I’ve always had a soft spot for investing in smaller companies, aka small caps. It’s what many private investors cut their teeth on. What’s more, there’s decent evidence that such companies outperform the wider market. This phenomenon has even got a catchy moniker: the small-cap effect.

To keep things manageable, in this piece I’m going to look at what actually constitutes a small cap, what the small-cap effect is and why it might exist. In a subsequent piece, I plan to delve into some of the investment trusts that specialise in small caps.

It’s dark down there

There are hundreds of small companies that inhabit the depths of the London market and, to be frank, there’s an awful lot of dross down there, especially in the oil and mining sectors. Many of these companies will never make a profit and seem to be constantly raising fresh funds to keep the lights on for a little bit longer. They have destroyed the wealth of many private investors.

However, there are also many fantastic smaller companies. Some have a long history of generating cash for their investors, while a few young upstarts may even grow to become the blue chips of tomorrow.

I reckon investment trusts can be a smart way to get involved in small caps. They make it easy to spread your risk over dozens of tiddlers in one fell swoop. As an added bonus, they largely tend to avoid those troublesome oil and mining industries. That’s handy if you’re a sucker for a tantalising story presented by a slick management team. Not that I would ever fall into that camp of course!

What is a small-cap company?

There’s no universally accepted definition of what a small cap is. It’s normally just the smallest companies listed on any particular market, so what constitutes a small cap often depends on what country you are investing in.

In the UK, £500m or below is one yardstick. Some folks also separate out the real tiddlers, say £100m or below, into a separate category called micro-caps. However, in the US, a small cap could be as large as $2bn or even $3bn.

Let’s stick with the UK to keep things simpler. The FTSE indices provide us with a handy point of reference, and many small-cap investment trusts analyse their holdings this way. It’s worth knowing how they are made up, so we can get a better feel for exactly what we are investing in.

Playing FTSE

Stocks in the FTSE 100 index (the largest 100) are usually considered to be blue chips, while those in the FTSE 250 (the 101st to 350th largest) are regarded as mid-caps.

The FTSE SmallCap sits below these two indices and consists of the next 300 or so largest companies on the main market. These three indices combined make up the FTSE All-Share. There is also the FTSE Fledgling index, with 100 or so more companies.

Not all companies listed in London are included in these indices. Exchange traded funds (ETFs), split capital investment trusts and venture capital trusts are excluded, for example, as are those with a large proportion of their shares held by their directors, government bodies, other public companies and so on.

Obviously, share prices and therefore market capitalisations shift around all the time. Therefore, you’ll probably find that there are a number of companies in the SmallCap index that are larger than the bottom reaches of the FTSE 250. Every quarter, FTSE rejigs the indices to account for these movements, so a few companies will be promoted while others will be relegated.

The number of companies in the SmallCap (and Fledgling) isn’t fixed, unlike the FTSE 100 or FTSE 250. Each June, any share that is valued at 0.15% or more than the total value of the SmallCap index is added.

At the last count, the SmallCap index was worth £81bn, so companies valued at more than £120m could be eligible. In a similar fashion, any company that is 0.1% or below (about £80m) is at risk of being demoted from the SmallCap to the Fledgling.

Aim down low

So far, we’ve just considered the main London market. There is also the Alternative Investment Market (AIM), which is more lightly regulated. Shares listed here tend to be riskier. It’s arguably not quite as bad now as it was before the financial crisis, as many of the more speculative shares got minced by the credit crunch.

AIM once boasted some 1,400 companies, whereas it has about 800 today. It’s still where a lot of the high-risk oil, gas and mining stocks reside. AIM has around 200 of them in all, compared to around 60 on the main market.

But there are many good companies on AIM, so we wouldn’t want to rule it entirely when it comes to looking for small-cap candidates.

What do small-cap investment trusts invest in?

Here’s how the FTSE indices compared at the end of November 2018:

| Index | Number of companies | Total size | Max size | Min size | Average |

|---|---|---|---|---|---|

| FTSE 100 | 100 | £1,804bn | £133bn | £1.4bn | £18bn |

| FTSE 250 | 250 | £344bn | £4.7bn | £208m | £1.4bn |

| FTSE Small Cap | 286 | £81bn | £732m | £31m | £284m |

| FTSE Fledgling | 102 | £5bn | £161m | £0m | £45m |

| FTSE AIM All-Share | 807 | £60bn | £2.9bn | £0m | £74m |

One thing to be aware of is that the SmallCap and Fledgling indices have a lot of investment trusts in them. There are 128 in the SmallCap and about 50 in the Fledgling. The FTSE 250 has 54 investment trusts in its ranks. The FTSE 100 just the one.

As a group, small-cap investment trusts that specialise in the UK typically invest in everything but the FTSE 100. They generally don’t invest in other investment trusts and they largely avoid the highly speculative oil and mining sectors.

That still leaves us with nearly 1,000 small/mid-cap companies. Plenty of choice then, meaning that the performance of individual small-cap investment trusts can vary quite significantly.

Some funds will focus on the top end, i.e. companies valued at a few hundred million to a few billion. Other funds might just go for companies valued at £100m or below. These latter funds would have a much higher risk profile, as the smallest companies tend to be the most volatile.

A recent trend has also seen some investment trusts go for more concentrated portfolios of 20 holdings or less, rather than the more usual 50 to 100. This ups the risk ante further still.

Some folks also like a basket approach when it comes to small-cap investment trusts, picking a couple that invest in ‘larger’ small caps, perhaps combined with one micro-capper. However you invest in this sector, you definitely need to peek under the bonnet to see what you’re actually buying.

The small-cap effect?

