Like many folks, I have been astonished by events at Woodford Investment Management. I knew it had some issues but not having followed the situation too closely, I didn’t realise quite what a massive hole it had dug for itself. And new revelations seem to be coming out on a daily basis.

I have to admit, though, as the discount on Woodford Patient Capital Trust widened towards 20% earlier this year, I was starting to get a little intrigued.

I’ve always liked the long-term approach WPCT was taking, its focus on home-grown businesses, and the fact that it only charges a performance fee and no basic management fee.

Indeed, it’s astonishing that Woodford took such an innovative approach when it came to WPCT’s charges, yet is refusing to waive the management fee for his Equity Income fund.

I had seen the net asset value of Woodford Patient Capital start to increase during 2018 and it looked, perhaps, as if the fund’s earliest investments might be starting to deliver.

So, Woodford Patient Capital began to creep up my article to do list. But it never reached the top.

I knew the Shareprophets website had been running articles criticising Woodford for a few years, and particularly over the last 18 months. Not being a paid subscriber of that site, I didn’t know the specific points being raised. But I was aware that they’ve exposed a number of small-cap shares over the past few years, so that had me a little on guard.

In March, the asset swap deal with Woodford Equity Income fund and the listing of private companies on the Guernsey Stock Exchange to get around unquoted asset limits came to light. Both smelled a bit off to me, so I lost interest in WPCT.

That was more luck than any investing genius on my part. I certainly never expected the carnage that followed a couple of months later.

Woodford and me

I’ve invested with Neil Woodford in the past, for many years having a chunk of my SIPP in Invesco High Income. That fund did pretty well for me.

But when Woodford left Invesco in 2014 to set up his own business, I decided not to follow him out of the door. His successor, Mark Barnett, seemed to follow a very similar approach so I took the lazy option and stayed put.

A few years later on, growing increasingly disillusioned with both Invesco High Income’s returns and the prospects for the UK market, I did belatedly switch into Fundsmith Equity.

My wife had a holding in Edinburgh Investment Trust – also run by Barnett – but that was ditched recently.

The rush from equity income funds

It’s clear from the FCA’s response to Nicky Morgan, the Chair of the Treasury Committee, that I wasn’t the only one to get disenchanted with equity income funds.

