I’ve been meaning to take a closer look at European Opportunities Trust for a while. It’s been a great performer for nearly 20 years, but its largest holding, Wirecard, hit the headlines last week for all the wrong reasons.

European Opportunities has now sold its entire stake in Wirecard. But the trust took a heavy hit, both in terms of money and reputation.

Key Stats For European Opportunities Trust

Figures are as of 19 June 2020 unless otherwise stated:

- Founded: November 2000

- Manager: Alexander Darwall (aged 57, manager since launch)

- Management firm: Devon Equity Management

- Ticker: JEO

- Benchmark: MSCI Europe

- 10-year net asset value return: 248%

- Share price: 718p

- Indicated spread: 716p – 720p (0.6%)

- Market cap: £775 million

- Discount to net assets: 8%

- Costs: OCF 0.9%, KID 1.0%

- Net cash: 1% as of 31 May 2020

- Historical dividend and yield: 5.5p and 0.8%, paid annually

- Results released: Feb (interims) and Sep (finals)

- Sector: Europe (1st out of 8 over the last 10 years)

- Links: Website and AIC page

Crosswires

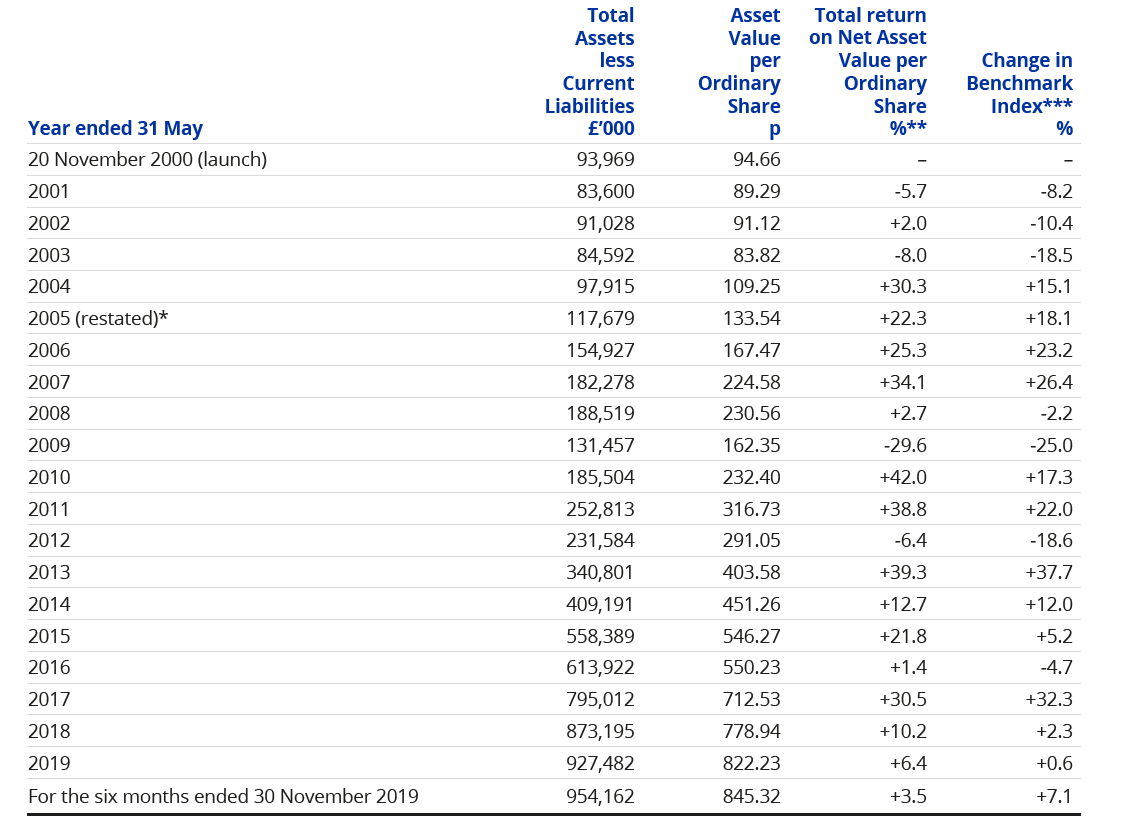

European Opportunities, known as Jupiter European Opportunities until last year, was launched in November 2000 and it’s been the best performing European investment trust since then. It’s been run by Alexander Darwall from inception.

