When it comes to running my portfolio, I spend a fair amount of time thinking ahead. I like to plan what new money I’m likely to add over the next year, whether to shift my position sizes a bit, and sell a holding or two to use up my annual CGT allowance.

I also like to try and prepare myself mentally for the next major market slump. And for this, I generally look back at what’s happened before to get a sense of what sort of falls are likely and for how long.

Doing this has helped me through the two market meltdowns of the last twenty years.

They still hurt like hell of course, but they stopped me making the big mistake of selling out because you’re frightened of where the market might go next.

Two decades of not a lot

History doesn’t tell us precisely what will happen next. Far from it. But it does provide a useful guide as to what to reasonably expect.

Being an investing nerd, I’ve been looking at studies of long-term market returns since the late 1990s. Ironically, over that timeframe, UK equity returns have been pretty unspectacular.

The FTSE 100 hit its infamous peak of 6,930 in December 1999. It didn’t rise above that level until February 2015.

Right now, the index only stands at around 7,300, just 5% higher.

Add in reinvested dividends and we have a 143% gain since the end of 1999. That sounds pretty decent, but it’s only equivalent to 4.6% a year.

The 2000s and 2010s have been a tough time to be a UK equity investor.

Taking a world view

Most investors have become increasingly global in their outlook. So we need to expand our investing history, too.

Credit Suisse’s latest yearbook puts world equity market returns at 5% a year. That’s net of inflation since 1900.

Bonds have returned just under 2% and cash just under 1%.

These figures are based on 23 markets which account for some 90% of current world stock market valuations. It includes total wipeouts in Russia and China for several decades and near zeroes from Germany and Japan.

The global stock market has been a resilient beast, to put it mildly.

It’s not been a smooth ride for shares, though. Bonds have done better the last twenty years or so, as interest rates have tumbled. However, the two decades before that, the 1980s and 1990s, were a great time to be invested in shares.

The UK has performed similarily to world markets in the long term (since 1900) and the medium term (since 2000).

European countries have largely been the laggards, while Scandanavian countries, North America, and Australia/NZ have done better than average.

The average that rarely happens

We know a market slump is coming at some point. However, we don’t know when, how deep it will be, or how long it will last for.

When I first started looking at long-term returns, I focused on the average annual percentages and used them to do some rough calculations of how my money might grow.

But discussion around this topic has become much more nuanced in recent years.

Yes, the average might be 7-8% a year (if we assume 5% plus inflation of 2-3%) but many individual years boast returns of 20%+ or losses greater than 5%.

Indeed, it’s a rare year that ends up producing returns in the range of plus 5-10%.

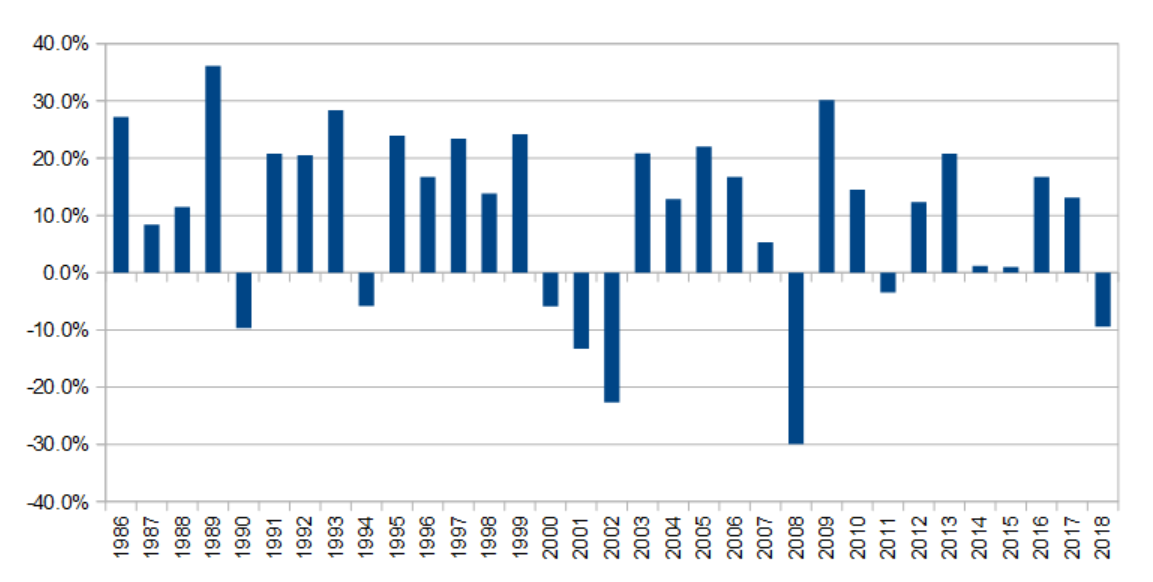

Here are the annual returns for the UK market, including dividends, since the mid-1980s:

Out of the last 33 years, only two of them produced ‘average’ returns between 5 and 10%.

Even more bizarrely, those two years were 1987 (8.4%) and 2007 (5.3%) — hardly the two times you would have expected to be the most average.

