Usually, an investment trust offers either income or growth. But a new kid on the recycling block, Gresham House Energy Storage Fund, appears to offer both: a 7% yield and the prospect of 8% capital growth. Is it too good to be true?

Gresham joined the market on 13 November 2018 at 100p, raising £100m in the process. The original fundraising target was £200m. However, as with many recent trust launches, the ongoing market wobble seems to have spoilt the party a little.

It’s an entirely new company that’s looking to build up a portfolio of energy storage systems (ESS), mostly using lithium-ion batteries. These will store power generated by wind turbines and solar panels when they produce more than is needed by the grid.

Why do we need energy storage?

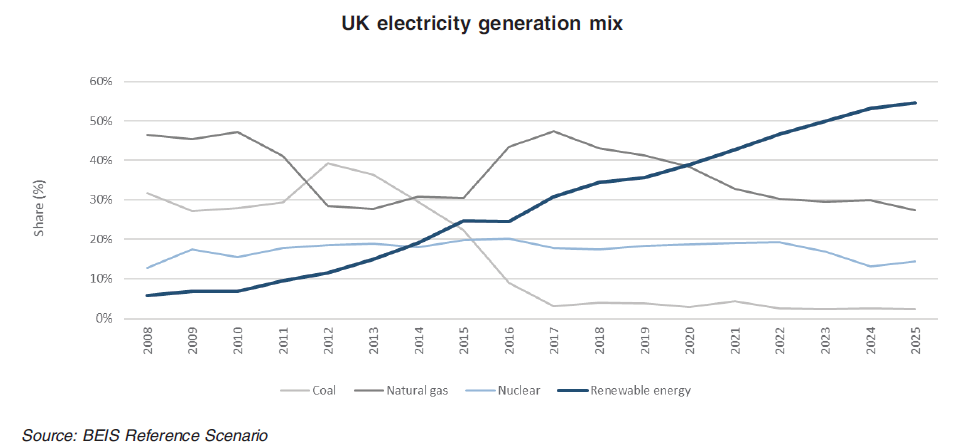

In short, government targets mean an increasing proportion of electricity generation in the UK is coming from renewable sources.

As the chart below shows, renewables currently account for about 30% of power generation in the UK, but that proportion could reach 50% within five years. Renewables have been replacing coal so far, but they may soon start replacing natural gas and nuclear as well.

Renewable power sources are more intermittent than traditional sources like coal, and their output rarely matches the daily and seasonal variations we see for electricity demand (more heat and light in the winter, the traditional kettle-based surges during adverts etc).

Increasingly, we need somewhere to store the power for a while, releasing it when needed. This is where energy storage systems come into play. They buy in electricity on the cheap when there is surplus supply — then they sell back at a higher price when there is surplus demand.

That’s the simple version. In practice, there are lots of complexities and long-term contracts involved when it comes to this type of business.

How energy storage systems make money

Rather than me reinventing the wheel, here’s how the company describes the four prongs of its revenue-generation model:

FIRM FREQUENCY RESPONSE (FFR)

The firm provision to the National Grid of a dynamic (i.e. proportionate) response based on changes in the UK grid’s electrical frequency, by either rapidly importing or exporting power to help maintain a steady 50Hz frequency.

ASSET OPTIMISATION

Projects are ‘optimised’ to maximise income from the wholesale (half-hourly) market and the balancing mechanism, through which National Grid balances supply and demand within each half hour, i.e. buying power at times of excess supply and selling power during periods of high demand.

CAPACITY MARKET

Introduced as part of the UK Government’s Electricity Market Reform in 2014. It pays generators a fixed fee for every hour they are available to deliver power when called to do so.

GRID PAYMENTS AT TIMES OF PEAK DEMAND

“Triads” are paid by National Grid to generators during the three half hours of highest annual demand. Payments are decreasing through 2021 as regulations change, however, several locations will continue to earn attractive income from Triads. Other grid payments can also be earned for generating during daily peaks. Amounts are specific to each project.

FFR is currently the major revenue earner, but National Grid is changing the way contracts are drawn up for this. The contracts only run for a couple of years (so much shorter than the lifetime of the ESS projects), so there is no guarantee that replacement contracts can be signed on profitable terms.

It’s asset optimisation which the company sees as the main revenue source going forward, possibly as soon as two years from now. This is essentially a play on the hourly/daily price of electricity becoming ever more volatile. Apparently, prices can even go negative at times (the first time this happened being back in 2015).