Last year, Darwall and his associates set up a new investment company, Devon Equity Management. The board of European Opportunities decided to follow him and they transferred the management of the trust away from Jupiter.

For some reason, the trust’s ticker has remained as JEO, despite the move from Jupiter and EOT seemingly being available.

Wirecard is a German payment technology firm and it’s long been Darwall’s biggest position. It has been a listed company for nearly 20 years but has rarely been far from controversy and it was often targeted by shorters.

The Alphaville column on the Financial Times website has been writing about Wirecard for five years with a series unsubtly tagged as The House Of Wirecard.

After one particularly damaging story in early 2019, Wirecard even went as far as taking out a lawsuit against the FT.

Wirecard’s shares plunged in April of this year on auditing concerns and then they collapsed again last week after 1.9 billion euros of cash appears to have gone missing. The CEO of Wirecard has since resigned.

Riding it up

European Opportunities bought its first tranche of Wirecard shares in December 2007, paying 9 euros.

By May 2009, it had a 1.0% position, valued at £1.8m.

It’s been one of the trust’s largest holdings since 2013 and for a brief time accounted for 17% of its entire portfolio.

The share price of Wirecard peaked at just over 190 euros in the summer of 2018, so at one stage it was probably a 20-bagger for Darwall.

Riding it down

At the start of this year, with Wirecard’s share price back down to around 100 euros, Darwall apologised for letting his position get so oversized.

As of 31 May 2020, Wirecard was still the trust’s largest holding at and represented just over 10% of its net assets. It was probably worth £105m just prior to the news of the missing cash.

Darwall sold his entire holding on 18 June. In a statement, Devon Equity Management said:

At the time of publication of KPMG’s report on the company’s internal investigation in March 2020 we engaged directly and extensively with senior management and the board. We were satisfied that its management would address the alleged issues identified in full. In retrospect this conclusion was a mistake, for which we apologise. When we ceased to believe in the investment case for the company on 18 June, we sold the position in its entirety.

Clearly the collapse in this holding is deeply disappointing. We will continue to follow developments, but our focus looking forward is to ensure that our investment portfolios deliver relative to their investment objectives and to learn from our mistakes. We are excited by and absolutely committed to the success of the strategy.

I guess that when, at one point anyway, you’ve made 20 times your money on a stock, it’s a lot harder to be impartial.

A small profit overall

The trust’s net asset value dropped 7.5% on 18 June, so I reckon the average sell price was around 30 euros.

Devon said its blended purchase price was 27 euros, with its most recent purchase in February 2019. But the trust would have made a handsome profit when it trimmed its position in 2017 and 2018.

Wirecard’s share price has fallen by another 50% since Darwall sold. It closed on Monday at 14.5 euros.

As you might expect, European Opportunities’ share price reacted sharply, too. It was 777p on Wednesday evening and finished the week on 718p.

But its shares fell as low as 656p on Friday morning and one of the trust’s directors, Sharon Brown, managed to buy £10,000 of shares at 676p.

Performance

It’s easy to forget that Darwall still has a great track record, even after the recent goings-on at Wirecard:

| Trust | Performance Nov 2000 to Jun 2020 |

|---|---|

| European Opportunities | 646% |

| Fidelity European Values | 571% |

| Henderson EuroTrust | 361% |

| Henderson European Focus | 278% |

| Baillie Gifford European Growth | 138% |

The MSCI Europe index is up around 160% over the same timeframe. That means Darwall has returned 10.8% a year versus 5.0% for European markets.

That’s a chunky level of outperformance.

What’s more, it’s been achieved without investing in the soaring US market of recent years.

10.8% a year from 2000 to 2020 means European Opportunities has beaten most global trusts over the timeframe, except Scottish Mortgage and Mid Wynd.

It’s been pretty consistent, too. European Opportunities has only underperformed its benchmark in three years since it launched (the years to May 2009, May 2017 and May 2020).

The figures for the full year to May 2020 aren’t in the above table but European Opportunities lost 7.0% while its benchmark fell 2.5%.

In all three years, therefore, the underperformance has been less than five percentage points. In other words, even when it’s lost some ground against the index, it hasn’t been that far behind.

The year ending May 2021 hasn’t got off to the best start, of course, so that could turn out to be number four.

Investment process

A recent note from Kepler contains this useful illustration:

[Darwall] is a bottom-up investor; using rigorous fundamental analysis to identify companies that can retain their high growth characteristics and profitability for much longer than many other investors expect. Alexander prefers companies that have less capital intensity, use digital channels and have a large amount of intellectual property.

