Buffettology Smaller Companies is one of several new investment trusts heading our way. It’ll be managed by the team at Sanford DeLand that is also behind the highly successful Buffettology open-ended fund.

26 October update — We heard this morning that this IPO has been pulled due to lack of interest. There’s a possibility it may resurface at a later date but it seems to be fairly rare for trust IPOs to get a second chance.

Let’s put my cards on the table first. I’ve long been a fan of the UK smaller company sector and I’ve stuck with it throughout what’s been a difficult 2020.

And I’ve also applied for a few shares of this IPO.

It will be a very small position for me, however. A toe dip and a cautious one at that.

The trouble with IPOs

I’ve got three trusts in this space already, all of which have recently been trading on double-digit discounts, as do many other UK-focused investment trusts.

Admittedly, the discounts on all three of my holdings (Henderson, BlackRock, and Acorn Income) have narrowed considerably over the last week.

Even so, it’s hard to justify loading up on a new trust that’s immediately going to be at a small premium, assuming it begins trading close to its issue price.

So I plan to see how Buffettology Smaller Companies progresses before committing any extra money. I’ll be looking at things like where its discount (or premium) settles at and the shape of its initial portfolio.

Many of the companies this trust plans to buy could be very small, so it might take some time to build its desired position sizes.

Indeed, the trust’s prospectus says although it “expects to be able to deploy the net proceeds within three months, deployment depends on there being favourable market conditions and the availability of good pricing opportunities.”

Key info for Buffettology Smaller Companies

Here are some selected highlights from the prospectus:

- Objective: to deliver an annual compounding rate of return over the long term, defined as 5-10 years, which is superior to the Numis Smaller Companies plus AIM (Ex Investment Trusts) Index

- Offer closes: Fri 23 Oct, although some intermediaries may have earlier deadlines

- Shares begin trading: Thu 29 Oct

- Ticker: BUFF

- Launch price: 100p

- Estimated initial net asset value: 98p (i.e. launch expenses are 2%)

- Net asset value updated: Daily

- Money raised: looking for £100m to £250m, followed by a placing programme raising up to £350m

- Initial directors’ investment: £105,000

- Managers: Sanford DeLand: Keith Ashworth-Lord (age 64), Andrew Vaughan, Eric Burns

- Annual management charge: 0.65% (no performance fee element)

- Estimated total annual charge: 0.96% (assuming £250m is raised)

- Type of investments: listed UK (main market and AIM), valued between £20m and £500m when purchased

- Unlisted investments: No

- Number of investments: typically 30-50 (maybe up to 60)

- Year-end: 31 Dec (first report for the period to 31 Dec 2020)

- Sector: UK Smaller Companies

- Gearing policy: Up to 15% but only for liquidity and discount management purposes, not for investment

- Dividend policy: no set level, so probably just income received less expenses incurred

- Wind-up policy: full or partial exit opportunity in the fifth year then every three years thereafter

- Websites: www.buffettologyIT.co.uk and Sanford DeLand

Everybody hates us!

To say the UK market is out of favour at the moment is an understatement.

Our main index is stuffed full of old-school energy companies and banks — the stuff of investing nightmares.

Nevertheless, we’ve had three UK-focused investment trusts announce their intention to list in recent weeks.

Tellworth British Recovery & Growth was looking to raise £100m and was due to list its shares on 13 October.

But last week it called the whole thing off, saying although it had received plenty of interest this hadn’t converted into actual demand.

Tellworth’s fund managers were fairly well regarded and it had generated some decent press coverage from its ‘Best of British’ approach. Yet it still got pulled, showing how hard it can be to get a new issue away.

Schroder British Opportunities is said to be looking to raise £250m to invest in both listed and unquoted companies. At the time of writing, SBO was yet to publish a prospectus so we don’t know its finer details.

That leaves Buffettology Smaller Companies as the sole runner right now.

