SDCL Energy Efficiency Income Trust, or SEEIT, is one of the newest members of the renewable infrastructure sector that has been hoovering up investors’ cash these past few years. But it offers something a little different.

The third pillar theory

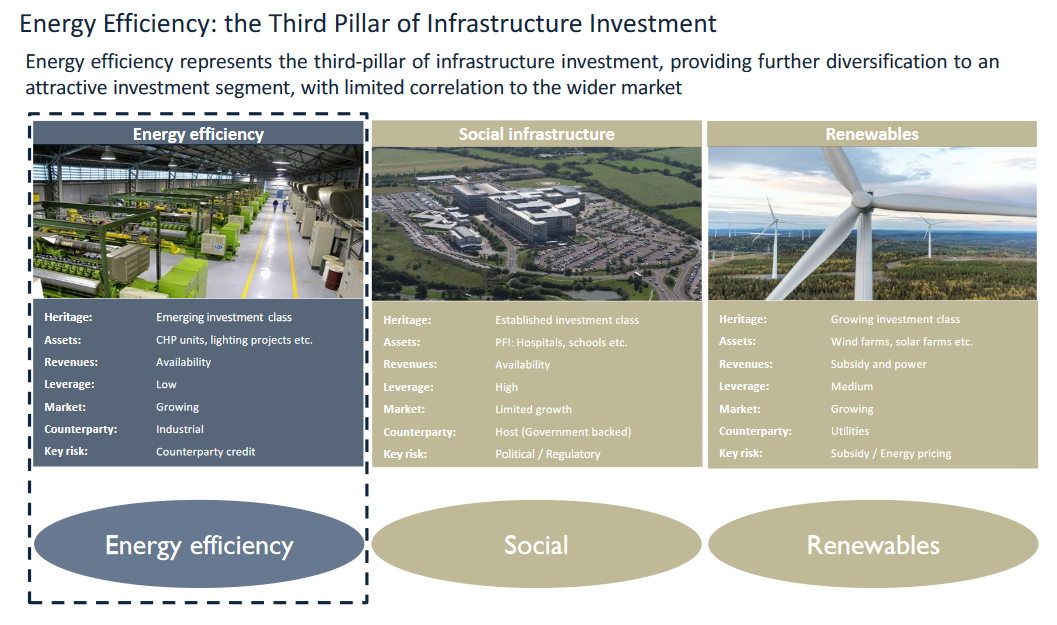

SEEIT describes energy efficiency as the third pillar of infrastructure investment, as shown in this slide from its latest presentation:

The first pillar is therefore what most people would understand by infrastructure: roads, schools, hospitals etc. The second is renewable energy generation: like wind and solar farms.

The third is making buildings more energy-efficient, either reducing their power consumption through things like LED lighting or generating power on-site via combined heat and power systems (CHP) or biomass boilers.

On-site generation should provide a more secure and resilient energy source and also reduce costs as less power is lost in the distribution process.

As these can be large, infrequent projects, SEEIT allows companies to offload some of the financial risk and also benefit from its expertise of the technologies concerned.