His focus does not, however, include start-ups or ‘preprofitability’ companies. Over any 12 month period, Alexander will buy between 10-15 new companies on average, which will represent around 0.5% of the portfolio each.

Once a company has been identified as a suitable investment, Alexander and Luca Emo research the company’s management teams to better understand them. He will then further add to the position as his confidence in the investment thesis increases. Until he believes that the growth ‘runway’ has shortened or expired, Alexander will continue to hold the position.

A key part of this process involves meeting the management teams – in the last year alone Alexander and Luca met around 190 companies.

A podcast at Fund Calibre adds a bit more colour about the decision to set up Devon Equity Management:

Richard Pavry [Devon’s CEO], Luca Emo [deputy fund manager] and myself have worked together for many, many years at Jupiter. And …. we made the decision to have a more focused, sharpened investment experience. It’s certainly going to prolong my enthusiasm and shelf life, which is what I really wanted to do.

We try to find special companies. And companies that are special are really companies that we think can flourish in different economic scenarios. Because we don’t do a lot of economic forecasting. I don’t know what the next surprise around the corner, it might be a good surprise might be a bad surprise.

And in fact, the COVID-19 episode has played to that because we never forecast this, of course no one did, but our companies, which do something special and different with strong balance sheets with lots of intellectual property and a bit less capital intensity – all those things are actually helping us at the moment. So, whilst we never forecast COVID-19, the fact that we like special companies is our best way and has, is proving to be a relatively good way of coping with this crisis.

So we’re looking at ‘Quality Growth’ here, for want of a better description. It’s pretty similar to the likes of Fundsmith and Lindsell Train, with the same focus on having a concentrated portfolio.