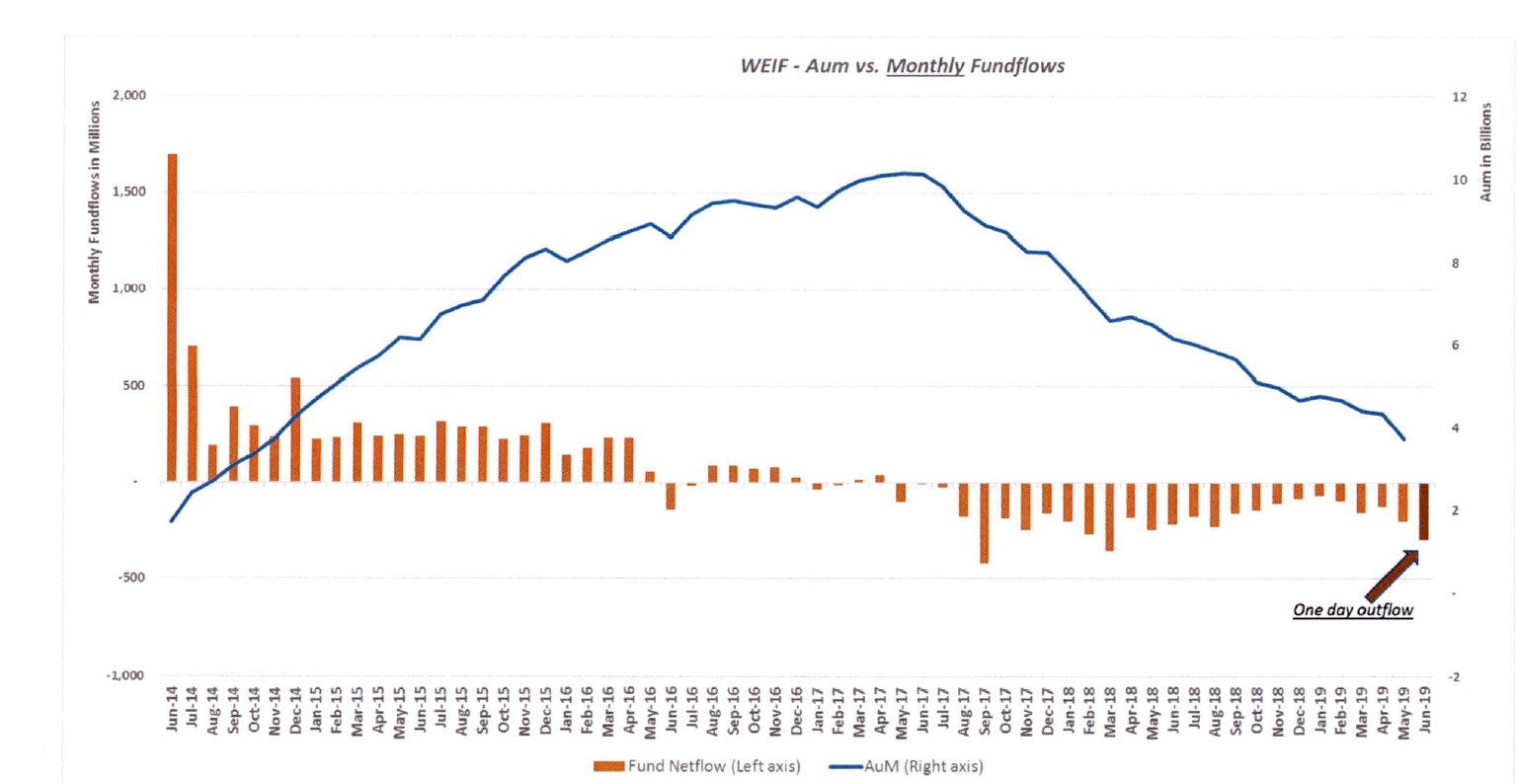

This chart shows the net flows in and out of Woodford Equity Income since it was set up five years ago.

The performance of this fund was actually very good for its first two years. And the money poured in.

You can see the first outflow month was when the EU referendum took place three years ago. That was when Woodford’s lead over the UK market started to shrink, although both the fund’s price and its assets under management continued to climb for another year.

April 2017 marked the start of a series of investing disasters for Woodford with Provident Financial falling from over £30 to less than £10. Others followed: Capita, the AA, Allied Minds, Purplebricks… the list goes on.

Every month since August 2017 saw serious money flowing out of Woodford Equity Income. A total of £4.3bn was taken over the last two years, according to the FCA.

This isn’t just a Woodford issue. Morningstar reckons some £15bn has flowed out of UK equity income funds in the last year and a bit, equivalent to about 20% of the sector’s value beforehand.

Punting on Patient Capital?

I’ve seen a few people suggest that because Woodford Patient Capital has fallen so far that it might be worth a punt.

Personally, I’m steering clear as I suspect there is a lot still to come out the woodwork.

The net asset value of the trust has fallen to 83.8p as of 20 June, down from 89.6p on 3rd June when the main fund was suspended, and a high of 105p back in November 2018.

That makes the current discount a massive 35% on the share price of 54.5p. David Stephenson reckons a discount of 40-50% might see some value hunters emerge.

The latest factsheet for Woodford Patient Capital is as of 30 April 2019 (yes, I would have expected May’s to have been released by now, too). This attributes around 16p of the net asset value of 96.7p at that time to Benevolent AI and Industrial Heat. Both holdings, and how they have been valued, have come under scrutiny by the Financial Times in particular.