The Analyst connection

I first came across Keith Ashworth-Lord in the 1990s when he used to write for Analyst magazine. Run by Jeremy Utton, Analyst was popular with many private investors who favoured a long-term investing approach and in-depth fundamental analysis.

It also had a marketing deal with a then-obscure Bristol-based financial services firm called Hargreaves Lansdown.

The bear market of 2000 to 2003 saw Analyst’s subscriber numbers decline significantly and it was eventually renamed Outstanding Companies Digest before, I assume, ceasing publication entirely.

Ashworth-Lord stayed with the business until late 2008 and then set up Sanford DeLand shortly afterwards.

His investing approach today doesn’t seem radically different from what I read in Analyst back in the 90s. The ideas have been refined and updated, naturally, but the core has remained.

Andrew Vaughan also worked at Analyst, but he only joined in 2005, a few years after I ceased being a subscriber. He’s obviously known Ashworth-Lord for a while although he only joined Sanford DeLand in 2017.

Vaughan has run Free Spirit since July 2019 and I would guess he’s in his early 50s.

Eric Burns only joined Sanford DeLand in early 2020 but he worked for many years at WH Ireland before that. Ashworth-Lord was a consultant for WH Ireland from 2006 to 2010, so I would assume that’s where they first met.

Burns studied at Durham in the early 1990s so I would guess he’s in his late 40s.

It will be interesting to see how much Vaughan and Burns are involved. Keith Ashworth-Lord is undoubtedly is the main man for now but he’ll turn 65 in January 2021 so succession is something that needs considering.

The Buffettology brand

As the prospectus states “Sanford DeLand has an association with Mary Buffett and David Clark, authors of the seminal ‘Buffettology’ series of investment books regarding Warren Buffett’s investment style.”

In 2009, Ashworth-Lord received a phone call from Clark, who he had known for some time already, asking if he would like to run a fund based on the Buffettology theme. That call kicked off the creation of Sanford DeLand.

Mary Buffett is the daughter-in-law of Warren Buffett although she is now divorced from Peter, Warren Buffett’s youngest son.

Buffettology is a catchy moniker even though Warren Buffett himself seems to have had a somewhat lower profile over the last year or so. But given he recently turned 90 that’s hardly a surprise!

It’s not clear how long Sanford DeLand has licenced the Buffettology brand for and, presumably, there are circumstances under which it could be revoked, but I would doubt this would have much impact on the investment case for this trust.

This passage from the prospectus is also worth noting:

The Company may, in addition, terminate the Investment Management Agreement with immediate effect on written notice if any two or more of Keith Ashworth-Lord, Andrew Vaughan and Eric Burns (or such other persons that the Company agrees in writing be treated as key persons from time to time) cease to be involved in managing the Portfolio and are not replaced within 90 days by alternative portfolio managers approved by the Company in writing (provided such approval may not be unreasonably withheld or delayed).

The usual notice period for termination otherwise is six months and no notice can be given in the first two years (I’m not sure if that latter part is a standard clause with new issues).

I assume any move away from Sanford DeLand would mean the rights to use the Buffettology branding would also cease but I didn’t see any reference to this in the prospectus.

Sanford DeLand’s open-ended funds

The two open-ended funds run by Sanford DeLand, both of which have a UK focus, have done really well since they launched.

Buffettology Fund

CFP SDL UK Buffettology Fund has grown like topsy and now has £1.4bn in assets.

It returned 237% from launching in March 2011 to the end of September 2020. That puts it top out of 202 UK funds over that timeframe.

Over the last five years, it’s up 85% which makes it 2nd out of 223 UK funds.

Free Spirit

CFP SDL Free Spirit Fund was launched in January 2017 and is up 50% since then making it 3rd out of 234 UK funds. Andrew Vaughan, who runs Free Spirit, made an impressive presentation at Mello Virtual a few months ago I thought.

Free Spirit leans more towards smaller companies. Although it only has £19m in assets right now, that’s actually about the same size the Buffettology Fund was during its fourth year as well.

