Caledonia Investments is one of several ‘family-run’ investment trusts that have very respectable long-term records but have struggled to keep up with global market indices in recent years.

Its nearest equivalents are probably RIT Capital Partners and Hansa, rather than investment trusts like Witan and Brunner where the family concerned have now taken more of a back seat.

Building up, trimming back

I first bought Caledonia in 2011 and then did a fairly major top-up in 2012 when its shares fell out of favour for a little while. I added to my position in 2015, 2016, and 2017.

After that, I changed the way I looked at my portfolio, thinking of how it all fitted together rather just being a collection of rash opportunistic purchases.

I decided my position size in Caledonia was a little too big, so I dialled it back a bit in early 2019.

Part of my holding sits outside of my ISA and I’ve had that earmarked as a disposal candidate for a while.

Key stats for Caledonia Investments

- Listed: 1960

- Ticker: CLDN

- Management firm: Self-managed

- Notable shareholders: Cayzer family owns 48.5%.

- CEO: Will Wyatt (age 52)

- 10-year net asset return: +101% (7.2% pa)

- Share price: 3,020p

- Indicated spread: 3,015p-3,025p (0.3%)

- Market cap: £1.7bn

- Net asset value (NAV): 3,508p as of 31 Oct 2020

- Discount: 22% as of 31 Oct 2020

- Costs: 0.9% OCF and 2.4% KID

- Number of holdings: Undisclosed, top 10 consists of 43% of net assets

- Net cash: 2%

- Results released: May (finals) and Nov (interims)

- Current dividend and yield: 61.5p and 2.0%

- Dividends paid: Jan (interim) and Aug (final)

- Sector: Flexible: 4th out of 17 over 10 years

- Links: Website – AIC page – Kepler 2018 report

Price details as of 2 December 2020

From shipping to investing

The history of Caledonia Investments is a little convoluted. It can be traced back to 1877 when the Cayzer family set up a shipping business called Clan Line. According to Wikipedia, Clan was “the largest cargo carrying concern in the world” in the 1930s.

In 1951, Caledonia Investments became the holding company for the Cayzer’s Clan Line stake plus their assorted other interests. It was floated on the stock exchange in 1960.

The Clan Line merged with another shipping firm called Union-Castle in 1956 and the combined entity was called British & Commonwealth (B&C).

As passenger shipping declined and cargo ships were replaced by containers, B&C spread out into other areas of the transport industry and then into financial services.

B&C still accounted for around 90% of Caledonia’s assets in 1987 when the trust’s directors decided a much wider level of diversification was required.

A deal was struck to sell the vast majority of Caledonia’s B&C holding for £100m in cash followed by £328m in instalments over the next few years.

It was fortunate timing as the deal was completed not long before the market crash on Black Monday and then B&C went bust a few years later following its disastrous acquisition of Atlantic Computers.

Starting afresh

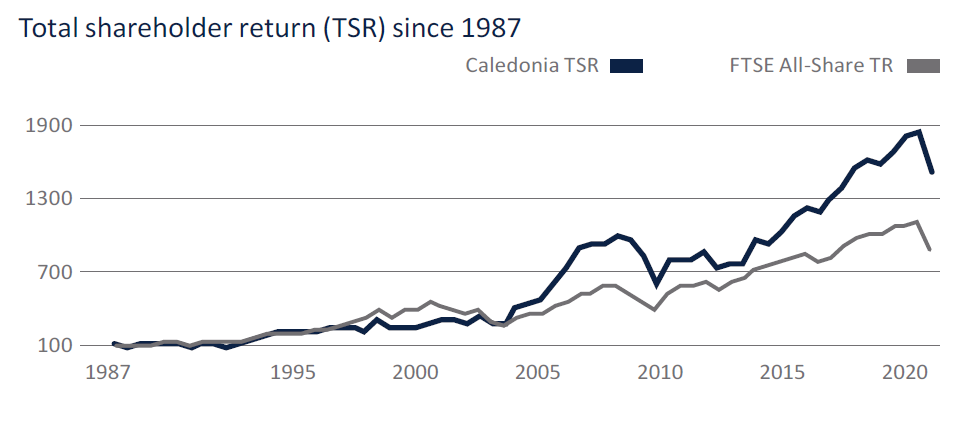

1987, therefore, effectively marks the beginning of Caledonia Investments as it exists today.

However, from 1987 to 2002, Caledonia’s performance against the FTSE All-Share was somewhat underwhelming.