The main Woodford Equity Income fund also owns many of the investments held by WPCT. These stakes need to be offloaded, and that is likely to decrease their value.

It’s unclear if WPCT will be a seller as well. Recently, it’s been right up to the limit of its £150m overdraft. Earlier this year “the bank overdraft facility was extended by 364 days to 16 January 2020“. I imagine the next review meeting will be a spicy affair.

The overdraft accounted for 19% of net asset value at 31 December 2018. Some new shares were issued earlier this year, but if the overdraft is still at £150m, it’s only just under 20% of net assets, which is WPCT’s stated gearing limit.

I reckon a net asset value of 82.5p or lower would take gearing over 20% at the maximum overdraft amount.

All quiet at the top

Strangely, the board of WPCT have been pretty quiet these past few weeks.

There was a brief statement saying that it was “pleased with the operational progress of its portfolio companies, which [it] believes continue to have the potential to deliver attractive returns, in line with the long-term mandate of the Company. The operational performance of these businesses is not impacted by recent events.”

No doubt there’s been a lot going on behind the scenes. If I were a shareholder, I’d be expecting to see a full review of how all investments have been valued, focusing on any uplifts since the trust first invested.

WPCT’s next set of results are for the half-year to 30 June. Its interims were released in early August in 2015, 2016 and 2017 but not until late September in 2018. Three months seems far too long to wait.

And I really can’t see how Woodford can remain as manager of WPCT given all that’s transpired.

How long will the suspension last?

Hargreaves Lansdown has published an update saying that the price of Woodford Equity Income has fallen by 5% since the fund was suspended (similar to WPCT’s net asset value reduction).

The suspension has to be reviewed at least every 28 days, meaning Monday 1st July is the latest date that can happen.

I’ve seen some speculation that the suspension could last several months. Given the FCA’s letter suggested that 33% of the fund’s assets as of 30 April were likely to take more than 180 days to sell that seems credible.

A further 32% was deemed to be liquid within 20-180 days. And, of course, the liquidity situation is only likely to have got worse since the end of April, given the redemptions since then.

Can we take some positives?

It might seem ghoulish to say that some good might come out of this sad affair, given nearly £4bn of investors’ money is still trapped in the suspended Woodford Equity Income fund. My sympathies are obviously with those affected.

But this does feel like a fairly isolated incident. It was a combination of a dominant personality that cut corners, mixed investment styles, and investing far too much in hard to shift assets in an open-ended fund.

I think we should be thankful that this has happened at what seems to be a fairly calm period for the stock market in general. Had it happened when prices were sliding, I think the fallout/contagion could have been far worse.

It also reminds us that investing is hard. Watching the likes of Scottish Mortgage, Lindsell Train and Fundsmith surge ever higher in recent years, it’s easy to forget that. A bit of humility every now and again, or even a slap round the face, can be essential.

None of these popular funds would seem to have the same liquidity issues as Woodford. Fundsmith, in particular, has always been at pains to adjust its investable universe as it grew in size, which was one of the reasons it created Smithson of course.

An open-ended disaster

It looks like something will be done about the decidedly suspect practice of holding illiquid assets in open-ended funds.

We saw a similar issue with funds that directly invested in property after the Brexit vote. Half of this £25bn sector ended up with its assets frozen for a number of months.

In normal conditions, it doesn’t matter of course. But in times of stress, when everyone rushes for the door at the same time, the system crumbles.

Thinking back, I’m actually surprised fund suspensions weren’t more of an issue during the Financial Crisis of 2008-9. Perhaps I just missed it, or perhaps alternative assets were too small to be an issue back then.

As a fan of investment trusts, I’m obviously keen to see more people get interested in closed-end funds. They’re clearly more appropriate for holding illiquid assets. However, it’s worth noting that investors in WPCT have seen its share price fall from 76.5p to 54.5p since Woodford Equity Income was suspended. That’s a fall of nearly 30%.

