Fundsmith Emerging Equities Trust, often shortened to FEET, is still struggling to keep up with its benchmark despite a lot of tinkering over the past few years.

FEET was launched on 25 June 2014, making it seven years old later this month.

Its IPO raised £193m, a not-insignificant sum that made it one of the largest of the 16 new issues that year.

However, it’s fair to say that FEET didn’t catch the investing public’s imagination in the same way that Fundsmith’s small- and mid-cap trust, Smithson, did when it raised a much chunkier £823m in 2018.

Like Smithson, FEET was set up as an investment trust due to the lower liquidity of its potential investments, making a closed-end structure with its fixed pool of capital far more suitable.

The median market cap is £5.8bn for FEET’s investments compared to £10bn for Smithson and £167bn for Fundsmith Equity.

A difficult start

For the first few years, FEET seemed to be doing OK despite emerging markets as a whole struggling to match the mega-gains made by the US tech giants.

Thanks to the Fundsmith aura, there was decent demand for FEET shares and the trust traded at a high single-digit premium for quite a while.

While FEET was lagging one of the sector’s stalwarts (JPMorgan Emerging Markets), it was ahead of the other (Templeton Emerging Markets). The Templeton trust snuck ahead of FEET at the end of 2016 and hasn’t looked back since.

By May 2019, Fundsmith Emerging Equities was trailing both trusts badly. It was up 16% since launch while Templeton was up 44% and JPMorgan had risen 80% over the same timeframe.

Changes were made with Terry Smith handing over the day-to-day management of FEET to Michael O’Brien and Sandip Patodia. Both O’Brien and Patodia had been part of FEET’s investment team since launch so it seemed to be a pretty smooth transition.

And in a rare show of humility from Fundsmith, the management charge for the trust was cut from an outrageous 1.25% to a still fairly rageous 1.0%.

Key Stats For Fundsmith Emerging Equities

- Listed: June 2014 at 1,000p

- Managers: Michael O’Brien (lead since June 2019) and Sandip Patodia (deputy since June 2019)

- Management firm: Fundsmith

- Ticker: FEET

- Sector: Global emerging markets (9th out of 10 over 5 years)

- Benchmark: MSCI Emerging and Frontier Markets Index (net sterling adjusted)

- Recent price: 1,340p

- Indicated spread: 1,335p-1345p (0.8%)

- Market cap: £356m

- Net asset value: 1,445p as of 7 Jun 21

- Discount to net assets: 7%

- Costs: 1.25% OCF, 1.34% KID

- Net cash: 3% (as of 31 May 2021)

- Number of holdings / top 10 holdings: 36 & 49%

- Results released: Mar (finals) and Aug (interims)

- Current dividend and yield: 2.0p and 0.15%

- Dividend paid: Jun

- Links: Website – AIC page – Edison (Jan 2021)

Price and related data as of 7 June 2021

Changes afoot

O’Brien and Patodia didn’t revamp the entire portfolio but it’s changed a fair bit over the last two and a bit years given Fundsmith’s preference for holding its investments for the long term.

There were 44 companies in the portfolio at the end of 2018 and 27 of those are still held today.

Nine new companies have been added over the last two years, the best known of which are probably NetEase, Tencent and Taiwan Semiconductor.

Three of the nine new additions — Info Edge, Metropolis Healthcare, and Avenue Supermarts, all of which are based in India — were among the top 10 holdings as of May 2021.

MercadoLibre, the current #2 holding, was a 9.1% position at the end of 2020. But it was merely the 34th largest at 1.3% at the end of 2018. The company’s share price rose fivefold over the course of 2019 and 2020 so it looks like FEET has added to its position a little along the way.

