Acorn Income Fund, one of my UK smaller company trusts, could be set for a major shake-up later this year after its directors announced a strategic review.

While Acorn’s long-term performance has been decent, with an annualised return of 12.2% from launch in February 1999 to the end of 2020, the last few years have seen it struggle.

Not your normal small-cap trust

This trust’s structure is pretty unusual. For starters, it’s very highly geared, using zero dividend preference shares (ZDPs) rather than bank debt.

The average level of gearing has probably been about 50% since the ZDPs were introduced in 2011. But changes in the number of ZDPs in issue are relatively rare, so the gearing level has moved between 30% and 80% as the price of small-cap shares has risen and fallen.

To mitigate some of the volatility this extra gearing causes (and to help ensure the ZDPs can be repaid when they fall due in early 2022), the underlying portfolio is split roughly three-quarters into UK smaller companies and one-quarter into corporate bonds and related income securities.

Here are the top 10 holdings and sector mixes for both portfolios as of 31 March 2021 to give an example of what’s in each of them:

Financials and industrials dominate both portfolios, with mining, oil & gas, and pharmaceuticals specifically excluded from the stock selection process:

What’s the attraction?

While other small-cap trusts made hay in late 2019 and over the last six months, Acorn Income has been left behind.

That’s odd as you’d expect a trust with this sort of highly geared set-up to do well in those sort of market conditions.

Acorn Income is one of three UK smaller company trusts I own, Henderson Smaller and BlackRock Smaller being the other two, to tap into the greater growth prospects that UK small-caps seem to have compared to their blue-chip cousins in the FTSE 100.

I’d say that both Henderson and BlackRock tilt toward the conservative side. Therefore, I allowed myself something a little more risque with Acorn Income Fund. I also thought that its additional volatility would allow me to build up my position at attractive prices.

I first bought Acorn Income three years ago and have added to this position a number of times since, mostly when I disposed of other trusts and decided to spread the proceeds over several of my remaining holdings.

My last two purchases were in April and August 2020 and these got me to a position size I was initially aiming for. As a result, and due to performance concerns, I decided that would be my final top-up for the time being.

I’m probably down around 5% in capital terms and up by a similar amount when you include dividends. However, the UK Smaller Companies sector is up 40% over the last three years and both Henderson and BlackRock are a little further ahead.

Key stats about Acorn Income Fund

A few extra stats than I usually include here, given the more complex nature of Acorn Income’s structure:

- Founded: 1999

- Ticker: AIF (ordinary shares) AIFZ (ZDPs)

- Style: 70-80% UK smaller companies, 20-30% fixed income and other income securities

- Number of holdings: 44 in smaller companies and 67 in income at last year-end

- Managers: Fraser Mackersie and Simon Moon (Unicorn: smaller companies) & Chun Lee and Robin Willis (Premier Miton: income)

- AIC sector: UK Equity & Bond Income (1st out of 2 over 10 years but would be 13th out of 20 if in UK Smaller Companies)

- 10-year net asset return: +195%

- Benchmark: Numis Smaller Companies Index (excluding investment companies)

- Share price: 353p

- Indicated spread: 348p-358p (2.8%)

- Market cap: £56m ordinaries + £34m ZDPs

- Net asset value per ordinary share: 414.4p

- Discount to net asset value: 15%

- ZDPs: 21.2m shares due to be repaid on 28 Feb 2022 at 167.2p per share (£35.5m)

- Gearing: 52% as of 23 Apr

- Costs: 1.8% OCF and 4.5% KID (latter includes 2.4% due to gearing)

- Domicile: Guernsey

- Year-end: 31 December

- Results released: Apr (finals) and Aug (interims)

- Current dividend and yield: 23p and 6.5% (likely to be reduced later this year)

- Dividend policy: pays from current year income and revenue reserves only

- Dividends paid: Mar, Jun, Sep, and Dec

- Links: Website — AIC — Edison (Nov 2020)

Price and related data based on 26 Apr 2021

A looming continuation vote

Acorn Income Fund has five-yearly continuation votes with the next one due at its AGM in August 2021. So, it’s not a good time to be losing ground against other similar trusts. This has spurred its directors into action.

The details are still being finalised, but in advance of the continuation vote, proposals will be put forward that might see changes to the trust’s:

- investment policy;

- corporate structure;

- gearing; and

- dividend policy.

In other words, pretty much everything could be tweaked.