Some of the Cayzers grew restless about this and Tim Ingram was appointed as the first non-family CEO.

The family squabbles continued, though, and the disgruntled relatives were eventually bought out at a cost of £88m in 2004.

Ingram did very well as CEO before eventually retiring from Caledonia in 2010. He’s since been the chairman of Greencoat UK Wind and a director of Alliance Trust.

Over the eight years to March 2010, not quite an exact match for Ingram’s tenure, Caledonia’s share price return was 132% while the FTSE All-Share managed just 51%.

Wyatt takes over

Will Wyatt, a sixth-generation descendant of the shipping empire’s founder, Charles Cayzer, replaced Ingram as CEO in 2010 and he remains in charge today. He started his career in corporate finance before joining Caledonia in 1999. He was a director for five years before taking the top job.

Wyatt’s record hasn’t been quite as good as Ingram’s but the trust has still been able to beat the UK market by a handsome margin. Caledonia returned 91% over the 10 years to March 2020 versus 54% from the FTSE All-Share.

Wyatt is still only 52 so you would suspect he’ll be CEO for some time to come. I’m not sure if there are plans to keep the job within the family when he does retire but it seems likely. There are two other Cayzers on the trust’s board but they are both a little older than Wyatt.

The Cayzer family currently owns 48.5% of Caledonia Investments. The majority of their stake (35% of Caledonia’s shares) is held by The Cayzer Trust Company which lists 88 separate shareholders.

Here’s the chart of Caledonia’s returns from 1987 to March 2020. On an annualised basis, it’s 8.6% a year for Caledonia versus 6.9% for the FTSE All-Share.

Caledonia has widened its lead since the end of March 2020 as it’s up 31% since then versus 18% for the FTSE All-Share.

Caledonia’s strategy

From the trust’s 2020 annual report:

Our aim is to grow net assets and dividends paid to shareholders over the long term, whilst managing risk to avoid permanent loss of capital.

We achieve this by investing in proven well-managed businesses that combine long-term growth characteristics with an ability to deliver increasing levels of income.

We hold investments in both listed and private markets, a range of sectors and, particularly through our fund investments, we have a global reach.

Caledonia lists four specific objectives:

- outperform the RPI measure of UK inflation by at least 3% over the medium- and longer-term;

- outperform the FTSE All-Share index over ten years;

- pay annual dividends increasing by RPI or more over the longer-term; and

- manage investment risk effectively for long-term wealth creation.

The first three of these have been achieved recently.

The fourth objective is rather more subjective but the steady progress of Caledonia’s NAV over time suggests to me it’s being met as well.

Over the ten years to September 2020, the trust’s NAV increased by 7.6% a year, the All-Share by 5.1%, and RPI by 2.7%. So Caledonia is ahead of both the All-Share and RPI+3%.

Caledonia’s dividend has increased from 35.3p to 61.1p over the last 10 years, representing annual growth of 5.6%. There was also a £1 special dividend in 2017.

Recent annual dividend growth has been a bit lower, typically in the region of 3-4%, and last week’s results saw a 2.4% increase in the interim dividend from 16.6p to 17.0p.

Caledonia is classed as one of the AIC’s Dividend Heroes having increased its payout every year since 1967. And with a relatively low yield and ample revenue reserves, it looks well placed to deliver annual dividend increases for a long time to come.

What’s the right benchmark?

You could argue that Caledonia’s targets are too modest. However, Wyatt says the trust has “an absolute return mindset” and it’s important to remember that the trust’s main purpose is preserving the Cayzer family’s wealth rather than out-and-out growth.

Such is the size of the family’s stake, us mere mortal shareholders are essentially just along for the ride.

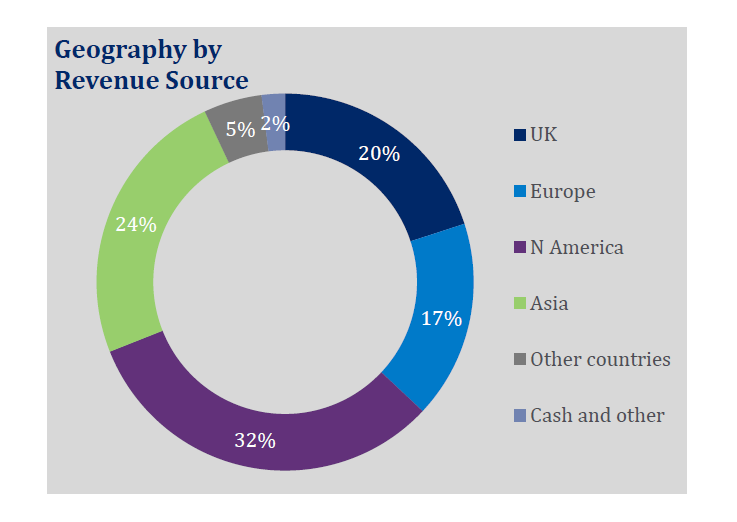

That said, given Caledonia has a global investment outlook, benchmarking itself against the UK market rather than a global index seems harder to justify with each passing year.