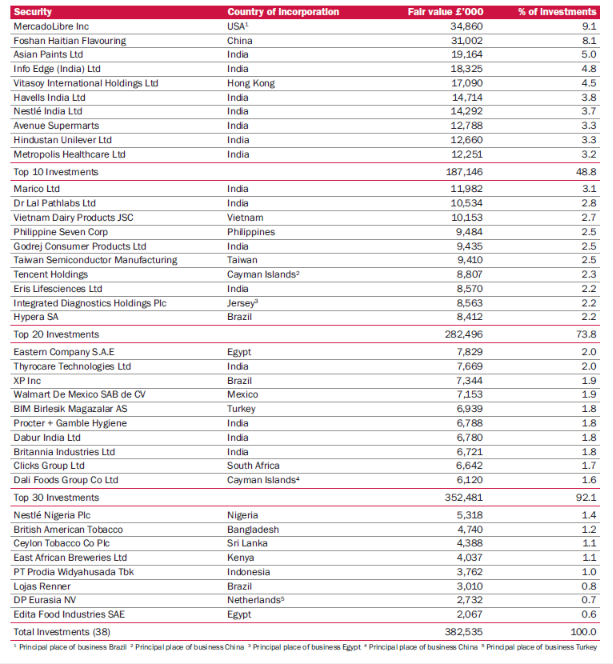

Here’s the latest full portfolio listing which dates back to 31 December 2020:

Since this list was published NetEase and a company yet to be disclosed have been added while PT Prodia, East African Breweries, Edita, and Dali have been sold. The four stocks sold so far in 2021 only accounted for around 4% of the portfolio at the end of 2020.

The country of incorporation is a little misleading in some cases as it doesn’t always tally with the main area of operations. For example, MercadoLibre is based in Latin America despite being listed in the US.

Portfolio turnover for 2020 was 21% which is pretty high compared to other Fundsmith vehicles. However, it’s averaged 34% over the last six years suggesting even before 2019 the investment focus of the trust was already shifting.

Shifting the portfolio’s focus

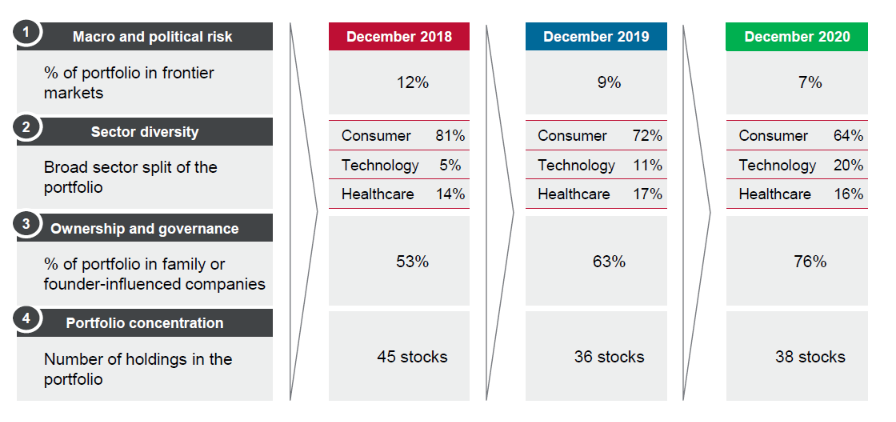

FEET’s AGM presentation a few weeks ago covered the ongoing changes since 2019 in some detail, splitting them into four categories:

- Macro and political risk — Reduce exposure to countries with relatively high macroeconomic and political risk,

particularly in frontier markets; - Sector diversity — Increase exposure to resilient growth companies in healthcare and technology sectors to

ensure that the fund performs better in ‘up markets’ whilst maintaining defensive qualities; - Ownership and governance — A decreased exposure to listed multinational subsidiaries and a greater emphasis on

investing in businesses with more entrepreneurial and incentivised management; and - Portfolio concentration — The number of holdings is likely to fall towards the low 30s. The guideline range is to be reduced from 35-55 to 25-40, more in line with other Fundsmith vehicles.

There was also this useful graphical summary of how these changes have been reflected across the portfolio:

The shift in the portfolio away from consumer stocks to technology is clear to see with the median year founded for investee companies shown on the monthly factsheet going from 1956 to 1978 over the last couple of years.

However, FEET has become even more concentrated on India, with the weighting by country of listing rising from 38% in May 2019 to 46% in May 2021.