There’s a couple of tables in the prospectus which illustrate this revenue shift. In 2018, the assumption is for revenue of £189,000 per MW of capacity, comprising 89% FFR and 11% Triad.

The base case for 2019 and 2020 is for £78,000 per MW (a drop of nearly 60%). This breaks down as 73% asset optimisation, 11% FFR, 9% Capacity and 7% Triad.

What do ESS projects look like?

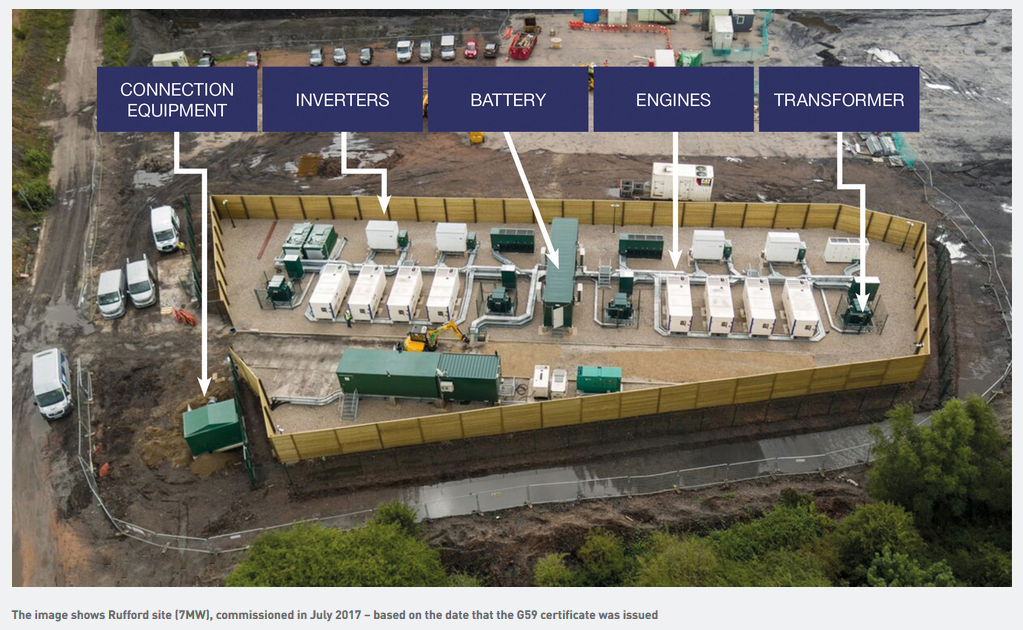

Not particularly impressive, I would say, at first sight anyway. The picture below is of Rufford, the smallest facility in the company’s seed portfolio at 7MW (some of the projects Gresham is hoping to buy are several times larger). It’s on land previously used for coal stocking at the former Rufford Colliery near Mansfield.

The trucks give an idea of the scale required and the equipment is apparently housed in shipping containers, so it’s easy to transport and replace. The containers have fire suppression and air conditioning systems.

These ESS facilities are operated remotely so tend to be unmanned apart from routine maintenance and repairs. The design is modular, so if one cell is not pulling its weight then it should be easy to slot in a replacement. The batteries are reckoned to last for 10 years or so.

Gresham says the planning requirements can be pretty laborious to navigate. I wouldn’t have thought these facilities pose too much of a risk to the public, but there could be end-of-life disposal costs. Most sites tend to be on agricultural, commercial or industrial land.

What projects will the fund invest in?