Portfolio

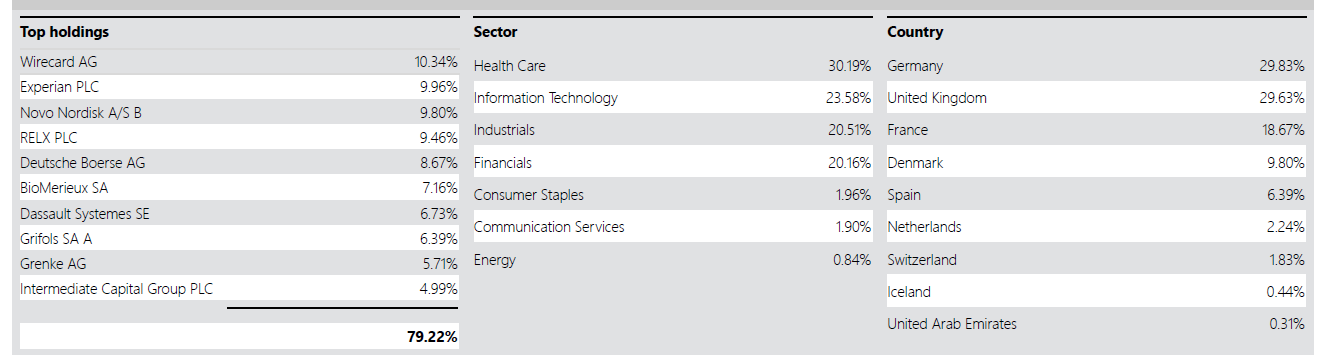

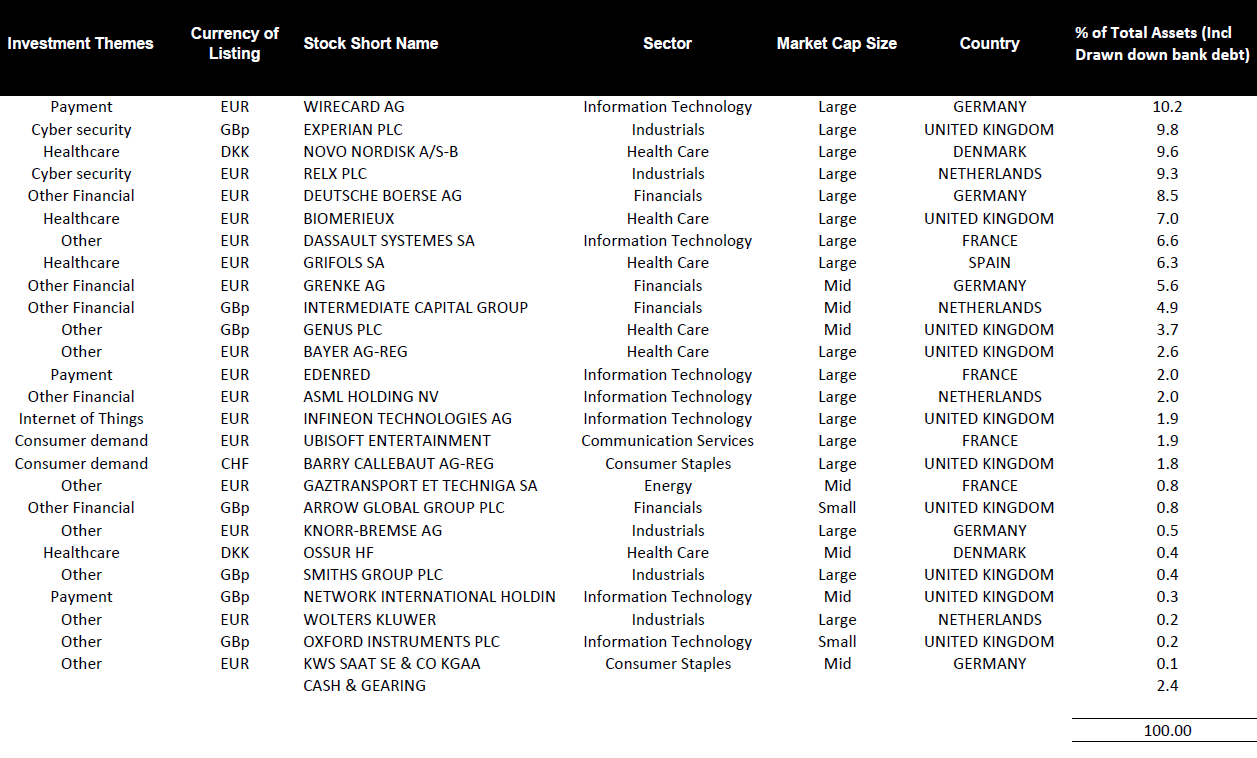

European Opportunities had 27 positions, before selling Wirecard, but its top ten accounted for around 80% of its net assets.

Here’s the summary as of 31 May 2020 with a sector and country breakdown:

And here’s the full listing:

It’s predominantly a large-cap portfolio, with just 16% in mid-caps and 1% in small-caps.

Portfolio turnover seems to have been fairly low in recent years. The 2019 accounts suggested around 15% by value of the portfolio was bought and sold in both 2019 and 2018.

The interim accounts to 30 November 2019 showed 31 holdings, of which 6 were new compared to a year previously. However, the position sizes for these were all quite small, ranging from 0.2% to 0.6%.

But some sizeable positions of 5% or so have been sold in recent months, namely Carnival, Adidas, and Amadeus IT.

Now that Wirecard has left the building, I can’t see any stocks on this list that I would have considered to be particularly controversial, although I’m not that familiar with some of the non-UK holdings.

Among the largest remaining positions, RELX is a Nick Train favourite and Novo Nordisk is often mentioned by Terry Smith.

Gearing

European Opportunities seems to run with a fairly low level of gearing. It currently has a flexible bank facility of £100m and net assets of around £900m.

£85m of this facility was drawn down as of November 2019 but the trust had a small net cash position as of May 2020, presumably due to recent investment sales. And the sale of Wirecard may have increased the net cash position a little further.

Discounts and premiums

European Opportunities has mostly traded at a discount over the past 10 years, so the current 8% discount isn’t entirely unprecedented.

However, the trust has enjoyed a premium at times, most notably from 2013 to 2015 and at times during 2018.

Charges

The fee structure has changed a bit following the move to Devon Equity Management.

With Jupiter, the management fee had been 0.75% of total assets plus a 15% performance fee.

It’s now 0.9% of net (rather than total) assets up to £1bn and 0.8% over that amount. The performance fee element has been removed.

There was a transition period up until 31 May 2020 where Jupiter continued to get its fee and Devon got 0.1%.

In absolute terms, the management fee was £7m the past two years (to May 2018 and 2019) but amounts of £7m and £13m were paid in respect of the performance fee. Other expenses came to about £0.75m.

0.9% on assets of £1bn, give or take, certainly isn’t cheap for a mainstream equity trust. So it needs to be backed up by continued outperformance.

