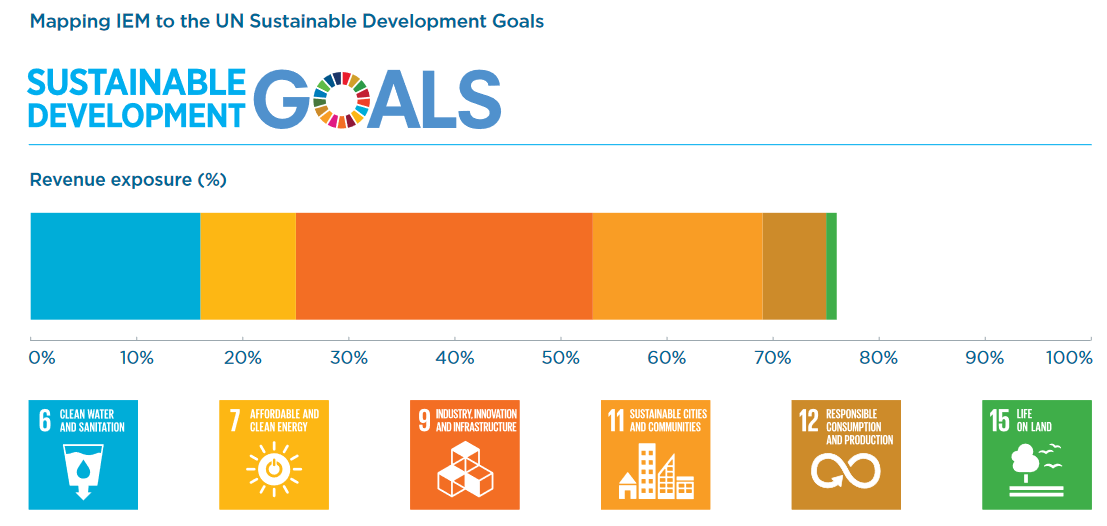

Right now, it far exceeds that 50% target with 74% of underlying revenues coming from these areas.

It also provides this useful graphic showing how that 74% is spread across the UN’s Sustainable Development Goals:

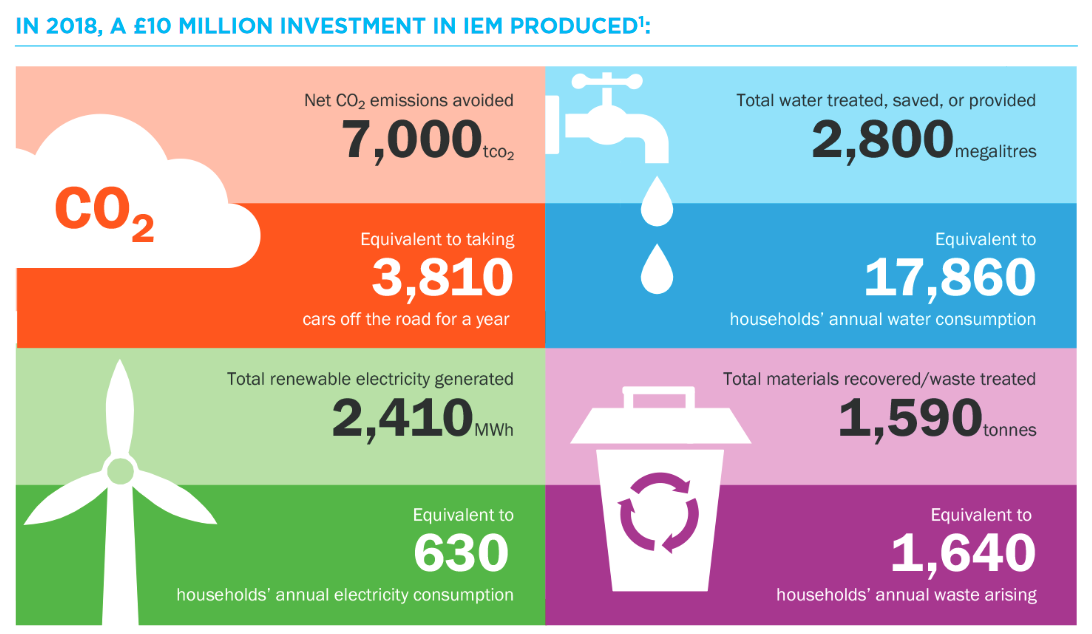

And if you need another chart to make you feel fluffy inside, here’s what a £10m investment in Impax Environmental theoretically does:

What’s in its portfolio?