In fact, the Buffettology Fund didn’t amass £100m in assets until sometime in 2017 I believe. And it’s only really in the last couple of years, as it grew considerably larger, that its top-ten holding list has contained much larger companies.

Free Spirit and the Buffettology Fund, with 27 and 31 companies respectively, operate slightly more concentrated portfolios than Buffettology Smaller Companies intends to.

Why launch an investment trust now?

There’s a good interview article with Keith Ashworth-Lord on Trustnet that covers why this trust is being launched:

Yet despite the strong performance of these funds, [Ashworth-Lord] has expressed his frustration that he has had to sell out of micro caps such as Driver Group, Air Partner and Revolution Bars, due to size constraints.

“We took a conscious decision to exit those positions last summer,” he said. “That was not a reflection of the company or the management, it was because we owned between 15 and 20 per cent of each and we obviously didn’t want to go above 20 per cent, as they start asking you to join the board and daft things like that.”

“And in aggregate, they accounted for 1.5 per cent of our NAV [net asset value], so if one of them had doubled it wouldn’t have moved the dial, yet they all demanded research resource.”

“We’ve been coming up with ideas at that £20m to £200m area which realistically couldn’t go into Buffettology and we thought the ideal structure for this would be a closed-ended fund because it is permanent capital. And then I don’t have those liquidity worries that I always have with the smallest stuff with Buffettology being open-ended.”

Ashworth-Lord is regularly interviewed by the media so he’s worth googling for more nuggets like this.

This PI World interview from a few months ago goes into a lot of detail over the course of an hour.

And he’s also written a book about his investing style called Invest In The Best.

I also found another Trustnet interview that covers his early career and the formation of his philosophy.

Investing policy

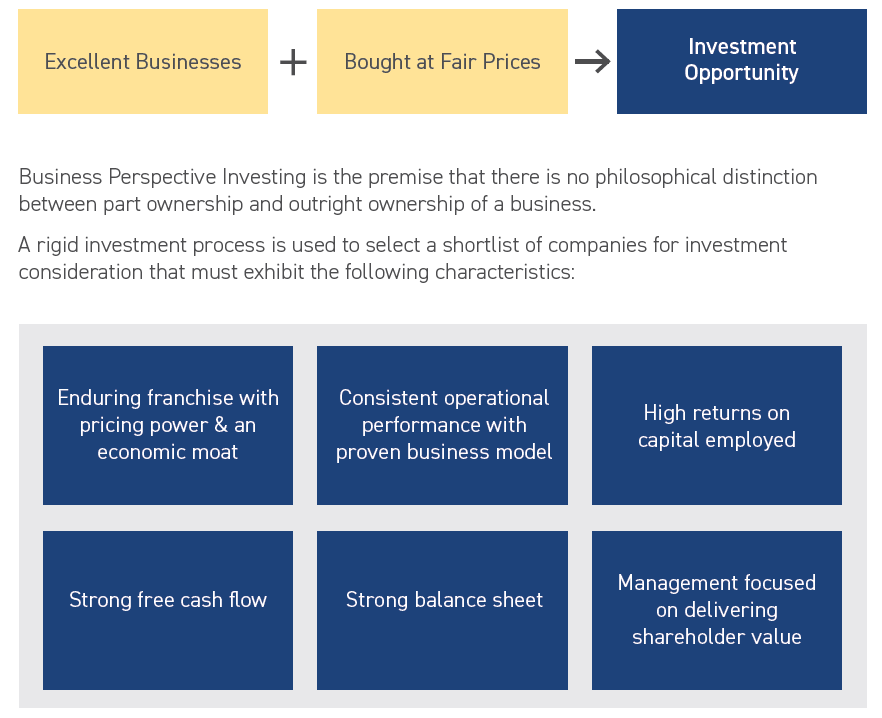

Buffettology Smaller Companies will mimic Sanford DeLand’s other funds in its use of “Business Perspective Investing”.