By country of registration, its UK/Channel Islands portfolio weighting is 43%. But this falls to 20% when you consider the source of underlying revenues.

For most of my investing life, the returns from US and UK markets have been very similar. There were differences in individual years, of course, but as this chart from Vanguard shows the overall returns from both markets were pretty similar for the period from 1990 to 2012.

Since the start of 2013, the US market has sped ahead and, given its size relative to everything else, this has driven the returns for global markets higher, too.

From January 2013 to October 2020, the UK market gained about 25% but global markets increased by 160%.

This is a quibble I have had with quite a few trusts, so apologies if you’ve heard this particular rant before!

Sector change

A change of AIC sector a couple of years ago from Global to Flexible also muddies the waters when you’re trying to assess Caledonia’s performance.

The Flexible sector is a very mixed bag with many trusts investing a large chunk of their portfolios in fixed-income and other types of assets.

As far I am aware, Caledonia has always been 100% equities, albeit mostly of the unquoted variety. Therefore, it sits near the top of the pile in the Flexible sector, which is a little flattering if you take it at face value.

For me, although you can make a case either way, Caledonia has more in common with the Global sector than our Flexible friends.

Three areas of focus

Caledonia has changed under Wyatt’s leadership, but it appears to have been evolution rather than revolution.

In 2011, he revamped Caledonia’s strategy into six distinct pools and introduced target weightings and returns for each of them. The six pools have been refined over the years and now just three remain:

- quoted equities;

- unquoted companies (called Private Capital); and

- private equity funds (split roughly evenly between the US and Asia).

The portfolio that Wyatt inherited in 2010 consisted of 63% in quoted equities, 25% in private companies and 12% in private equity and hedge funds.

Back then, the stakes Caledonia held in quoted companies tended to be quite large, such as its 13% stake in merchant bank Close Brothers and 17% in British Empire Securities (now AVI Global).

Today, the quoted companies it owns tend to be much larger (Microsoft, BATS, Unilever etc) so the proportion held by Caledonia is tiny and therefore much more liquid.

Meanwhile, the opposite seems to be happening with unquoted businesses. Caledonia still invests in around 8-10 businesses at any one time, but it seems to be taking bigger stakes and investing up to £100m. Its largest positions now tend to be its unquoted ones.

Here’s the current split between the three categories, along with their target and actual returns:

| Category | Target weighting 2015 | Target weighting 2020 | Sep-20 weighting | Target return | 5-year target return | Actual 5-year return |

|---|---|---|---|---|---|---|

| Quoted | 50-70% | 35-50% | 36% | 9.0% pa | 54% | 74% |

| Private Capital | 20-35% | 35-45% | 33% | 14.0% pa | 93% | 27% |

| Private equity funds | 15-20% | 20-25% | 29% | 12.5% pa | 80% | 87% |

The quoted portfolio consists of growth (10% pa target) and income (7% pa target), giving a blended average of 9%.

The target weighting for Private Capital was increased in 2016. As this pool consists of relatively few positions, the timing of sales and purchases means the actual weighting hops around a lot from year to year.

Looking at this table, it would seem that it isn’t so much a lack of US exposure holding back recent returns, but the performance of the Private Capital division.

World markets have returned around 80% in the past five years so the returns from Caledonia’s quoted portfolio and its array of private equity funds have been roughly comparable.