I find these sort of breakdowns useful as I’m not familiar with many of the companies that Impax Environmental is invested in.

Looking at its top investments they:

- provide re-usable pallets and crates;

- improve efficiencies across industrial processes, such as remote asset tracking and optimising equipment operation;

- operate wind farms;

- generate geothermal energy;

- provide water and waste services;

- make water heaters/boilers and water/air purification systems;

- produce components for high-voltage power conversion systems in mobiles, PCs, TVs; and

- manufacture water treatment units, air purifiers, and water softeners.

Other up-and-coming themes discussed in its recent reports include electric vehicles, the war on plastics, and reducing the environmental impact of ‘fast fashion’.

Impax Environmental is invested in 63 businesses at the moment. Only one of these, Ensyn, is unlisted and it accounts for just 1% of net assets (it was written down from 1.8% earlier this year).

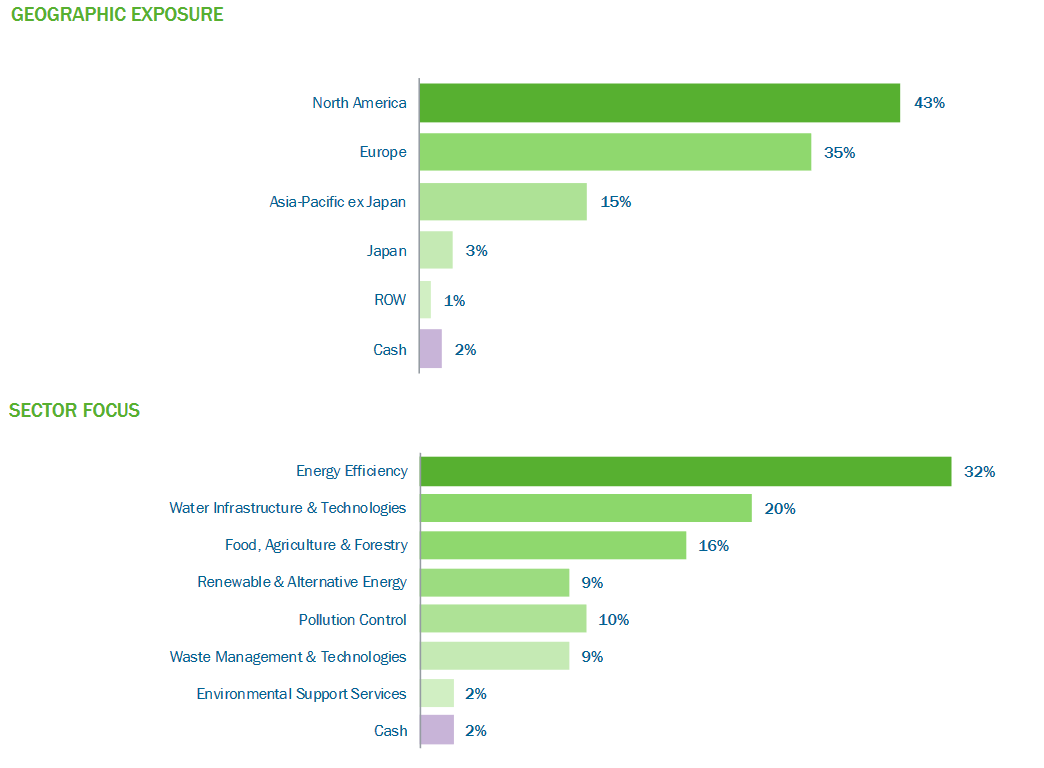

Impax seems to be sticking to developed markets for the most part, with 78% of its portfolio in North America/Europe and 18% in Asia:

It looks like a very evenly invested portfolio. 63 holdings and 2% cash suggests an average position size of 1.55%.