The growth of energy efficiency

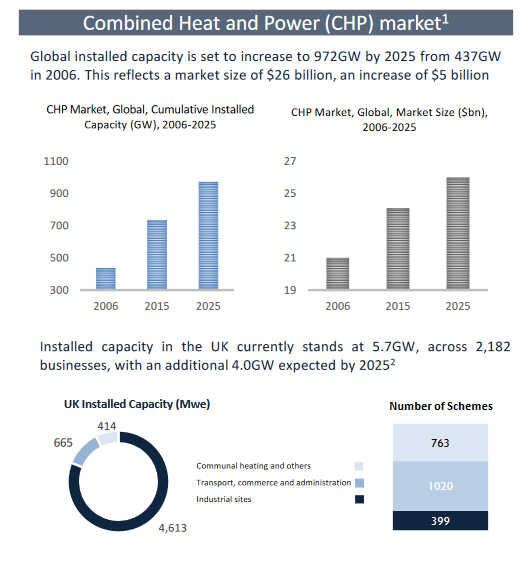

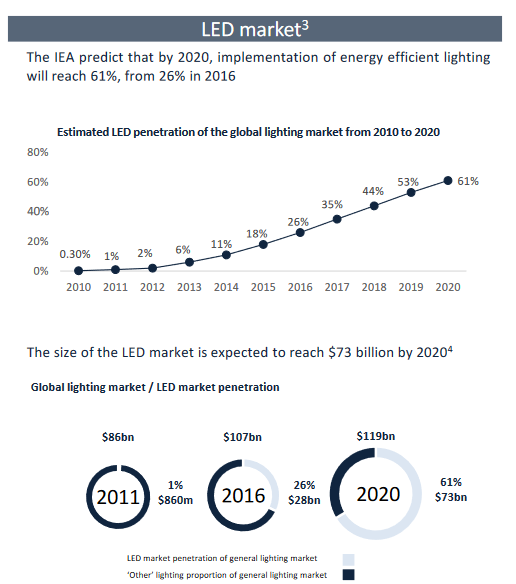

SEEIT has produced a couple more charts, showing the growth of CHP and LED technology:

We can see that the LED market is growing far more quickly than the more mature CHP market. However, in the UK, CHP appears to be growing slightly more quickly than it is elsewhere.

What’s SEEIT done so far?

SDCL Energy Efficiency joined the London Stock Exchange in December 2018, a couple of weeks before markets bottomed out. So, it did pretty well to raise £100m out of its original £150m fundraising target, given how skittish investors were at the time. A link to its Prospectus can be found here.

£87m of that £100m was spent on acquiring a seed portfolio from SDCL’s main existing fund. £57m was for assets that were already up and running while the remaining £30m was for “contracted investment opportunities”.

A small US acquisition for £4m, being a 71% stake in a CHP project, followed in March 2019.

Then £72m of funds were raised in April. The placing price was 101p, a whisker over the 100p flotation price.

An initial dividend of 1p was declared in May, while June saw a deal with Tesco to provide rooftop solar panels for its supermarkets. This is for a £5m spend initially, with plans to add a further £10m.

And a few weeks ago, SEEIT published its first set of results, covering the period to 31 March 2019 plus a useful accompanying presentation. (I can see a full report has also been published since I completed writing).

When SEEIT joined the market, its net asset value dropped from 100p to 98p due to flotation costs. The 31 March 2019 revaluation saw this number increase slightly to 98.4p. Net asset values will only be provided every six months, as of 31 March and 30 September.

A punchy premium is par for the course

SEEIT’s share price started rising steadily in February and currently stands at 107p. That puts it on a 10% premium to its latest net asset value, once that’s adjusted for the recent 1p dividend.

That sounds pricey — well, it is pricey — but it’s lower than the 15% average premium across the wider renewable infrastructure sector.

Newer funds tend to trade at smaller premiums, as you might expect, with US Solar and Aquila European Renewables both around the 5% mark. More established funds are in the high teens right now, with Bluefield Solar Income Fund at an eye-watering 22%.

The lower premiums on the newer funds is one of the reasons I’m sniffing around these trusts as I build up the green credentials of my portfolio. As a trade-off, you do have shorter track records and often brand-new types of infrastructure investment (as far the retail market goes).

Here are SEEIT’s largest investments right now:

Santander UK Lighting, 28% of portfolio

This is a LED lighting project comprising 90,000 lamps across over 800 of Santander’s offices and branches across the UK. Building management systems, processes and optimisation and HVAC (heating, ventilation, and air conditioning) units have also been installed in certain offices. The agreement for the provision of lighting has 7 years remaining.

In January 2019, Santander announced it would be closing 140 UK branches over the course of 2019, although it’s not clear how many of the 800 the SEEIT deal covers are affected. A payment from Santander is expected to compensate for any branches closed.