The investment management agreement has a 6-month notice period so protective notice has been served to start the clock ticking on a possible manager change as well.

The Board did add the proviso that “this action should not be interpreted as an indication that the current Investment Advisers will not be involved in the management of Acorn’s portfolio post the conclusion of the strategic review.”

I wrote about manager changes just a few weeks ago but I didn’t think I might be dealing with a similar situation in my own portfolio so soon afterwards!

[A few weeks after I wrote this piece, the outcome of the strategic review was published and a change of manager to BMO was proposed along with a switch in investment focus to ‘global sustainable equity income’ – I did another piece with some initial thoughts on this.]

Acorn’s early days

Although the make-up of this trust could change significantly in the coming months, I think it’s worth recapping the history of Acorn Income Fund to set the scene.

Certainly, for a trust that has only been around for just over two decades, it has already seen a fair number of changes.

Acorn Income has had the same basic structure throughout of a highly-geared portfolio split into smaller companies and income-focused assets.

This trust was initially run by Collins Stewart, who handled all the admin aspects and ran the income portfolio.

The smaller companies portfolio was first managed by Peter Webb, who is best known for running the Eaglet Investment Trust (Eaglet was a top performer in the 1990s before coming unstuck in the 2000s).

Webb went off to set up Unicorn Asset Management in 2000, bringing the mandate for Acorn Income’s smaller companies portfolio with him.

John McClure worked alongside Webb, I believe from Acorn’s launch, and eventually took over when Webb left Unicorn in 2008.

The first big challenge

In the 2000s, gearing was achieved through a long-term bank loan, although I believe the level of borrowing was generally a little bit lower than it has been in recent years.

At the AGM in 2006, a massive 68% of shareholders voted against the trust carrying on at its first continuation vote. This was shy of the 75% required for a formal wind-down but it resulted in a massive tender offer which saw 70% of shareholders opting for their cash back.

Collins Stewart lost the overall mandate with Premier Asset Management (now known as Premier Miton) taking over their role and the income portfolio. Unicorn remained in charge of the smaller companies portfolio.

From small acorns…

As the global financial crisis deepened, Acorn Income’s net assets sank to just £8m by the end of 2008.

The gearing kicked in at that point as markets started on their long bull run.

In four of the next five years from 2009 to 2013, the share price returns were between 50% and 65%, catapulting Acorn Income up the performance charts. Like many trusts, there was a pause for breath in 2011 as the Greek financial crisis reached its peak.

Somewhat surprisingly, the second continuation vote in August 2011 saw 1.6m votes against continuing and 2.2m in favour of carrying on. Although, once again, it was some way short of the 75% needed for a formal wind up, it wasn’t exactly a vote of confidence either.

Acorn Income’s bank loan was due to be repaid in early 2012 but it was not renewed due to the Bank of Scotland’s decision to depart from the investment trust sector. The directors decided to replace the bank debt with ZDPs.

ZDPs cost a little more than bank debt, but all the interest is effectively rolled up into the final payment. The lower cash cost enabled Acorn Income to dramatically increase its dividend from 7p in 2011 to 12p in 2012. It’s nearly doubled since then, reaching 23p in 2020.

Tragedy strikes

Simon Moon and Fraser Mackersie were formally appointed as co-managers in 2013 but McClure was still the main man. In the early 2010s, he owned 287,000 shares in the trust, which was a stake of just over 3%.

But McClure died in 2014 after a short illness at just 50 years of age.

Moon and Mackersie took charge of the smaller companies portfolio. They both joined Unicorn in 2008 and had worked alongside McClure since that time.

The trust’s performance moderated over the next few years but many small-cap trusts did much the same thing. The Brexit vote saw the overall UK market fall from favour as investors grew cautious about smaller companies — they were seen as more vulnerable due to their size and greater domestic focus.

Nevertheless, a whopping 91% of the ZDP shareholders voted to roll over their shares in late 2016, extending their expiration date from January 2017 to February 2022.

And a few months prior to that, the third continuation vote was a resounding yes. 2.3m voted to continue with just 5,800 wanting a wind-up.

The last few years have been relatively uneventful on the corporate new front although in August 2019 it was announced that Paul Smith, the manager of the income portfolio, was leaving Premier for personal reasons.

Chun Lee and Robin Willis took over as co-managers of the income portfolio, having both been partly involved with Acorn Income for a number of years already.

Moon and Mackersie

I’ve seen a fair amount of comment that Acorn Income is not the same since John McClure passed away.