However, the largest position is just 2.7%. The top ten range from 2.1% to 2.7% and account for 24% of the portfolio. The most recent full list on its website suggests just 7 holdings were below 1% of assets.

Given the ‘pure play’ focus of the portfolio, many of the holdings are quite small companies. 18% of the portfolio consists of companies valued at $2bn or less. Nearly half, 46%, are worth in excess of $5bn.

Investing style

There is a Kepler research note produced in March 2019 which has some useful background on Impax’s investing style.

It describes Impax as “bottom-up growth stock pickers, but [with] a valuation driven methodology”. This has tilted the portfolio away from the US and glamour stocks such as Tesla and towards the more genteel valuations that can be found in Europe.

For the most part, Impax’s investments are profitable companies (or they will be very soon). Based on earnings estimates for the next 12 months, 97% by value of its investments are classed as profitable. According to Kepler, Impax sees “the most attractive investment point is when a profitable company with established technology is beginning to scale up”.

Lightly geared

Gearing tends to be relatively modest. Net of cash, it’s currently 2%.

There are two five-year fixed-rate loans ($20m and £15m) plus an undrawn £20m credit facility. So the maximum level of borrowings should be £50m, which is less than 10% of the current market value of £580m.

A powerful performance

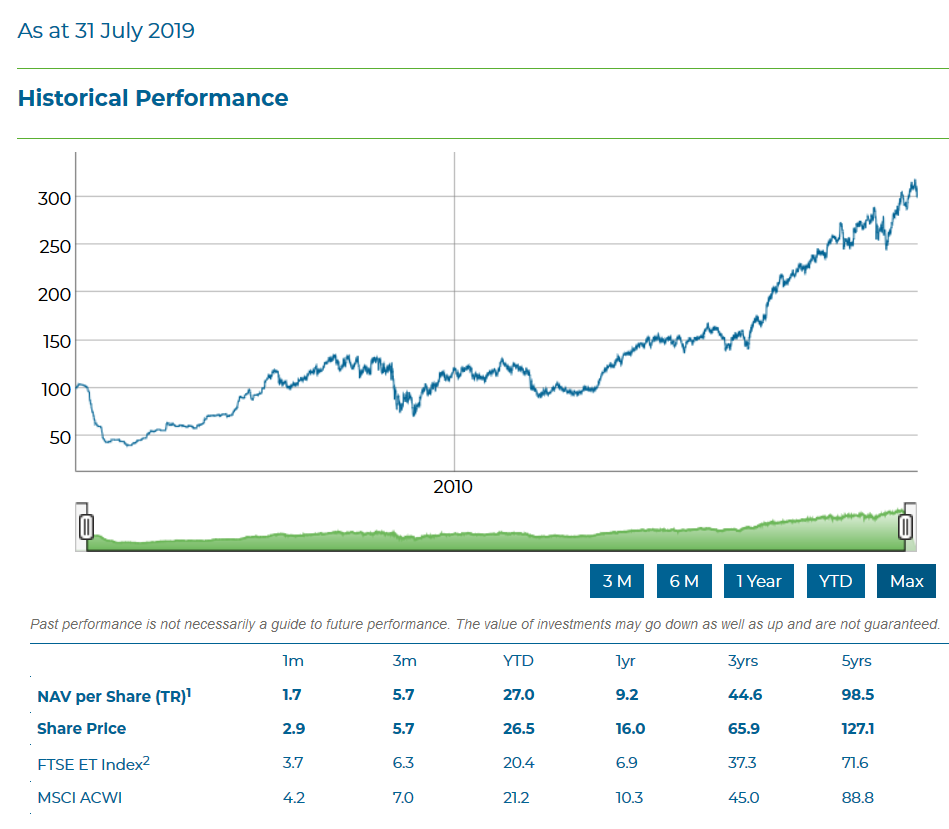

Despite its slightly low US weighting, Impax has still managed to keep pace with global markets over the last five and ten years. That’s no mean feat.

The chart shows that Impax Environmental has had its struggles over the years.

The share price fell from the issue price of 100p to as low as 40p in its first year as the tech bubble drew to a close.