Moy Park Biomass, 24% of portfolio

This project comprises 86 biomass boilers at several poultry farms operated by Moy Park in Lincolnshire and it has 17 years left to run. The supply agreement includes a fee for each boiler plus a variable amount for heat produced above a threshold.

The project is also entitled to a sum under the Renewable Heat Incentive from OFGEM, calculated with reference to the heat output of the boilers. The biomass boilers use wood pellets as feedstock, provided under a 20-year agreement with Land Energy Girvan Limited.

There is also a separate lighting project for 15 Moy Park sites, worth another 6% of the portfolio and which has 5 years left to run. Moy Park is a pretty substantial company, with £1.5bn in turnover and £60m in profits as per its latest accounts.

Huntsman Energy Centre, 23% of portfolio

This project involves the installation of three steam raising boilers and two steam compressors at Huntsman’s premises at Wilton in North Yorkshire. Huntsman is a US-listed chemical company with a market cap of around £4bn.

The agreement covers design, building, operation, and maintenance. The steam generated will be sold to Huntsman in return for contracted revenues over 15 years.

This is SEEIT’s only construction project at the moment, but it has seen some delays which resulted in 10% being held back from the acquisition price.

Northeastern US CHP, 7% of portfolio

The project, which comprises CHP units for a prison, university, multi-family developments and a nursing home, has a total installed capacity of 2.5MW of CHP and 1,250 tonnes of cooling capacity.

The units are each subject to Energy Purchase Agreements, which benefit from long-term contracted cash flow, and each unit has been fully operational and revenue-generating for over a year. Revenues from the sites are generated through electricity sales, the provision of hot and chilled water and from electricity demand reduction.

Concentration concerns

It seems like a pretty concentrated portfolio right now, with the five assets described above comprising nearly 90% of its value. But if you add in the cash raised in the April fundraising, the largest project (Santander) comes down to 10% of net assets.

SEEIT’s Prospectus laid out dates for 4 separate fundraisings during 2019, one in each quarter. That timetable seems to has slipped a bit and no mention of further placings seemed to be made in its recent results.

This trust does seem to have a big pipeline of opportunities, with more than 20 projects valued at £770m. The bulk of this, £470m, is said to be CHP, with the balance of £300m from LED, rooftop solar and cooling.

The results presentation indicates that there could a couple of large deals in the pipeline. There is a range of deals sizes given for each of the two categories and the upper end is £150m for CHP and £125m for LED, rooftop solar, and cooling.

I’m not sure if these are specific deals or indicative sizes. If it’s the former it would be a major step in scale and potentially make the portfolio more concentrated than it is now.

The Prospectus sets out some investment restrictions, which are measured at the time of any new investment:

- at least 25% of assets to be in the UK;

- maximum single project and single counterparty exposure to be 20%; and

- projects in development and construction should not exceed 35%.

Nothing overly alarming there, although it seems likely that the portfolio could shift from being pretty much all UK today to being much more geographically diversified. The pipeline deals are located in UK, Europe, and the US.

Asset lives seem quite short

One quibble I have right now is that the asset lives seem quite short compared to other infrastructure investments I have looked at. HICL is up around 30 years, while Bluefield Solar is looking to extend its contracts from 25 years to 40. I work on the theory that setting up new projects is costly and time-consuming, so the longer the asset life the better.

SEEIT’s average is just 11 years and its Prospectus says most projects are likely to be between 3 and 20 years. LED lighting projects seem to have the shortest lives.

SEEIT also faces more counterparty risk, as the investing jargon goes. In other words, as its main clients tend to be corporates, they are more likely to go bust or change their plans than public-sector bodies. We’ve already seen an example of that with Santander’s plans to close some branches.

SDCL’s story

There’s not a massive amount of information on SDCL (which stands for Sustainable Development Capital LLP) in the SEEIT Prospectus, and its website is pretty sparse as well.