Portfolio

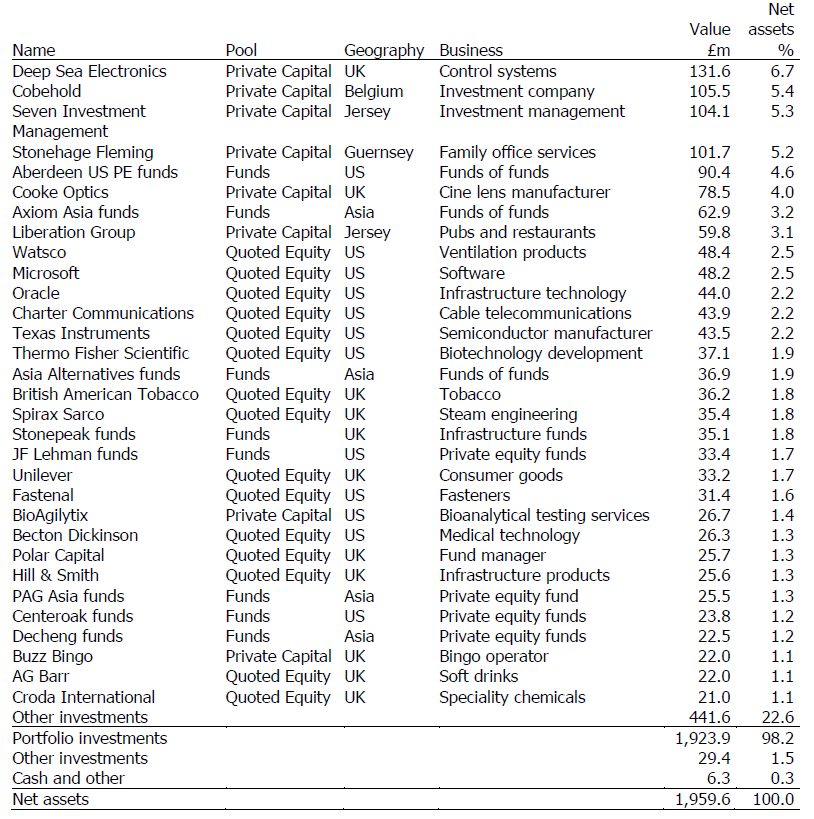

Here are Caledonia’s main investments as of 30 September 2020:

Overall, portfolio turnover tends to be fairly low. It was around 25% in both the years ending March 2020 and March 2019.

Private Capital

Private Capital is run by Duncan Johnson who joined Caledonia in 2011. He’s the head of a team of seven who all have board-level positions in the various companies Caledonia has invested in.

Nearly all this category is accounted for the eight companies listed in the table above.

With one exception, their businesses are UK-based and are relatively recent investments made between 2015 and 2019. Cobehold is the outlier, being focused on Europe and held since 2004.

Caledonia owns between 89% and 99% of Deep Sea, Cooke, 7IM, Buzz Bingo, and Liberation, alongside smaller stakes in Stonehage Fleming (37%), Cobehold (5%), and BioAgilytix (9%).

The Caledonia Private Capital website also lists an investment in US-based Bloom Engineering made in 1989, a 22.5% stake in Sports Information Services bought in 2005, and a 2010 investment in a commercial property firm called Brookfield Partners. These are in the books at a collective value of £27m, down from £34m a year ago.

Caledonia says it looks to invest between £25m and £125m in a company, with a typical holding period of 7-10 years, providing both stability and capital to let it execute its growth plans. It doesn’t tend to use as much debt as other private equity firms, preferring to extract income via dividends.

With the Cayzer connections, the trust has been able to build up a wide network of contacts over the years which it uses to source new deals.

Robust market position, consistent financial performance and profit delivery, steady demand-led growth drivers, and an established management team are key requisites for new investments. Underlying profits in excess of £7m, margins over 10%, and high cash conversion are also sought.

Of all the companies in this category, Buzz Bingo (formerly Gala Bingo) has been hit hardest by the pandemic. It shut a quarter of its clubs in the summer and underwent a company voluntary arrangement (CVA) in August to restructure its business.

Caledonia appears to have invested around £150m in Buzz since 2015, including £22m in the recent restructuring. Earlier in the year, there seemed to be some optimism about its relaunched online offering, but no further details were added in the results last week.

Liberation, which operates pubs and restaurants, has seen about £100m invested since 2016, plus a further £37m last month to fund an acquisition. So, Caledonia is sitting on a large loss here as well. Two-thirds of its business is in the Channel Islands, though, where COVID restrictions have been less extreme.

Cooke Optics specialises in cinematography lenses. Therefore, demand for its wares dipped due to films and TV shows being put on hold. Its factory is based in Leicester, causing further issues due to the prolonged nature of restrictions in this part of the country.

Both Buzz and Liberation were valued at a small loss last September before the pandemic hit, which was a few years after Caledonia’s initial investment. And 7IM, first bought in 2015, doesn’t seem to have shown that much capital growth yet either.