Yes, they can still sell, but it’s conceivable that their losses could end up being even greater than those still left in the Woodford Equity Income fund.

Listed, well kind of…

The FCA’s letter highlights that most funds have a 10% limit on unlisted securities (although non-UCITS funds can have 20%), but that the definition of unlisted is pretty woolly.

And it also seems that breaches that happen mid-month but are resolved by the end of the month go unreported. If I’m holding a fund, I’d rather know that it was sailing that close to the wind.

I actually quite like the simple ‘bucket’ approach that Link Financial Services, who runs Woodford Equity Income, uses. It would be good to see this used across other funds and investment trusts, to give us a better idea of what our underlying holdings consist of, and to see how this ratio changes over time:

Fund fees and Best Buy lists

Hargreaves Lansdown is coming under a lot of scrutiny for its promotion of Woodford Equity Income in its Wealth 50 list. It recently defended its stance in this letter to Nicky Morgan, outlining a lot of what happens behind the scenes. It’s well worth reading.

It’s clear it had fairly major doubts about Woodford, yet out of 3,000 funds its clients could invest in, it still thought two of Woodford’s deserved to be in the top 50.

The FCA reckons Best Buy lists have outperformed other funds — but its study only looked at the period from 2006 to 2015. A lot has happened in those last four years and I wonder if you’d get the same result now.

I’m also not a fan of funds having different levels of charges. Woodford Equity Income has four — A,C,X and Z — but I don’t think it’s unusual in that regard.

Z is the cheapest at 0.65% a year and A the most expensive at 1.5%. Typically, the most expensive is for those buying directly while the largest platforms, like Hargreaves Lansdown, get a discount for volume.

In addition, Hargreaves Lansdown was able to negotiate a further discount so its clients only paid 0.6% initially, and 0.5% from January 2019.

Hargreaves says its Best Buy lists are research-led, but there’s obviously a conflict of interest here. In my ideal world, a fund would just have a single charge and then platforms can compete using their own fee structures.

Passive gets another boost

As Monevator eloquently said a couple of weeks ago, the biggest takeaway is that the average investor is likely to be better off in index funds.

I’m still in the camp that it’s possible to beat the market. But it’s certainly not easy and it takes a lot of work, both upfront and on an ongoing basis.

Most people, and by that I would say perhaps as much as 99% of us, should have their investing decisions on auto-pilot.

I should probably close this rambling piece with a couple of things I hope don’t happen — although I fear they might.

I hope the regulators don’t overreact and bring in a raft of new restrictions around funds in a knee-jerk response. We could see them coming down on the companies that administer these funds, and costs for investors rising as a result.

And I hope people don’t get put off investing by this fiasco. Yes, there are risks but they can be sensibly managed. By far the biggest risk to your wealth is that you sit in cash and never invest.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

I forgot to mention that Dan Grote at Citywire has done some excellent work on the ongoing Woodford saga.

https://citywire.co.uk/investment-trust-insider/author/dgrote

Good article, thanks.

For WPCT the 20% gearing limit is only relevant at the time of borrowing. At 31.12.2018 gearing was at 19% of NAV so now as the NAV has fallen it’s very likely the gearing is well over 20%.

That shouldn’t cause any issues in itself. But of course on roll-over of the loan there’ll be some interesting discussions. In today’s lending market it’s unlikely to be a problem, except the interest rate payable by WPCT will increase due to the higher loan-to-value. And of course if there is stress in the loan markets and the loan called in, WPCT will need to do a fire sale of assets to meet the loan repayment.

So there are some risks with this holding. I have some shares but will not sell at these prices but nor will I add due to the risks you’ve mentioned here.

Actually this whole Woodford scandal is quite sobering:

A fund investing in early-stage / binary outcome companies that don’t pay any dividends should have gearing of ZERO. That’s just a basic common sense. What on earth was Woodford thinking? And the directors surely were asleep or incompetent. What was I thinking investing in this?