Here’s a graphic from the flyer explaining what that involves:

Pages 35 to 37 of the prospectus expand on this in more detail for those who want to dig deeper.

It’s nothing enormously original, being another variation on the quality investing approach that many funds and trusts claim to employ.

Of course, everyone interprets ‘quality’ in a slightly different way and to a stricter or looser extent.

Buffettology Smaller Companies intends to be a long-term holder, which it defines as at least 5-10 years. It also says that the portfolio turnover to date in the Buffettology Fund suggests its portfolio turnover is in the region of 25 years.

Looking at some of the larger and better-known companies currently held by the Buffettology Fund and Free Spirit probably sheds a little more light on how this approach might look in practice:

- Games Workshop

- London Stock Exchange

- Experian

- Unilever

- Auto Trader

- Next

- Homeserve

- Diageo

- GlaxoSmithKline

- Intertek

- Hargreaves Lansdown

- RELX

There’s quite a lot of overlap with the companies held by Lindsell Train here, including Experian which has recently been added to the Lindsell Train UK fund.

There’s not that much overlap with the likes of Fundsmith or Blue Whale, although they tend to be less UK focused.

Games Workshop has been Buffettology’s biggest success story and has been held by the fund since it launched. Its shares rose only gently up until 2016 but they have gone from £5 to over £100 since then.

Other big winners over the years have been asset manager Liontrust and Bioventix, which develops antibodies for medical diagnostic tests.

Investment restrictions

Cribbing from the prospectus, Buffettology Smaller Companies will follow these guidelines:

- invest up to 10% (at the time of investment) in any one company;

- invest up to 25% (at the time of investment) in companies operating in a single ICB supersector;

- will not acquire securities that result in it controlling greater than 29.9% of the voting rights (at the time of investment) of any one company;

- will not invest in any unlisted securities; and

- will not invest more than 10%, at the time of investment, in closed-ended investment funds.

The second one, relating to sector diversification, probably needs expanding. There are 20 ICB supersectors, listed from page 9 onwards on this PDF.

But the prospectus also adds that “it is unlikely that the Company will invest in early-stage technology or biotechnology companies, mining and extraction companies, or companies in the banking and insurance sectors.”

So that would seem to rule out four supersectors and cuts down the options somewhat in a further two.

There’s no explicit ethical stance but companies will be bought with long-term sustainability in mind.

Early on in this process, is a key question: “is this a company Sanford DeLand expects to be around, in more or less its current form, in 20 years’ time?”. If the answer is “no”, Sanford DeLand will not invest.

The prospectus states that there are around 600 listed UK companies valued at between £20m and £500m but that Sanford DeLand only considers about 200 of these to be in its investable universe.

It seems likely that the trust will carry a small cash balance most of the time as the prospectus suggests it will use a watchlist to monitor potential investments so that they can be bought when “pricing opportunities arise”.

When it comes to selling investments the two main triggers are likely to be a material change in the business’s prospects or the acknowledgement that the initial assessment was flawed.

Positions won’t be sold because their valuation dips below £20m or rises above £500m. Additionally, it’s stated that “it is highly unlikely that a decision to sell an investment will be made on grounds of an apparent temporary overvaluation of its share price.”

Buffettology’s track record in smaller companies

Perhaps the most contentious thing in the prospectus, which is also reproduced in the three-page flyer, is the extracted track record of Buffettology’s previous smaller company investments.

There are some eye-popping numbers here but I think they needed to be treated with caution.

As the prospectus highlights, the performance figures seem to be heavily dependent on the gains from just two companies (Games Workshop and Liontrust) that returned over 1,000%.

It also tells us that 26 companies valued between £20m and £500m at acquisition by the Buffettology Fund and have been used in this calculation but that the total number of companies used in the monthly weightings was between 10-20.

So even with the 10% cash weighting, it’s a highly concentrated portfolio and certainly much more concentrated than the investment trust is likely to have.