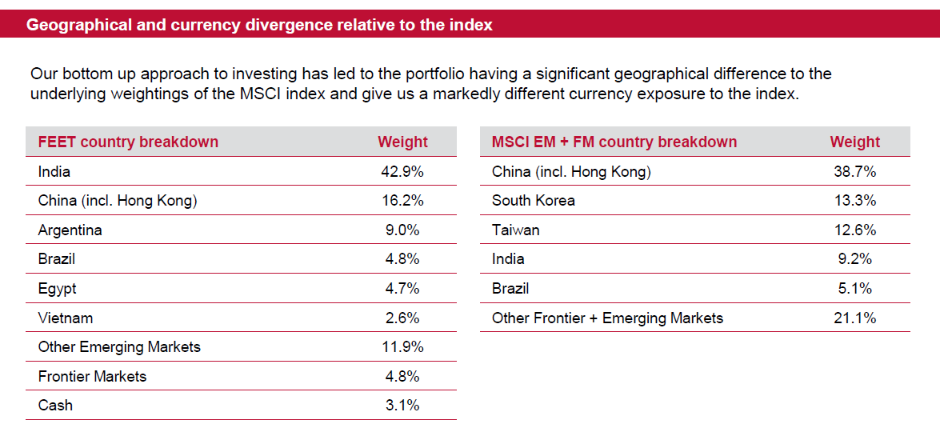

Here’s how the FEET portfolio compares with its benchmark index on a geographical basis:

FEET regards South Korea and Taiwan as developed markets so they are largely ignored when picking investments.

The concentrations towards China and India are essentially flipped compared with the benchmark, primarily because FEET believes Chinese companies are generally poor capital allocators.

Yet, it’s been Chinese companies rather than Indian ones that have been powering ahead in the last few years and this factor drives a lot of FEET’s underperformance when compared to other trusts in the sector.

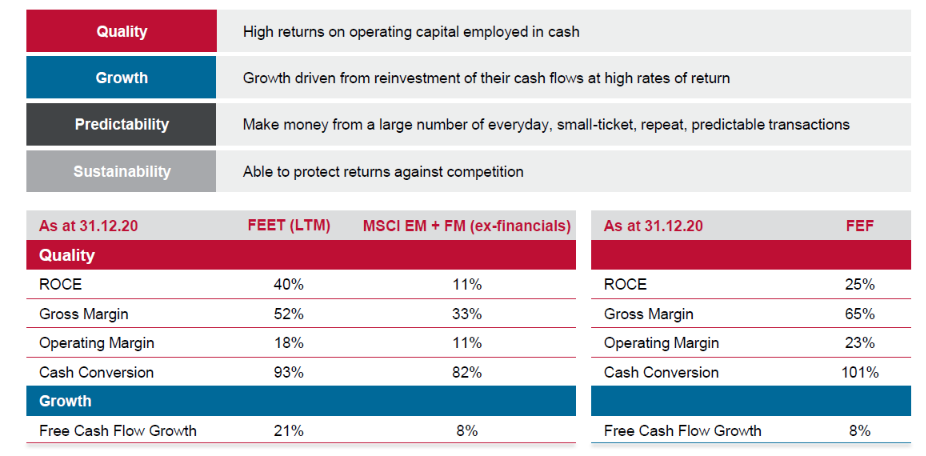

The usual Fundsmith metrics

A major plus point with all Fundsmith vehicles are the portfolio summaries, analysing how its investments compare with the wider market.

FEET handsomely beats its benchmark on every measure although there are quite a few differences compared with the main Fundsmith Equity fund.

Return on capital employed (ROCE), which is often cited as the most important of these metrics, is much higher for FEET than it is for Fundsmith Equity as is free cash flow growth. But both profit margins and cash conversion aren’t quite as good.

It’s tough to know how the overall quality of FEET’s portfolio compares to Fundsmith Equity given the mix of metrics. My impression is that it’s not as high but that’s probably heavily influenced by the relative returns over the past few years.