Caledonia’s other major unquoted investments are more recent so it’s harder to judge their success. Except for Cooke, they seem to have been more resilient during the turmoil of 2020.

On a valuation basis, Caledonia seems to err on the cautious side. It was good to see prompt action in the March 2020 NAV update relating to the carrying value of Buzz, Liberation and other COVID-affected businesses, not waiting for the full-year accounts to be published in May.

For me, though, the jury is still very much out on this part of the portfolio. Caledonia has had success with large stakes in UK consumer-facing businesses in the past, such as tripling its money between 2013 and 2016 on Park Holidays, so you can understand why it has continued to invest in this space.

But since the Park bonanza, the collective returns have been disappointing and, admittedly with a massive dollop of hindsight, it makes the decision to increase the target weighting to this category back in 2016 look somewhat questionable.

True, a lot of the damage has been COVID-related but I’d like to see the current set of Private Capital businesses prove their worth before any significant additional money is put to work in this category.

Quoted

This category is run by a team of four and led by Mathew Masters who has been with Caledonia since 2006.

The performance of this part of the portfolio has been decent rather than spectacular. There are many familiar names that you see in other quality-focused portfolios, such as Microsoft, Thermo Fisher, Spirax-Sarco, and Unilever.

The geographic split is roughly 50% US, 45% UK, and 5% Europe.

Caledonia likes to own “high-quality companies that compound their earnings over the long term”. Changes tend to be fairly infrequent. In the last six months, there was only one outright purchase, namely Fortis (US utilities), and one outright disposal of Tritax Big Box.

Somewhat confusingly, a few companies seem to be held in both the growth and income sub-categories of the Quoted portfolio. I’m not sure I really see the need for two separate sub-categories and the income requirement results in an undesirably large UK weighting.

Private equity funds

The fund category is run by a team of three and headed by Jamie Cayzer-Colvin, who worked a subsidiary of Caledonia from 1995 and then joined the head office team in 1999. He’s been a director of Caledonia since 2005.

There is less detail disclosed about this category but we do know that 45% is invested in Asia, 52% in the US, and 3% in the UK. They are 49 funds in total, which gives Caledonia exposure to over 1,000 separate businesses.

This is the newest area of the portfolio, as relatively little was invested this way prior to 2011. Caledonia saws it took a cautious approach, initially investing in funds of funds to get a feel for what was on offer in the US and Asia.

As of March 2020, there were substantial undrawn commitments of £308m across all the funds, representing over half the latest valuation of £568m for this category. Presumably, these are spread over several years but there are undrawn borrowing facilities which can cover most of this amount.

The returns from this category have been very good and noticeably better than those Caledonia has generated recently from Private Capital.

What’s more, most of the latest fund valuations could be conservative. 84% by value are based on 30 June and the remainder are from 31 March.

I suspect the Private Capital strategy of buying large, direct stakes is too ingrained in Caledonia’s DNA to be ditched completely, but I’d be curious to know what discussions have taken place internally about using more UK and European private equity funds.

That big old discount

Caledonia has traded on a discount to net assets of between 15% and 25% for most of the time I have been invested in it.

Sometimes you think the discount is finally starting to narrow and then it whipsaws back out again.

Caledonia’s NAV is updated monthly. Its portfolio consists of one-third of prices that can be updated daily with the other two-thirds probably only updated every three or six months. So you often see the largest NAV moves on 31 March and 30 September when the trust presents its results.

When I originally purchased Caledonia, I was hoping the discount would gradually narrow over time and give a little kicker to my returns.

It’s safe to say that I’ve given up on that idea now.

The Cayzer family’s large holding means that significant share buybacks aren’t really feasible. Stock exchange rules mean a formal takeover offer is triggered if their holding exceeds 49.9%.

And although the board is able to buy back some shares, the last repurchase I could see was for £0.2m back in May 2018.

The large family stake also means you’re unlikely to see an activist investor come along and shake things up or a larger entity making a hostile takeover offer.

Caledonia also has a pretty low profile given its size. It rarely seems to pay for any broker research from the usual suspects, the Kepler report from 2018 linked in the Key Stats section above being the only one I found. The trust’s managers don’t seem to give many press interviews either.

The private equity element of Caledonia is also cited by many people as a factor.

The current sector discount for the AIC Private Equity sector is 17% but it’s probably around 20% if you strip out the outlier that is 3i. That’s pretty similar to Caledonia’s normal discount level.

