I am a numbers guy, so I love to crunch data to get a feel for a topic. Luckily, numbers are one thing that the investment trust industry has in spades thanks to the excellent data made available by its trade body, www.theaic.co.uk.

Here’s a whistle-stop tour of some of the key numbers that help define the world of investment trusts.

How many?

As of June 2018, there were 402 different investment trusts. You can download the latest list here.

One thing I like about the investment trust industry is that the number of funds is fairly stable over time. You don’t tend to get funds or managers rushing in or out of the sector. Over the last ten years, the total number of investment trusts has varied from about 450 at its peak in 2008 to a low of about 385 at the end of 2016.

Most of the investment trust industry is made up of what are known as conventional investment trusts. There is also a subset of venture capital trusts — these offer certain income and capital gains tax advantages (but mainly if you subscribe for new shares, rather than buying them on the stock market). There are 67 venture capital trusts at the moment, so they account for one in six investment trusts.

How domestic?

While all venture capital trusts are domiciled in the UK, about a third of conventional investment trusts are domiciled offshore.

But they aren’t that far offshore, with the vast majority (90% or so) being based in either Guernsey or Jersey. There are a few each that are based in Bermuda, the Cayman Islands, Luxembourg, and Ireland, plus a few other countries with one apiece.

How big?

The total market value of the investment trust industry is around £160bn. That makes it less than one-seventh the size of the mainstream fund sector (unit trusts, open-ended investment companies etc) which is worth in excess of £1,200bn. I don’t have figures for the UK ETF market, but it’s probably somewhere in the middle of the two, given there are over 1,000 UK ETFs now and 500 or so ETCs/ETNs.

The biggest investment trust is 3i, which is valued at £8.7bn, while Scottish Mortgage takes the second spot with £7.5bn. These are the only investment trusts that are large enough to be included in the FTSE 100 index right now. I believe both Alliance Trust and Foreign & Colonial have been members of the FTSE 100 in the past, though.

‘Big’ investment trusts are pretty rare, as there are currently only eight investment trusts valued at over £2bn and a further 28 valued at between £1bn and £2bn.

The average value for conventional investment trusts is about £470m, and there are 30 valued at less than £30m. Venture capital trusts tend to be much smaller, with an average market value of around £60m.

I think size matters, as I would be hesitant in buying into a very small investment trust as there could be liquidity issues (meaning it’s hard to buy and sell in any significant volume).

On the flip side, larger investment trusts can find it harder to grow quickly, as they have to spread their portfolio over a larger number of positions. But it’s worth remembering that, for the most part, these investment trusts have become large by being successful for a long period of time.

Most new investment trusts seem to come to the market with a value of £100-200m. See this article for my quick look at which new investment trusts that have joined the market since the start of 2017.

How old?

Another key attraction for me when it comes to investment trusts is the length of time many of these funds have been in existence. The oldest is Foreign & Colonial, which celebrated its 150th birthday earlier this year.

In all, there are now 25 investment trusts that date back a century or more. Most of these veterans are more generalist in nature, and they can be found in the global and UK equity income sectors in particular. But there are a few well-weathered specialist funds such as Henderson Smaller Companies (1887), JPMorgan American (1881) and TR Property (1905).

How indebted?

One thing that differentiates investment trusts from other funds is that they can use borrowing. In long bull markets, like the one that we’re presently enjoying, this can provide a useful kicker to your returns. When asset prices fall, the reverse can be true of course.

Right now, the average gearing level across all investment trusts is 7%. Many funds have no borrowings at all, but it’s pretty common to see higher levels of debt in income-orientated funds, and especially property funds.

Most trusts have a gearing range, with 0-20% being fairly typical, so that gives you a fair idea of what to expect when it comes to their attitude towards borrowing.

How costly?

Investment trusts used to have a reputation for being cheaper than other funds, but the rise of passive investing and moves to clean up the wider investment industry (such as the Retail Distribution Review) means that no longer may be the case.

The average investment trust charge is 1.35%, rising to 1.53% if you add in performance fees as well.

How cheap?

Shares in investment trusts are bought and sold on the stock market like individual companies, so their prices go up and down according to supply and demand, and often differ from the underlying value of the assets they hold.

Funds that trade at a higher value than their underlying assets are said to trade at a premium, while the reverse is called trading at a discount. An investment trust’s premium or discount will vary over time, as does the average across the entire industry.