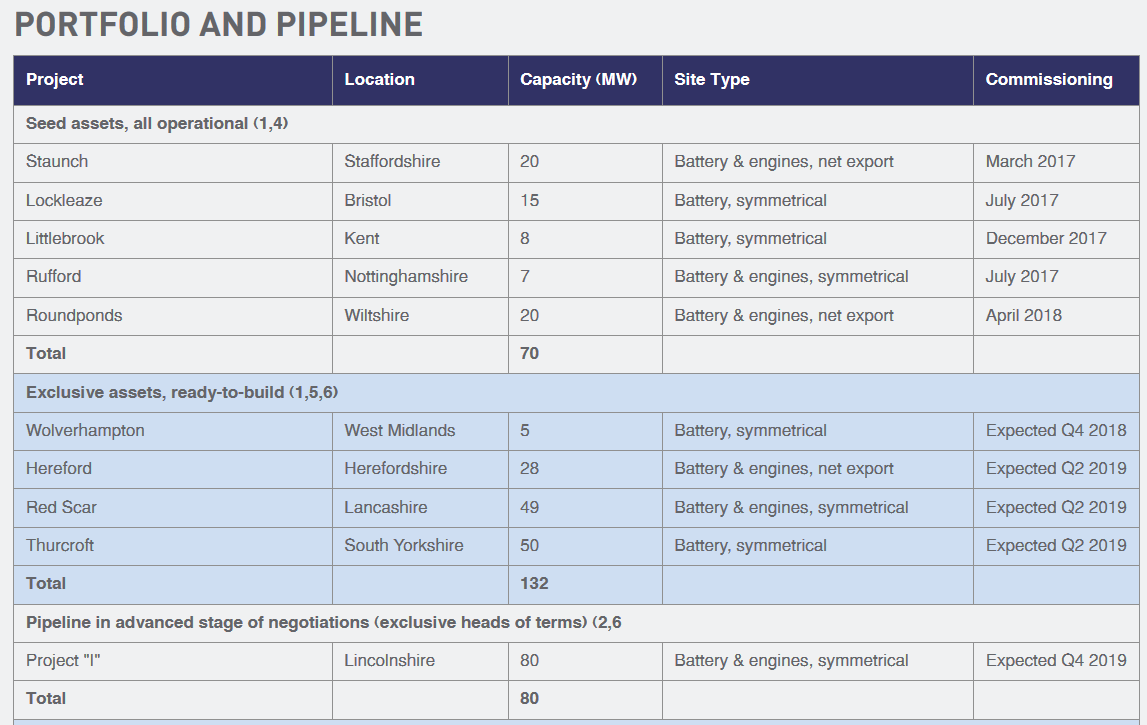

Gresham House Energy Storage Fund is starting with a seed portfolio of 5 projects rated at 70 MW. These will cost £57.2m (a ratio of £0.82m per MW) and have been operational for 6-18 months. They are all on 25-year leases.

It’s buying from its advisor, Gresham House. So, yes, that’s the conflict of interest siren you can hear. The price is said to be at arm’s length but I did search for some comparative costs, albeit briefly.

Gore Street Energy Storage Fund, which operates in the same space, says it has invested £15m for four projects rated at 29MW (of which its ownership share is 27.1MW). That’s £0.56m per MW, so quite a bit cheaper. This fund joined the market in May 2018 but struggled to raise money and ended up with just £30m.

Gore Street has a mixture of ‘in front of the meter’ and ‘behind the meter’ facilities. With the former, you have direct links to National Grid. The latter, usually smaller in size, provide storage for other companies who have their own links (and therefore who presumably take a cut of the profits).

Gresham House’s facilities should all be ‘in front of the meter’. Therefore you would expect them to be more valuable, but I’m not sure to what degree. As these funds invest their cash, we’ll be able to see how these purchase costs vary.

The pipeline cometh

Gresham House Energy Storage Fund has exclusivity agreements over further 4 projects rated at 132MW, due to be completed in 2019, with a further 80MW of projects at the heads of terms stage. There’s another 60MW of potential acquisitions that have been identified by the company but not specified.

Gresham intends to buy these projects once they have been constructed and are ready to operate, although it may provide some finance prior to making an acquisition.

A placing programme will run over the next year to raise more money. This will help buy the exclusive and pipeline assets. It’s not exactly clear what these will cost, but let’s assume the price paid per MW is similar to the seed portfolio. Purchasing the 212MW shown above would, therefore, cost in the region of £175m.

£40m or should be left over from the initial public offering. That suggests a further £135m might be needed from the placing programme and from taking on borrowing.

Breaking down the 15% return

Gresham has said intends to take its gearing level up to 50%. It’s worth considering how this contributes to the headline annual return figure of 15% (which is net of costs). Again the prospectus provides…

The underlying return from the portfolio is essentially the 7% yield plus the 1% fee. Say, 8%.

We can sense check this against the base case revenue assumption of £78,000 per MW from earlier. The seed portfolio of 70MW should generate revenues of £5.5m, which is 9.5% of the purchase cost. So there are presumably other costs in the mix knocking that down to 8%.

