I’ve just been listening to an FT podcast all about the idea of a Financial Room 101. The redoubtable Justin Urquhart-Stewart suggested we banish Junior ISAs from existence. They’ll either snort the proceeds, drink them, or spend them he said, or words to that effect.

I’ve got some sympathy with that view. And it’s not the first time I have heard something similar. Nevertheless, a few years back, I opened Junior ISAs for both our young children.

It’s more than a decade until they can get their sticky hands on the cash, so it’s a while until I’ll see whether Justin is right.

But one of the main reasons I did this was to force myself to teach them children about investing and other financial gubbins. So if they end up spending everything on their 18th birthday… well, then that will be my fault.

The quick and dirty on Junior ISAs

Junior ISAs are essentially just shrunken-down adult ISAs. They were introduced in 2011 and replaced the previous system of Child Trust Funds.

When your child turns 18 their Junior ISA automatically converts into adult ISA, although they can take administrative control when they are 16.

You can put in £4,368 for each child for the 2019/20 tax year and this limit generally rises at the rate of inflation each year.

Junior ISAs can be either cash or stocks & shares, just like the adult version. You can have one cash and one stocks & shares if you wish, as long as you contribute less than the annual limit each tax year.

With the exception of the relatively new Innovative Finance ISAs, I think you can pretty much invest in the same range of things available for adult ISAs. But I’m hoping there aren’t too many Junior ISAs stuffed full of ultra-risky AIM oil exploration firms!

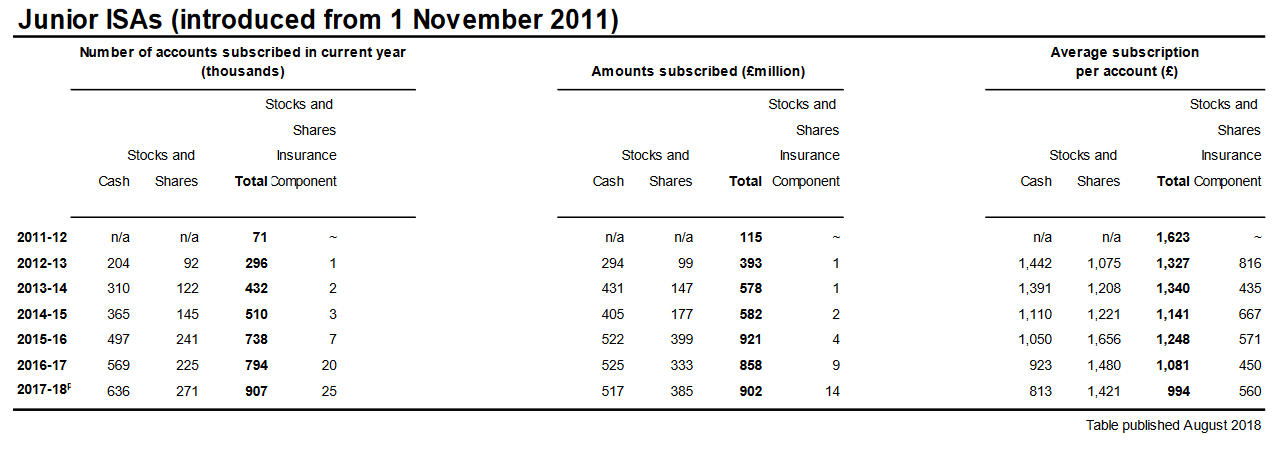

Some Junior ISA stats

There isn’t a massive amount of information available on Junior ISAs but here are some summary figures (click to enlarge):

In 2017/18, we can see that fresh money was added to nearly 1 million Junior ISA accounts. The average subscription level was around £1,000.

It’s great to see how much they have caught on. Triple the number of accounts were subscribed to in 2017/2018 compared to five years earlier.

I think there are around 14 million children in the UK. Nearly 1 million contributing in a single year is a significant percentage, although there could be some double-counting in there with some children having both the cash and stocks & shares versions.

Less encouraging is that the amount of new money invested has remained at £0.9bn for the last three tax years.

As of April 2018, Junior ISAs were worth a collective £4.15bn. Of that, £1.85bn was in stocks & shares and £2.3bn was in cash.