I think that’s a little unfair on Moon and Mackersie although it’s more difficult to assess how good McClure’s record was now that we are in 2021.

Moon and Mackersie have both co-managed Acorn Income (£75m of assets) and Unicorn UK Income (£586m) since 2013, the latter broadly matching the UK market over that period.

Mackersie has been lead manager for Unicorn UK Growth (£110m) since early 2011, delivering a total return of 197% in his first decade versus 86% for the UK All Companies sector.

Moon has led Unicorn UK Smaller Companies (£55m) since 2013. It has returned 160% over the last 8 years, matching the UK smaller companies investment trust sector.

The other M&M funds share many holdings with Acorn Income and when you look at the sort of companies currently owned, I think the type of stocks held have a lot in common with those in the portfolio during John McClure’s time.

Moon and Mackersie are still relatively young. They both left university in 2003 which means they are probably 40ish today.

Unicorn is very small in fund management terms, looking after just £1.5bn in assets, so that means Moon and Mackersie are responsible for just over half of its business.

Skin in the game

Those involved with the trust these days don’t seem to hold as much as John McClure did before his passing.

Three of the four directors own 74,000 shares between them. Most of these are held by David Warr who looks set to leave the Board once the strategic review, continuation vote, and ZDPs are sorted out.

No directors bought ordinary shares in 2020 but a couple of them bought some ZDPs.

Employees of Premier Miton own around 6,000 shares. However, I couldn’t see any information on the stake held by Moon and Mackersie although the most recent Edison note in November 2020 said “they have also added to their own holdings in AIF”.

Untangling performance

One big problem I do have with Acorn Income is that the various moving pieces make it hard to know what’s working well and what isn’t.

The Numis Smaller Companies Index (NSCI) is the comparator Acorn Income most often uses. It measures the bottom 10% of the UK stock market by value and is widely used as a benchmark for smaller-company trusts.

However, Acorn’s official benchmark appears to be 75% NSCI and 25% ICE Bank of America Merrill Lynch Sterling Non-Gilts Index, with the latter measuring its income portfolio.

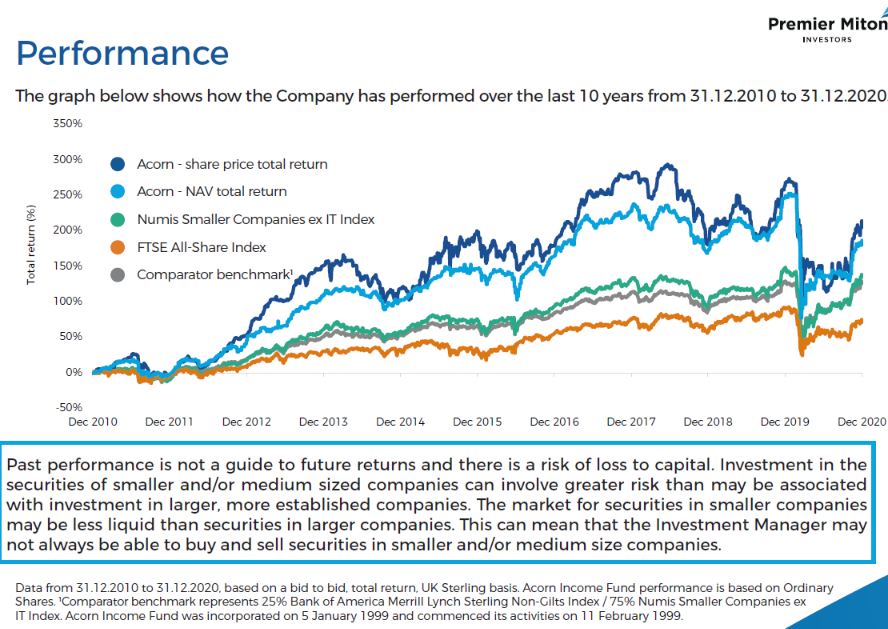

Given corporate bonds have generally performed well in the last decade, as interest rates have been on the decline, this distinction has meant the NSCI (the green line in the chart below) and Acorn’s official benchmark (the grey line) haven’t performed that differently:

Charts like this look pretty but it can be hard to discern relative performance when you look at the most recent years and the gaps between the lines are much wider.

From eyeballing, though, it does suggest strong outperformance up until mid-2018 but falling back thereafter.

And yes, that’s pretty much the point at which I first bought!