Gearing of 50% should add a further 4%, all else being equal.

The remaining 4% or so comes from:

- 1% – a 10% revenue increase from the asset optimisation base case;

- 1.6% – expanding grid capacity;

- 0.8% – extending leases for a further 10 years; and

- 0.2% – reducing operating and maintenance costs.

Interestingly, Gore Street is more conservative when it comes to gearing, setting a maximum of 15%. Gore Street also aims to provide capital growth but I don’t think it has set out a specific figure. But the lower level of gearing it’s targetting suggests its returns might be a little lower.

Key players

Ben Guest, the fund’s manager, seems to have brought to the seed portfolio to Gresham House. He owns 11.5% of the fund’s shares. There’s a decent interview with him here on Proactive Investors that’s worth a watch. The key standout for me was he will concentrate on the UK, as the opportunity is so large.

One of the non-execs is David Stephenson, best known as the Financial Times’s Adventurous Investor. He’s written a column for his site explaining why he’s so keen on this particular fund.

Despite Guest’s hefty stake, it’s a little disappointing to see that the three non-execs only have 5,000 shares each. That means they have committed just £15,000 in total. Between the three of them, they are collecting £150,000 in salaries each year.

What could go wrong?

An awful lot it would seem. The more I read the prospectus, the more nervous I become. That’s what a good prospectus should do, you might say.

Lithium-ion is the company’s favoured technology but others could ultimately prove to be more cost-effective. Sodium- and zinc-based batteries are namechecked. As are flow batteries and compressed air technology. Gresham says it’s prepared to pivot if necessary but it would have a legacy lithium-ion portfolio weighing it down.

Battery costs continue to fall, with a further 50% fall predicted over the next decade. Batteries account for about a quarter of the total project cost, muting the effect of this. Still, future ESS units could undercut those being built right now.

It’s essentially a brand, new market, with the rules being made up as we go. And electricity markets are notorious for their complexity. Should the tide shift, the damage could be done to the share price before we understand the magnitude of any change. This announcement today from the company about the Capacity Market is a good example. The effect on revenues seems to be fairly minor, but it illustrates how the ground can shift rapidly beneath investors’ feet.

The reliance on National Grid as, it would seem, the sole customer is obviously a big risk. I must admit, I’m not entirely sure why National Grid doesn’t put these systems in place itself, but that may be due to my lack of knowledge about the way this market operates.

Political inference is another concern, naturally. The push for more renewables seems likely to continue, especially now it’s becoming cost-effective without any subsidy. But with ESS projects essentially creaming off cash from the grid by exploiting price volatility, they could be an easy target.

Chunky dividends to come?

Let’s ditch the red flags for now and go back to the numbers…

Gresham’s plan is to pay a dividend of 4.5p in respect of 2019 and 7p for following financial years. Hopefully that 7p will grow over time as well. The first dividend is due to be declared in April 2019 and subsequent payments will be made quarterly. That implies an initial yield of 4.5% based on the issue price, rising to 7%.

Again, Gore Street provides a useful comparator. It is promising to pay a 4% dividend in its first year and 7% thereafter. Very much in the same ball park then.

Run of the mill charges

Fairly standard stuff here for one of these so-called alternative finance funds.

The management charge is 1.0% up to £250m of net assets, falling to 0.8% for net assets above £500m. Total annual ongoing costs, per the Key Information Document, are said to be 1.34%

The price action so far

Gresham has moved to a premium of 5-6% pretty much straight out of the gate. It’s trading at 103p versus an estimated net asset value of 97-98p.

The quoted spread is 102-104p, but trades seem to be going through fairly close to 103p.

Closing thoughts

I’m looking for a little alternative action in my portfolio right now. Both to add a little income and to reduce volatility. I’ve already taken a nibble at Bluefield Solar Income Fund, for example. And I did take a look at Gore Street when it joined the market, too, admittedly not in much detail.

One niggling concern I have is that I’m not that familiar with Gresham House. The name goes back a long way, but the current management team haven’t been in place that long. It seems to be expanding quite aggressively and recently announced it was taking on the management of the Baronsmead venture capital trusts (of which I own one) from Livingbridge.

All that said, I could see myself taking a small position in this fund at some stage, ideally at a smaller premium that it boasts at the moment. For now, I think I’ll just keep watching and see how it gets on raising the additional cash to fund its pipeline purchases.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.