However, it’s interesting to compare the discount experience of Caledonia with RIT Capital Partners. The latter is 50% larger and invests in a slightly wider range of assets such as hedge and credit funds.

The two trusts have performed very similarly over the last decade yet RIT has often traded at a premium. The Rothschild family stake in RIT is a bit smaller, at around 21%, but it rarely needs to do share buybacks.

I hold both trusts, with a similar size position in each. RIT just seems to have a little bit of magic fairy dust in eyes of most investors, because the family behind is better known and it had an excellent record in its early years before becoming somewhat more conservative.

A little gearing

Caledonia’s official gearing range is somewhere between 10% net cash and 10% net debt.

But it has rarely had any gearing over the past several years and even when it has, it’s only been 1-2% at most.

The trust had £115m of net cash in March 2020 and a very similar level in March 2019. A year before that it had £208m in net cash.

As of 30 September 2020, there was a small net debt position of £7m. But that’s negligible next to net assets of £2bn.

Caledonia has borrowing facilities of £250m in place, should it feel the need to get a little more aggressive or be required to put substantial amounts into its private equity funds.

£113m of these facilities expires in July 2022 and the remainder has just been renewed on a five-year term to May 2025.

Fully drawn, these facilities would result in gearing of 12-13%. That’s a little outside its +/-10% target range but still fairly modest.

Charges

Caledonia’s standard ongoing charge figure was 0.85% for the year to March 2020, which seems quite low.

Total costs came in at £17m for 2020 and £27m for 2019, with the latter higher due to a whole bunch of performance share awards.

I had a little rant about executive compensation in my last article on Caledonia so I won’t repeat the arguments in full again.

Suffice to say that the three executive directors receive a total of £1.5m in basic payments but this can more than treble to £4.7m if performance targets are met.

Some targets are based on personal objectives but the proportion based on the trust’s share price growth goes from a minimum of 3% pa and reaches its maximum level at 10% pa. For Jamie Cayzer-Colvin’s incentive scheme, the fund category performance has a range of 6% pa to 13.5% pa.

These don’t seem particularly onerous to me and a large proportion of the outcome is dictated by basic stock market movements, which the directors obviously have no control over.

The costs in the much-maligned Key Information Document come in at 2.43%, with a large part of the difference relative to the ongoing cost figure attributed to the underlying charges of the funds Caledonia invests in.

Skin in the game

With a collective holding of 48.5% worth some £800m, mostly held via trust, the Cayzer family are seriously invested here.

Outside of the trust, Wyatt has a direct holding of 1.1m (£33m) and Jamie Cayzer-Colvin owns 0.37m (£11m). The Chairman, a director since 2015, owns a more modest 4,072 shares (£120,000).

There are four independent directors who own 14,400 shares (£430,000) between them, which seems like a reasonable vote of confidence.

Caledonia has around 60 employees and its Employee Share Trust owns around 1% of the trust’s shares for subsequent transfer to employees exercising options or for awards under its bonus scheme.

In summary

I’ve blown hot and cold with Caledonia Investments for some time now.

I like the stability and long-term approach that comes from the large family holding. Staying in the game is the first and arguably only thing you need to do to ‘win’ at investing.

Yet it also means that the trust’s performance will rarely shoot the lights out and at times I may have to look wistfully at the massive gains made by the likes of Baillie Gifford and think what could have been.

Like many people, though, my base expectation is for a period of lower equity returns in the 2020s relative to the 2010s. That seems to be when Caledonia does best, so while I’ve been happy to trim my position, I am reluctant to sell out completely.

The high director costs are a little unsettling. They’re nothing new but seem pretty egregious given the value of the shares they hold.

And if the directors have performance targets, I think they should be relative to wider market returns. While I understand the trust targets absolute returns, with an all-equity portfolio like this the general direction of the market is a big factor.

The recent troubles in the Private Capital division are the only major misstep I can recall since I began investing in Caledonia nearly a decade ago. I don’t think it’s serious enough yet to warrant selling out completely but it’s something I am now watching a lot more closely.

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Hi IT Investor,

Like you a substantial holder of Caledonia. Thank you for your detailed, thorough review, much appreciated.

My feelings about this IT are similar to yours, I regularly consider selling and its latest positive move may give me the opportunity to do so.

What really caused concern was its lack of any defensive features when Covid struck. For a trust with modest ambitions, with questionable management targets and consequently high cost I’m wondering why I’m still a holder!