Breaking it down further

I’m primarily interested in this trust as a small-cap play. So what I really wanted to know was:

- how has the smaller companies portfolio has performed; and

- how that got translated into the trust’s overall performance after the additional impact of the income portfolio and the high level of gearing.

To get a handle on this, I pulled out these key numbers from Acorn’s accounts:

| Year to 31 December | Numis Smaller Companies Index (ex ITs) | Share price return | NAV return | Smaller companies portfolio | Income portfolio | Gearing at start of the year |

|---|---|---|---|---|---|---|

| 2011 | -9.1% | -4.4% | -1.2% | 0.1% | n/a | 25% |

| 2012 | 29.9% | 60.5% | 48.0% | 32.7% | n/a | 72% |

| 2013 | 36.9% | 63.9% | 42.9% | 40.9% | 12.0% | 55% |

| 2014 | -1.9% | -12.9% | -3.1% | -1.2% | 8.0% | 43% |

| 2015 | 10.6% | 36.0% | 22.1% | 26.3% | 2.9% | 48% |

| 2016 | 11.1% | -6.3% | 6.9% | 8.6% | n/a | 44% |

| 2017 | 19.5% | 34.5% | 24.2% | 24.9% | n/a | 45% |

| 2018 | -15.4% | -23.7% | -16.9% | -14.0% | n/a | 39% |

| 2019 | 25.2% | 28.6% | 27.4% | 26.5% | n/a | 52% |

| 2020 | -4.3% | -14.1% | -17.1% | -12.2% | n/a | 44% |

As with many of my tables, there’s a lot to unpack.

I’d say that the smaller companies portfolio has actually done pretty well, with particularly good relative years in 2011, 2015, and 2017. The only really poor year on a relative basis was 2020. It returned 203% over the decade with the NSCI producing 136%.

Figures for the income portfolio rarely seem to be reported for some reason, which I hadn’t picked up on before. There are vague references to “positive contributions” and similar phrases but an annoying lack of detail.

You would expect this part of the portfolio to be relatively steady and its impact on total return to be reduced by its smaller size. But I’d still like to know how it’s doing. The fact that the two portfolios are sometimes adjusted in their relative sizes by the directors, to take on or reduce risk, makes it hard to estimate the returns from the other information provided.

Acorn Income sometimes takes out derivative products to lessen risk as well, such as a FTSE 100 put option taken out in April 2020. As the market recovered nicely from that date, it turned out this protection wasn’t needed, but it’s not clear how this affected returns.

The gearing doesn’t work?

There are five years where the smaller companies portfolio returned 25% or more over the last decade. Only in 2012, when the initial level of gearing was extremely high, did this translate into a significantly higher NAV return.

In 2013, 2015, 2017, and 2019 the NAV return was actually marginally lower than the smaller companies portfolio return, which is puzzling.

However, in the down years of 2014, 2018, and 2020, the downside effect of the high level of gearing does seem to be in evidence.

When you look at the decade as a whole, the smaller companies portfolio return of 203% is higher than the 188% increase in the trust’s NAV.

In other words, the very high level of gearing hasn’t amplified underlying returns at all.

While this is undoubtedly a simplistic take, it does suggest to me that some part of this trust isn’t working as intended.

Certainly, Acorn Income could benefit from some attribution analysis when it comes to presenting its results showing the breakdown from portfolio performance, via the various gearing decisions and effects, through to net asset value returns.

What might happen to Acorn Income’s dividend?

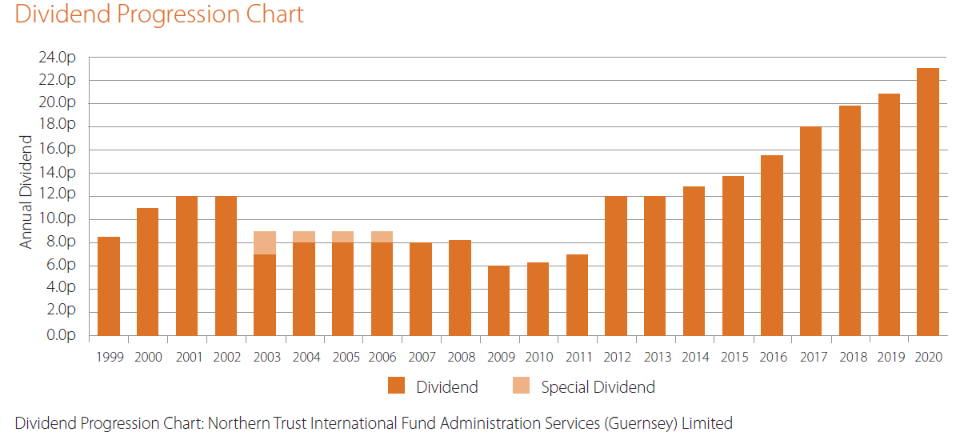

I haven’t dwelled on the 2020 results much but what happened last year suggests the likely level of future dividends.