Half a dozen Junior Cash ISA accounts currently offer 3% or more, but I think more parents should be investing these accounts. Keeping too much money in cash is far riskier than investing in the stock market over the timeframes we are looking at here.

Choosing a provider

You seem to be able to open stocks & shares Junior ISAs with most major brokers these days. And there are a few specialist providers as well.

Charges are normally the same as adult ISAs. Because of the smaller sums involved, percentage fees usually work out cheaper than fixed monthly charges.

Right now, annual fees typically range from 0.15% to 0.45%. The minimum monthly and lump-sum amounts vary quite a lot, too.

I have to confess I ended up at the more expensive end. I won’t name them explicitly but let’s call them Largreaves Hands Down.

What to invest in

Like many folks, while I am happy to take some active risk with my own investments, I tend to be more cautious when making decisions for others.

That means I’m sticking to passive investing for now. I may switch to some investment trusts at a later stage, especially if my children show more interest.

To begin with, though, I wanted an investment that can continue on its merry way without any monitoring, should something happen to me.

That means a fairly narrow choice of the larger fund providers and their global tracker offerings. In the interest of mixing things up a bit, I went for Fidelity Index World which charges just 0.12% a year.

Of course, admin fees take the effective annual charge up to nearly 0.6%.

I can live with that for now, but I’m not averse to moving providers at a later stage if the sums add up. Now that exit fees seem to be on the way out, that’s becoming easier to do.

Playing fair

I decided to put equal amounts in for both children at the same early age. It’s been a good few years for global equities so the eldest is up nearly 60% and the youngest about 25%.

I opted for a couple of lump sums rather than setting up regular monthly contributions.

Here the thinking was that I didn’t want to invest too much: I want the amount when they turn 18 to be meaningful but not too tempting! Lump sums gave me a bit more control over that.

If we assume global equities return around 5-6% above inflation over the full 18 years then the spending power of our initial contributions could increase by 2.5 to 3 times.

I used 3 times to make a very rough estimate of what the actual figure might be when they turn 18.

I’m going to encourage them to keep as much invested as possible, and I might even add a bit more if they do. But I expect at least some of it will go towards funding a house deposit or getting them through university.

If they do spend it, my plan involves lots of sulking and a few beers (for me, not them). But it is their money and I do want them to be responsible for what they do with it.

Alternatives to Junior ISAs

Junior ISAs aren’t the only way to go of course. You can open taxable accounts in a child’s name or even Junior SIPPs.

I plumped for Junior ISAs rather than a SIPP as I wanted to see them benefit from the money while I still had a few marbles left. Plus, I suspect the ISA regime is marginally less likely to be fiddled with by the government.

You do get more control with a taxable account but I’ve learned from my own investments how valuable ISAs can be as tax shelters.

Even though you might not think you’ll benefit when you first set them up, it’s amazing how investments can compound over the sort of timeframe we’re looking at here.

When to tell them

As I wrote this piece, it occurred to me that the one thing I haven’t really worked out is when to tell them about their Junior ISAs.

I guess you could hide the post from them, given how late most teenagers tend to sleep. But that doesn’t seem right.

We’re just introducing pocket money for the eldest now, so I see that as the first step in this process.

They both have savings accounts as well, which they don’t know about either. That will probably be stage two.

And I guess once we are happy that’s not been an unmitigated disaster then the grand unveiling of the Junior ISAs can take place!

Disclaimer

Please note that I may own some of the investments mentioned above -- you can see my current holdings on my portfolio page.

Nothing on this website should be regarded as a buy or sell recommendation as I'm just a random person writing a blog in his spare time and I am not authorised to give financial advice. Always do your own research and seek financial advice if necessary!

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.

Thank you for interesting article. I think Mr Justin Urquhart-Stewart is wrong. I think instilling in children at an early age:

– saving

– an interest in stocks

– the wonders of compounding

As for them blowing on blo, that does not say much of his opinion about his children or children in general. I have every confidence that my son won’t.

I invest his child allowance each year:

I started with BRK.B and he is now in BVXP, BDPERS, FUQUIT, JPM and DIS

I’ve opened JISA’s too. This is partly to educate my children about investment, but I am still working on how to fully communicate with them on this.

I therefore hope that Justin is wrong!