Calendar years can deceive, too

Looking at the totals for individual years conceals some wild swings.

The market crash of 1987? Not obvious from the chart above.

The Asian and Russian crises of 1997/8 which put paid to Long-Term Capital Management? Nope. The UK market declined 24% between July and October 1998 but again it’s not obvious from this chart.

There were falls of nearly 20% in 2010/11 and 2015/16, too. Both are MIA, although these annual figures show 2011 as producing a small drop.

A quote to invest by

I’ve used this quote from Morgan Housel before. It’s such a great frame of reference, it’s well worth wheeling out again:

Markets crash all the time. You should, at minimum, expect stocks to fall at least 10% once a year, 20% once every few years, 30% or more once or twice a decade, and 50% or more once or twice during your lifetime. Those who don’t understand this will eventually learn it the hard way.

The two takeaways for me: big falls are part of the way the market works and they occur more regularly than you might expect.

Since I’ve been an active investor, the largest peak-to-trough UK market falls I’ve experienced have been 24% (1998), 48% (2000-03), and 46% (2008-09). I’ve seen three other drops of 15% or more.

I’m kind of hoping those last two could turn out to be my ‘50% or more’ lifetime falls, but I’m certainly not going to count on it.

There’s no law saying markets have to behave as they have done in the past.

In terms of duration, the falls of less than 25% I’ve witnessed lasted about a year at most before the market regained its previous peak.

The two major ones lasted a little over five and three years respectively.

Prepping for the next one

It’s now a decade since the last major market slump. I’ve no idea if another one is just around the corner or another decade or more away.

But I’d much rather decide what I’m going to do in advance. I don’t want to be forced into action when the headlines are all screaming “meltdown!”

My basic strategy with the last two major falls has been pig-headed obstinance: I didn’t sell out of any positions and move into cash to wait it out. That’s because I don’t believe market timing is a sensible strategy.

At times, I have let my cash balance build up a little, but more because of a lack of conviction about what to buy rather than general market concerns.

Seeking safety in cash often seems like a smart move. But much more often than not, markets tend to rebound and being out of the market is a costly mistake. So I play the odds, accepting that occasionally this will mean getting stung.

I reckon I’ll approach the next slump, whenever it happens, in much the same fashion.

My portfolio looks somewhat different, though. It’s much more global and I think it’s a little less risky overall due to the infrastructure trusts I have been investing in. While I have a fair amount of small-cap exposure, it’s less than I had going into 2000 and 2008.

Everything changes

However, things have changed a lot for me on a personal basis since the first two major drops.

When the first one came along, I was single and didn’t have that much invested. The new contributions I was able to make every year to my portfolio made a significant difference.

The first drop was also a little different in that it was a lot more drawn out than the global financial crisis. It was more death by a thousand cuts than the swift beheading of 2008-09.

Strangely, as I look back on it now, I actually don’t remember as being that bad from an investment point of view.

It was largely confined to technology and media shares, while more traditional businesses actually did quite well, as they were on such low valuations.

I had some tech exposure — heck, I even bought some Lastminute.com — but nothing too aggressive.

Panic on the screens of London

The global financial crisis was a much sterner test for my investing cojones. It was absolutely brutal at times, with more and more terrible news piled on day after day.

I remember thinking it could actually be the end of the financial system as we know it. Subsequently, reading accounts of those involved in the bailouts, I realised how close we came.

The first phase of the financial crisis lasted for a year and a bit, taking out the likes of Bear Stearns and Northern Rock. But it was the six months starting in September 2008 where most of the carnage happened.

My portfolio took one hell of a beating. I was living with my soon-to-be wife and we were both earning decent salaries. I was able to invest a reasonable amount of new money and by the end of 2009, my investments were worth more than they were at the end of 2007.

Why #3 could be tougher for me

I’ve continued to invest regularly and my portfolio is worth many times more than it was prior to the last market meltdown.

That’s not because of any great genius on my part. It’s mostly down to saving hard and riding the markets higher.

But it also changes things. Sure, the last fall hurt in percentage terms. But the pound damage the next one inflicts could be an order of magnitude greater.

I’m not sure how that might feel.

I’ve got a lot less time to recover financially, being that much closer to official retirement age. And as I’m now working part-time, I’m not adding as much in the way of new money to my portfolio.

Plus, I’ve got two young kids. That changes your perspective on all manner of things.

All things considered, while I think I can draw confidence from the (pig-headed) way I faced my first two market slumps, I need to be prepared for the fact the next one is likely to feel very different.

In other words, I shouldn’t get too cocky just because I survived similar episodes before!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

I think I could face a third financial crisis, in fact a rerun of anything since 1985, and in my records only in 2001, 2002, and 2008 have losses exceeded 10% on a calendar year basis. I would stay invested through such a crisis.

I’m less sure about things if it is a rerun of the 1930’s depression or the 1970’s stagflation.

I’m less sure about things if it is a rerun of the 1930’s depression or the 1970’s stagflation.

Yes, not having lived through those periods, as an investor anyway, I think it’s much harder to envisage how they might feel. I think the latter is the more likely of the two to recur (the world was such a different place in the 1930s), but who knows what might happen.