At the moment, the average discount is 3%, and about two-thirds of conventional investment trusts trade at a discount. However, many of the larger funds that are popular with private investors trade at small premiums, and you can see premiums of around 10% for income-orientated funds in specialist sectors.

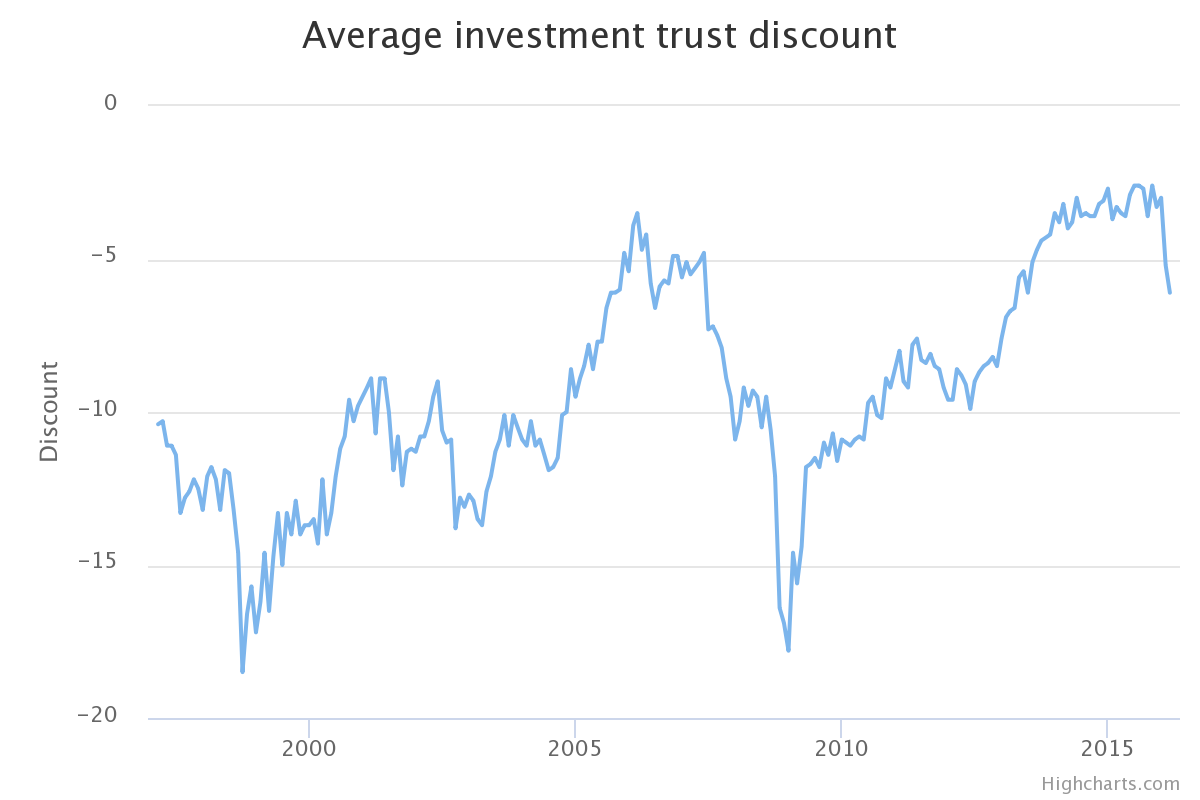

The chart below shows how the average investment trust discount has moved over time.

As you can see, discounts have generally narrowed over time, and have continued to do so since this chart was created.

It also shows how savagely discounts can increase when markets suffer a setback, as they did in 2008/09 for example. Generally, this effect is short-lived, but it’s definitely worth being aware of the fact that holding investment trusts is not for the faint of heart.

As well as discounts widening and the underlying investments they hold falling in value, the gearing effect can mean that investment trust share prices can be hit three ways in times of trouble. So, if you tend to sell during market panics (top tip: generally a bad idea), then investment trusts may not suit you.

How come?

Now, you might think that I’ve left one key number out of this article, and arguably the most important one of all. And that’s how well have investment trusts performed.

I think this topic deserves a fuller examination, especially with respect to how well investment trusts have performed against other types of fund, so I plan to cover that in a forthcoming article.

Of the investment trusts listed in this article, I hold Henderson Smaller Companies.

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.