Here’s the dividend record since the trust launched in 1999 and you can see that the path was far from smooth in the 2000s but the 2010s saw steady increases:

Four equal payments are usually made each year and the initial payout of 5.75p for the first quarter of 2020 was set in February 2020. It was six weeks before the first UK lockdown so the 10.6% increase over the previous year seem punchy but not outrageous at the time.

But it wasn’t long before widespread dividend cuts began. We even saw dividends that have already been declared being cancelled just prior to payment.

Dividends from Acorn Income’s smaller companies portfolio fell by 36% in 2020 which was a little less than the 44% decline in the UK market overall.

The average holding period tends to be nearly five years but 2020 saw 11 disposals and 8 additions taking the portfolio size down from 47 to 44.

Companies perceived as most vulnerable to a prolonged downturn were trimmed. As it turned out, these bounced back a lot more quickly than most people expected so this strategy, while sensible given what was known at the time, may have ended up hurting the trust’s relative performance.

The revenue return per share for the year ended up at 13.75p per share, way below the 23p paid out in dividends. Revenue reserves fell from 21.6p per share at the end of 2019 to 12.4p.

Acorn Income has paid 5.75p for the first quarter of 2021 and intends to pay the same amount in the second quarter, so that will have drained revenue reserves further still.

The intention is not to pay dividends from capital, so the third and fourth quarter dividends are likely to be a lot lower.

From the 2020 results:

The Board has been pleased to see the recovery in earnings throughout the second half of the year, certainly reaching a level which was far from visible during the second quarter, and although our projections do show a recovery in the Company’s revenues for 2021 and thereafter, the Board believe that it is likely that a return to a sustainable and covered dividend will necessitate a lower dividend payment in future years.

A recovery in revenues suggests, all else being equal, revenue return per share could be somewhere in the region of 15-16p for 2021 but that’s pure speculation.

However, if the strategic review ends up suggesting a lower level of gearing and/or bank debt replacing the ZDPs, then this will likely mean a lower revenue return per share with a corresponding lower dividend.

Bad process or bad outcome?

It goes without saying that it’s been a disappointing three years as a shareholder of this trust.

I’m pleased that I stuck to my original plan when it came to position sizing, though, given it was a riskier play. Building into a holding like this over time, as you get more familiar with its foibles, seems to work for me.

The question I need to answer is whether the process of choosing this trust was flawed or whether I just got unlucky with a bad outcome. The latter happens when investing… with alarming frequency!

I think the idea of taking a little more risk with my third small-cap trust was a reasonable one. Something equally quirky like Oryx or Rights & Issues would have worked out better but I was a little concerned these were one-man shows with their managers possibly close to retirement.

Undoubtedly, I was somewhat lured towards Acorn by the twin headlights of its great 10-year performance from 2008 to 2018 and its high dividend yield.

I can’t claim to be have been caught out by the trust’s high gearing as I’m both old and ugly enough to know what that could do to returns.

Nevertheless, the fact gearing hasn’t helped over the last decade is surprising.

Perhaps the lesson is that when they are many moving parts, the chance of something breaking is pretty high.

Prediction time

I’m very curious to see what the strategic review suggests.

My hunch is that the ZDPs will disappear and be replaced by a lower level of bank debt. I wouldn’t be upset to see the dual-portfolio approach vanish as well, as it would seem a little redundant if borrowings are reduced.

Of course, such changes would mean there is then little to differentiate Acorn Income from other small-cap trusts. It’s a packed field already with 12 trusts with assets of £150m or less and another 13 ranging from £200m to £1,500m.

Acorn Income’s long-term performance is in the same ballpark as many of the top-performing UK smaller company trusts of the last 20 years. However, it’s been a rockier ride.

In recent annual reports, there have been charts showing Acorn’s returns and volatility compared to other UK small-cap and all-company trusts. But these were notably absent from the 2020 annual report that’s just been published.