Why does it take a team of 4 to run the quoted pool when they hardly ever trade!

My original thoughts were that it was a similar offering to RIT and at a substantial relative discount and so it has proved but its wealth preservation features were really tested this spring and very much found wanting!

Kind regards

Mark

Thanks, Mark.

I think it’s tough for pretty much any trust’s share price to stand firm in routs like we saw in February and March of this year. It’s the price that has to be paid for having something that you can always buy and sell on the open market. Even stalwarts like Personal Assets and Capital Gearing saw their prices fall for a little while, as did many of the renewable infrastructure trusts.

Caledonia’s NAV fell about 12% from February to March and a lot of that was them having to do a “market overlay” as they called it as they didn’t have up to date figures for all their direct investments and PE funds. I think that’s pretty decent in the circumstances for a fund which is entirely equity-related (and not tech-focused).

RIT’s NAV performance has been a little better so far this year, as it didn’t fall as far in March 2020, but I would put that down to having less direct equity exposure.

However, although its NAV is about 5% ahead of Caledonia so far this year, as it has slipped from a premium to a discount, its share price performance has actually been a little worse!

Brilliant article. I have an emotional (I know, I know) attachment as they were an early monthly savings toe tip into the world of ITs back in the mid 90s. Ive held on and have invested for my childrens SIPPs as I feel the family will keep them around for the 50 years they need. Along with equal stakes in RIT, ATS and Law Debenture I keep an eye on other potential widows and orphans opportunities for them with Brunner coming to mind. Hansa is a new one for me though.

I’m sorry but I just don’t get it.

I’m all for managers and families who are aligned, but I think this is very different from a wealthy family who live off the dividends, which is what this feels more like.

There are so many more interesting ITs to choose from in all sorts of areas. To take a simple example, if you had 50% Capital Gearing (which I note has outperformed Caledonian over 3 and 5 years, with a lot less risk) and 50% Smithson (or Martin Currie Global Unconstrained etc.), you’d have a global, diversified portfolio with reasonable risk, aligned partners with integrity, reasonable fees, and a decent chance of superior performance.

I know it’s hard to sell things, and be sure you’re wrong (I’ve finally sold a few mistakes this year, after waiting far too long in case they came back). And I know the appeal of these families – I dabbled with Majedie when they reworked the portfolio, but decided that William Barlow doesn’t really know what he’s doing and the fees were overly generous.

Hey ho – I may be wrong though!

I had some Caledonia for a while but became bored of it and switched into some BG trusts which have since massively outperformed it. I am always a bit nervous of these semi-private ITs as my interests and those of the family/managers might not be aligned and I wonder whether a pals operation has the skills and contacts and knowledge to compete with the big boys. For PE I think there is better to be found elsewhere. Beating the FTSE is no great achievement. Possibly a keeper but personally I wouldn’t rate it as a buy. As someone once said Can’t Recommend A Purchase 😉

Thanks, J. I suspect I have an attachment to CLDN as well despite not being invested as long as you. And the same applies with me and RIT.

Hansa has had a rough decade as its largest holding in Ocean Wilsons, a LSE-listed Brazilian shipping firm, has been a big drag on its performance. Edison has done a number of notes on it which explains its strategy: https://www.edisongroup.com/company/hansa-trust-han/1756/

It’s probably even more quirky than RIT, ATST or CLDN though.

Well made points as usual Tom.

I think CLDN is actually ahead of both PNL and CGT over 3 and 5 years now, but not by a substantial amount and it’s definitely been more volatile. There’s clear water on a 10-year view, but you’d expect that given the amount of fixed-income that PNL and CGT have held throughout.

I’m happy with the position size I have with this (or will be once I ditch the non-ISA part). I have much more in quality growth (Lindsell Train, Fundmsith, Smithson, JGGI) plus small-caps and healthcare so I’m happy to hedge my bets a bit with a little CLDN/RIT on the side. As always, I reserve the right to change my mind should I run out of patience 🙂

Good piece. I have a similar issue with funds of this type albeit my largest IT holding is in RIT. There I forgive management as it provides access to PE and other assets (and hedge funds) mere mortals cannot own. But the big general ITs with a UK market focus have been marching like lemmings off the cliff for years. Trusts (or rather three legged dogs) like City of London etc need to go back to their Boards and make changes. The London market is hugely weak and even with a swing back towards value miners and oil and gas and iffy death science firms offering bombs and tobacco products just will not cut it. Tech in the UK in 2020 is a total disaster and the pipeline of home grown growth IT firms likely to IPO is almost non-existent.