It was founded in 2012 by Jonathan Maxwell, who oversaw the 2006 flotation of HICL Infrastructure while working at HSBC. It has four funds, with a combined initial investment of £200m.

The UK fund accounts for half of that £200m and seems to have been effectively rolled into SEEIT via the acquisition of the seed portfolio. It has produced an IRR of 10%, but that largely seems contingent on the acquisition price of the assets being rolled into SEEIT.

The other funds (in Ireland, the US, and Singapore) are delivering at or above target returns, said to be CPI (i.e. inflation) plus 4%. These were set up a little later than the UK fund, in 2014 and 2015.

SDCL’s staff number 25, of which 15 are investment-related.

Maxwell’s connection to HICL looks to have got one infrastructure heavyweight onto SEEIT’s board, though.

SEEIT’s chairman, Tony Roper, was HICL’s fund manager for a number of years up until 2017. He has also sat on the investment committee of the Renewables Infrastructure Group (TRIG). He’s a director of Affinity Water and a non-executive director of Aberdeen Standard European Logistics Income.

The three directors of SEEIT subscribed for £65,000 of shares at the IPO and a further £20,000 in April’s placing.

Annoyingly, I can’t find any information on what Maxwell’s shareholding is. I’m sure I read somewhere that he has a significant stake, but it would be good to know the details. He is not on the list of major shareholders which covers holdings of 5%+.

The main institutional shareholders are CCLA (18%), Investec (13%), Newton (10%), M&G and Tesco Pension (both 9%).

Gearing, dividends, and target returns

SEEIT’s eventual gearing target is 35% of net assets (at the time of borrowing). There could be further gearing within project SPVs or for acquisitions that could increase this to 50%.

There is a £25m revolving credit facility that runs until June 2022, with the option for a further £40m of acquisition-related finance.

The initial annual dividend is expected to 5.0p, covering the year ending 31 March 2020. This would rise to 5.5p for the year ending 31 March 2021 and grow thereafter. Dividends are to be paid twice a year.

Targeted annual returns, after all fees are paid, are 7-8%. The CPI plus 4% figure mentioned earlier currently equates to 6%. Therefore, I would guess the target is roughly based on that plus 1-2% for a boost from the trust’s gearing.

Fees

These don’t seem too bad. SDCL gets 0.9% for the first £750m of net assets, and 0.8% over that level. There doesn’t seem to be any performance element.

The ongoing cost figure is currently reckoned to be 1.38%, once you add other fees like audit, registrar and so on.

Summing up

I’m very much in two minds about this as a potential investment.

As a form of infrastructure investment, it should be relatively uncorrelated to stock market returns. And it also should face less regulatory risk and be less exposed to power price fluctuations than other renewable infrastructure trusts.

Roper’s involvement is also reassuring. And it does seem that many of the first-movers in these types of specialised investments go on to provide the best returns.

But the shorter asset lives make me a little more cautious, as does the fact that I would assume that there is quite a lot of competition in LED lighting. On the face of it, I would have thought it is a fairly simple technology, so I’m not clear how much value SEEIT can add.

And if I was to be cynical, while its projects are energy efficient, its end clients of banks, car park operators, poultry and chemical companies wouldn’t tick many ethical boxes.

With target returns flagged at the 7-8% level, I’d like to see a lower premium as well. I suspect I’m likely to keep watching this one for the time being to see what progress it makes.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Thanks for the excellent write up ITI.

As you conclude, many of the projects are not very sound from an ethical stand point…poultry farms especially, so that would be a red line.

Also, I am not convinced that biomass is the solution to reducing CO2 emission. Many use wood pellets which are shipped in from the likes of the US and Canada. The transport is very carbon intensive and the net result is a higher carbon output per KwH compared to gas and certainly far more than solar and wind.

So personally, I will not be adding this to my portfolio.

Thanks diy. The Moy Park biomass project does indeed use wood pellets. It doesn’t say if they are imported but the supply agreement is with a company that has a wood pellet production facility at Girvan in Scotland, so I would guess they come from there.