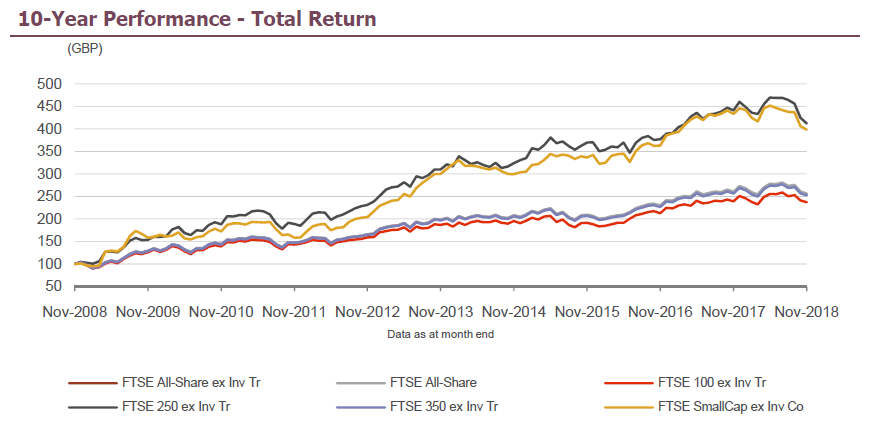

Google ‘small-cap effect’ and you should see a pretty long list of examples, both close to home and wider afield. Here’s one example, comparing the recent performance of the FTSE 100 to the FTSE 250 and SmallCap.

I like this chart as it demonstrates a few different things.

First, smaller companies have done a lot better this past decade, up 300% or so versus around 130% for the FTSE 100. The Fledgling has done even better — it’s up 500%!

Second, the SmallCap and FTSE 250 have performed very similarly, suggesting it does make sense to think about ‘larger’ small caps as well as tiddlers.

It also shows just how much the performance of the FTSE 100 dominates the FTSE All-Share. If you are investing in a plain vanilla UK tracker, it’s largely blue chips you are pinning your hopes on.

To get some small-cap action, you need a specialist fund. If index trackers are your thing, then there are six ETFs that track the FTSE 250 and one that tracks the UK MSCI SmallCap index (which is pretty similar to the FTSE 250 it would seem). For the active investors among us, there are around 20 investment trusts.

Quick to slide, quick to rebound

It’s important not to get carried away by these gains of course. These charts start in the depths of the financial crisis, flattering the final numbers considerably. As a guideline, small caps tend to fall further when the market declines, and then rebound more quickly.

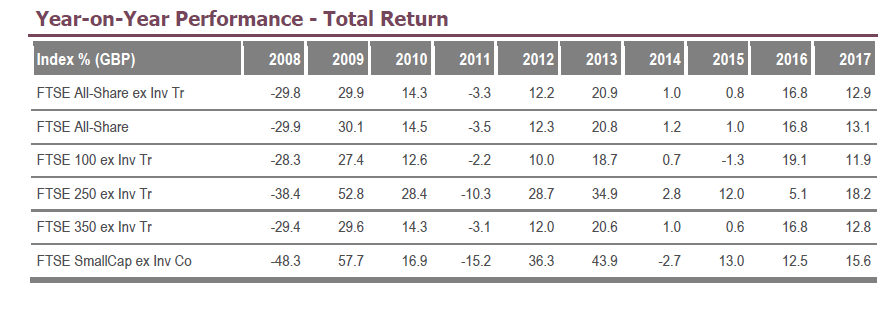

The SmallCap’s performance over the last ten years reflects this, with a harrowing 48% drop in 2008 followed by a spectacular 58% rebound in 2009. Generally, when the market has risen, the SmallCap has done better, and vice versa. Ditto for the Fledgling.

So far in 2018, before today’s 3% fall, the All-Share was down 7% compared to 12% for the SmallCap ex Investment Trusts.

There are many reasons why you would expect small caps to be quite a bit more volatile than the wider market. Small companies are generally considered to be more vulnerable to economic downturns. The loss of a few customers tends to hit them harder, they are often focused on a niche market, and they find external funding harder to obtain.

They tend to focus on their own domestic markets, and individual economies by definition will be more volatile than the global economy.

Often their shares are thinly traded, meaning it only takes a few people selling to make a significant dent in their share price.

The end of the small-cap bull run?

A question vexing some investors, including myself, is whether now is a good time to invest in small caps.

This bull market has gone on longer than pretty much anyone expected, but if recent falls turn into something a little nastier, small caps could be hit hard. Small-cap investment trusts might face a double whammy, with their discounts widening at the same time.

I’m no market timer, so I’m planning to hold my collection of small-cap investment trusts for a few decades if I can. Should the market take a nose dive, then I’d probably be looking to top-up in this sector. But I understand why some people might feel it’s worth waiting for a more attractive entry point.

Looking longer term

November’s Trustnet magazine has a good article from pages 2 to 7 covering more historical data on small caps.

For example, there’s the Numis Smaller Companies Index that covers the smallest 10% of the London market and dates back to 1955. It has returned 15.2% per annum since then, versus 11.8% for the wider UK market.

The article also highlights that small caps outperformed in 19 out of the 21 largest global markets from 2000 to 2017, by an average of five percentage points. Quite why small caps have done so well around the world is little less clear. In most cases, stock market gains come from a relatively small proportion of companies. That’s probably true for small caps, too, but their small size means that the potential gains they offer are just a little bit larger.

This article also points that UK small caps lagged the main market throughout the 1990s, with the decline of the manufacturing sector at this time identified as the chief suspect. Like all investing themes, there can be prolonged periods where the market sticks two fingers up at you, just because it can.

To sum up, small caps can be highly profitable for truly patient investors. But be prepared for them to scare the bejesus out of you along the way.

More on this topic: UK small-cap trusts & Global small-cap trusts

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.