Skin in the game

European Opportunities currently has six directors, three of whom have been on the board for quite some time: Andrew Sutch (Chairman, on the board since 2011), Philip Best (Chair of Audit Committee, since 2009), and John Wallinger (since 2000). Perhaps they gave Darwall too long a leash over Wirecard?

The board also includes the former Chancellor of the Exchequer, Lord Lamont, who has served since 2015.

The directors collectively own around 340,000 shares (worth some £2.4m), with Wallinger having by far the largest stake (256,000).

Darwall owns 3.64 million shares in European Opportunities, currently worth around £26m, so his interests should certainly be aligned with the trust’s shareholders. He appears to have owned a similar number of shares since at least 2008.

At 57, he should also have many more years at the helm and seems genuinely enthused about setting up a new investment business. Luca Emo, his deputy, is 39.

There is a non-compete clause with Jupiter, so European Opportunities should be the focus of attention for a little while. An open-ended fund has been set up, but it has assets of less than £100m, and Devon also appears to run some money for institutional investors.

According to filings at Companies House, Darwall seems to own 80% of Devon, with Luca Emo and Richard Pavry owning 10% each.

Summing up

Here is a marmite trust if ever there was one.

A lot of investors seem to write off managers who have had a one-off disaster like this or who own one business they don’t like (Tesla and Scottish Mortgage being the classic example).

They worry, with good reason some might say, that it shows that the underlying investment process is flawed.

I tend to be more naive forgiving, on the basis that all great managers have howlers now and again. No investor gets everything right all the time — or even close to it.

However, I am wary of companies that are regularly targeted by shorters, especially when it’s regarding aggressive accounting and poor cash flow rather than just excessive valuation. Far more often than not, as far as I can see, the shorters are proved correct.

Here in the UK, Globo, Quindell, and Burford spring to mind.

All that said, Darwall still has a great track record, particularly when you consider the lack of US stocks in the portfolio.

What’s more, decisive action was taken to cut the holding in one fell swoop once the situation became untenable and the appropriate apologies were issued. That’s in stark contrast to the likes of Neil Woodford who tried the keep his cracked plates spinning.

I plan to keep an eye on this one. But as its focus is Europe rather than Global, it’s less likely to find its way into my portfolio.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

I see in the news today that the former CEO has been arrested for fraud.

Thanks for another stimulating blog. I am a newish reader and enjoy your insights.

You list Globo, Quindell, and Burford as examples of short-sellers accurately identifying weak companies. Although Burford Capital’s share price fell hugely after the short attack in August 2019, the company hasn’t imploded in the way Muddy Waters prophesied and the shorter’s allegations seem to have been successfully dismissed by Burford’s management. Do you still think there is a serious cause for concern?

Thanks IT Enthusiast.

I’ve never looked at Burford in any great detail so I can’t offer any particular insight on where it stands now.

While it hasn’t imploded in the same way as the other two, I mentioned it as an example as it’s more recent and its share price still seems to be a long way below the level it was before Muddy Waters came along.

Thank you. I bought shares in Burford Capital about five years ago when they were less than 300p. The company was doing something innovative with a huge addressable market, and was well-run. It’s been an exciting ride, the shares touched £20 (at which point my wife urged me to take profits) before falling back last year, but are still about twice what I paid for them.

I have been consistently impressed by the lucidity and intelligence of the company’s annual reports. Some investment trusts (TR Property, Allianz Technology, Finsbury Income and Growth) produce insightful and educational comments on the portfolio and the market, some write discursive essays suitable for The Economist (Scottish Mortgage) and most produce defensive corporate blah (every Asia Pacific trust I have tried, and I have tried a lot, each of which has duly regressed to the mean). I instinctively prefer the first group, I feel I know what Marcus Phayre-Mudge and Nick Train are thinking and have greater confidence in their judgements. Or am I old-fashioned in even bothering to read these reports?

It doesn’t sound old-fashioned to me, but then I’m happy to wade through annual reports for interesting nuggets of information.

However, it’s always worth bearing in mind that large chunks of annual reports are effectively marketing and tell shareholders what they want to hear (maybe less so with investment trust than ordinary businesses). So we always need to be wary of getting too cosy with management – something I am occasionally guilty of!

Wirecard has filed for insolvency today and the share price has crashed again to 3 euros. So it’s down some 90% from my rough estimate of the price European Opportunities got when it ditched its position last week.