The trust’s charges need revisiting as well, I think. As the 0.7% percentage fee is charged on total assets rather than net assets, the ongoing charges figure looks expensive, particularly next to the larger trusts in this sector.

There’s also a 15% performance fee over returns of over 10% a year on the higher of two points: the 2007 tender offer or the last time a performance fee was paid (which was for 2017).

With the fourth continuation vote coming up in a few months, a lot will rest on what the directors come up with to get Acorn back on track. But they deserve credit for increased marketing of the trust in the past year, which has helped to narrow its trading spread, and for leaving little off the table when it comes to the strategic review.

As this trust is sitting on a fairly wide discount right now, partly because its small size makes regular share repurchases an unattractive option, I’m in no rush to make a quick decision here.

If the proposals aren’t well-received, there could be a tender offer or full wind-up, which could facilitate an exit much closer to net asset value.

If the shake-up looks attractive, I’ll need to decide whether to stay put or not. These days, when I lump in my sole venture capital trust as well, I’ve probably got a bit too much invested in UK small-caps. So that’s another factor I’d need to weigh up when the picture becomes clearer.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Another great write up, thank you. Funny, Acorn is one I keep coming back to as I like Unicorns VCT and especially its top holding. The discount alone makes it interesting but I do wonder if the discount does hide the future uncertainty. Its a minnow and with probably too many individual holdings I keep excusing myself.

I used to be a holder, but exited a couple of years ago. I haven’t crunched the numbers, but suspect that the reason the gearing hasn’t benefited the performance in a rising market is the income sub fund. In simple terms there is an income fund backing the zeros and an ungeared smaller Co’s equity fund. It’s not really quite that simple, as the portfolios and the capital don’t precisely match, but I’m sure this is why the gearing benefit is missing.

@J – Thanks! Yes, that VCT has done pretty well although I don’t think M&M have ever been formally involved with it. The discount has been quite wide for a little while now, and has been all over the place over the last 10 years so difficult to know if the uncertainty is a factor with it right now. I reckon it’s more likely to narrow than widen from here but we’ll have to see how things play out.

@Phil D – congrats, sounds like a well-timed exit. The company has often said the income portfolio should cushion the effect of the gearing but not completely cancel it out and I was expecting to see some gearing uplift from a portfolio that trebled in a decade. But without the income performance figures, we’re in the dark really. To be honest, if the income side did nullify the gearing then you could argue what’s the point of having this structure at all. I’m not sure we’ll get much more than a summary of the strategic review but it may shed some light on what’s happened.

Thanks, this is a particularly good review.

Attracted by the yield, I considered Acorn for the portfolio of a family member about four years ago, but ended up going with another Premier Miton split-capital investment trust, now called Premier Miton Global Renewables, which has been a great success. The volatility of smaller companies make for a queasy combination with so much gearing, and buffering with corporate bonds adds further complexity as you describe. Lots of gearing always unsettles me: my two big losses, Marconi and Candover, were both caused by excessive debt.

I find selling decisions much harder than buying ones: something about reversing a decision that seemed right before and the lingering possibility of recovery.

Thanks, Tom D. I was happy with the gearing and complexity in a small position alongside another couple of small-cap trusts. It would have been too much for me otherwise I suspect.

And selling is undoubtedly tough – it’s very easy to change course just before the tide turns, to mix my metaphors. But I do find the basket approach can help with these things. By buying a handful of similar trusts you can get a better feel for the overall sector and it feels more natural to switch trusts along the way as you learn more about what seems to work and what doesn’t.

There’s absolutely no point in having high gearing if most of the proceeds are then invested in fixed income. Far too much work and complexity to bother. Better to have a simple and cheaper bank debt at a lower level. Whoever thought of their strategy needs to explain themselves. Do you know if that decision was at the board level or the manager? I assume the board.

Board level I believe although it’s been the same set-up since the trust was created in 1999 and the board has obviously consisted of many different individuals since then.

The recent announcement of the change of strategy is quite remarkable. Rather than a geared play on UK small caps (a decent place to be at the moment), they are going into a global equity income strategy. It doesn’t even sound like global small caps, which could have been something to get into.

I liked the idea of Acorns growing into oaks!

Yes, it’s quite a change! I did another piece about it here in case you haven’t seen it yet.

https://www.itinvestor.co.uk/2021/05/acorn-income-jumps-on-the-sustainable-bandwagon/

Thx for this- I wouldn’t touch it with a barge pole