The fall of the multinationals

The “decreased exposure to listed multinational subsidiaries” is perhaps the most notable change since 2019 as the returns and attractive financial metrics of these sort of companies were touted as one of FEET’s great strengths when it first came to market.

In the 2014 prospectus, the Investable Universe consisted of 139 companies of which a fifth were said to be “quoted subsidiaries or franchisees of multinational companies” that were likely to be held by the main Fundsmith fund. Over half of this initial Universe consisted of food companies, food and staples retailers, or beverage companies.

A further prospectus in August 2016 said the Universe had shrunk to 98 companies but that now 42% of those were subsidiaries or franchisees of multinationals (although which of these might be held by the original Fundsmith was no longer mentioned).

O’Brien and Patodia seem a lot less keen on these types of companies saying their leadership often lacks the entrepreneurial spirit needed to succeed.

Six of these multinational subsidiaries remain in the portfolio today. As of the end of 2020, they accounted for 13% of net assets with Hindustan Unilever and Nestle India being the largest.

FEET’s Owner’s Manual doesn’t seem to have been updated for the changes to the Investable Universe, still quoting the initial 139 companies and showing their performance up to March 2014:

These numbers are certainly impressive but clearly, the average performance over the last seven years would have rather different. And it shows the limits of backtesting, not that we should really need another example.

It’s possible the numbers have been updated elsewhere and I’ve missed it but it would be useful to know how large the Investable Universe is today and how many companies remain from the 2014 incarnation.

Performance

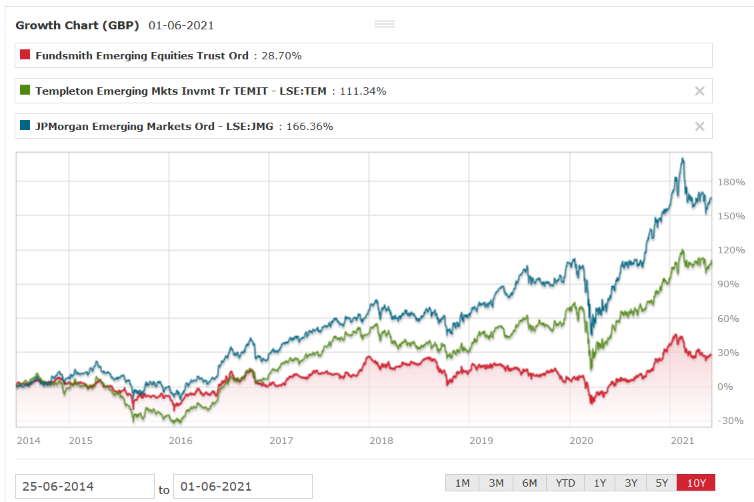

Since launch, FEET is now up 29% in share price terms, according to Morningstar, with Templeton up 111% and JPMorgan up 166% over the same period.

However, even with the overhaul in the trust’s approach, the relative performance since May 2019 tells a very similar story to the first five years. FEET is up 13% since then, with its discount level around the same level, with Templeton up 46% and JPMorgan up 47%.