I’m a little surprised this chart was given the prominence it was. I’d like to have seen a few examples of the actual weightings used so that we could have had a better idea of the concentration.

In fact, given there were only 26 companies used in the calculation, you could have included time held, total gain over that period, and average monthly weighting for all of them.

Portfolio candidates

Looking at the portfolios of the Buffettology Fund and Free Spirit as of 28 February 2020 (the last full list available right now) should give us some idea of the companies that may be bought by the trust.

Here they are, listed in order of percentage of assets they represent:

Buffettology Fund

- Focusrite

- AB Dynamics

- Bioventix

- NCC Group

- MJ Gleeson

- RM

- Craneware

- PayPoint

- Trifast

- Scapa

- Provident Financial

- The Restaurant Group

Free Spirit

- EKF Diagnostics

- dotdigital

- Mortgage Advice Bureau

- Tristel

- Tatton Asset Management

- Bloomsbury Publishing

- The SimplyBiz Group

- Craneware

- MJ Gleeson

- Vp

- S&U

- Eleco

MJ Gleeson is the only duplicate between the two open-ended funds.

Of the companies Buffettology and Free Spirit are already invested in, I think only Eleco is valued below £100m.

We can also add Driver Group (£25m) and Air Partner (£40m) that were called out in the Trustnet interview I mentioned above. These were recent sells made due to the size constraints of the open-ended fund. Revolution Bars was also mentioned but it has slipped back below £15m.

It’s been a while since I’ve looked closely at individual small-caps such as these but, from what little I do know, this list does seem a bit of a mixed bag.

It’s pre-COVID-19 of course and the world has changed a great deal, so it may be that many of these companies might not make it into the portfolio of Buffettology Smaller Companies.

Directors

The trust will have four directors, of whom only Stephanie Eastment seems to have extensive experience of being on the board of an investment trust.

They are due to be paid £113,000 between them, which is pretty competitive.

As noted in the Key Info section, they plan to invest a collective £105,000 in the IPO. That’s a decent show of support but nothing out of the ordinary.

However, there appears to be no information on how much Keith Ashworth-Lord and other staff at Sanford DeLand plan to invest, which is very disappointing.

Charges

Not a lot to say here at this stage.

The investment trust has a lower management charge paid to Sanford DeLand than the open-ended funds. That results in a slightly lower total cost of 0.96% versus 1.2% for both open-ended funds.

However, that 0.96% figure is dependent on £250m being raised, so it could be higher if the IPO falls short.

It seems a fairly average charge for a trust of this size that invests purely in listed companies.

The placing programme

The IPO is looking to raise as much as £250m but there is also a placing programme that will use C shares to potentially raise another £350m between the IPO date and 29 Sep 2021.

C shares are often used by trusts that want to raise a significant amount of new cash but where the proceeds take a while to invest.

The idea is that two separate portfolios are created so that the original investors don’t suffer a cash drag while the new money raised is put to work.

Once the new money has been invested, the C shares are converted into ordinary shares and the two portfolios are merged.

I don’t have any strong opinions on the use of C shares but the sums involved look a little large for a trust looking to invest in companies as small as £20m.

Seeing as the Tellworth trust didn’t manage to raise £100m and had to pull its IPO, I may be worrying about something that’s never going to happen.

But if this trust hit £500m and was spread over 50 companies, its average position size would be £10m. That could make investing in anything under £100m much more difficult.

Should the placing programme be mostly utilised, I’ll be watching to see what impact this has on the portfolio and any comments made by the investment team.

Summing up

Despite being cautious about IPOs in general, this is the second I’ve subscribed to in the last two years (Smithson being the other one).

Both times I have taken only a very small position at the outset, so I don’t feel too guilty about my weakness of chasing the shiny new thing.

And in both cases, it’s allowed me to buy an investment trust run similarly to an open-ended fund that I’ve admired for some time.

I’ve added to Smithson several times since it floated and I may do the same with Buffettology Smaller Companies if it continues to look promising.