Muddy Waters were spot on in regard to Burford although parts of the market may disagree. Fundamental Governance issues were there in the relationships between Executives and the valuation of WIP in the accounts raises question marks. I sold all of my Burford shares when I read the Muddy Waters report and did the same recently with Tesla when Elon Musk ranted about the bona fides of the Covid-19 lockdown in Freemont, California calling out the County Officials as Fascists. I do wish that SMT, which I hold, would reduce it’s exposure substantially to Tesla. Market Fund managers seem to have a forgiveness issue with poor Governance who only really understand the importance of the matter when owners sell their stocks.

Some decent points made on JEO in the latest Funds Fanatic podcast: https://citywire.co.uk/investment-trust-insider/news/wirecard-scandal-my-faith-in-darwall-has-been-shattered/a1373339

Both Gavin Lumsden and Dan Grote were shareholders it appears. They also pointed out that Darwall owns over 3% of the trust’s shares, which I missed completely as it didn’t seem to be mentioned in last year’s annual report for some reason. Have amended the article therefore.

Thanks for another comprehensive write-up. I’ve followed Darwall for a while, and he’s undeniably impressive. As you say, the style is very much Fundsmith-esque, reflected by key holdings like Novo Nordisk & Amadeus.

Wirecard has clearly been a problem for a while – I think you offer one of the best explanations – it would be hard not to have a big anchor bias towards any investment that has rewarded you so handsomely.

I have been uncomfortable with one or two other holdings over the years (though I may be being wishy-washy) such as Provident Financial – apart from the fact that the stock crashed (again after superlative performance for a long time), I don’t feel entirely uncomfortable investing in ‘money-lenders’ or some might say loan sharks, though I know there is an argument they provide a necessary service. And I also wasn’t a massive fan of ‘Genetically-Modified’ Syngenta – again a very subjective PoV.

While it’s disappointing that they didn’t spot the Wirecard problem, when others had, I do admire the way they unemotionally sold it straightaway. It’s interesting to see how people react when they do make a mistake.

I read a very interesting paper recently putting a good argument for Europe’s continuing decline versus the US and China, so my European weighting is drifting down. I am happy to get most exposure from Fundsmith and Lindsell Train.

But if I was going to invest in Europe, Darwall would be up there, though I’d also put the Comgest Euro Smlr Cos fund into consideration, which is very much a European version of Smithson.

My only final wondering is how hungry Darwall is (perhaps more so since he left Jupiter, not that it helped Woodford…). He is extremely wealthy, with some impressive country property (side research R US…) and there is always the chance that after many years of intense work and success, he’s enjoying the fruit of his labours, and is not focused on work as much. Against this is his multi-million pound shareholding in the trust, though it’s probably chump change against what he’s earned over the years.

I think this is something one always has to bear in mind with successful fund managers. It’s not always easy to identify – one has to try and make a judge of character with whatever you have.

Thanks for those insights Tom. Always great to hear from someone who has been following these folks for a long time. For many years, I largely limited my research to the trusts I held, so part of the reason for this blog is to catch up with other parts of the IT world that have passed me by.

Interesting about the large abode he has and I suspect there is some truth in that these older managers (Smith, Lindsell, and Train) are all now gradually winding down their day-to-day involvement. Perhaps the experience they now have is a substitute for the extra hours they used to put in, but it’s tough to know from the outside.

I’m sure a large chunk of the performance fees that JEO earned for Jupiter will have been paid to Darwell, but I would have thought his JEO stake is still his major asset.

Darwall did remark in that podcast that he felt reinvigorated by launching Devon. And I suspect the Wirecard fiasco may even prove beneficial in the long term, as I doubt he’d want this episode to dominate his legacy.

Will be an interesting story to watch!

Another Excellent article. I held this trust for over 15 years in a way – initially held the Jupiter Unit trust then transferred the value into the investment trust around 10 years ago. It has performed excellently and I am willing to bear with it even though recent performance is poor. So tempted with the Montanaro Euro Smr Cos but I still resisting changing. I agree every investor will make a mistake and Mr Darwell has performed so well over so many years it can not just be luck. The 20 year figures you provide, which take into account the Wirecard fiasco, are still so impressive.

Have only become aware of your website 2 months ago, and I congratulate you on the level of detail and research you go into, as well as the excellent writing style which makes it so easy to read. Keep up the good work and thank you!

Thank you for the kind words, HM 🙂

JEO seems to have lagged the sector a little since the end of July as well, but I don’t think you can draw any conclusions from such a short timescale. Hope it comes good for you.

Warren Buffett lost a substantial amount in Tesco a couple of years ago – So even the greatest screw up sometimes