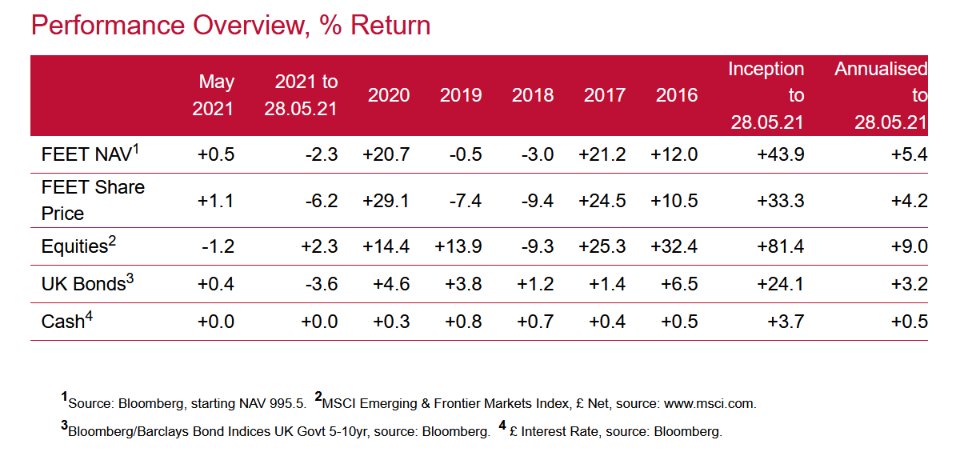

And here’s the latest performance breakdown from FEET’s monthly factsheet for May 2021:

2016 and 2019 have been the worst calendar years to date on a relative basis. Although 2020 was a very decent year with respect to the trust’s benchmark, FEET has lost ground again in 2021.

Part of this could be the wider move to value and away from quality and growth investing styles that we’ve seen in recent months.

Since inception, FEET’s net asset value return has been 5.4% per annum compared to 9.0% per annum for its benchmark.

The trust’s managers

Both O’Brien and Patodia joined Fundsmith in the run-up to the FEET IPO.

Here are their career histories taken from the trust’s documentation:

Michael O’Brien

Michael joined Fundsmith in October 2013. He began his career at Guinness Flight Global Asset Management (subsequently Investec Asset Management) in 1994 as an analyst, taking responsibility for the Group’s UK Small and Emerging Companies Funds in 1997, and subsequent to this the Recovery Fund. Michael also was an investment advisor to the Group’s Venture Capital Trust.

In 2000 Michael joined Collins Stewart as a UK analyst covering a wide range of sectors and was also instrumental in the development of the firm’s research product. Michael holds an MPhil from Cambridge University.

Sandip Patodia

Sandip joined Fundsmith in 2014 from Morgan Stanley, where he had been a vice-president within the UK investment banking team. Sandip spent four years with Morgan Stanley as a corporate broker, providing corporate finance advice to UK listed companies on all aspects of their interaction with the equity markets.

Prior to that he spent four years working as a M&A adviser at Ernst & Young. Sandip holds a first-class honours degree in Electronics and Computer Science from Aston University and is a qualified chartered accountant with the Institute of Chartered Accountants of Scotland.

I couldn’t see any specific age information so I would guess late 40s and late 30s respectively based purely their CVs.

Having dedicated managers with oversight from Smith seems a more logical approach to me and it seems to be working well at Smithson. Of course, we don’t know whether O’Brien and Patodia would have run the trust in a significantly different fashion up until 2019.

Charges

At 1.0% the basic management charge for this trust is 0.1 percentage point higher than both Fundsmith Equity and Smithson but then FEET is pretty small by comparison.

It’s a little expensive compared to other emerging market trusts of a similar size but not especially so.

The average OCF for the sector is 1.07% and only one trust, JPMorgan Emerging with £1.7bn of assets, comes in below 1% with an OCF of 0.94%.

Dividends

I doubt any FEETers are in it for the yield.

The trust first paid a dividend in 2019, when it was 2.0p a share. It rose to 3.2p in 2020 before falling back again to 2.0p in 2021.

The underlying portfolio yield is currently 1.4%, and therefore mostly swallowed up by the trust’s charges. The stated dividend policy being “to pay only those dividends required to maintain UK investment trust status”.

Discount control

The discount on FEET shares is monitored and tweaked with marketing efforts, share issues and buybacks rather than being tightly controlled with a strict zero discount policy.

The stated aim is for “a sustainable low discount or premium to the NAV per share”.

FEET rarely traded at a discount when Terry Smith was running things but the trust has been at a 5-15% discount for much of the last two years. However, its current discount of 7% is in line with the sector average.

Share issues were made on a fairly regular basis from March 2016 to March 2019, increasing the share count from 19.3m to 26.6m.

A few share buybacks have taken place in the last six months but only for a combined total of 40,000 shares (£0.5m).

Skin in the game

As with all of Fundsmith’s vehicles, shareholder alignment is excellent.