An overly aggressive placing programme is probably my biggest concern right now but I’d also like to see how much the team of Ashworth-Lord, Vaughan, and Burns have invested.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

I found this a very interesting and informative article. I’ve been thinking about this IT and your article preemptively addresses many of the questions I had! Many thanks and keep them coming!

Thanks, David.

It’s always a leap of faith when it comes to trust IPOs, as they start with a blank slate, but there’s arguably a bit more to go on here than usual as we can see the two existing funds they run.

It’s going to be interesting to see how much interest there is for this one. It doesn’t seem to have generated that much coverage from what I can tell. I suspect it will manage £100m, and therefore go ahead, but I would be surprised if they get the full £250m.

Sorry to see this now got pulled:

https://citywire.co.uk/investment-trust-insider/news/buffettology-becomes-second-small-cap-trust-to-pull-launch-but-fintech-fund-tries-its-luck/a1417488?ref=investment-trust-insider-latest-news-list

I’d been looking to get involved with this post-IPO; I’d found your analysis of the potential portfolio particularly interesting.

You think they’ll try again when there’s clear sky ahead post-Brexit/Covid/US election?

Hi David,

Yes, it was a shame. Ashworth-Lord appeared on the interactive investor podcast last week and although he couldn’t comment on how the IPO was progressing, it was very close to the last date for applications so I read that as a fairly good indication it was going to proceed.

Of the three UK IPOs that have been announced recently (Tellworth and Schroders being the others), Buffettology seemed to me to have the best chance of a successful launch. I would be surprised if the Schroder one goes ahead now, especially as it’s yet to publish a prospectus.

I guess whether Buffettology comes back for another go depends on how close it got to raising the amount required and what sort of feedback it got from institutions — which is something that rarely makes it way into the public domain.

However, it does seem pretty rare that trust IPOs come back for a second try so the odds probably aren’t great. I think Hipgnosis Songs was the last one that did and got away successfully.

I agree with all you comments above – this was by far the most attractive of the the 3 proposed IPOs IMHO.

Even though I much prefer closed ended funds, on the back of the launch being pulled I am looking closely at the Free Spirit fund as I like the approach (hadn’t realised quite how small it currently is).

I found this interesting comment in the annual report (Feb 2020) which explains the (deliberate) small overlap between the 2 open ended funds:

“…In the summer, we took the decision to reduce overlapping

holdings between Free Spirit and UK Buffettology so that investors

can hold both funds side-by-side without undue concentration at

the individual company level….”

…which explains your observation above.

Keep up the excellent analysis – really enjoy reading articles like this!

Thanks, David. Even though the IPO was pulled, I still found it useful to do the analysis. I found this video on both the open-ended funds which may be of interest – yet to watch it myself though.

https://candlewickcapital.com/2020/09/14/buffettology-and-free-spirit-joint-webinar-recording-09-09-20/

Ah thanks for that! Just watched it and approx 5 mins was spent explaining why both OEICs are complimentary with minimal holding overlap and should not be thought of as an “either/or”.

Just out of interest on your travels did you find any indicator of how much “skin in the game” either of the managers have in their funds?

I didn’t find any info on that I’m afraid. Some open-ended funds seem to disclose it in their annual report but I didn’t see it in the latest one for Buffettology/Free Spirit.

Hi again – in the most recent AJ Bell podcast (dated 04/11/20) there was an interesting interview with Keith A-L.

Couple of key takeaways (for me at least!)

* Definitely planning to having another go at launching the IT – next year (“it’s oven ready!”) as the hard work has been done – but post US election/Brexit

* Blamed failure of this launch squarely on impending lockdowns

* Planning a global fund launch next year with same methodology. Sounded like it’ll be an OEIC not IT – but I still found this an interesting prospect!

Regards

oops – meant to post the link to that podcast – it’s here:

https://www.youinvest.co.uk/podcasts

Thanks David – will download that when I get the chance.