As First World problems go, paying exit fees on your investment account must rank pretty highly. But ultimately, as more and more of us invest, it is important that the charges we incur are both fair and transparent. And broker exit fees, in many cases, seem to be neither.

When fees fell

I still remember having to call my broker when I wanted to buy or sell an investment back in the 1980s and 1990s. I think I used to pay about 1.5% to 1.75% of the deal value for the privilege… with no cap. A decent-sized investment might cost in excess of £100 in commission charges.

Then came the Internet, and transaction fees began to tumble. They seem to have bottomed out at around £10-£12 per deal, although you can get cheaper rates if you are a frequent trader or prepared to set up a regular investment plan.

Then came the RDR review in 2013, which forced brokers to re-examine their fee structures. Quite radically in many cases. Interactive Investor broke ranks first, if I recall, introducing a £20 quarterly fee. Many brokers followed, and it’s now fairly rare not to have some sort of administration charge. Some are flat fees, while others are percentage based.

Then brokers began to merge. Suddenly, lots of people were facing a completely different set of investment charges from when they initially signed up. This brought exit fees into sharp focus for many of us, and it wasn’t a pretty sight.

Most people choose their broker on the basis of the dealing and regular administration charges. By looking at the size of your portfolio and how frequently you trade, you should be able to make a reasonable stab at what a broker might cost you over the course of a year.

Exit fees lurked in the background, and as far as I know haven’t really changed that much in the past few decades. You probably looked at them before you signed up, but you didn’t pay them that much attention at the time.

Exit fees unmasked

Look at an online resource, like the excellent broker comparison tool at Monevator, and you can see that exit fees are commonplace.

£25 per holding seems to be the most typical charge, with a sprinkling of £10 and £15, and the odd zero. Some firms set a maximum, such as £125 or £250, but many have no cap.

We’re all taught to be properly diversified, of course. This means a typical portfolio with 15-20 holdings could easily cost you £375-£500 to move elsewhere.

Moving cash is usually free, so you could sell your investments and then buy them back again. But that means you need to pay two lots of trading charges, stamp duty, and suffer the buy-sell spread. You also risk the underlying investment moving against you while you transfer over the cash to your new broker. Oh, and you might create a capital gains tax liability as well!

Why so serious?

It seems bizarre to me that it costs £10 to buy or sell an investment, but often more than double that to transfer one you already own.

While it’s unclear how much the switching process costs the providers themselves, the wide variation in fees suggests firms aren’t merely covering their own costs. And Hargreaves Lansdown, probably the most cost-efficient operator in the market, charges the full £25 per holding plus £30 on top to close your account as a final clip round the ear for daring to go elsewhere.

In recent years, free switching has become a cornerstone of consumer finance. Whether it’s your bank account, broadband operator, or energy supplier, switching is usually free these days. We’re always encouraged to look for a better deal. It helps us save money and provides an incentive for firms to become more efficient. Exit fees on investment accounts stick out like a sore thumb in this regard.

There’s been increasing press coverage of this topic in recent months. That’s encouraging, as that can help build the pressure and ultimately lead to real change. It happened with PPI, for example, although regrettably, it took several years.

Transfer tales

In practice, I have tended to avoid exit fees by gradually moving between brokers over an extended period of time. I’d buy any new investments with my new provider, and gradually sell down positions in my old one. It’s not that efficient of course, and it’s not something you should have to do.

Every now and again, you used to see ‘new customer offers’ with incentives that covered the cost of switching, and I have used those in the past. But they seem to be quite rare these days.

I’ve spoken to some people in the industry over the years, and my understanding is that a surprising amount of the switching process is still done manually. Even if one side has fully automated systems, if the other side is still paper-based when it comes to switching then that doesn’t really help.

I actually transferred a SIPP earlier this year and that actually went remarkably smoothly, taking just a few days. But you hear tales of transfers taking weeks or even months to complete. ISAs tend to be worse than ordinary dealing accounts, and SIPPs are the pits it would seem. Perhaps I just got lucky with mine.

Of course, it’s not in the interest of the broker you’re switching from to speed things up. To be fair, there can be added complications that aren’t immediately apparent. Dividends might be received by your original broker long after the underlying investment has moved to a new home. Some funds have many different share classes, and your new broker may not offer the one you currently hold.

The FCA gets radical

As part of its ongoing study into investment platforms, it was heartening to see that the FCA is considering a ban on exit fees. An interim review was published last month, with final recommendations expected in early 2019.

Here’s a snippet:

7% of consumers in our research say they have attempted to switch at some point but failed to do so. Consumers note significant actual and perceived barriers to switching – that the switching process is too long or complex and that they have to pay exit fees.

These are the same issues that firms themselves say affect the switching process and timelines. The lack of standardisation of the switching process, the number of parties involved, the complexities around the specifics of switching various product wrappers and underlying investments are all impacting consumers’ experience and ability to switch, raising barriers to switching.

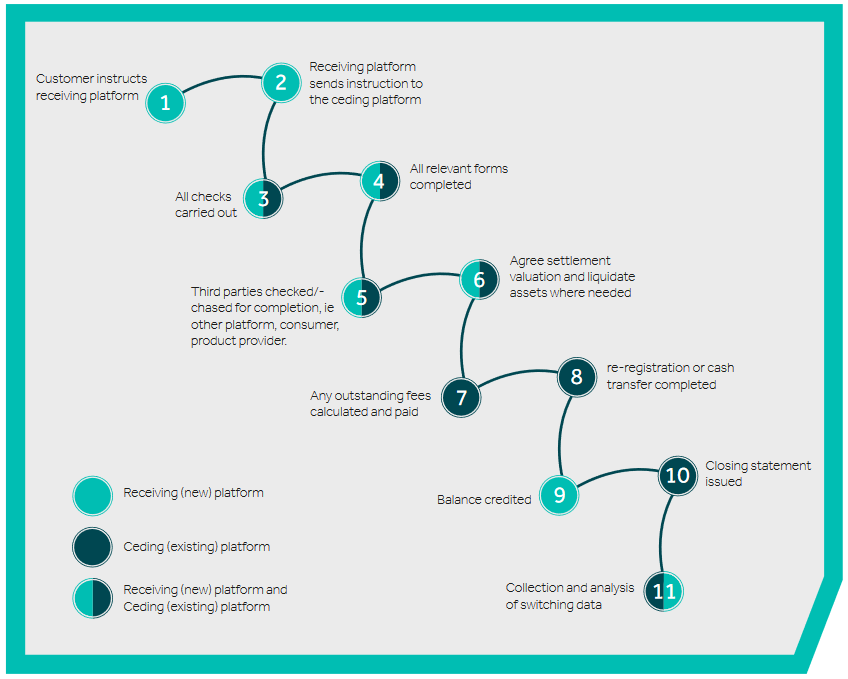

And there was this image illustrating the various iterations the process goes through. The back and forth is considerable, much like conveyancing when you move house.

The FCA also revealed that exit fees only account for 0.17% of total fee income.

Now, that number might be so small because so many people are deterred from switching in the first place. But it suggests a ban on exit fees may not mean a large increase in regular fees occurs to replace any lost income.

The interim report also revealed that there isn’t much evidence of these investment platforms making out like bandits while they mind our money. Among the main providers, there was a roughly equal mix of profitable firms, those breaking even, and loss makers.

Let’s hope the FCA has the courage of its convictions and decides to switch off exit fees for good in early 2019.

Subscribe to IT Investor

Get an email alert every time I publish a new article. Your email address won't be used for anything else.