The directors own around 120,000 shares (£1.6m) and O’Brien held 27,400 (£0.4m) at the end of 2020 up from 21,000 a year earlier.

Terry Smith invested £5m at the IPO buying 500,000 shares and had increased this to 580,000 by mid-2019 when O’Brien took charge.

Smith now owns 847,000 shares (£11m). You could argue that this a small fraction of the £300m the Sunday Times reckons he is worth (and that was at the end of 2019) but it’s hard to consider an 8-figure investment as anything but meaningful.

Closing thoughts

I’ve looked at FEET a couple of times now on this blog. The first time was in 2018, prior to the manager change, then again in late 2019 when the rejiggling had just begun.

It seems like decent progress has been made since then yet the relative performance is still a concern.

The Fundsmith style of investing has had a decent tailwind behind it for the last decade but, for whatever reason, its success in developed markets has clearly not been transferrable to emerging markets.

Not every investing style works all the time so has FEET just been unlucky with its timing or is there something more fundamental causing a problem here?

The heavy concentration towards Indian stocks would still seem to be the most likely culprit now that the sectoral imbalances have been lessened and the portfolio has been streamlined.

It’s certainly been a major factor in stopping me from adding FEET to my portfolio alongside Fundsmith Equity and Smithson. I try to keep my investing style fairly simple and avoid any sizeable country or regional bets.

China’s GDP per capita is about five times that of India although the two were roughly equal in the early 1990s. My best ill-informed guess is that China will continue to widen its lead from here.

That said, the Indian stock market has actually performed a lot better than the Chinese market since the early 1990s, with the last 5 years being the major exception. Maybe FEET’s time will eventually come even after its seven years of struggles?

Whether China should still be classed as an emerging market now it is the second-largest in the world is another question. Certainly, were China to be removed from FEET’s benchmark, it would make the trust look a lot better on a relative basis even though its absolute performance would of course be unchanged.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Appreciate your ever-thorough overview as ever. I keep wanting this to turnaround, and it looks like it’s going in the right direction, but isn’t quite there yet.

It seems to me that they didn’t know what they were doing (compared with the main fund) at the start. It also looked, portfolio-wise, that they were basically just copying Arisaig, the EM Consumer specialists.

Arisaig have pivoted in recent years to EM tech giants, and it’s interesting to see FEET gradually doing the same. Arisaig explain themselves much better – it’s hard to know FEET’s thinking as clearly.

The country weighting is more like Pacific Assets, though even they added to China in the past year. I understand the historic reluctance, but there are too many great businesses to avoid it now, I think.

It’s good that FEET are getting rid of the Frontier stuff, which hasn’t worked & the most of the multi-nationals (ditto). Overall, the portfolio looks really strong to me – my only concern is that there are some nosebleed valuations in some of the quality stuff.

And I know it’s subjective, but I’d love it if they got rid of the Tobacco…

Overall, it stays in my ‘too hard’ pile. The portfolio looks great now, but I’d want to see the performance improve and, most importantly, a higher conviction in the fund managers’ investment strategy.

I know Fundsmith don’t like to go into detail (I suspect as most of their Retail investors aren’t interested), but I just don’t get what they’re doing here.

Thanks, Tom.

I should have mentioned in the article that I held the JPMorgan trust for several years, mostly while emerging markets were struggling, and it still managed to deliver a decent return. Austin Forey has done a great job and I think he’s been running it since 1994.

I suspect FEET taught Fundsmith a few harsh lessons in its early years and they put these into effect when they launched Smithson.

Thank you for this. I have long been put off by the emerging markets tag after getting frustrated by Templeton many many years ago. I more recently stuck with Vanguard VFEM and whilst not making any direct comparison I feel happier with that. I kept looking at FEET but happier I stuck with Smithson.

Thanks, J. I’m always amazed by just how different emerging market and developed market returns have been over time. Some great charts showing that here: https://www.longtermtrends.net/emerging-vs-developed-markets/

Interestingly, the returns have been very similar for the past 2 years – I wonder how long that will continue though?