In the financial crisis, it dipped from 13op to 75p.

Indeed, it took over ten years from launch for this fund to finally wave goodbye to its 100p flotation price.

Buybacks and share issues

From March 2009 to June 2017, Impax Environmental was a fairly habitual buyer of its own shares. Back then, it generally traded on a discount of around 10% to its net assets.

In 2017, the discount started to narrow, presumably as climate concerns started rising up the agenda and its investment performance was seen to have kicked up a gear or two.

Since October 2018, Impax Environmental has usually traded at a small premium and it has begun to issue new shares. In January 2019, it said that:

Given the potential for further share issuance, the Board recognises that existing shareholders and potential investors alike will welcome some clarification on its intentions regarding premium and discount management.

The Board therefore confirms that it remains committed to using its powers, including those to issue and buy back shares, in a proactive manner with the aim of seeing the shares, in normal market conditions, trading close to net asset value on a consistent and long-term basis.

The share count was over 300m when the initial buyback programme began in 2009. It dropped to as low as 180m before the recent share issues began. It’s now 188m.

The two managers

Both managers have been running Impax Environmental since it began. Long tenures like this are always good to see, in my opinion.

They joined Impax AM in 1999 and 2000, a couple of years before the trust launched. They also run a number of Impax AM’s other funds.

I couldn’t find their exact ages, but browsing LinkedIn and squinting at photographs suggests they are early or mid-50s. So, there’s a reasonable chance one or both could be moving on over the next few years.

But there does seem to be strength in depth across Impax AM. The trust has access to 16 investment professionals including Ian Simm, Impax AM’s founder, who chairs its Investment Committee.

I couldn’t find details on how many shares Impax employees, including the trust’s two managers, owned.

Dividends are low

As you might expect, most of the companies Impax Environmental owns don’t pay out much in the way of dividends.

The trust’s current yield is just 1% although the payout has grown substantially over the last ten years or so. The first dividend paid was 0.2p back in 2007. The latest was 3p.

Dividends are generally paid out of the revenue received each year. The payout has only fallen once, though, from 0.85p to 0.75p in 2010 and the current revenue reserve is about 1.5 times the most recent dividend.

Charges look decent

These don’t seem too bad for a £600m fund.

One thing I do like is that the management charge is 0.9% of net assets up to £475m but 0.65% above that level.

It’s refreshing to actually see a meaningful step down like this. Many funds just go for something like 1.0% to 0.9%, meaning that assets have to grow substantially before the charges become significantly lower.

Once you add in other costs, the ongoing charge is currently 1.04%. The Key Information Document shows 1.48%, with 0.27% of the difference due to portfolio transaction costs but no further breakdown provided.

Directors and their shareholdings

The directors, all non-executive, receive between £23,500 and £32,500 a year. They owned 133,500 shares (£407,000) between them as of 30 June.

One director, Julia Le Blan, is set to retire at next year’s AGM. She is being replaced by Stephanie Eastment, who joined on 1 July and increased her shareholding to 6,000 earlier this month.

Summing up

There’s a lot to like here and I might even open a position when some fresh funds become available.

I like its commitment to lower charges now that the fund is over a certain size and its long history (for an environmental fund anyway).

One thing that is perhaps surprising is the lack of similar trusts tackling this theme. The other two in the sector, Menhaden and Jupiter Green, only have combined assets of £120m. The former has only been around for four years while the latter’s performance has been very uninspiring.

Renewable infrastructure has been a very popular theme in recent years, but there would seem to be scope for more trusts that offer direct investment into environmental equities.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Nice write up (as usual) IT.

IEM was the first trust to join my fledgling ‘green’ portfolio last October and happy with performance so far. Return for the year to date is 25% which includes the 3p dividend (2.5p previous year). I have since added several other funds and Impax represents around 5% of my portfolio.

The trust has a good track record over the past 20 years but personally, I would like to see an increased weighting to renewable energy and take on board such companies as Siemens Gamesa and Orsted for example as well as battery storage solutions provided by the likes of UK start-up Highview.

Thanks DIY. Your timing looks pretty good right now. It’s eased off a little these past few weeks so that’s tempted me a little more.