As Marc Andreessen correctly stated ‘software is eating the world’. Until such time as the UK gets its ducks in a row (likely decades away) and enables people to build and scale tech firms money invested in the UK market is likely to seriously underperform the USA and China. These countries will continue to pull ahead and deliver the returns needed to at some point have a retirement pot.

Disclosure: Short FTSE. Long SPY, QQQ, China.

@Nick

Yes, Caledonia is certainly not the most exciting vehicle to hold – BG trusts are several times more lively! I think you’re right when you say to need to understand the family’s motivations if you want to hold this trust. They seem happy to grow gradually over time and to miss out on big gains if that means they avoid the worst losses. Not an approach that suits everyone and probably not a trust for someone in their 20s and 30s who is in a better position to take on a bit more risk.

Thanks, Arb. I’ve had a similar view of the UK market as a whole for a few years now. There are plenty of good companies but I don’t see banks, oil, and miners in particular as great places to have your money for the next two or three decades. They may spike occasionally but I have no insight into when.

That said, I did own a bit of CTY for a couple of years until last summer – still not really sure why I did that!

This is a great article. Well done.

I have held some shares in Caledonia for approximately 18 of the most turbulent months I have ever known and they are only slightly below what I paid for them which is good news. However, this is a long term investment and I very pleased to be invested in this Trust, given the track record on dividends and particularly given the discount to NAV, which provides a cushion. I am confident that in the medium term I will have no cause to regret the decision to invest in Caledonia.

Bye bye Buzz Bingo 🙁

Caledonia today (17/03/21) announced it has sold its stake, effectively for nil value, rather than participate in a further refinancing.

Caledonia Investments plc (“Caledonia”) announces that it has sold its shareholding in Buzz Bingo (“Buzz”) to Intermediate Capital Group (“ICG”) for a nominal amount. The Covid-19 crisis and the severe restrictions imposed by the Government on leisure sector businesses have led to Buzz’s clubs being unable to trade for much of the past 12 months. Buzz was refinanced in the summer of 2020 as part of a company voluntary arrangement, in which Caledonia invested £22m. However, the third national lockdown has resulted in a further requirement for new capital.

Caledonia, having carefully assessed the available investment opportunity, chose not to participate in the latest fundraising and has sold its shares to ICG which, together with Barclays, have provided further capital to Buzz. The investment in Buzz was valued at nil in Caledonia’s most recent net asset value statement as at 28 February 2021.

A full portfolio trading update will be released in early April, incorporating the year end valuations.

Thanks for the Buzz Bingo news which I had missed. Sale of the stake adds to my concerns over the quality of the trust’s private capital operation, and removes one of the reasons that was making me contemplate topping up my holding in CLDN. As the lockdown ends I had thought that CLDN’S exposure to two UK consumer facing businesses – Buzz and the Liberation pubs operation – might work to its advantage, especially as it appeared to be a patient long-term investor. Bingo does not fit my idea of a high quality asset. But neither were holiday parks, and CLDN did very well from them. Whereas a PE trust like HGCapital concentrates on areas, such as software related business, where it can add real value, it is far from clear where CLDN’s skills lie in this area of direct PE investment. Hopefully, this mistake might make CLDN’s board abandon its idea of playing as direct private equity investors and put CLDN’s money with professional PE fund managers.

@bill hall – I was finding it hard to get a handle on the success or otherwise of Caledonia’s P/E operations as well. They are all fairly sizeable so a couple of successes or couple of failures in quick succession can make quite a difference to their returns.

I have actually sold out of Caledonia completely in the last few weeks, taking the opportunity to build up my new position in Keystone Positive Change in its place after Keystone’s share price slipped back in line with all the other Baillie Gifford trusts.

Looking back, I held CLDN for nearly 10 years in total. It struggled initially but it had a pretty good run from mid-2012 to the end of 2019. However, in the wake of the pandemic, the share price is at roughly the same level it was at the end of 2016.

The 31 Mar 2021 NAV figure should be released very soon and that could see an uplift given that it’s the year-end number which should see updated values for all the unquoted holdings and some of the PE funds. So, I may regret my haste!

[Edit] NAV update this morning and the shares are up 6%!

https://investegate.co.uk/caledonia-investmnts–cldn-/rns/unaudited-net-asset-value-and-portfolio-update/202104090901239684U/